Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Trying to pin down the exact amount of super you need for retirement can feel like shooting at a moving target. The Association of Superannuation Funds of Australia (ASFA) offers a helpful starting point: they suggest a goal of $595,000 for a single person wanting a 'comfortable' lifestyle, and $690,000 for a couple.

But these are just benchmarks. They're useful signposts, but they don't tell the whole story of your personal retirement journey. Your unique vision for the future is what will truly define your 'magic number'—and our process at Wealth Collective is designed to help you calculate and achieve it.

Setting the Benchmark for Your Retirement Savings

When people ask, "how much super do I need?", what they’re really asking is, "how much money do I need to live the life I want after I stop working?". The ASFA Retirement Standard is the most recognised guide in Australia for answering this because it splits retirement into two clear lifestyle categories:

-

A Modest Retirement: This covers all your basic needs with a simple, no-frills lifestyle. It’s a step up from relying solely on the Age Pension and allows for some simple leisure activities.

-

A Comfortable Retirement: This is what most of us picture. It supports a better quality of life, letting you enjoy more dining out, travel, private health insurance, and the freedom to pursue hobbies without worrying about every dollar.

It's important to know these benchmarks assume you own your home outright and are in reasonably good health. They take the vague idea of "retirement" and turn it into a concrete financial goal.

Here's a quick look at the ASFA targets. This table shows the lump sum needed at age 67 to support the annual income for each lifestyle.

| Lifestyle | Annual Income (Single) | Super Needed (Single) | Annual Income (Couple) | Super Needed (Couple) |

|---|---|---|---|---|

| Modest | $32,666 | $100,000 | $46,494 | $100,000 |

| Comfortable | $51,278 | $595,000 | $72,148 | $690,000 |

These figures give you a clear target to aim for, but how do they stack up against reality for most Australians?

Comparing Australian Averages to Retirement Targets

It's one thing to see the target, but another to know how you're tracking. Projections show the average Australian man aged 60-64 has around $358,000 in super, while the average woman has $278,000.

Even if a couple combines their balances, they might still fall short of the $690,000 ASFA recommends for a comfortable retirement. You can find out more about how these retirement savings figures compare with long-term goals.

This gap highlights a critical point: average is just that—average. Your life and goals are anything but.

A generic number is a good starting point, but a personalised plan is what secures your future. The difference between an average retirement and your ideal retirement is found in the details.

Why Your Magic Number is Unique

While industry benchmarks are a fantastic guide, they can't factor in what makes your life, well, yours. Your perfect retirement number is deeply personal.

To get closer to your real number, ask yourself:

-

Will I still be paying off a mortgage or renting?

-

Do I have big travel plans or expensive hobbies I want to fund?

-

Do I plan on helping out my kids or grandkids financially?

-

What’s my personal comfort level with investment risk?

Answering these questions is the first step in moving from a generic benchmark to a meaningful, personal target. It’s where genuine financial planning begins, and it’s the exact starting point of our Retirement Roadmap service—helping you translate these guidelines into a practical strategy built for your unique life.

Defining Your Ideal Retirement Lifestyle

The industry benchmarks are a great start, but they don't capture the most important part of the equation: what retirement actually means to you. The question "how much super do I need to retire?" is less about hitting a generic number and more about funding a life you’re genuinely excited to live.

This is where we must move past vague labels. What does ‘comfortable’ really look like in your world? Is it trading the city grind for a sea change? Or is it staying put to be close to the grandkids, helping with their school fees, and enjoying regular dinners out?

Your vision is the true foundation of your financial plan. Without it, you're just chasing a number on a spreadsheet.

From Vague Ideas to a Tangible Vision

To bring your retirement vision into focus, you have to think in terms of real-world activities and expenses. It's a fun exercise in imagining your ideal week, month, and year once you've stopped working.

This process is a core part of how our advisers at Wealth Collective help clients define their 'wildly successful financial life'—it’s all about translating personal dreams into a precise, achievable target.

Let's break down what different lifestyles might actually involve:

-

The 'Modest' Lifestyle: This is about covering all the essentials without financial stress. You’d own your car, take a local holiday each year, and afford simple pleasures like a weekly coffee with friends. It’s a secure life, but big-ticket items would require serious saving.

-

The 'Comfortable' Lifestyle: This offers much more breathing room. It might mean flying overseas for a holiday each year, upgrading your car without worry, and dining out a couple of times a week. You can afford good private health insurance, pursue pricier hobbies, and generally live without pinching pennies.

Which of these sounds closer to what you have in mind? Or is your ideal retirement a unique blend of the two?

The goal isn't just to stop working; it's to start living the life you've been working towards. Defining this lifestyle is the most critical step in determining how much super you actually need.

Questions to Define Your Retirement Budget

To paint a clearer picture, it’s time to get specific. Thinking through these questions will help you build a much more realistic financial snapshot of the future you want.

-

Home and Living: Will your mortgage be paid off? Are you dreaming of any major renovations? Do you plan to downsize, or perhaps buy a caravan and hit the road?

-

Travel and Hobbies: How often do you really want to travel? Are we talking weekend getaways, or are month-long European adventures on the bucket list? What hobbies will you finally have time for, and what do they cost?

-

Health and Wellbeing: Do you want top-tier private health insurance? Will you need to budget for ongoing medical care or even potential aged care down the track?

-

Family and Giving: Is helping out your kids or grandkids financially part of the plan? Do you want to be in a position to leave a meaningful inheritance?

Answering these questions does more than just help you build a budget. It transforms the vague concept of 'retirement' into a vibrant, motivating picture of your future.

Once that picture is crystal clear, calculating your personal superannuation target becomes a much more straightforward exercise. This clarity is the very first thing we establish in our Retirement Roadmap service, because it ensures your entire financial plan is built around what truly matters to you.

The Key Factors That Shape Your Retirement Number

So, you’ve started dreaming about your ideal retirement lifestyle. That’s the fun part. Now we need to look at the financial forces that will shape your journey. Your personal retirement number isn't just about funding your hobbies; it’s also shaped by the Age Pension, how long you'll live, inflation, and healthcare costs.

Getting a handle on these factors is non-negotiable for anyone serious about figuring out exactly how much super they'll need.

The Age Pension: Your Financial Safety Net

The Age Pension is the foundation of retirement income for many Australians. It's a critical safety net that ensures a basic standard of living, but it was never designed to fund a 'comfortable' lifestyle on its own. However, it can dramatically reduce the heavy lifting your super has to do.

Eligibility for the Age Pension is based on income and assets tests. Depending on your super balance and other assets, you might get a full pension, a part pension, or nothing at all.

A common myth is that you need to run your super down to zero to get the Age Pension. The reality is far more nuanced. A smart retirement plan often uses super to top up a part pension, making your own savings last much longer.

Understanding how your super and the pension can work together is a game-changer. A strategy that intelligently combines them can seriously lower the lump sum you need to accumulate.

Longevity: The Blessing That Requires a Bigger Nest Egg

The good news is, we’re living longer than ever. A 65-year-old Australian man today can expect to live to 85, and a woman to nearly 88. The financial catch is that your retirement savings need to last for 20, 30, or even more years.

This is what we call longevity risk—the very real danger of outliving your money. A nest egg that looks fantastic at age 67 might feel thin by age 87. This is precisely why building a robust super balance is so crucial. It’s not just for the early, active years; it’s for providing security deep into your later years.

Inflation: The Silent Erosion of Your Savings

Inflation is the simple fact that the cost of living goes up, meaning the dollar you save today will buy less in the future. A retirement plan that ignores inflation is doomed to fail.

If your retirement savings aren't growing faster than inflation, you're actually going backwards. Your purchasing power shrinks every year. This is why your super has to be invested wisely, not just parked in a cash account. A sound investment strategy is designed to deliver growth that outpaces inflation, protecting the real-world value of your savings.

Healthcare and Aged Care: The Underestimated Costs

As we get older, our healthcare needs increase. Many retirees prefer the choice that comes with private health insurance, and these premiums, along with out-of-pocket costs, can become a major drain on your budget.

Then there's the potential need for aged care. Whether it’s help at home or residential care, the costs can be enormous and are often overlooked when planning for retirement. Building these potential expenses into your super target provides a vital buffer. Protecting against these kinds of risks is a core focus of our Guided Growth service.

These factors help explain a confidence gap many Australians feel. While our super system is admired globally, recent analysis shows only half of us feel ready for retirement. This is exactly the gap that expert financial planning is designed to close.

A Practical Guide to Calculating Your Super Target

Alright, we’ve covered the big ideas. Now it’s time to roll up our sleeves and put a number on it. This is where the dream of retirement starts to become a concrete plan.

There’s a straightforward way to get a solid first estimate of the super you’ll need. It’s all about figuring out your annual spending, seeing what the government might chip in, and then working backwards to find your magic number.

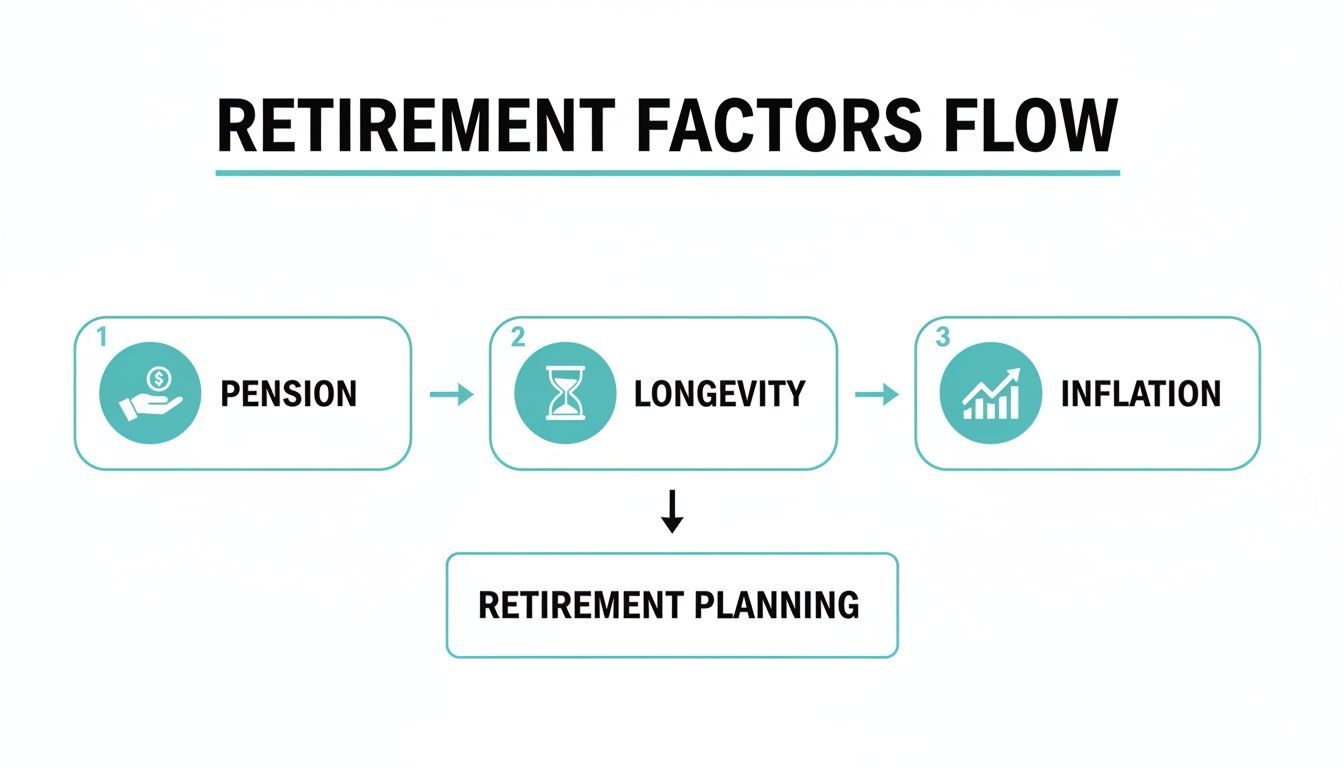

This simple diagram shows how the external forces we talked about—the pension, longevity, and inflation—all influence your retirement number.

They're all connected. Your target is directly linked to how much pension you might get and how hard your money has to work to keep up with rising costs over many years.

The Back-of-the-Napkin Formula

The goal of this exercise is to calculate the income gap your super has to fill each year.

Here’s the basic four-step calculation:

-

Estimate Your Annual Retirement Spending: How much do you need each year to fund your desired lifestyle?

-

Subtract Your Expected Age Pension: Deduct any government pension you think you’ll be eligible for.

-

Calculate Your Annual Income Gap: This is the amount your super needs to generate for you each year.

-

Determine Your Super Target: Multiply your annual gap by 25.

That final "multiply by 25" step is a shortcut based on a well-known retirement planning guideline: the 4% rule.

What Is the 4 Percent Rule?

The 4% rule is a classic rule of thumb in retirement planning. It suggests you can safely withdraw 4% of your total investment balance in your first year of retirement, and then adjust that amount for inflation each year after that. Following this has historically given people a high chance of their money lasting for 30 years or more.

So, if you retired with a $1,000,000 super balance, this rule says you could comfortably draw an income of $40,000 in your first year.

The 4% rule is a guidepost, not gospel. It's a fantastic starting point, but market conditions or a more cautious approach might mean a lower withdrawal rate—say, 3.5%—is a safer bet. Getting this drawdown strategy right is a critical part of ensuring your money outlasts you.

Putting It All Together: Retirement Calculation Examples

Let's see how this works in the real world. The table below shows how different goals create wildly different superannuation targets.

| Client Profile | Desired Annual Income | Assumed Age Pension | Net Income Needed from Super | Estimated Super Target |

|---|---|---|---|---|

| Young Pro Couple (35) | $80,000 | $20,000 (Partial) | $60,000 | $1,500,000 |

| Exec Nearing Retirement (55) | $120,000 | $0 (Ineligible) | $120,000 | $3,000,000 |

| Small Business Owner (60) | $65,000 | $29,000 (Full Single) | $36,000 | $900,000 |

As you can see, there's no "one size fits all" number. Your answer is completely tied to your personal vision and financial reality. The young couple has time on their side, while the executive needs to make aggressive contributions. The business owner can integrate the pension as a key part of his income stream.

While this calculation is a brilliant starting point, a truly solid financial plan must stress-test these numbers against tax, fees, and market swings. This is exactly what our Guided Growth service does, turning rough estimates into a detailed, robust strategy.

To get started on your own numbers, a great first step is to complete our initial fact-finding questionnaire.

Common Retirement Planning Mistakes to Avoid

Knowing what to avoid on the path to retirement is just as important as knowing what to do. A few seemingly small missteps can quietly snowball over the years, taking a huge bite out of your final nest egg.

Many people get their investment mix wrong at the wrong time. A young person playing it too safe with a cash-heavy fund leaves decades of powerful growth on the table. Conversely, someone near retirement with an overly aggressive portfolio risks a market downturn that could slash their balance right when they need it most. It’s all about striking the right balance for your stage of life.

The Hidden Costs of Inaction and Fees

Another huge mistake is underestimating the slow bleed from high super fees. A difference of just 1% in annual fees might not sound like much, but over a 30-year career, it can quietly siphon hundreds of thousands of dollars from your final balance.

Just as costly is the ‘set and forget’ approach. A classic oversight is failing to switch your super from the accumulation phase to the tax-free pension phase once you stop working. It's a simple step, but missing it means you're needlessly giving a chunk of your own money to the tax office every year.

A critical part of a solid retirement plan is avoiding these unforced errors. Simple mistakes like staying in the wrong super phase or paying unnecessarily high fees can cost you tens of thousands of dollars over your retirement.

The Real Cost of Sticking with the Status Quo

Failing to make that tax-efficient switch is a far more common—and costly—problem than you might think. Recent reports found that some new retirees could lose as much as $136,000 over their retirement just by leaving their funds in taxed accumulation accounts.

It is estimated that 700,000 Australians over 65 who aren't working full-time are paying extra tax each year, all because they haven't shifted into the tax-free retirement phase. You can dig deeper into how these administrative oversights impact retirement savings on wealthlab.com.au.

It just goes to show how much proactive management and good advice really matter. At Wealth Collective, our process is designed to help you sidestep these exact kinds of costly errors. We ensure your strategy matches your stage of life and that critical transitions are handled correctly, making sure your money is working as hard as possible for you.

So, What's Next on Your Retirement Journey?

Understanding the numbers is a fantastic start. But the real progress happens when you turn that knowledge into a solid action plan. This is where you swap theory for reality and start building a strategy that will secure your future.

A generic "how much super do I need?" figure is a good starting point, but it's the personalised strategy that truly builds wealth and peace of mind. Your journey to feeling confident about your financial future can start with one simple chat.

Let's Build Your Personal Plan

The path forward shouldn't be overwhelming. Instead of getting bogged down in endless numbers, the key is to take one manageable step at a time. The aim is to build a plan that is uniquely yours.

A great retirement plan isn’t about restriction; it’s about freedom. It gives you the confidence to spend your money on what brings you joy, because you know your future is looked after.

This is where expert guidance can make all the difference. We help connect all the pieces of the puzzle—your lifestyle goals, your investment approach, and how to make the most of the Age Pension—into one cohesive roadmap. Our Retirement Roadmap service is designed to give you exactly that clarity.

To see how this all comes together, have a look at our guide on creating a comprehensive retirement roadmap.

Book a Complimentary Chat

The best way to figure out how much super you really need to retire is to talk it through with an expert. We can help translate your vision for retirement into a clear, achievable financial target.

We invite you to book a complimentary, no-obligation 10-minute call with our team. In this quick chat, we can help you get clearer on your retirement goals and show you how our process can help you get there.

Your Superannuation Questions Answered

It's completely normal to have questions when planning for retirement. Let's tackle some of the most common ones we hear from our clients.

When Can I Actually Get My Hands on My Super?

Generally, you can access your super once you hit your 'preservation age' and you’ve officially retired. Your preservation age is set by the government and falls between 55 and 60, depending on when you were born.

A key milestone to remember is that once you turn 65, you can access your super money whether you're still working or not. It's crucial to get these rules right, as dipping in early can come with hefty tax penalties.

Can I Get By on the Age Pension Alone?

For most people, the honest answer is no—not comfortably. The Age Pension is a safety net designed to cover the bare essentials. It falls a long way short of the income needed for what ASFA calls a 'comfortable' retirement.

Relying solely on the pension means giving up many of the things that make retirement something to look forward to—like travel, dining out, or funding your hobbies. This is why building your own nest egg through super is so critical for genuine financial freedom.

My Super Balance is Looking a Bit Low. How Can I Catch Up?

First, don't panic. If you feel you're behind, you're not alone, and there are effective ways to give your super a serious boost.

-

Contribute a little extra: Making additional contributions is the most direct way to accelerate growth. You can do this through pre-tax 'salary sacrificing' or after-tax personal contributions.

-

Consolidate your super: Many of us have old super accounts from past jobs being eaten away by fees. Rolling them into one fund is a simple move that can save you a small fortune.

-

Check your investment strategy: Is your investment mix right for your stage of life? Being too conservative, especially when you're younger, means your money might not be working hard enough.

Working out which of these moves will give you the most bang for your buck is where expert advice really pays off. A financial adviser can help you pinpoint the best strategies for your unique situation to get your retirement savings on track.

At Wealth Collective, our job is to help you move from questions and uncertainty to a clear, confident plan. When you're ready to get serious about designing your retirement, the next step is just a quick chat.

Book a complimentary 10-minute call with our team today and let's start building your wildly successful financial life.