Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Planning for retirement isn’t just about spreadsheets and superannuation statements. It starts with a much more personal question: what do you actually want your future to look like?

At Wealth Collective, we believe a successful retirement plan begins with your personal vision. It’s about turning those daydreams of travel, hobbies, and family time into a clear, tangible goal. This vision becomes the blueprint for every financial decision you make, transforming what can feel like an overwhelming task into a series of achievable steps.

Defining Your Ideal Retirement Lifestyle

Before we touch the numbers, we need to get crystal clear on your destination. What does “retirement” really mean to you? It’s not just an end date for work; it’s the beginning of a whole new chapter you get to design.

Many people have vague ideas like “I want to be comfortable” or “I’d like to travel a bit.” That’s a great start, but to build a solid financial plan, we need more detail. Specific, tangible goals are what we’re after.

Visualising Your Day-to-Day Life

Take a moment and imagine a typical week in your ideal retirement. What are you doing?

Perhaps you’re spending more time in the garden or finally lowering that golf handicap. Maybe you see yourself volunteering for a local cause, learning a new language, or just being more present for your grandkids.

Think about these practical lifestyle elements:

- Daily Activities: Will you be eating out regularly, joining clubs, or funding hobbies that come with a price tag?

- Home Life: Is the plan to stay put in your current home? Or are you thinking of downsizing to a lock-and-leave in Perth, or maybe a sea change down to the South West?

- Travel Plans: Are we talking weekend trips around WA, annual overseas adventures, or is the dream to buy a caravan and explore Australia?

Every one of these choices has a different cost attached. Sketching them out helps build a realistic picture of the income you’ll need. This is the foundation of the Retirement Roadmap we create with our clients here at Wealth Collective—it’s the first and most important step.

Understanding the Financial Realities

Once that vision is clearer, we can start attaching some numbers to it. While everyone’s situation is unique, industry benchmarks like the ASFA Retirement Standard can be a handy starting point. But the real magic happens when you personalise these figures to your own life.

Recent statistics from the Australian Bureau of Statistics paint a stark picture. The average intended retirement age is now 65.6 years, yet only 33% of Australians feel confident they’ll actually get there on time. With concerns about inflation (49%) and the economy (40%) weighing heavily, it’s never been more important to have a solid plan.

Your retirement plan can’t be built on guesswork. It needs to be a detailed projection of the life you want, supported by realistic financial calculations. This clarity is what turns retirement anxiety into confident action.

From Vision to Financial Target

The whole point of this exercise is to arrive at a specific number: the annual income required to fund your ideal retirement. This becomes your North Star.

For instance, a couple looking forward to a quiet life in their paid-off home with a few local holidays will have a vastly different income target than another couple planning extensive international travel. Pinning this number down gives purpose to everything that follows, from optimising your super to building your investment portfolio.

This is where every conversation at Wealth Collective begins. By first understanding your personal vision, we can then build a financial strategy designed to make it happen. It’s the most crucial part of the process, ensuring your money is working towards the life you genuinely want to live.

Before we move on, take a few minutes to see where you stand with this quick self-assessment.

Your Personal Retirement Readiness Checklist

Use this self-assessment to see where you stand and what key questions to consider on your retirement planning journey.

| Planning Area | Current Status (Not Started, In Progress, Complete) | Key Questions to Ask Yourself |

|---|---|---|

| Lifestyle Vision | What does my ideal day, week, and year in retirement look like? | |

| Income Goal | How much annual income will that lifestyle require? Have I accounted for inflation? | |

| Superannuation | Do I know my current balance, fees, and investment option? Am I making extra contributions? | |

| Investments | Do I have investments outside of super? Does my overall portfolio match my risk tolerance? | |

| Debt Management | What is my plan to be mortgage-free by retirement? Do I have other debts to clear? | |

| Insurance | Is my life, TPD, and income protection insurance still appropriate for my needs? | |

| Estate Plan | Do I have an up-to-date Will, Power of Attorney, and superannuation beneficiary nominations? |

Completing this checklist can give you a powerful snapshot of what you’ve already accomplished and where you need to focus your attention next.

Now, with a clear target in mind, the next logical step is to make sure the biggest retirement asset for most of us—our superannuation—is working as hard as it possibly can to get you there.

Giving Your Superannuation a Serious Boost

Think of your super as the main engine powering you towards retirement. Just letting it idle won’t get you there comfortably. You need to get under the hood and make some smart tweaks to really open it up.

Too many people fall into the trap of thinking their employer’s contributions are all they need. The reality? For most, it’s just not enough. Taking an active role is what turns a basic super account into a serious wealth-building tool. This is a massive focus of our Retirement Roadmap service – we make sure your super works as hard for you as you’ve worked for it.

Getting More Money In: Strategic Contributions

One of the most straightforward ways to ramp up your super balance is simply to put more in. The good news is the Australian system gives you some powerful tax incentives to do just that.

There are two main ways to contribute:

-

Concessional (Before-Tax) Contributions: This is money that goes into your super from your pre-tax pay, like your employer’s mandatory contributions or anything you salary sacrifice. The big win here is that it’s taxed at a flat 15% going in, which for most people is a lot lower than their personal income tax rate.

-

Non-Concessional (After-Tax) Contributions: This is money you add from your bank account after you’ve already paid tax on it. You don’t get a tax deduction for putting it in, but the earnings grow in a low-tax environment (max 15%), and it’s generally tax-free when you take it out in retirement.

If you’re earning a decent income, salary sacrificing is a simple yet powerful strategy. You’re effectively lowering your taxable income for the year while simultaneously boosting your retirement nest egg.

The gap between what most Aussies have in super and what they’ll need is pretty confronting. Proactive contributions are the bridge. They let you take advantage of tax breaks and the magic of compounding to close that gap.

If you want to get back to basics on how it all works, our guide on what superannuation is in Australia is a great place to start.

Making Sure Your Investments Match Your Timeline

Putting money in is only half the battle. How that money is invested inside your super fund is just as critical. Most funds give you a menu of options, from conservative to high growth. The right choice for you comes down to your tolerance for risk and how many years you have left in the workforce.

Let’s say you’re in your late 50s. A ‘Balanced’ option might be a good fit. These typically have a mix of growth assets like shares and property (60-70%) and a cushion of defensive assets like cash and bonds. It offers a blend of growth potential without taking on extreme risk.

But if you’re in your 40s, you have time on your side. You could lean into a ‘Growth’ or ‘High Growth’ option, which might have 80-95% in shares. The ride will be bumpier, but the long-term returns are potentially much higher. Being too conservative when you’re young is one of the biggest mistakes we see – it can mean leaving decades of compound growth on the table.

The Power of Compounding in Action

Let’s be blunt: a comfortable retirement doesn’t come cheap. The ASFA Retirement Standard suggests a couple needs around $73,875 a year. To fund that, you could be looking at a super balance of roughly $1.875 million. That number can be a shock when you see that the median super balance is closer to $208,000.

It’s a huge gap, but it’s not impossible to close. With the superannuation guarantee now on its way to 12%, the potential for your balance to compound is stronger than ever.

Small, consistent actions now can make an enormous difference down the line. It’s the powerful combination of smart contributions and the right investment mix that really gets the compounding engine firing. At Wealth Collective, our job is to help you fine-tune that engine, making sure every dollar is working its hardest to build the future you deserve.

Building Wealth Beyond Your Super Fund

Think of your superannuation as the engine of your retirement plan – it’s powerful and essential. But relying on it alone is like trying to build a house with just a hammer. A truly secure retirement is built with a full toolkit, creating multiple income streams to handle whatever life throws at you. This is where a smart investment portfolio comes in.

Creating wealth outside of super gives you options. It can provide an income if you want to retire early before you can access your super, fund big goals like a holiday home, or simply be an extra layer of financial security. This approach is central to our Guided Growth philosophy at Wealth Collective, where we help clients build lasting wealth that works alongside their super.

Getting to Know Your Investment Building Blocks

‘Investment portfolio’ might sound intimidating, but it’s really just a collection of different assets working together to grow your money. The trick is to understand the main ‘asset classes’ and the job each one does.

I like to think of it like a balanced meal. You need a mix of different food groups for a healthy diet, and your portfolio needs different asset classes for healthy, sustainable growth.

Here are the three core building blocks you’ll come across:

- Shares (or Equities): When you buy shares, you’re buying a tiny slice of a company. They offer the best potential for high growth over the long term, but they also come with more ups and downs along the way.

- Property: This is usually direct ownership of a residential or commercial property. It can provide a steady rental income and long-term capital growth, but it’s not something you can sell in a hurry if you need cash fast.

- Bonds and Cash: We often call these ‘defensive’ assets. Bonds are basically loans you make to governments or big companies in return for regular interest payments. Cash is, of course, the most secure, but it also offers the lowest returns.

The real magic happens when you mix them together. Spreading your money across these different assets in a way that matches your goals and your comfort with risk is what we call diversification. It’s the age-old wisdom of not putting all your eggs in one basket.

To give you a clearer picture, here’s a quick breakdown of how these common investment options stack up.

A Snapshot of Common Investment Options

| Investment Type | Typical Risk Level | Potential Return Profile | Best Suited For |

|---|---|---|---|

| Cash & Term Deposits | Very Low | Low | Short-term savings, emergency funds, and capital preservation. |

| Bonds (Government & Corporate) | Low to Medium | Modest | Generating a stable income stream and balancing higher-risk assets. |

| Australian Shares (Equities) | High | High (Capital Growth & Dividends) | Long-term growth and generating franked dividend income. |

| International Shares (Equities) | High | High (Primarily Capital Growth) | Diversifying away from the Australian market for long-term growth. |

| Direct Property | Medium to High | Moderate to High (Rent & Capital Growth) | Long-term investors comfortable with low liquidity and hands-on management. |

This table is just a starting point. Within each category, there are countless variations, but it helps to see how each piece of the puzzle can play a different role in your overall strategy.

Crafting an Investment Strategy That Works for You

Your investment strategy outside of super needs to work hand-in-glove with your superannuation and make sense for your retirement timeline. There’s no such thing as a one-size-fits-all portfolio; the right strategy is always going to be deeply personal.

For instance, one of our 55-year-old clients in Perth aiming to retire in seven years might have a portfolio heavily weighted towards blue-chip Aussie shares that pay consistent dividends. The goal here is to build a reliable income stream to supplement their eventual super pension.

On the other hand, a 45-year-old client might have a larger allocation to international growth stocks, accepting more short-term volatility for the potential of greater long-term growth.

Your investment portfolio is a powerful tool for achieving specific life goals. By aligning it with your unique vision for retirement, you create a focused plan that goes far beyond simply accumulating money.

A great place to start is to ask yourself: what is the main purpose of these investments? Is it to generate income now? Grow the capital for later? Answering that one question will shape the entire structure of your portfolio.

The Most Powerful Move: Eliminating Debt

Before you can truly accelerate your wealth building, you have to deal with the biggest financial drag for most pre-retirees: debt.

Walking into retirement with a mortgage is like trying to run a marathon with weights tied to your ankles. It dramatically increases the income you need to generate just to break even.

Becoming debt-free is one of the most liberating and financially powerful moves you can make. It frees up a huge amount of your cash flow, which can then be funnelled into your investments, turbocharging their growth in those critical final years before you finish work.

There are two popular and very effective ways to tackle debt:

- The Debt Snowball: Focus all your extra repayments on your smallest debt first. The psychological win of knocking one debt over gives you the motivation to keep going.

- The Debt Avalanche: This is the purely mathematical approach. You prioritise paying off the debt with the highest interest rate first, saving you the most money in interest over time.

Whichever method feels right for you, the goal is the same: to walk into retirement with a clean slate. Here at Wealth Collective, we see debt reduction as a non-negotiable part of a solid retirement plan. It’s a core focus of our Guided Growth service because it lays the foundation for building genuine, sustainable wealth.

Smart Ways to Ease Into Your Retirement

Those last few years on the job are more than just a countdown to clocking off. This is a strategic time where the decisions you make can have a massive impact on your first decade of retirement. Getting a handle on the tools and government benefits available can be the difference between a good retirement and a great one.

Helping our clients navigate this transition smoothly is a huge part of the Retirement Roadmap we build. It’s all about weaving together smart strategies, like a Transition to Retirement (TTR) pension, with a clear understanding of government support like the Age Pension. This combination helps you maximise your income and keep more of your hard-earned cash.

The “Transition to Retirement” (TTR) Strategy: A Soft Landing

A Transition to Retirement (TTR) strategy is a seriously useful tool. It lets you tap into your super once you hit your ‘preservation age’ (between 55 and 60, depending on your birth date), even while you’re still working. It’s all about giving you flexibility.

Think of it as opening a tap on your super and turning it into a regular income stream. Most people use it in one of two ways:

- Cut back your hours, not your pay: You could drop from five days a week to three, for example, and use the TTR income to fill the gap in your payslip. It’s a fantastic way to ease into retirement without a sudden shock to your budget.

- Turbo-charge your super and cut your tax: You can keep working full-time and ramp up your salary sacrifice contributions into super. The TTR income then comes in to replace that sacrificed pay, so your take-home pay stays the same. This can be a brilliant move to fatten up your super balance in the final stretch.

A TTR isn’t a one-size-fits-all solution, but for many people, it’s a golden opportunity to call the shots on their exit from the workforce. If you’re keen to dig into the details, you can learn more about how transition-to-retirement pensions work.

Getting to Grips with the Centrelink Age Pension

For many Australians, the Centrelink Age Pension will be part of the retirement income puzzle. It’s a safety net designed to support you, so knowing the basics of how it works is essential.

To get the pension, you need to be of Age Pension age (currently 67) and meet the residency rules. After that, Centrelink runs two key tests to figure out if you’re eligible and how much you’ll get:

- The Income Test: This looks at all the income you receive from part-time work, investments, and pensions from your super fund.

- The Assets Test: This adds up the value of your assets. The good news is it excludes your family home, but it does include investment properties, cars, shares, and your superannuation balance.

Centrelink applies both tests and pays you based on the test that results in the lower pension payment.

It’s a common myth that you have to be broke to get the Age Pension. The thresholds are more generous than many people realise, and even a part-pension can make a huge difference to your annual income.

How you structure your finances can impact your eligibility. This is where getting professional advice is worth its weight in gold, as it ensures your assets are set up in the most effective way to maximise any entitlements you might have.

Keeping Your Tax Bill Down in Retirement

The final piece of this transition puzzle is understanding tax. Or more specifically, how to pay as little of it as legally possible.

The fantastic news is that Australia’s superannuation system is incredibly tax-friendly in retirement. Once you’re over 60 and officially retired, any money you pull out of your super—whether as a lump sum or a regular pension—is typically 100% tax-free.

This is a massive advantage, but there are a few other things to keep in mind:

- Investment Income: Any money you earn from investments held outside of super (like share dividends or rent) is still taxable.

- Timing is Everything: If you need to access your super before you turn 60, different tax rules apply. Planning the timing of any big withdrawals is critical.

The goal is to build an income stream that’s as tax-efficient as possible. At Wealth Collective, we help our clients structure their retirement income to keep their tax obligations to a minimum, ensuring their financial plan is not just robust, but sustainable for the long haul.

Protecting Your Assets and Securing Your Legacy

Planning for retirement isn’t just about growing your nest egg; it’s also about building a fortress around everything you’ve worked so hard for. As you edge closer to finishing work, the game changes. It becomes less about chasing high-risk growth and more about protecting your capital. This is a crucial mental shift, and it means taking a good look at your personal insurance and legacy planning.

Getting these fundamentals sorted provides a level of peace of mind you can’t put a price on. It’s about ensuring one unexpected life event doesn’t throw your plans into chaos or leave your family in the lurch. This is exactly what our Protection Plus service at Wealth Collective focuses on—making sure you’re truly secure.

Reviewing Your Personal Insurance Cover

Here’s something we see all the time: people in their late 50s still paying for insurance policies that were set up for a 40-year-old with a massive mortgage and young kids. Your life has changed, so your cover should too.

As your debts shrink and your super grows, your insurance needs evolve dramatically. If you don’t adjust your policies, you’re likely overpaying for cover you no longer need.

A pre-retirement insurance check-up should zero in on three key areas:

- Life Insurance: Its main job is to pay off debts and replace your income for your family. If the house is paid off and your super is healthy, you may need less cover than you think.

- Total and Permanent Disability (TPD) Insurance: This provides a lump sum if you can never work again. With fewer working years ahead, your TPD cover may need adjusting.

- Income Protection: This has been your safety net, ready to replace your income if you got sick or injured. Its relevance naturally fades as you get closer to stopping work altogether.

Getting this right can free up hundreds, sometimes thousands, of dollars in annual premiums. That’s money that could be put to much better use, like a last-minute super contribution.

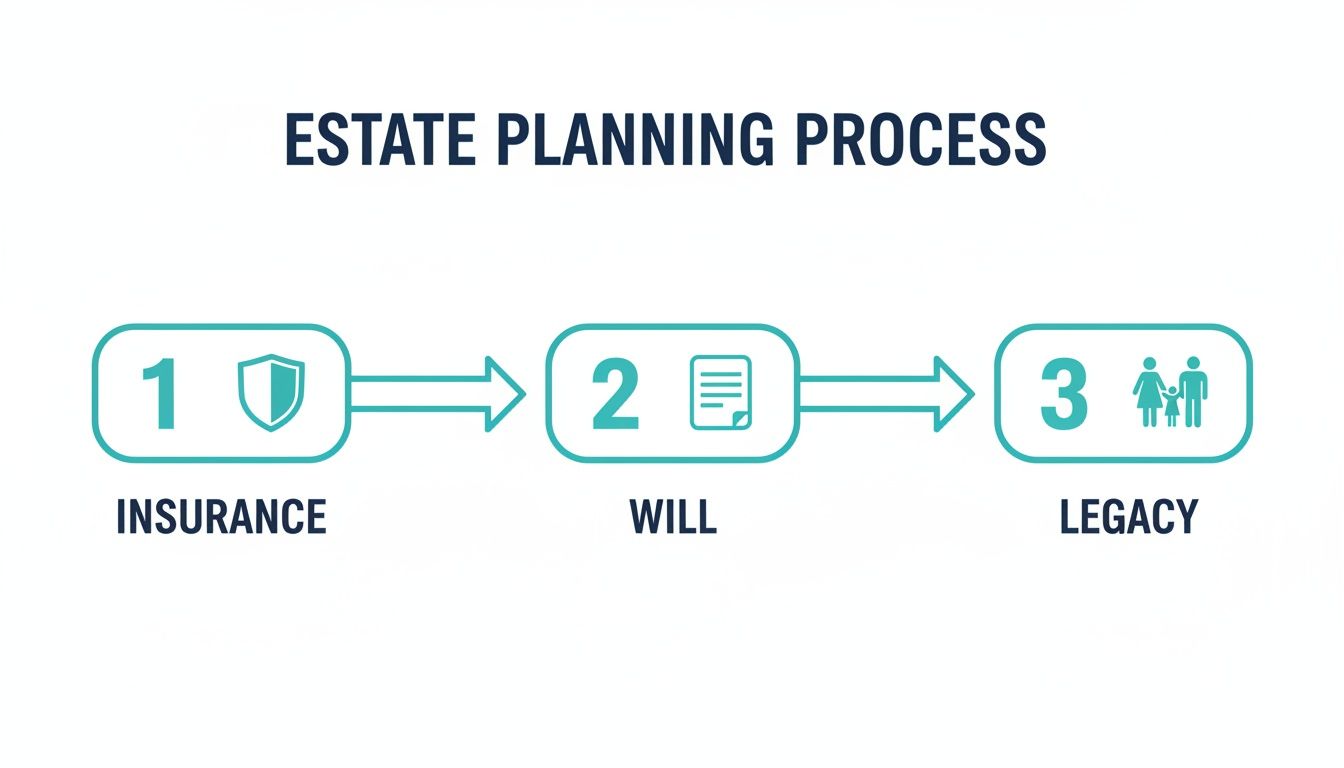

The Cornerstones of a Solid Estate Plan

Estate planning is simply about making clear decisions now for how your assets are managed and passed on. A proper plan ensures your wishes are followed, saving your loved ones a world of stress.

For anyone here in Western Australia, there are three documents that form the absolute bedrock of a good estate plan:

- Your Will: This is the legal playbook for who gets what. Without a valid Will, the government steps in to divide your assets according to a rigid formula—which often isn’t what you would have wanted.

- Enduring Power of Attorney (EPA): This lets you appoint someone you trust to manage your financial and property affairs if you ever lose the capacity to do so yourself.

- Enduring Power of Guardianship (EPG): This appoints a trusted person to make personal and lifestyle decisions for you—like where you live or what medical care you receive—if you can no longer make them.

An estate plan is one of the greatest gifts you can give your family. It provides clarity and direction when they need it most, preventing potential disputes and ensuring a smooth transfer of your legacy.

One final piece of the puzzle that catches many people out is superannuation. Your super doesn’t automatically get included in your Will. You have to fill out a specific form to tell your super fund exactly who you want to receive it. Our guide on what happens to your super when you die walks you through this in more detail.

Putting these protections in place is a fundamental part of a retirement plan that’s built to last. At Wealth Collective, our Protection Plus service is designed to bring you clarity and confidence, ensuring your assets are shielded and your legacy is secure.

Your Personal Retirement Action Plan

All this information is valuable, but only if you act on it. We’ve walked through the key elements of how to plan for retirement, but the real magic happens when you turn these insights into concrete actions. It’s time to take the wheel of your financial future.

Every successful retirement we’ve helped build started with simple, manageable steps. The next logical move is to translate this information into a plan that’s uniquely yours. This is the heart of what we do at Wealth Collective; we create a tailored Retirement Roadmap that gives you clarity and a clear path forward.

Creating Your Roadmap

We believe good financial advice should be simple and stress-free. Your roadmap is designed to be just that: a straightforward summary of your key tasks, from finalising super contributions to getting your estate plan in order. Think of it as your personal checklist to keep you on track.

A great plan doesn’t have to be complicated, but it must be personal. It’s about making confident decisions that align with the specific lifestyle you want to achieve.

This visual breaks down the simple but crucial steps involved in securing your legacy.

Following this process ensures your assets are protected and your wishes are crystal clear, giving you and your family genuine peace of mind.

Ready to build a secure and fulfilling future? Book a complimentary 10-minute chat with our team today to see how we can help get you started.

Got Questions? We’ve Got Answers

When you start digging into the details of retirement planning, a lot of questions pop up. Here are some of the most common ones we hear from our clients, along with some straight-talking answers.

How Much Super Do I Really Need to Retire Comfortably?

This is the big one, isn’t it? While everyone’s ‘magic number’ is different, the Association of Superannuation Funds of Australia (ASFA) suggests a couple aiming for a ‘comfortable’ retirement might look for an annual income around $75,000. To generate that, you could be looking at a super balance close to $1.8 million, assuming you own your home outright.

But that’s just a guide. The only number that truly matters is yours. The best way forward is to map out what your ideal retirement looks like and what it will cost. This is the first thing we do when building a Retirement Roadmap for our clients—it all starts with your vision.

Is It Too Late to Plan for Retirement in My 50s?

Not a chance. Your 50s are an incredibly powerful decade for building wealth. In fact, this is often when you’re at your peak earning potential, which makes it the perfect time to make serious headway.

Think of it as the final sprint. This is the decade to:

- Make the most of ‘catch-up’ contributions to your super.

- Get serious about knocking off any lingering debts, especially the mortgage.

- Fine-tune your investment strategy now that your retirement horizon is clearly in view.

- Get a second opinion from an expert to make sure you’re not leaving any opportunities on the table.

What Is a Transition to Retirement Strategy?

A Transition to Retirement (TTR) strategy is a clever way to ease into your post-work life. Once you hit your preservation age, it lets you draw an income from your super while you’re still working.

It’s all about giving you flexibility. You could drop back to four days a week at work and use your TTR income to top up your pay packet. Or, you could keep working full-time and use it to turbo-charge your super contributions in a very tax-effective way.

A TTR can be a game-changer, but it’s not for everyone. It’s one of those things that really depends on your personal situation, so it’s always best to chat with a financial adviser to see if it makes sense for your final few years on the job.

Figuring out how to plan for retirement has a lot of moving parts, but you don’t have to piece it all together on your own. The team at Wealth Collective is here to turn the complexity into a clear, straightforward plan.

Why not book a complimentary 10-minute call? Let’s see how we can help you build your wildly successful financial life.