Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You might think of income protection as your ultimate financial backstop, but it’s not designed to cover everything. It generally won’t pay out for job loss due to redundancy, a normal pregnancy, self-inflicted injuries, or for illnesses you had before you even signed up. Understanding these built-in gaps is the first, and most important, step to making sure your financial safety net is actually as strong as you think it is.

Your Financial Safety Net Has Gaps You Need to Know

Picture this: you’ve done everything by the book. You’ve landed a great job in Perth, put a solid financial plan in place, and taken out income protection insurance. Then, out of the blue, an illness knocks you off your feet, and you get the gut-wrenching news that your claim has been denied.

This isn’t just a hypothetical nightmare; it’s a reality for too many Australians who get caught out by the fine print in their policies.

The whole point of this insurance is to replace a chunk of your income if you’re too sick or injured to work. But the real value of that protection comes down to what is and, crucially, isn’t covered. For a full rundown, you can learn more about what income protection insurance is in our comprehensive guide.

Why Exclusions Exist

At the end of the day, insurers are in the business of managing risk. They build exclusions into their policies to keep premiums from skyrocketing and to avoid paying claims for events that are almost guaranteed to happen, are within your control, or are simply too risky to cover.

Without these boundaries, the cost of cover would be unaffordable for most of us. The most common reasons for exclusions are:

- Pre-existing medical conditions you had before the policy kicked in.

- High-risk activities and hobbies that dramatically increase your chance of getting hurt.

- Self-inflicted harm or injuries you get while doing something illegal.

- Events unrelated to sickness or injury, like being made redundant.

A policy’s true strength isn’t just in what it promises to cover, but in the clarity of what it doesn’t. Recognising these limitations is crucial for building a truly resilient financial plan.

The Wealth Collective Approach

For the dual-income families and ambitious business owners we work with here in Western Australia, income is the engine that drives every single financial goal. A denied claim isn’t just a minor setback; it can completely derail long-term plans for building wealth and securing a comfortable retirement.

This is exactly why the first step in our Protection Plus service is a deep dive into any cover you already have. We don’t just glance at the benefit amount; we stress-test your policies against your specific lifestyle, health profile, and occupation to find those hidden gaps.

By getting a crystal-clear picture of what your income protection does not cover, we can then build a strategy that gives you genuine security. This guide will walk you through these exclusions, one by one, so you can make informed decisions and ensure your financial future is properly protected.

Pre-Existing Conditions: The Most Common Reason a Claim Gets Knocked Back

When an income protection claim is denied, the reason often comes down to two simple words: pre-existing condition. It’s the biggest hurdle people face when trying to claim, but it’s also one of the most misunderstood parts of any policy.

Most of us think of a pre-existing condition as a major, ongoing illness like diabetes or heart disease. The reality is much broader. That old footy injury from uni that flares up now and then? That brief chat with a therapist a few years back? Even that nagging lower back pain you see the physio for every so often? An insurer can classify all of it as pre-existing. If it’s in your medical history before you sign on the dotted line, it’s fair game.

This is exactly where people get caught out. It’s easy to forget a past issue or just assume it’s too trivial to mention. But when you’re applying for insurance, full and honest disclosure isn’t just a good idea—it’s your best defence against having a claim rejected down the line.

The Real-World Impact of Not Disclosing Everything

Failing to disclose a pre-existing condition can have devastating consequences, even if the reason you have to stop working is completely unrelated.

Picture this: you’re a professional in Perth, loving the active WA lifestyle. One weekend, a friendly game of footy goes wrong, and you end up with a serious back injury. You put in a claim, feeling relieved you have income protection to fall back on, only to receive a letter saying it’s been denied.

Why? The insurer dug into your medical records and found notes from a few physio visits for back pain years ago that you never declared on your application. This isn’t some rare horror story. Back and knee issues are incredibly common reasons for insurers to add specific exclusions to a policy. In fact, a study of over 500 policies found that 5% had loadings or exclusions for back and knee problems, making it the third most common carve-out. Insurers see these as a red flag, especially for active people. You can read more about how insurers assess these risks on Skye.com.au.

From the insurer’s perspective, your history makes you more likely to claim in the future. This is backed up by the numbers. APRA statistics show that over the last three years, a massive 72.9% of claim denials were due to issues like non-disclosure or specific policy exclusions.

Getting Your Head Around the Jargon

When you do the right thing and disclose a pre-existing condition, the insurer has a couple of options. They won’t always just say no. More often, they’ll offer cover with one of the following:

-

A specific exclusion: This is the most frequent outcome. The insurer will cover you for almost everything except for claims related to that specific condition. If you’ve had knee trouble in the past, they might put a “knee exclusion” on your policy.

-

A loading: This is when the insurer agrees to cover the condition, but they’ll charge you a higher premium to account for the extra risk. Your cover costs more, but you’re not left with a gap.

An exclusion means you pay for a policy that has a specific, known weakness. A loading means you pay more for a policy that doesn’t. Figuring out which is right for you is a crucial financial decision.

For the dual-income families and business owners we work with at Wealth Collective, we see your income as the engine of your entire financial plan. A policy full of exclusions creates a false sense of security, leaving that engine unprotected just when you need it most.

Your Best Defence is a Watertight Application

The application is your one and only chance to get this right. It means carefully going through your entire medical history, no matter how small or insignificant a past issue might seem. This is precisely where getting some expert help can make all the difference.

As part of our Protection Plus service, we guide clients through this minefield. We sit down with you to meticulously comb through your medical history, ensuring your application is accurate, honest, and complete. This proactive work dramatically reduces the risk of an insurer slapping on unexpected exclusions or, worse, denying a legitimate claim when you’re at your most vulnerable.

By tackling potential problems upfront, we help you secure a policy that delivers genuine protection, not just an empty promise. Don’t leave your income to chance. Booking a brief introductory call with our team can give you the clarity you need to ensure your financial safety net is built on solid ground.

How Lifestyle Choices and Hobbies Can Void Your Policy

Your income protection policy is there for the unexpected curveballs life throws your way, but it’s not designed to be a safety net for every single situation. Insurers are, at their core, risk assessors. Certain lifestyle choices or high-octane hobbies can dramatically ramp up the chance of you making a claim, which is why they’re often listed as standard exclusions in the fine print.

For many professionals and business owners here in Perth, an adventurous lifestyle is a huge part of the appeal of living in WA. The problem is, that weekend rock climbing trip or dirt bike session could have serious financial consequences if things go wrong. If an insurer considers an activity “high-risk,” any injury you sustain while doing it might not be covered.

When Adventure Becomes an Uninsurable Risk

During the application process, insurers will dig into your hobbies and pastimes. It is absolutely crucial to be upfront and honest about any activities that could be seen as hazardous.

Common examples that raise a red flag include:

- Skydiving or BASE jumping

- Motorsport racing (cars, bikes, you name it)

- Playing sports at a professional or even semi-professional level

- Mountaineering or rock climbing

- Scuba diving beyond certain depths or in specific conditions

Holding back on this information is a massive gamble. If you need to claim down the track, the insurer can deny it on the grounds of non-disclosure, even if you’ve paid your premiums on time for years. They’ll argue that if they’d known about the increased risk, they would have either charged you a higher premium or specifically excluded that activity from your cover right from the start.

Self-Inflicted Harm and Illegal Acts

Beyond adrenaline-fueled hobbies, some exclusions are pretty much universal across every policy. These relate to situations where the injury or illness wasn’t an unforeseen accident in the way insurance is meant to work.

A fundamental principle here is that intentional acts are not covered. This means any self-inflicted injuries or illnesses resulting from suicide attempts will be excluded. Likewise, if you’re injured while committing a criminal act—say, you’re in a car accident while driving under the influence—your claim will be denied. Insurers simply won’t foot the bill for situations arising from illegal behaviour.

It’s a tough pill to swallow, but insurance is built on a foundation of good faith. Policies are there to protect you from life’s unexpected accidents, not the predictable outcomes of dangerous or illegal choices.

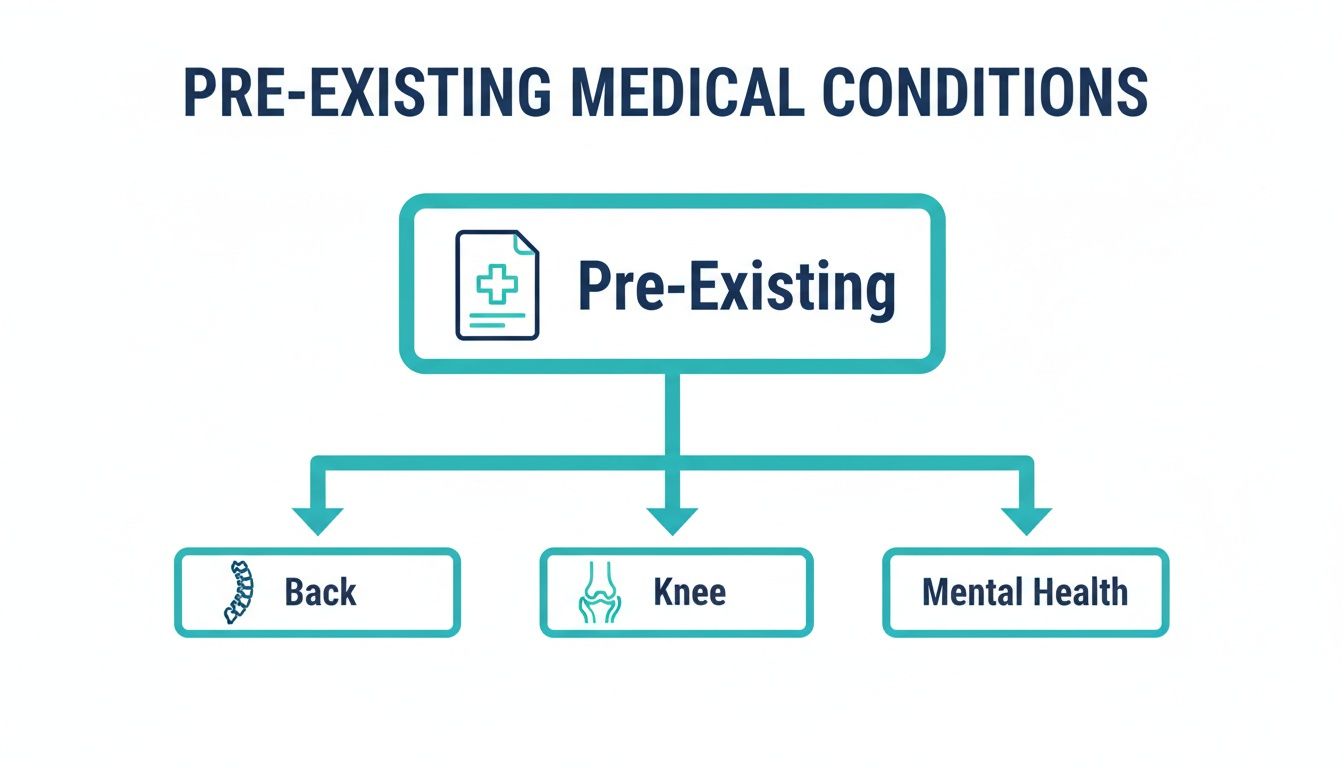

The diagram below highlights some of the most common pre-existing conditions that can lead to policy exclusions. It’s worth noting how often these intersect with lifestyle choices and hobbies.

As you can see, previous issues with your back, knees, or mental health are frequently flagged by insurers, often leading to specific carve-outs in your cover.

Substance Abuse and Other Exclusions

Another critical exclusion to be aware of relates to substance abuse. If your inability to work is a direct result of alcoholism or drug addiction, you can expect your claim to be rejected. There can be grey areas, like if the condition is proven non-addictive and part of a formal rehab program, but this varies hugely between insurers and is never a guarantee.

The following table breaks down common activities and situations, helping you see the line between what’s generally covered and what’s likely excluded.

Common Lifestyle and Activity Exclusions

| Situation or Activity | Typically Covered? | Common Exclusions and Nuances |

|---|---|---|

| Weekend sports (e.g., social tennis, local footy) | ✅ Yes | Usually covered, but professional or semi-professional participation is often excluded. |

| DIY home renovations | ✅ Yes | Injuries from everyday activities are generally fine, unless you’re using explosives or doing something reckless. |

| Driving to and from work | ✅ Yes | Standard commuting is covered. |

| Recreational Scuba Diving | ⚠️ Maybe | Often excluded if you dive beyond a certain depth (e.g., 30 metres) or engage in technical/cave diving. |

| Motorsports (track days, racing) | ❌ No | Almost universally excluded due to the high risk of serious injury. |

| Aviation (as a private pilot) | ❌ No | Flying a private aircraft is a standard exclusion unless you have specific, expensive cover. |

| Injury during a criminal act | ❌ No | If you’re injured while breaking the law (e.g., drink driving), your claim will be denied. |

| Self-inflicted injury | ❌ No | Intentional self-harm is a standard exclusion across all policies. |

It’s a stark reminder that the devil is always in the detail of your Product Disclosure Statement (PDS).

Imagine you’re a small business owner in Perth, injured during a weekend skydiving adventure. It’s a nightmare scenario to discover that your policy specifically excludes high-risk activities, leaving you without a financial lifeline. This isn’t just a hypothetical; participation in risky sports is a classic non-covered scenario, alongside criminal acts, war, and self-inflicted injuries. Recent APRA figures showed 577 income protection claims were denied in a single year, often due to these exact kinds of gaps in cover. You can discover more insights about common IP exclusions from Aspect UW.

At Wealth Collective, our Protection Plus service is designed to prevent these situations from happening. We dive deep into your lifestyle, hobbies, and work to make sure your policy truly matches the life you lead. By flagging these potential exclusion traps upfront, we help you find cover that delivers genuine peace of mind, not just a false sense of security.

Don’t wait until it’s too late to discover your policy has holes. A quick, complimentary 10-minute chat with our team can get you started on a protection strategy that actually protects you.

Understanding the Jargon: Waiting Periods and Key Definitions

Beyond the obvious exclusions like pre-existing conditions, some of the biggest traps in income protection policies are hidden in the technical definitions. Words like “waiting period” or “total disability” might seem simple enough, but the insurer’s specific definition can be the difference between a paid claim and a denied one.

Getting this part wrong is a classic case of finding out your policy doesn’t cover the very thing you need it for. For the professionals and business owners we work with, a small misunderstanding here can have devastating financial consequences. It’s not just about having a policy; it’s about having the right one.

Waiting Periods: Your Time-Based Excess

Think of the waiting period as a time-based version of the excess on your car insurance. It’s the period you have to wait after you stop working due to illness or injury before your benefit payments start. You choose this upfront, and it has a huge impact on both your premium and your financial risk.

Most policies in Australia offer common waiting periods like:

- 30 days

- 60 days

- 90 days

A shorter wait, say 30 days, means money will start flowing much sooner. Naturally, this convenience comes with a higher premium. On the flip side, a 90-day waiting period will make your policy much more affordable, but you’ll need to cover your own expenses for three full months.

This is a critical trade-off. A 2022 survey revealed that nearly a third of Australians (31%) would face serious financial hardship if they lost their income for just three months. Opting for a 90-day waiting period to save a bit on premiums could backfire badly if you don’t have a solid emergency fund to bridge that gap.

‘Own Occupation’ vs ‘Any Occupation’: A Career-Defining Difference

Arguably the single most important clause in your entire policy is how it defines “disability.” This sets the rules for when you can actually claim. There are two main definitions you need to know: ‘Own Occupation’ and ‘Any Occupation’.

‘Own Occupation’: You’re considered disabled if your injury or illness prevents you from performing the key duties of your specific job. A surgeon who damages their hand and can no longer operate would be covered, even if they could still work as a medical consultant.

‘Any Occupation’: This is much tougher. You’re only considered disabled if you can’t perform any job that you’re reasonably suited for based on your education, training, or experience. The same surgeon would likely have their claim denied because they are still perfectly capable of working in other roles.

For anyone in a specialised role—surgeons, pilots, architects, skilled tradespeople—an ‘Own Occupation’ definition is absolutely essential. It protects the unique, high-value skills you’ve spent years building. ‘Any Occupation’ policies are always cheaper, but they offer a far weaker safety net. It’s a detail often buried in the fine print of default policies, like some offered through super funds. You can dive deeper into how these policies work in our guide to income protection inside superannuation.

Total vs Partial Disability

Finally, let’s look at what happens when you’re not completely out of action. A total disability benefit kicks in when you can’t work at all. But what if you’re well enough to return to work part-time or in a lighter capacity?

That’s where a partial disability benefit is meant to help, topping up your reduced income as you get back on your feet. The catch? The rules can be surprisingly strict. Some policies will only pay a partial benefit after you’ve been totally disabled for a specific length of time first, creating yet another potential gap in your cover.

Getting these definitions right is the core of what we do in our Protection Plus service at Wealth Collective. We don’t just glance at the monthly benefit amount; we stress-test these crucial definitions to make sure your policy is built to protect your career and your income. By translating the fine print, we help you secure a policy that delivers real peace of mind, not just the illusion of it.

What About Pregnancy, Mental Health, and Redundancy?

It’s easy to think of income protection as an all-purpose safety net, ready to catch you whenever life throws a curveball. But this is a dangerous assumption, and one that often leads to shock and financial stress right when you can least afford it.

Let’s get straight to the point and tackle three of the biggest—and most costly—misunderstandings: pregnancy, mental health, and losing your job. These are major life events where financial stability is everything. Assuming you’re covered when you’re not can dismantle your best-laid plans in an instant.

Pregnancy Is Not an Insurable Illness

This is a common source of confusion. To put it simply, a normal, healthy pregnancy isn’t considered an illness or an injury. That means the time you take off for maternity leave isn’t a claimable event under a standard income protection policy. The insurance is there to protect you from unexpected medical events, not planned life stages.

Where it gets more nuanced is when serious medical complications pop up. If you develop a medically diagnosed condition linked to your pregnancy—think severe pre-eclampsia or something that requires doctor-ordered bed rest—and it stops you from working, then you may have a valid claim. The line in the sand is between a standard pregnancy and a disabling medical complication.

The Nuances of Mental Health Cover

As our understanding of mental health has improved, the insurance world has responded, but not always in the way you might expect. While some policies provide solid cover for conditions like depression and anxiety, many are now tightening the rules with specific exclusions or limitations. You absolutely have to check where your policy stands on this.

For example, an insurer might:

- Refuse to cover any mental health conditions at all.

- Exclude specific conditions you’ve sought advice or treatment for in the past.

- Cap the payout period, meaning they’ll only pay your claim for a limited time, like 24 months, even if you can’t return to work.

Given that mental health issues are a leading reason for income protection claims in Australia, this isn’t a detail you can afford to gloss over. You need to know what’s excluded before you ever need the support.

A policy with a broad mental health exclusion is like having home insurance that doesn’t cover fire. It leaves one of your biggest risks completely exposed.

Redundancy Is a Different Beast Entirely

Let’s clear this one up for good: income protection insurance will not pay you if you are made redundant, get fired, or if your business closes down. It is purely for when you are unable to earn an income because of a diagnosed illness or injury.

You can get separate insurance specifically for redundancy, but it’s a completely different product with its own set of rules and conditions. Trying to lean on your income protection policy to soften the blow of a job loss will leave you high and dry.

At Wealth Collective, our Protection Plus service is all about cutting through the noise. We skip the jargon and stress-test your existing cover against these exact scenarios to show you where you’re truly protected and where the gaps are. It’s about building a plan that delivers genuine security, not just a false sense of it. Book a complimentary 10-minute call to get the clarity you need to properly protect your income.

Your Action Plan for a Stronger Financial Defence

Understanding what your income protection doesn’t cover is the first crucial step. But knowledge is only powerful when you act on it. Now it’s time to build a sturdier financial defence by reviewing your existing cover and proactively bridging any gaps you find. Think of it this way: your income is the engine of your financial life, and a well-structured plan is what keeps it protected.

Start by digging out your current policy documents. Don’t just glance at the benefit amount; hunt for the specific details we’ve been discussing. The goal here is to move from uncertainty to absolute clarity, so you can make decisions with confidence.

Review Your Current Policy

When you’re looking over your cover, you need to find clear answers to some critical questions. If you can’t easily find them in the Product Disclosure Statement (PDS), that’s your cue to call your adviser.

- What specific exclusions are listed? Look for clauses related to pre-existing conditions, your high-risk hobbies, or mental health.

- What is my waiting period? Be honest with yourself—do you have enough savings to comfortably get through this gap?

- Is my policy ‘Own Occupation’ or ‘Any Occupation’? This definition is a game-changer, especially if you’re in a specialised career.

- Are there any caps on benefits? Keep an eye out for limitations on certain claims, like a two-year cap on mental health benefits that many policies now have.

A policy review isn’t about finding problems; it’s about creating solutions. Identifying a weakness in your cover today is far, far better than discovering it when you’re already trying to make a claim.

Bridging the Gaps in Your Cover

Once you’ve identified where the gaps are, you can take strategic steps to fill them. Your income protection policy is just one piece of the puzzle. A truly robust financial defence has several layers of protection.

A great place to start is building a dedicated emergency fund. This cash buffer is your first line of defence, designed to cover your waiting period and other immediate expenses that will inevitably pop up.

On top of that, other types of personal insurance work hand-in-hand with your income protection. Policies like Trauma Insurance or Total and Permanent Disability (TPD) cover different life-altering events and provide lump-sum payments to clear debts or cover major medical costs, taking huge pressure off your recovery.

This multi-layered approach is the foundation of our Protection Plus service here at Wealth Collective. We don’t believe in a “set-and-forget” strategy. We’re here to help you build a complete protection plan that addresses the specific risks you and your family face.

The next logical step is to make sure your strategy is sound. We invite you to book a complimentary 10-minute introductory call with a Wealth Collective adviser for a professional assessment of your plan.

Frequently Asked Questions About Policy Exclusions

It’s completely normal to have a heap of questions when you start digging into the details of income protection. Honestly, understanding what your policy doesn’t cover is just as important as knowing what it does.

Here are the straight answers to some of the questions we get asked all the time.

What Happens if a Medical Condition Develops After My Policy Starts?

This is a great question. Generally, if a brand new medical issue pops up after your policy is officially in place, you should be covered.

The key here is that you were completely upfront and honest about your health during the application process. The real trouble with exclusions almost always traces back to health problems that existed before you took out the cover, even if they seemed minor at the time.

Can Exclusions Ever Be Removed from a Policy?

Sometimes, yes. It’s not guaranteed, but it’s definitely possible.

Let’s say the insurer put an exclusion on a past knee injury from your footy days. If you’ve gone a long time—often years—with no pain, symptoms, or treatment, you can ask them to take another look.

You’ll need to provide fresh medical evidence to back up your claim that the issue is resolved. The insurer has the final say, but having a financial adviser go into bat for you can make a huge difference to your odds of success.

Think of your policy as a living document. Your health can improve and life changes, so your cover should be able to adapt with you.

Does Being Made Redundant Mean I Can Claim?

This is a big one, and the answer is a hard no. It’s a really common point of confusion.

Income protection insurance only pays out when you’re unable to work because of a diagnosed illness or injury. It offers zero protection if you lose your job through redundancy, being let go, or your company closing down.

There are separate, specific policies for redundancy, but they are a completely different kettle of fish. Mistaking your income protection for this kind of cover can leave you in a very tough spot financially. That’s why a solid financial plan doesn’t just rely on insurance; it also includes a healthy emergency fund. To see how these different covers work together, check out our guide on the main types of life insurance available in Australia.

Getting your head around these details is where good advice is worth its weight in gold. At Wealth Collective, our Protection Plus service is all about giving you total clarity and confidence in your financial safety net. Book a complimentary 10-minute call today and let’s make sure your cover is truly built for life’s real challenges.