Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

For most business owners, their company is far more than just an asset on a balance sheet. It's a legacy, built from the ground up through years of sweat, sacrifice, and vision. But all too often, succession planning for business owners gets pushed to the bottom of the to-do list, leaving that hard-won legacy dangerously exposed.

The reality is, without a clear plan for the future, you're leaving the fate of your company, your personal financial security, and your family’s well-being entirely to chance. At Wealth Collective, our process is designed to turn uncertainty into a clear, actionable strategy, starting with a simple introductory call.

Why Your Business Legacy Needs a Succession Plan Now

You’ve poured everything into your business. It represents your dedication and often, the bulk of your personal net worth. It’s surprising, then, how many Australian entrepreneurs are simply not prepared for the day they finally step away.

This isn’t just about planning a comfortable retirement. A sudden illness, an unexpected accident, or a death can force a transition at the worst possible moment. This can throw a company into chaos and seriously erode the value you've worked so hard to build. Without a documented plan, your life's work could get tied up in messy legal battles or sold for a fraction of what it's truly worth.

The Numbers Don’t Lie

The scale of this issue across Australia is staggering. Many business owners are operating on hope, not strategy, and the data paints a very clear picture of the risks involved.

The Reality of Succession Planning for Australian Business Owners

| Statistic | Finding | Implication for Your Business |

|---|---|---|

| Only 19% of family businesses | Have a formal, documented succession plan in place. | You are in the majority if you haven’t planned, but this puts you at significant risk of value destruction and family conflict. |

| $3.5 trillion | The estimated wealth to be transferred between generations in Australia over the next 20 years. | A massive portion of this wealth is tied up in private businesses. A poor transition means your family misses out on their share. |

| $432 billion | The “untapped value” locked within these private businesses that could be realised with better planning. | Failing to plan is not just risky; it’s actively leaving money on the table that could fund your retirement or your family’s future. |

These figures, drawn from sources like Grant Thornton’s insightful 2025 Family Business Report, show a widespread vulnerability. A huge number of owners are gambling with their legacy, and the odds aren’t in their favour.

It’s Not a Task, It’s a Strategy

We get it. Succession planning can feel overwhelming and emotional. It forces you to confront your business mortality. But reframing it as a proactive strategy for strengthening your business—rather than just an exit chore—changes the entire dynamic.

A well-executed plan does so much more than just prepare for your departure. It actively improves your business right now.

- Maximises Business Value: The process forces you to look under the hood, identify weaknesses, and shore them up, making your company more robust and valuable to a buyer or successor.

- Ensures a Smooth Handover: It creates a clear roadmap for leadership transition, defining roles and responsibilities to minimise disruption and reassure employees, customers, and suppliers.

- Protects Your Family: A solid plan prevents ugly disputes between heirs and ensures your loved ones are looked after financially, in line with your personal wishes.

- Reduces Your Tax Bill: With enough foresight, you can structure the transition to access tax concessions, keeping more of the sale proceeds for your own retirement.

The biggest mistake you can make with succession planning is waiting. Thinking of it as a long-term strategic project, not a last-minute retirement task, is the secret to protecting your wealth and securing your legacy.

At Wealth Collective, we’ve seen the fallout from a lack of planning first-hand. But we’ve also seen the incredible relief and confidence that comes from finally having a clear roadmap in place. Our process starts by understanding your personal and financial goals, then works backwards to build a business exit strategy that actually achieves them.

Having an initial chat with an adviser is the single most important first step. It turns the vague notion of “someday” into a concrete, actionable plan. This isn’t about rushing you out the door; it’s about putting you back in control. Starting the conversation now gives you the one thing you can’t buy later: time. Time gives you options, leverage, and the ability to transition on your own terms. Booking an initial call is a simple, no-obligation way to start this vital process.

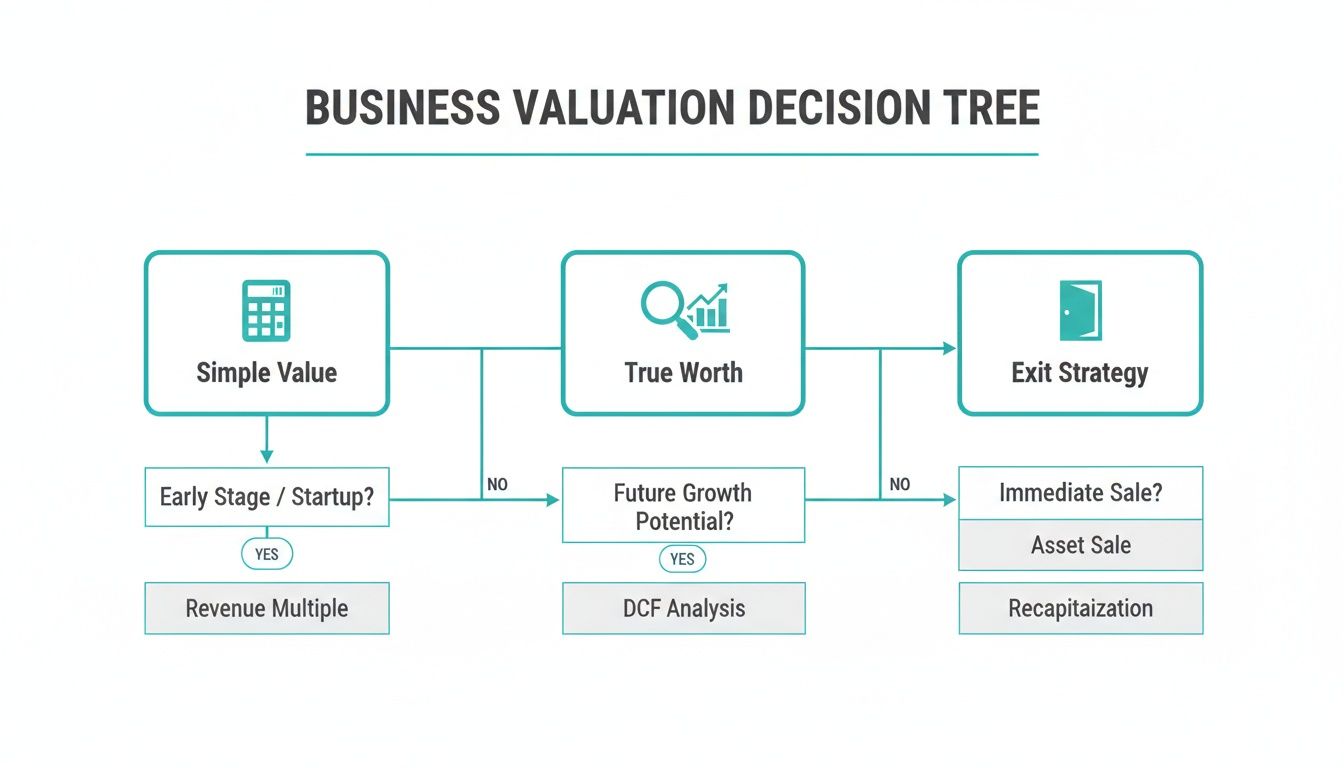

Determining What Your Business Is Actually Worth

Before you can map out your exit, you need an honest, clear-eyed view of what you’re starting with. That means knowing what your business is truly worth—not the number in your head, but its real value on the open market.

It’s a step a surprising number of business owners get wrong. They often fall back on simple rules of thumb, like applying a quick multiple to their profit. This is a massive oversimplification, like valuing a home just by the number of bedrooms, ignoring its premium location or solid build quality. The real value is almost always hidden in the details.

Looking Beyond the Balance Sheet

A proper valuation goes so much deeper than just your profit and loss statement. It’s about assessing the qualitative factors that make your business strong, competitive, and appealing to someone else.

We’re talking about things like:

- Brand Reputation: Is your business the first name people think of in your industry? A powerful brand commands a serious premium.

- Customer Loyalty: Do you have a solid base of repeat clients who provide predictable revenue? Long-term, sticky customers are a massive asset.

- Intellectual Property: Think patents, trademarks, or unique in-house software. These aren’t always obvious on paper but can be incredibly valuable.

- Strength of Your Team: A business that hums along smoothly without you personally steering the ship every day is infinitely more valuable than one that relies entirely on you.

A professional valuation isn’t just about getting a number; it’s a strategic health check for your business. It shines a light on what you’re doing right and, just as importantly, flags the weaknesses you need to fix before you can exit successfully.

Getting a handle on these drivers is the first real step towards strategically boosting your business’s worth. It gives you a clear financial baseline for every decision you make from this point forward.

Common Valuation Methods

There’s no single “magic formula” for valuing a business. In reality, professionals use a blend of methods to arrive at a defensible figure. Knowing the basics will help you have a much more productive conversation with your advisers.

- Asset-Based Valuation: This approach adds up the value of all your assets (cash, equipment, property, inventory) and subtracts liabilities. It’s often a starting point for asset-heavy businesses but can miss the mark for service-based companies.

- Market-Based Valuation: This method looks at what similar businesses in your industry have sold for recently. Its accuracy depends entirely on finding truly comparable sales data, which can be tough for private businesses.

- Income-Based Valuation: This is one of the most common and relevant methods. It focuses on what a business is built for: generating future income. The valuation is typically based on a multiple of past or projected cash flow or earnings.

A formal valuation report from an independent expert is a non-negotiable part of any serious succession plan. It gives you an objective benchmark that you and a potential successor can trust, heading off disagreements and making sure you get a fair price. Strong numbers are the bedrock of a healthy company, a topic we cover in more detail in our guide to small business cash flow management.

This valuation becomes the foundation of your entire exit strategy. It will influence everything from which transfer option you choose to how you structure your tax affairs. Once you have that solid number in hand, you can finally start making confident, informed decisions. Think of it as the first real move on the chessboard, setting you up for a smooth transition and a secure financial future.

Exploring Your Succession Pathways and Exit Options

With a clear valuation in hand, the big question becomes: who do you pass the keys to? This is where your business strategy and your personal life goals finally intersect. The best path will depend on your finances, your timeline, and the kind of legacy you want to leave behind.

For many Australian business owners, this decision can feel monumental. So, let’s break down the four most common pathways. Each one comes with its own set of trade-offs, affecting everything from your final pay out to how your company’s story continues.

As you can see, understanding your business’s true worth—not just its balance sheet value—is what truly empowers you to choose the right exit.

Passing the Torch to Family

For many entrepreneurs, the ultimate dream is keeping the business in the family. It’s the clearest path to preserving your name and the culture you’ve built. Done right, it feels like a natural continuation for everyone.

But this path is loaded with emotional complexity. You have to be brutally honest: does your son, daughter, or niece have the genuine passion and skill to take over? Research often shows that a staggering 70% of family businesses don’t make it to the second generation. It’s rarely about profitability; it’s almost always about a lack of real planning.

Think about:

- The upside: A powerful legacy, cultural continuity, and the potential for flexible payment arrangements.

- The risks: Family conflict is a huge one. How do you treat non-involved children fairly? Is the heir apparent truly the best person for the job?

A smart strategy we often implement with clients is “estate equalisation.” This involves leaving the business to the child who runs it, but using other assets, like life insurance proceeds, to provide an inheritance of equal financial value to their siblings. It’s a practical way to keep things fair and avoid future resentment.

Selling to Your Management Team

A Management Buyout (MBO) can be a fantastic solution. You’re selling to a team that already lives and breathes your business. They know the clients, the culture, and the operational quirks. This massively de-risks the transition and rewards the people who helped you succeed.

The biggest challenge here is almost always money. Your key managers probably don’t have the cash sitting around to buy you out at full market value. This is where vendor financing often comes into play, where you lend them a portion of the sale price, which they pay back over several years out of the company’s profits.

Pursuing a Strategic Trade Sale

A trade sale means selling to another company, often a larger competitor or a supplier in your industry. This option almost always delivers the highest price tag. The buyer isn’t just buying your profits; they’re buying a strategic advantage—your customer base, market footprint, or unique technology.

The trade-off is that your business’s identity will likely disappear as the acquiring company absorbs your brand, culture, and operations into its own. For an owner who is deeply connected to what they’ve built, this can be a tough pill to swallow, no matter how big the cheque.

Finding an External Third-Party Buyer

The final route is selling on the open market to a third party, like a private equity firm or another entrepreneur. This throws the net wide, creating the largest possible pool of potential buyers and potentially a better price.

Be warned: this process is intense. Your business will be scrutinised under a microscope during due diligence. Your financials, contracts, and internal processes have to be bulletproof. It’s a purely commercial, arm’s-length transaction focused squarely on the numbers.

Each of these pathways dramatically impacts your personal wealth and retirement plans. How the deal is structured, when you get the cash, and the tax implications all need careful modelling. This is exactly where our Retirement Roadmap service makes a difference. We align your business exit with your personal financial blueprint, making sure the proceeds of your life’s work actually fund the retirement you’ve earned.

Choosing your exit is more than a business decision—it’s a life decision. To talk through which of these paths might be the right fit for you, an initial call with our team can provide the clarity you need.

Navigating the Financial and Legal Maze

You’ve chosen your successor—a massive milestone. But now comes the part that can feel daunting: tackling the numbers and the paperwork to make it all official, secure, and tax-efficient.

This is where the true value of your life’s work is either protected or eroded. Getting the financial and legal framework right is what turns a business asset into personal wealth, funding the next chapter of your life.

Minimising Your Tax Burden

The minute you sell your business, the Australian Taxation Office (ATO) sees a Capital Gain, and they’ll be ready to take their share through Capital Gains Tax (CGT). Without a solid plan, a surprisingly large chunk of your sale proceeds can disappear in tax.

Thankfully, the government has created powerful small business CGT concessions to help owners unlock their wealth for retirement. These can be a game-changer.

Here are the four key concessions that could dramatically reduce, or even completely wipe out, your tax bill:

- The 15-Year Exemption: If you’ve owned the business for at least 15 years, are over 55, and are retiring, you might not pay any CGT at all.

- The 50% Active Asset Reduction: This allows you to instantly cut the capital gain on a business asset by 50%.

- The Retirement Exemption: You can shield up to a lifetime limit of $500,000 in capital gains from tax. If you’re under 55, that amount just needs to be paid into your super fund.

- The Rollover Concession: This lets you put the tax bill on hold for at least two years, giving you breathing room to find a replacement asset or plan your next move.

Be warned: you don’t get these concessions automatically. Strict rules apply, like your business needing an annual turnover below $2 million or having net assets under $6 million. Working with an adviser is essential to make sure you tick all the right boxes and structure the sale for the best possible tax outcome.

Channelling the Proceeds into Your Retirement

Once you’ve protected your sale proceeds from the taxman, the next job is to put that capital to work for your future. For most business owners, this means moving the funds into superannuation—the most tax-effective vehicle for growing your retirement nest egg in Australia.

This is a central part of our Guided Growth service at Wealth Collective. It’s not just about getting the best price; it’s about having a concrete plan for how that money will fund the life you actually want to live post-business. By strategically contributing your sale proceeds into super, you take advantage of low tax rates on investment earnings and can eventually access a tax-free income stream in retirement.

Solidifying Your Legal Foundations

When it comes to handing over a business, a handshake deal is a recipe for disaster. You need airtight legal documents that protect everyone involved and leave no room for ambiguity. This is your best defence against future disputes and costly litigation.

Your legal team will handle the drafting, but you need to be across the essential documents that form the bedrock of your plan.

Key Legal Documents for Your Succession Plan

| Document | Purpose |

|---|---|

| Buy-Sell Agreement | Think of this as the rulebook for the exit. It’s a binding contract that spells out exactly what happens when an owner leaves due to retirement, death, or disability. It sets a pre-agreed valuation method, preventing arguments and ensuring a fair and orderly transfer of shares. |

| Shareholder or Partnership Agreement | This is the core document governing how the owners work together. It must be updated to reflect the succession plan, clearly defining the rights and responsibilities of both the incoming and outgoing owners. |

| Updated Will and Power of Attorney | Your personal estate plan and your business succession plan must be in perfect sync. If they aren’t, your business shares could get stuck in probate, causing chaos for your family and the business. Find out more about the risks by reading our guide on what happens if you don’t have a will. |

Getting these financial and legal details right isn’t just about ticking boxes. It’s about taking control of your financial future and ensuring the culmination of your life’s work actually secures the future you’ve worked so hard for.

Assembling Your Succession A-Team

Trying to navigate a business exit on your own is one of the most common—and costly—mistakes we see owners make. It’s a complex journey, and going it alone often leads to lost value, missed opportunities, and unnecessary stress.

The smartest thing you can do is build your professional ‘A-Team’. This isn’t just an expense; it’s a strategic investment in securing the best possible outcome.

Think of your succession plan as a blueprint for a house. You need an architect, a plumber, and an electrician all working together. Your advisers are the master tradespeople who ensure the final structure is solid.

The Key Players You Need in Your Corner

Every successful transition relies on three core professionals working together.

- Your Financial Adviser: This is your big-picture strategist. Their job is to ensure your business exit delivers on your personal life goals, answering the question: “What number do I need from this business to fund the retirement I want?”

- Your Accountant: The accountant is your expert on tax and valuation. They are critical for getting your financials in order, maximising access to valuable CGT concessions, and preparing the business for a clean, tax-effective sale.

- Your Lawyer: Your lawyer makes it all legally binding. They draft crucial documents like a watertight Buy-Sell Agreement and ensure the business transition aligns with your personal estate planning, preventing legal battles down the road.

An owner engaging these advisers separately, who never speak to each other, often results in a fragmented plan with dangerous gaps. A coordinated, team-based approach is non-negotiable.

Here at Wealth Collective, we often act as the project manager for the entire succession process. We ensure your A-Team is on the same page, that deadlines are met, and that every decision serves your ultimate personal and financial objectives.

Making the Most of Your Advisory Team

Just hiring a team isn’t the final step. To get real value, you have to manage the process. Be completely transparent about your goals, provide all necessary information, and insist that your advisers collaborate directly.

If you’re wondering where to start, our guide on how to choose a financial adviser offers practical steps for finding the right strategic partner for your journey. The quality of your team will have a direct impact on the quality of your exit.

Your Succession Planning A-Team Roles and Responsibilities

| Adviser | Primary Role | Key Contribution To Your Plan |

|---|---|---|

| Financial Adviser | The Strategist: Aligns the business exit with your personal wealth and retirement goals. | Models financial outcomes of different sale options. Plans how to invest the proceeds. Acts as the central point of contact for the advisory team. |

| Accountant | The Tax Expert: Manages the financial and tax components of the transaction. | Conducts a professional business valuation. Structures the sale to maximise CGT concessions. Prepares financial statements for due diligence. |

| Lawyer | The Drafter: Ensures the entire process is legally sound and binding. | Drafts and reviews the Buy-Sell Agreement. Updates shareholder agreements. Aligns the business plan with your personal Will and estate documents. |

Building this team creates an incredible support structure. It replaces uncertainty with the clarity and confidence of a well-managed project. With the right experts in your corner, you can finally move forward, knowing every detail has been handled and your legacy is secure.

Your Succession Planning Questions, Answered

When business owners first sit down with us at Wealth Collective to talk about their exit strategy, the same handful of questions almost always surface. It’s a massive topic, and it’s completely normal to have a lot on your mind.

Let’s tackle some of the most common ones we hear every day.

How Long Does Business Succession Planning Actually Take?

Honestly? Longer than most people think. This isn’t something you can knock over in a few months.

For a well-structured plan, you should be thinking in terms of 2 to 5 years from start to finish. For more complex businesses or family transfers, it can take closer to 10 years.

The timeline depends on the business’s complexity, your successor’s readiness, and the legal and tax structuring required. The single biggest gift you can give yourself is time. Starting early provides the breathing room to get a proper valuation, mentor your successor, and make smart use of tax concessions. Rushing it will almost always leave money on the table.

What’s the Single Biggest Mistake to Avoid?

Without a doubt, the most damaging mistake we see is simply leaving it too late. So many owners treat succession as a single event tied to retirement, not as the long-term business strategy it truly is.

Putting it off forces a rushed sale under pressure, leading to a lower valuation and fewer options. A close second is failing to communicate the plan clearly with family and key managers.

Secrecy breeds uncertainty and conflict, which can unravel the very legacy you’re trying to protect. A clear, well-communicated plan is a powerful tool for giving everyone peace of mind.

How Do I Make Sure the Business Can Run Without Me?

This is the end game. The ultimate goal of any great succession plan is to make yourself redundant, shifting from day-to-day operator to strategic guide.

Getting there involves a few key disciplines:

- Write the Playbook: Document everything. Your critical processes, from sales to operations, need to be written down so someone else can follow the map.

- Delegate Real Authority: Truly empower your team. Give them the autonomy to make decisions, and then let them make them.

- Develop Your Successor: This can’t be left to chance. A structured development plan is essential to groom your replacement for real leadership.

A huge part of this is building a financial safety net for the business itself. As part of our Wealth Collective process, we help clients implement Protection Plus plans using tools like key person insurance. This policy is designed to shield the business from the financial shock of losing you or another vital team member, ensuring stability right when it’s needed most.

A well-executed succession plan is the final, and arguably most important, act of a successful business owner. It doesn’t just secure your financial future; it protects the legacy you’ve spent a lifetime building.

To start turning your ‘one day’ exit into a concrete, actionable plan, let’s have a chat. Book an initial call with the team at Wealth Collective today and we can help you navigate every step with clarity and confidence.