Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Choosing the right super fund is one of the most critical financial decisions you’ll ever make. It’s not just an administrative task to tick off when you start a new job; it’s about choosing the engine that will power your retirement. At Wealth Collective, we see that getting this right from the start can put you decades ahead financially.

Why Your Super Fund Is Your Most Important Financial Move

For too many Australians, super is an afterthought—a “set and forget” account that just gets topped up with each payslip. But that passive approach can be incredibly costly. Taking a hands-on role in setting up a superannuation fund that genuinely fits your life and goals is the difference between a comfortable retirement and just getting by.

This isn’t about becoming a stock market guru overnight. It’s about making a few smart, informed choices now. Whether you’re in your 20s and just starting out, a high-income earner looking to maximise your nest egg, or approaching retirement, the fund you choose is the bedrock of your long-term wealth.

The Real Power of Proactive Super Management

Let’s talk numbers for a moment. The Australian superannuation industry is colossal. As of September 2025, total super assets hit $4.5 trillion, a 9.4% jump from the previous year. In that year alone, contributions soared to $215.6 billion. You can dig into these figures yourself over on the APRA website.

What does that mean for you? It means you have a chance to get your piece of a very large, growing pie. By actively managing your super, you can unlock some serious advantages:

- Better Investment Returns: You can move beyond the default option and select an investment strategy that matches your timeline and comfort with risk.

- Lower Fees: It sounds small, but even a 0.5% difference in fees can add up to tens or even hundreds of thousands of dollars over a lifetime.

- Smarter Insurance: Default insurance is often a one-size-fits-all solution. You can tailor your life, TPD, and income protection cover to what your family actually needs.

- Tax Efficiency: Super is a tax-friendly world. The right setup helps you make the most of those benefits to grow your money faster.

Don’t underestimate the impact of being engaged. The gap between a default super account and a well-managed one can easily be hundreds of thousands of dollars by the time you retire. It’s the single biggest lever most of us have to pull for our financial future.

Here at Wealth Collective, we help clients cut through the noise. Our job is to translate the jargon and complexity into a simple, clear plan that works for you. We start by understanding where you are now and where you want to be. For a quick refresher, our guide on what superannuation is in Australia is a great place to start.

Taking that first step is often the hardest part, but it doesn’t have to be. A quick, no-obligation chat with one of our advisers can give you a personalised perspective and get you on the right track from day one.

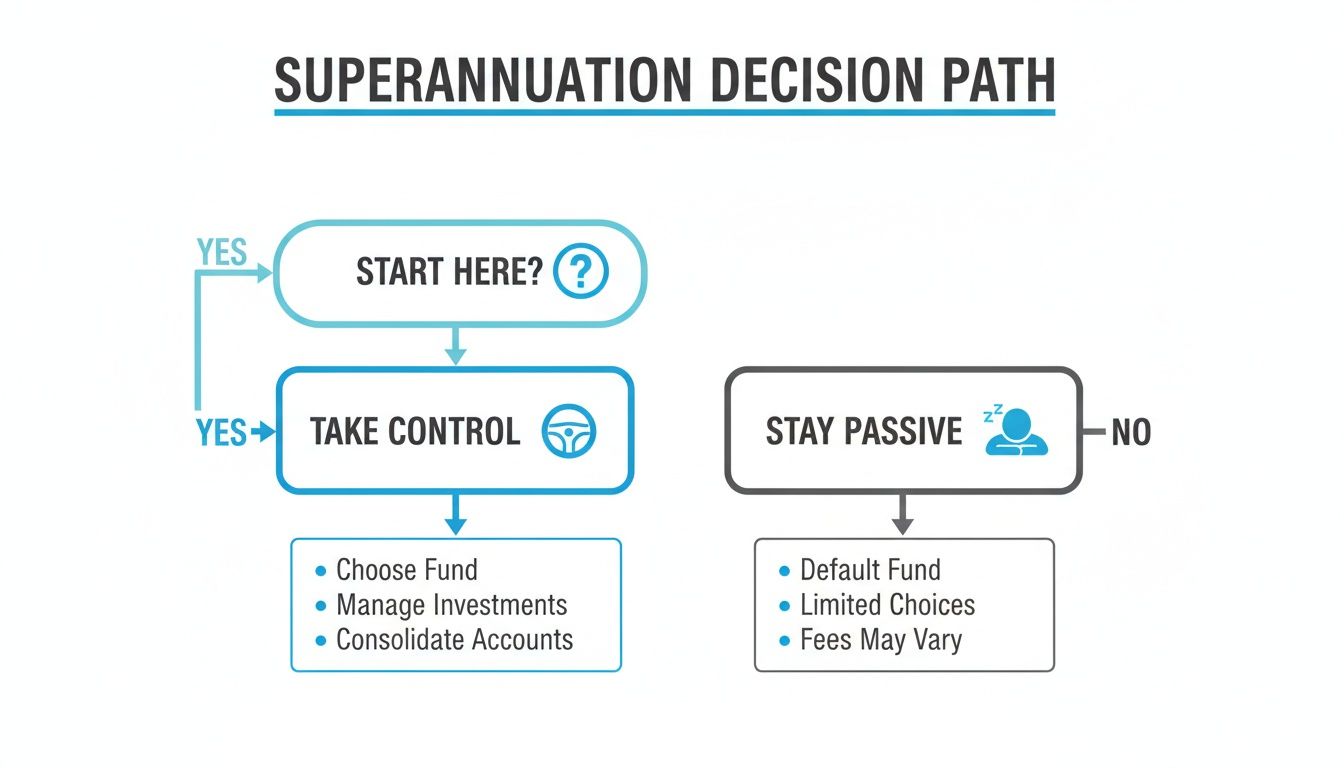

Choosing the Right Super Fund Structure for You

Before you do anything else with your super, you have a fundamental choice to make. It’s not just about picking a fund with a fancy name; it’s about choosing the type of fund that truly aligns with your life, your career, and how hands-on you want to be.

Getting this wrong can be a costly mistake. You could end up paying higher fees than you need to or being stuck in an investment strategy that doesn’t match your goals. The Australian super system offers a few distinct paths, each built for a different kind of person. Understanding them is your first real step toward taking control.

This decision is often the first big fork in the road. Are you someone who’s happy to let the experts handle it, or do you want to be in the driver’s seat?

As the flowchart shows, it really boils down to two philosophies: a professionally managed, “set-and-forget” approach, or taking complete control yourself. There’s no single right answer—it all depends on your financial situation, your risk appetite, and frankly, how much time you’re willing to commit.

Superannuation Fund Types at a Glance

To help you see the differences side-by-side, here’s a quick comparison of the main fund structures. Think about where you fit as you review the options.

| Fund Type | Best For | Key Feature | Average Balance | Consideration |

|---|---|---|---|---|

| Industry Fund | Most people, cost-conscious investors | Run to profit members, historically low fees and strong returns. | $97,294 | Can have less investment choice compared to other types. |

| Retail Fund | Those wanting more investment choice or advice | Wide range of investment and insurance options, often linked to banks. | $140,306 | Fees can be higher, so you need to weigh up the benefits. |

| Public Sector Fund | Government employees | Known for reliability, competitive fees, and sometimes defined benefits. | $236,428 | Membership is usually restricted to public sector workers. |

| SMSF | High-net-worth individuals, business owners | Complete control over investments, including direct property. | $849,678 | High responsibility, complex compliance, and requires a large balance to be cost-effective. |

Each of these structures serves a purpose. Your job is to find the one that best serves you.

APRA-Regulated Funds: The Popular Choice

Most Australians have their super in what’s known as an APRA-regulated fund. This category includes Industry, Retail, and Public Sector funds. Think of them as the “managed for you” option, where a professional trustee makes the big investment decisions for all members.

-

Industry Funds: These are the classic “profit for member” funds. They’ve built a reputation for low fees and solid long-term performance, making them a popular choice for young professionals and cost-conscious investors.

-

Retail Funds: Offered by big financial names like banks, these funds often give you a much wider menu of investment and insurance choices. The flexibility and platform features can be a major drawcard for those wanting more options.

-

Public Sector Funds: As the name suggests, these are primarily for government employees. They are well-regarded for their reliability and competitive fee structures. Some even still offer defined benefits, a rarity these days.

The numbers tell the story. Industry funds alone hold 14.35 million accounts, grabbing 50% of the market share. Retail funds, while serving fewer accounts, tend to have a higher average balance of $140,306. And with an impressive average balance of $236,428, public sector funds look after 15% of the nation’s super assets.

The bottom line? An APRA-regulated fund is a straightforward, effective choice for most people. You delegate the day-to-day work to the experts, freeing you up to focus on everything else.

Self-Managed Super Funds (SMSF): The Path to Control

On the other end of the spectrum is the Self-Managed Super Fund, or SMSF. This is for the person who wants ultimate control. With an SMSF, you are the trustee. You make every investment call and you’re personally responsible for keeping the fund compliant with the law.

A perfect example is a small business owner who sets up an SMSF to buy their own commercial premises. The business then pays rent directly into the super fund. It’s a powerful wealth-building strategy, but it demands serious expertise and a large starting balance to make financial sense.

While SMSFs account for a small number of total super accounts, they hold a massive 25% of all superannuation assets. The average SMSF balance is a hefty $849,678, attracting savvy investors who want to call the shots. If you’re curious, we’ve laid out the good, the bad, and the ugly in our detailed guide on the pros and cons of a self-managed super fund.

Deciding between a managed fund and an SMSF is one of the biggest financial decisions you’ll make. The stakes are high, and this is where getting expert advice is non-negotiable.

At Wealth Collective, our Guided Growth service is designed specifically to bring clarity to this choice. We dig into your complete financial picture—your income, your goals, your risk tolerance—to identify the structure that will set you up for success, not just for today but for the long haul.

Book an initial call with us to see how we can help you navigate this choice with confidence.

Getting It Right: Your Legal & Compliance Duties

You’ve picked a fund type. Now comes the part where your legal responsibilities really crystallise.

If you’ve gone with a standard Industry or Retail fund, most of the heavy lifting is handled for you. These are APRA-regulated funds, meaning a professional trustee is legally on the hook to manage everything in your best interests. They deal with all the tricky compliance with APRA and the ATO, so you don’t have to.

But if you’re venturing down the path of a Self-Managed Super Fund (SMSF), you’re personally stepping into that trustee role. This isn’t a hat you can wear lightly. It’s a serious commitment with significant legal weight, and the ATO—your regulator—is watching closely. Getting this wrong can bring some eye-watering penalties.

The Essential Legal Foundations of an SMSF

Before a single dollar can be rolled over or contributed, your SMSF needs a rock-solid legal framework. This isn’t just bureaucratic box-ticking; it’s the very foundation that makes your fund legitimate and keeps you out of trouble from day one.

The first crucial piece of the puzzle is the trust deed. Think of this as the constitution for your fund. It lays out all the rules, from who can be a member to how and when benefits can be paid. This is a highly specialised legal document, and using a generic template is a recipe for disaster. It needs to be drafted by a specialist to comply with super laws and give you the flexibility you might need later, like the ability to borrow for an investment.

Next, you have to appoint your trustees. You’ve got two main choices for how to structure this:

- Individual Trustees: Simple enough—all members of the fund are also the individual trustees. It’s often quicker to set up, but it can create administrative headaches later on, particularly when a member joins, leaves, or passes away.

- Corporate Trustee: This involves setting up a special purpose company to act as the trustee, with all fund members serving as directors of that company. Yes, there’s an upfront cost, but this structure provides far better asset protection and makes administrative changes (like adding a new member) a much cleaner process.

With your trust deed and trustee structure sorted, the final step is registering the fund with the ATO to get an Australian Business Number (ABN) and a Tax File Number (TFN). Only then is your fund officially ‘live’.

Understanding Your Core Duties as a Trustee

Becoming an SMSF trustee means you have a legal duty to every single member—even if it’s just you and your spouse. Every decision you make is governed by two iron-clad principles.

The first is the sole purpose test. This is non-negotiable. Your fund must exist for the sole purpose of providing retirement benefits for its members (or their dependants if a member dies). Using the fund to buy a holiday house you plan to use, or lending money to a relative, is a massive breach of this rule.

Acting as a trustee is a significant responsibility. The ATO expects you to act with care, skill, and diligence. Breaching your duties can result in personal fines of up to $1.1 million for the most serious offences, and your fund could lose its concessional tax status.

The second principle is that you must always act in the best financial interests of all members. This means every investment decision has to be made with the clear goal of growing their retirement nest egg. You formalise this through your fund’s investment strategy—a written document you’re required to create and review regularly, covering risk, diversification, returns, and cash flow needs.

Navigating these legal hoops is precisely where getting the right advice is so critical. As part of our process, Wealth Collective helps you weigh up whether an SMSF is the right move and guides you through every step of setting it up correctly. We connect you with legal experts to ensure your trust deed is robust and your structure is sound, protecting you from compliance pitfalls.

book a complimentary introductory call today and we can show you exactly how to build your fund the right way.

Building Your Investment Strategy for Growth

Alright, you’ve jumped through the hoops to get your fund legally set up. Now for the exciting part—actually putting your money to work. This is where we move from paperwork to performance, creating a deliberate investment plan for the long haul.

There’s no single “best” way to grow a super balance. Your strategy needs to be shaped by your own life stage, your income, and how far away retirement is. A young professional will have completely different goals—and a different tolerance for risk—than someone just a few years away from finishing work.

Age and Ambition: Two Common Scenarios

Let’s look at a couple of real-world examples. Picture a 30-year-old professional. With decades ahead of them, they can afford to take on more risk for the chance of much higher returns. Their focus should be squarely on aggressive growth, making sure they’re capturing all their employer contributions and perhaps even using salary sacrificing to give their balance a serious boost.

Now, contrast that with a 55-year-old executive. They’re in the final stretch. While growth is still important, their main concern is protecting the capital they’ve already built. They’re probably using catch-up concessional contributions for one last push. Their investment mix will naturally be more balanced, designed to lock in their gains and shield them from market volatility.

Balancing Growth and Defensive Assets

Every solid investment strategy comes down to finding the right blend of growth assets and defensive assets. This mix will ultimately determine your long-term returns and how bumpy the ride is along the way.

-

Growth Assets: Think of these as the engine of your portfolio, aimed at capital appreciation. This includes things like Australian and international shares and direct property. They offer the biggest potential for growth but also come with more volatility.

-

Defensive Assets: These are your portfolio’s stabilisers, providing a cushion and reliable income. We’re talking about cash and fixed interest investments, such as government and corporate bonds. They won’t shoot the lights out with returns, but they are essential for protecting your nest egg when the markets get choppy.

The right mix for you comes down to your personal comfort with risk and your investment timeline. An investor in their 20s or 30s might feel comfortable with an 80-90% allocation to growth assets. Someone on the cusp of retirement, however, might dial that right back to 50% or even less.

I’ve seen it time and time again—the power of a disciplined, long-term approach is undeniable. Markets go up and down, but staying invested in a well-diversified portfolio consistently delivers results over the years. The secret is building a strategy you can actually stick with.

The numbers back this up. In the year to June 2025, the median Growth fund (with 61-80% in growth assets) delivered a strong 10.5% return. That marked the 14th positive return in 15 years. You can get a deeper dive into these figures with this in-depth analysis of super fund returns.

Diversification: The Only Free Lunch in Investing

If there’s one principle that’s non-negotiable, it’s diversification. You’ve heard it before, but it bears repeating: never put all your eggs in one basket. Spreading your money across different asset classes (shares, property, bonds), regions (Australia, US, Europe, Asia), and industries (tech, healthcare, resources) is the smartest move you can make.

This is how you smooth out your returns. When one corner of your portfolio is struggling, another is likely performing well, creating a much more stable and predictable path to growing your wealth. It’s a fundamental part of setting up a super fund that can weather any economic storm.

This is exactly where professional guidance can make all the difference. Designing an investment strategy that truly reflects your goals, timeline, and risk profile is the core of what we do in Wealth Collective’s Retirement Roadmap service. We don’t just pick funds for you; we design a complete, tailored investment plan from the ground up to put your money to work intelligently.

To see how we can map out a plan to accelerate your wealth creation, book a complimentary introductory call today.

Looking Beyond Investments: Insurance, Fees, and Tax

Your super is much more than just a savings account for retirement. When set up correctly, it becomes a financial fortress—protecting your family while growing your wealth in an incredibly tax-friendly way. But many people get caught up in chasing investment returns and overlook three critical areas: insurance, fees, and tax.

Getting these elements wrong can quietly sabotage your future. Let’s break down how to manage them.

Is Your Family Genuinely Protected? A Hard Look at Insurance in Super

Most super funds give you some default insurance cover straight out of the box. Relying on it is one of the biggest financial traps we see.

This basic cover usually includes a mix of:

- Life Insurance (Death Cover): A lump sum for your loved ones if you die.

- Total and Permanent Disablement (TPD): A payout if a serious injury or illness stops you from ever working again.

- Income Protection: Replaces a portion of your income if you’re temporarily off work due to sickness or injury.

The problem? This default cover is generic. It’s a one-size-fits-none amount that has no idea about your mortgage, your kids’ school fees, or the lifestyle your family is used to. It creates a false sense of security, often leaving a devastating gap between what your family would get and what they’d actually need. You can dive deeper into these options by understanding the main types of life insurance.

This is a critical part of our Protection Plus service at Wealth Collective. We don’t just accept the default. We conduct a detailed needs analysis to ensure your insurance cover inside and outside of super is precisely what your family requires to maintain their lifestyle, no matter what happens.

The Silent Killer of Your Retirement Nest Egg

Fees. They look so small on your annual statement, but they are the silent killer of retirement wealth. Over 30 or 40 years, the corrosive damage they do is staggering.

The difference between a fund charging 1.5% and one charging 1.0% a year might sound trivial. It’s not. It’s life-changing.

Let’s put it in real numbers. Say you’re 35 with a $150,000 super balance. If your fund averages a 7% return over the next 30 years, that tiny 0.5% difference in fees will cost you over $120,000 by retirement. That’s a new car, a few overseas holidays, or years of extra financial freedom—gone.

That’s why digging into the fee structure is a non-negotiable step. You need to know exactly what you’re paying in administration fees, investment fees, and any other hidden costs.

Making the Tax Man Work for You

Now for the good news. Australia’s superannuation system is one of the most generous tax environments you’ll ever find. If you know how to use it, you can seriously accelerate your wealth.

The magic comes from a few key advantages:

- Investment earnings inside super are taxed at a maximum of just 15%, a huge discount for most people compared to their marginal tax rate.

- Concessional contributions (like your employer’s payments or salary sacrificing) are also taxed at 15%, a massive upfront tax saving for many.

- Once you turn 60 and switch to a pension, things get even better. Your investment earnings and any income you draw become completely tax-free.

This isn’t a “set and forget” task. Optimising your insurance, keeping fees low, and making the most of these tax rules requires regular attention. Getting professional advice ensures all these moving parts are working together, turning your super from a simple savings pot into a powerful wealth-creation engine.

Ready to make sure your super is working as hard as it can for you? Book an initial call with us and we’ll help you get a clear picture of how to optimise your fund for the future.

What’s Next? Putting Your Super Plan Into Action

We’ve covered a lot of ground, from the nuts and bolts of choosing a fund to the finer points of investment strategy and legal duties. It can feel like a mountain of information, and that’s perfectly normal.

The goal isn’t to become an overnight expert. It’s to feel equipped enough to make your next move with confidence.

At Wealth Collective, our whole approach is built around turning this complexity into a clear, stress-free plan for you. We want you to feel empowered to make confident decisions about your financial future.

So, where do you go from here? The most direct path forward is a quick, complimentary 10-minute chat with one of our award-winning advisers. It’s a completely informal, no-obligation call designed to give you a personal perspective on your own situation.

It’s your chance to ask those specific questions that have been on your mind and see what professional guidance could look like for you. Instead of letting this sit on your to-do list, schedule your call and turn what you’ve learned into concrete action.

Your Super Fund Setup Questions, Answered

When you start digging into superannuation, it’s natural for a bunch of questions to pop up. Whether you’re thinking about starting an SMSF or just trying to get your existing super sorted, getting straightforward answers is the first step. Here are a few of the most common queries we tackle for clients every day.

How Do I Pull All My Old Super Funds into One Place?

If you’ve had a few jobs over the years, you probably have a few super accounts floating around. Bringing them all together is one of the simplest and most effective things you can do.

The quickest method is usually through your myGov account, which links to the ATO. The platform helps you track down any lost super and lets you consolidate it into your main fund with just a few clicks. Your new fund will also have a rollover form you can fill out. Getting this done is non-negotiable—paying multiple sets of admin fees is a sure-fire way to drain your nest egg. It also gives you a single, clear picture of your savings, making everything much easier to manage.

Individual vs. Corporate Trustee for an SMSF: What’s the Real Difference?

Choosing your trustee structure is a big deal when setting up a Self-Managed Super Fund (SMSF). With an individual trustee structure, every member is a trustee. It’s often cheaper and faster to set up initially, but it can get messy down the track. All fund assets have to be held in the names of every single member, which can be a real headache.

A corporate trustee, on the other hand, means you set up a special-purpose company to act as the trustee. Yes, there’s a higher upfront cost, but it offers far better asset protection and makes the admin work a breeze. For example, if a member joins or leaves, you just update the company directorship—you don’t have to retitle every single asset. It’s the go-to structure for long-term flexibility.

How Much Say Do I Really Get Over Investments in a Public Fund?

While you don’t have the granular control of an SMSF, most industry and retail funds offer a lot more investment choice than people realise. You’re definitely not stuck with the default ‘Balanced’ option if it doesn’t suit you.

Most major funds now provide a “member direct” or choice menu, which lets you build a portfolio from the ground up. You can typically pick and choose from different asset classes, such as:

- Australian Shares

- International Shares

- Listed Property

- Fixed Interest and Bonds

- Cash

This gives you a great middle ground—you can align your investments with your personal risk tolerance without taking on the heavy legal and admin burden of an SMSF.

When Should I Seriously Consider Setting Up an SMSF?

An SMSF is a massive commitment, and it’s certainly not for everyone. The right time to consider one is when you have both the means and the motivation. Financially, you’d want a substantial balance—most advisers suggest a starting point somewhere between $200,000 and $500,000 to make the running costs worthwhile.

But the real deciding factor is your desire for control. An SMSF makes sense if you want to invest in specific assets like direct property or unlisted businesses, and you’re prepared to take on the full legal responsibility of being a trustee. It’s a decision that should always be made after a serious chat with a financial professional.

Getting answers to these questions is a great start, but a truly successful strategy is built on a personalised plan. At Wealth Collective, our award-winning advisers specialise in turning these complex choices into clear, confident actions.

If you’re ready to stop guessing and start building, book a complimentary 10-minute introductory call. Let’s figure out the next steps for your wildly successful financial life, together.