Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Think of your finances like a river. Cash flow is the current that keeps everything moving—money comes in like rainfall and flows out to cover your daily costs. Real cash flow management is all about learning to guide that current, making sure it nourishes your financial goals instead of flooding your budget or drying up when you least expect it.

What Is Cash Flow and Why It Matters for Your Finances

Put simply, cash flow is the movement of money into and out of your bank account. It’s a straightforward idea, but getting it right is the single most important factor for your financial wellbeing. Understanding and controlling this flow is what separates feeling stressed about money from feeling confident and in control.

Your income—whether from a salary, business revenue, or investments—is your inflow. Your expenses—like rent, groceries, loan repayments, and tax—are your outflow. When more money is consistently coming in than going out, you have a positive cash flow. This surplus is the fuel for every single one of your financial goals.

The Foundation of Financial Success

Trying to build wealth without a clear picture of your cash flow is like trying to follow a map in the dark. You might feel busy and like you’re making an effort, but you have no real way of knowing if you’re heading in the right direction.

Effective cash flow management isn’t about trying to stop your spending completely. It’s about building channels to direct your money where it can do the most good, preventing droughts (running out of cash) and floods (uncontrolled spending).

When you truly get a handle on your cash flow, you can:

- Reduce Financial Stress: Knowing exactly where your money goes eliminates that awful anxiety of surprise bills or coming up short at the end of the month.

- Pay Down Debt Faster: By identifying where you have a surplus, you can strategically make extra repayments on high-interest debts, saving yourself thousands over time.

- Invest with Confidence: A consistent, positive cash flow is what allows you to make regular contributions to your superannuation and other investments, letting your wealth compound.

- Achieve Major Life Goals: Whether it’s saving for a home deposit, that dream holiday, or an early retirement, your cash flow is the engine that will get you there.

A Critical Skill for Individuals and Businesses

This isn’t just a concept for big corporations; it’s absolutely vital for families, individuals, and especially for small business owners. In fact, cash flow has become the number one worry for small businesses, with 43 per cent of owners naming it their main challenge. This shows just how crucial it is to get this right in our current economic climate.

For a business, poor cash flow can mean being unable to pay staff or suppliers, even if the business looks profitable on paper. For a family, it means living from one pay cheque to the next, never quite getting ahead to build an emergency fund or plan for the future.

At Wealth Collective, we see cash flow management as the cornerstone of all good financial advice. By first creating a clear, actionable plan, we help our clients direct their resources effectively. This proactive approach paves the way for building lasting wealth and achieving financial freedom, and it all starts with a simple call to map out your journey.

The Hidden Costs of Unmanaged Cash Flow

When we talk about poor cash flow, it’s easy to think of it as just a numbers problem—a shortfall on a spreadsheet. But the reality is far more personal. It’s that constant, low-level hum of anxiety in the back of your mind as you tap your card, wondering if you’ve budgeted correctly.

It’s the feeling of being perpetually one unexpected car repair or medical bill away from a genuine crisis. For so many Australians, this is the exhausting cycle of living pay cheque to pay cheque. The relief of payday is quickly swallowed by the stress of watching the account balance dwindle, leaving little room for savings, let alone long-term dreams.

The Toll on Personal and Business Finances

This strain can be particularly crushing for small business owners. I’ve spoken with countless entrepreneurs who’ve spent sleepless nights agonising over whether to pay themselves or make sure their staff and suppliers are looked after. This isn’t just a business decision; it’s a deeply personal one that takes a heavy toll.

And it’s a widespread issue. Recent data shows a staggering 80 per cent of Australian small to medium businesses have felt the pinch of cash flow problems. To keep the doors open, 27 per cent of these owners admitted to dipping into their own savings or forgoing a salary entirely. You can see more details in this analysis of cash flow challenges for Australian businesses.

A business can be profitable on paper and still fail because it runs out of cash. This illustrates the critical difference between profit and cash flow—profit is an accounting concept, but cash is the real money you need to operate day-to-day.

This constant juggling act doesn’t just impact the business’s bottom line; it comes with significant personal and emotional costs that we don’t talk about nearly enough.

The Emotional Price of Financial Instability

The fallout from poor cash flow ripples through every part of your life, well beyond your bank account.

- Pervasive Stress and Anxiety: The mental load of constantly worrying about money is draining. It can seriously affect your health, your focus at work, and your relationships.

- Strained Relationships: Money is one of the biggest sources of friction for couples. When things are tight, even small disagreements about spending can escalate into major arguments.

- Lost Opportunities: A lack of cash on hand means you miss out. That could be a smart investment opportunity, a well-deserved family holiday, or the chance to hire a key person to grow your business.

- Decision Fatigue: When every single financial choice feels like it carries immense weight, you eventually burn out. This exhaustion makes it even harder to find the energy to create a positive cash flow management plan.

Building financial resilience is the only real antidote to this kind of stress. This is where having a trusted partner can completely change the game. At Wealth Collective, our Protection Plus service is designed specifically to help you build that financial buffer, giving you the confidence to handle whatever life throws your way. By creating a safety net, we help turn financial anxiety into financial security.

Your journey towards a less stressful financial life can start with a simple, no-obligation introductory call to see how we can help.

Practical Steps to Master Your Personal Cash Flow

Knowing the theory is one thing, but taking decisive action is where real financial progress happens. It all comes down to building simple, sustainable habits that put you firmly in control of your money.

Forget the idea that managing your cash flow is about extreme penny-pinching. It’s actually about making sure your money is working for you and aligned with the life you want to build. Let’s walk through the practical steps to get you started.

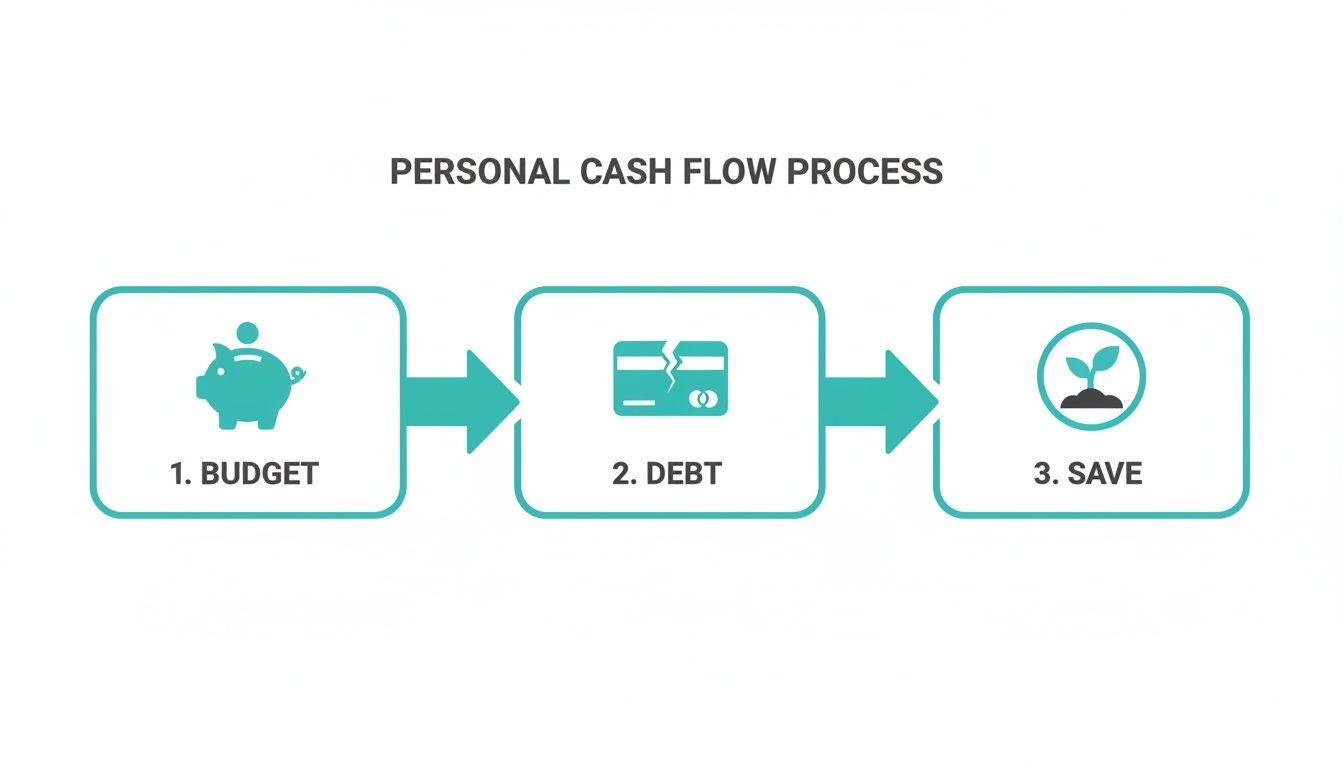

The process boils down to three core actions: creating a budget, getting on top of your debt, and building your savings.

Think of this flow—budget, reduce debt, save—as the engine for creating wealth. When you master these three areas, you kickstart a positive financial cycle that fuels your future.

Create a Budget That Empowers You

Let’s be honest, the word “budget” can make you think of a restrictive financial diet. A much better way to see it is as a spending plan—a tool that gives every dollar a specific job. The goal isn’t just to track where your money goes, but to intentionally direct it toward what truly matters to you.

A great first step is to simply track your income and expenses for one month. Use a basic spreadsheet or your favourite app to get a clear picture of your spending habits. You’ll probably be surprised by the small, recurring costs that add up and could easily be redirected elsewhere.

Once you know the numbers, you can create a simple plan:

- Cover your necessities: Allocate funds for the non-negotiables like your mortgage or rent, utilities, groceries, and transport.

- Pay your future self: Dedicate a specific portion of your income to savings, investments, or extra debt repayments. This is crucial.

- Leave room for life: A budget with no space for fun is a budget you won’t stick with. Make sure you set aside money for lifestyle spending so you don’t feel deprived.

This simple structure shifts your cash flow from something that just happens to you into a powerful tool you consciously control.

Choose Your Debt Reduction Strategy

High-interest debt from credit cards or personal loans is one of the biggest roadblocks to a healthy cash flow. Tackling it aggressively frees up hundreds, or even thousands, of dollars each year that you can then put towards building wealth instead of paying interest.

Two of the most popular and effective strategies are the ‘avalanche’ and ‘snowball’ methods.

Tackling debt isn’t just about paying back what you owe; it’s about reclaiming your future income. Every dollar of debt you clear is a dollar you can invest in your own goals.

The right strategy for you really depends on what motivates you:

- The Avalanche Method: With this approach, you throw every spare dollar at the debt with the highest interest rate first, while making minimum payments on everything else. Mathematically, this saves you the most money in interest over time.

- The Snowball Method: Here, you focus on paying off the smallest debt first, regardless of the interest rate. The psychological boost from clearing a debt completely gives you the momentum to roll that payment onto the next one.

Both methods are proven to work. The most important thing is to pick one and commit to it. A well-managed cash flow is what allows you to make those extra repayments consistently. To learn more about optimising your everyday money, you might find our guide on the benefits of a cash management account helpful.

Build Your Financial Safety Net

An emergency fund is a non-negotiable part of good financial health. This is simply a pool of savings—typically 3-6 months’ worth of essential living expenses—kept in an easy-to-access account. It acts as your financial buffer against life’s inevitable curveballs, like a sudden job loss, a medical issue, or an urgent repair.

Without this fund, an unexpected bill can easily push you into high-interest debt, completely derailing your progress and creating a mountain of stress. Your emergency fund is what protects your long-term investment strategy, ensuring you never have to sell your assets at the wrong time just to cover a shortfall.

These are the exact kinds of practical habits we help our clients build through our Guided Growth service pillar. A Wealth Collective adviser works alongside you to create a personalised system for budgeting, debt reduction, and strategic saving, providing the structure and accountability needed to turn these actions into lasting financial success.

Forecasting and Managing Your Business Cash Flow

For any business owner, cash flow isn’t just a line on a spreadsheet; it’s the very pulse of your operation. It’s the money you need to pay your staff, settle supplier invoices, and jump on opportunities as they arise.

It’s easy to get fixated on profit, but cash is what keeps the lights on day-to-day. A business can look great on paper—turning a healthy profit—but still go under if it runs out of the cash needed to pay its immediate bills. That’s why getting a firm grip on cash flow management is so vital for your company’s survival and your own financial peace of mind.

Why Forecasting Is Your Secret Weapon

Running a business on guesswork is a recipe for disaster. This is where cash flow forecasting comes in. It swaps uncertainty for a clear, forward-looking map of your finances, helping you spot potential shortfalls and make smart decisions long before you’re in crisis mode.

The gold standard for staying ahead is a 13-week rolling cash flow forecast. This involves tracking every dollar you expect to come in and go out, then updating it weekly with actual numbers to keep it sharp and relevant.

Why 13 weeks? It’s the sweet spot. It’s long enough to plan strategically but short enough to be accurate and actionable. It helps you answer the really tough questions:

- Will we have enough cash for payroll next month?

- Can we commit to buying that new equipment in two months?

- When’s the best time to handle our upcoming tax and superannuation bills?

A cash flow forecast is like a weather report for your business finances. It gives you the chance to prepare for storms before they hit and take advantage of the sunny days when they arrive.

Key Metrics to Keep on Your Radar

To build a reliable forecast, you need to track the right numbers. These key performance indicators (KPIs) give you a real-time health check on your business’s financial pulse.

Here are some of the most essential metrics every business owner should be watching.

Essential Cash Flow Metrics for Your Business

| Metric | What It Measures | Why It’s Important |

|---|---|---|

| Days Sales Outstanding (DSO) | The average number of days it takes to collect payment after a sale. | A high DSO means your cash is tied up in unpaid invoices, putting a strain on your working capital. |

| Days Payable Outstanding (DPO) | The average number of days it takes for you to pay your suppliers. | A higher DPO can improve your cash flow, but stretching it too far can damage supplier relationships. |

| Cash Conversion Cycle (CCC) | The time (in days) it takes to convert inventory and other inputs into cash from sales. | A shorter cycle means your money isn’t tied up in the business for long, freeing up cash for growth. |

| Working Capital | Current Assets minus Current Liabilities. | This is the cash you have available to fund your day-to-day operations. A positive figure is crucial. |

| Operating Cash Flow (OCF) | The cash generated from your core business operations, before investments or financing. | This is a true measure of your business’s ability to generate cash on its own. |

Watching these numbers isn’t just an accounting exercise. It’s about understanding the story your finances are telling you, so you can write the next chapter yourself instead of letting circumstances dictate it for you.

Practical Tactics to Boost Your Business Cash Flow

Once your forecast gives you a clear picture, it’s time to take action. This is all about optimising your working capital—the money that circulates through your business every day. Here are a few powerful moves you can make.

Get Paid Faster

The longer your invoices go unpaid, the more pressure you put on your own bank account. If you offer 30-day payment terms, you’re essentially giving your clients an interest-free loan. It’s time to shorten that cycle.

Try these simple strategies:

- Incentivise prompt payment: A small discount, like 2% off if paid in 10 days, can work wonders.

- Use progress payments: For big projects, invoice at key milestones rather than waiting until the end.

- Make paying easy: Modern accounting software with one-click online payment options removes friction for clients.

- Follow up consistently: Automate polite reminders for overdue invoices. A clear process is your best friend here.

Intelligently Manage Your Payments

Gaining control isn’t just about speeding up what comes in; it’s also about strategically managing what goes out. This doesn’t mean avoiding essential costs, but timing them so they don’t catch you by surprise.

Plan for those big, predictable bills like quarterly BAS, superannuation payments, and annual insurance premiums. A great trick is to regularly put money aside into a separate high-interest savings account specifically for these expenses. This turns a looming financial headache into a series of small, manageable steps.

At Wealth Collective, our expertise lies in connecting these business strategies with your personal financial plan. We show you how to use modern accounting tools to build a robust financial foundation, turning smart cash flow management into the engine that drives both your business growth and your family’s wealth. To learn more, check out our guide on small business cash flow management.

Common Cash Flow Mistakes to Avoid

It’s one thing to have a great financial plan, but it’s just as important to know what can trip you up along the way. When it comes to managing your money, there are a handful of predictable mistakes that we see people and businesses make time and time again.

The good news is that because these errors are so common, they’re also entirely avoidable. Spotting these traps is the first step to building a financial foundation strong enough to handle whatever life throws at you.

Overestimating Future Income

This one’s a classic. It’s so easy to start spending against money you don’t have yet—a promised work bonus, a big sales contract that’s almost signed, or a seasonal rush you’re counting on. Relying on uncertain income to cover today’s bills is a gamble that can quickly backfire, leaving you in a serious shortfall if the money comes in late, or worse, not at all.

A much safer approach is to base your budget on your guaranteed, consistent income. Think of any extra cash that comes in as exactly what it is: a bonus. Use it to get ahead by paying down debt, topping up your savings, or making an investment. Just don’t bake it into your regular monthly plan.

Forgetting the Small Leaks

Big, one-off expenses rarely sink a budget on their own. The real culprit is often the slow, silent drain of small, recurring costs you barely even notice. That daily coffee, the handful of streaming services you don’t watch, or the gym membership gathering dust—these “financial leaks” can easily add up to hundreds of dollars a month.

A study by US Bank found that a staggering 82% of businesses that failed cited cash flow issues as a primary cause. This shows just how devastating even seemingly minor financial missteps can become when they’re not managed properly.

Try tracking every dollar you spend for just one month. It can be an eye-opening exercise that clearly shows where your money is going. Once you see the leaks, you can make a conscious choice about what’s adding value to your life and what you can cut to free up cash for the things that truly matter.

Failing to Build a Cash Buffer

Life is full of surprises, and not all of them are good. Without a cash reserve set aside, a single unexpected event like a major car repair, a sudden medical bill, or a dip in business revenue can instantly become a full-blown financial crisis. Reaching for a high-interest credit card or a personal loan in a panic is a mistake that can take years to recover from.

This is why having an emergency fund is non-negotiable. Aim to build a buffer that covers 3-6 months’ worth of essential living expenses. For businesses, a similar cash safety net is crucial for navigating slow periods or covering unexpected costs without going into debt. For more practical advice on this, you can learn more about how to pay off debt faster in our detailed guide.

Mixing Personal and Business Finances

For any small business owner, this is a particularly dangerous habit. When you use your personal credit card for business supplies or dip into the business account to cover household bills, you create a tangled mess. It’s not just an accounting headache; it makes it impossible to know if your business is actually profitable.

The fix is simple but absolutely critical: maintain completely separate bank accounts and credit cards for your business and personal life. This discipline creates clarity, makes tax time infinitely easier, and most importantly, it protects your personal assets if the business runs into trouble.

At Wealth Collective, our advisers help you sidestep these common errors from day one. We work with you to create a structured financial plan that fits your life and goals, ensuring you have the right systems in place to manage your cash flow effectively. Book a no-obligation call today to see how we can help you build, protect, and grow your wealth.

Build Your Financial Future with Wealth Collective

So, you now have a solid grasp of the ‘what’ and ‘how’ behind managing your cash flow. The next logical question is, who can help you put it all into practice? Getting your money in order is about more than just spreadsheets; it’s about having a trusted expert in your corner.

Think of healthy cash flow as the engine that powers everything you want to achieve financially. Our job at Wealth Collective is to help you build, tune, and maintain that engine, ensuring you have a smooth ride toward your goals. We take the principles from this guide and work with you to create a clear, personalised, and actionable strategy. We know that your financial life isn’t static, and neither is our advice.

Mapping Your Goals to Our Services

We’ve designed our services to meet you exactly where you are, whether you’re just starting out, growing your wealth, or planning for the decades ahead.

This table shows how we align our expertise with what matters most to you.

| Your Financial Goal | Relevant Cash Flow Challenge | Wealth Collective Service Pillar |

|---|---|---|

| Create a Financial Safety Net | You worry about unexpected bills or income loss and need a buffer to protect your family and assets. | Protection Plus helps you build resilience by structuring insurance and emergency funds. |

| Actively Build Wealth | You have surplus cash but aren’t sure how to best use it to reduce debt, invest, or save effectively. | Guided Growth provides the framework to make your money work harder through smart investments and debt strategies. |

| Secure a Comfortable Retirement | You want to ensure your cash flow will support your desired lifestyle for the rest of your life without the fear of running out. | Retirement Roadmap crafts a long-term plan to ensure your assets generate the income you need. |

No matter your objective, a solid cash flow plan is the foundation for getting there.

Your Journey to Financial Clarity Starts Now

Taking control of your cash flow is the single most powerful step toward achieving your financial goals. It’s what turns financial anxiety into a feeling of empowerment. With a clear plan, ambiguity becomes action, and stress gives way to security.

We believe the best financial advice starts with a simple, stress-free conversation. It’s about understanding you first, before we even talk about numbers.

That’s why we’ve made the next step incredibly easy. Your path to financial confidence begins with a no-obligation 10-minute introductory call. This is your chance to chat with an experienced adviser, ask your most pressing questions, and discover what a personalised cash flow management strategy can do for you.

Book your free 10-minute call with a Wealth Collective adviser today, and let’s start building your wildly successful financial life, together.

Frequently Asked Questions About Cash Flow Management

Getting a handle on your finances naturally brings up a few questions. We hear them all the time from clients. To give you some clarity, here are our straightforward answers to the most common queries we get about managing cash flow.

How Is Cash Flow Different From Profit?

This is a big one, especially for anyone running a business. It’s easy to confuse the two, but they tell very different stories. Profit is an accounting measure—it’s the figure you get when you subtract all your expenses from your revenue on paper.

Cash flow, on the other hand, is the real money moving in and out of your bank account. You can have a “profitable” month but be unable to pay your bills because your clients haven’t paid their invoices yet. There’s a reason for the old saying: “Revenue is vanity, profit is sanity, but cash is king.” At the end of the day, cash is what keeps the lights on.

How Often Should I Review My Cash Flow?

That naturally leads to the next question: how often should you be checking in? The honest answer is that it depends on your specific situation, but the most important thing is to be consistent.

- For Personal Finances: A monthly check-in is a fantastic rhythm to get into. It’s frequent enough to spot where your spending is going, review your budget, and make small course corrections before they turn into major problems.

- For Small Businesses: We strongly recommend a weekly review. This gives you a tight grip on operations, helps you anticipate large payments, and allows you to update your 13-week rolling forecast so there are no nasty surprises.

What Is the Best Way to Start Managing My Cash Flow?

It can feel overwhelming, but the best first step is surprisingly simple: track everything for one month. Don’t change a thing about your spending habits just yet. Your only job is to record every single dollar that comes in and every dollar that goes out.

This one exercise gives you an unfiltered snapshot of your financial reality. You’ll see exactly where your money is going, uncovering those little “financial leaks” and finding clear opportunities to improve. With that baseline, you’re ready to build a budget that actually works for you.

Your goal isn’t just to see where the money went, but to gain the clarity needed to tell your money where to go next.

Do I Need Complex Software for Cash Flow Management?

Definitely not, at least not when you’re starting out. While some fantastic software tools can automate a lot of this (especially for businesses), they aren’t essential. A simple spreadsheet is more than powerful enough for managing personal or family finances.

The key is finding a system you’ll actually stick with. It’s far better to have a simple method you use consistently than a fancy tool you never open. Start simple, build the habit, and you can always explore more advanced options as your confidence and needs grow.

Building financial clarity is all about putting these small, consistent habits into practice. This is exactly what we help our clients do at Wealth Collective—turn financial knowledge into real-world results that you can see and feel.

Ready to stop worrying and start building? At Wealth Collective, we translate complex financial topics into clear, actionable plans.

Book your free, no-obligation introductory call with an adviser today and discover how a personalised strategy can help you achieve your goals. Visit us at https://wealthcollective.co.