Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

When it comes to your financial security, one of the first questions we often hear is, "Can I claim my life insurance premiums on tax?" It’s a smart question, and the short answer is usually no. But—and this is a big but—there's a major exception that can make a huge difference to your finances: income protection insurance.

So, Is Life Insurance Tax Deductible? Here's The Straight Answer

Let's cut through the noise. For most personal policies, the Australian Taxation Office (ATO) considers the premiums a private expense, much like your car or home insurance. You're paying to protect your family's future, not to generate taxable income.

This is why your typical life insurance, Total and Permanent Disability (TPD), and trauma insurance premiums are not tax deductible when held personally. These policies are designed to pay a lump sum of capital, which itself isn't considered taxable income. The logic is simple: no income, no deduction.

The All-Important Exception: Income Protection

This is where the game changes completely. Income protection insurance is the one standout policy that is generally tax deductible.

Why? Because its entire purpose is to replace your income if you can't work. The payments you receive from an income protection claim are treated as assessable income, so the ATO allows you to claim the cost of the premiums you paid to secure that potential income stream.

This is a critical distinction, and structuring it correctly is key to a tax-effective financial plan.

A Quick Summary for Individuals

To make this crystal clear, here’s a simple table breaking down what you can and can’t typically claim as an individual taxpayer.

| Quick Guide to Insurance Premium Deductibility | ||

|---|---|---|

| Insurance Type | Tax Deductible for Individuals? | Key Condition |

| Life Insurance (Death Cover) | No | Payout is a capital lump sum, not income. |

| TPD Insurance | No | Payout is a capital lump sum for injury/illness. |

| Trauma Insurance | No | Payout is a capital lump sum for a specific medical event. |

| Income Protection | Yes | Protects your ability to earn an income, and benefits are assessable. |

Remember, this is a general guide. Your specific circumstances can introduce nuances, which is why getting the right advice is so important.

At Wealth Collective, our first step is always to ensure you understand these fundamentals. A well-built financial safety net is about more than just having cover; it’s about structuring the right cover in the most tax-efficient way possible as part of your overall wealth strategy.

Understanding this core difference is the first step. Next, we’ll explore how ownership—holding a policy personally, through your business, or in super—adds another layer to the tax puzzle. For a full rundown on these cover types, you can explore our guide on the different kinds of life insurance.

How Policy Ownership Changes Your Tax Position

When people ask, “is life insurance tax deductible?”, they often focus only on the type of policy. But that’s just half the story. The other, arguably more important, piece of the puzzle is who owns the policy.

The tax rules shift completely depending on whether you hold your cover personally, through your business, or inside your super fund.

Think of it this way: if you buy a car for personal use, you can’t claim fuel costs on your tax return. But if you’re a courier using that exact same car for deliveries, those costs suddenly become legitimate business expenses. The car hasn’t changed, but its purpose and ownership have, and that makes all the difference to the ATO.

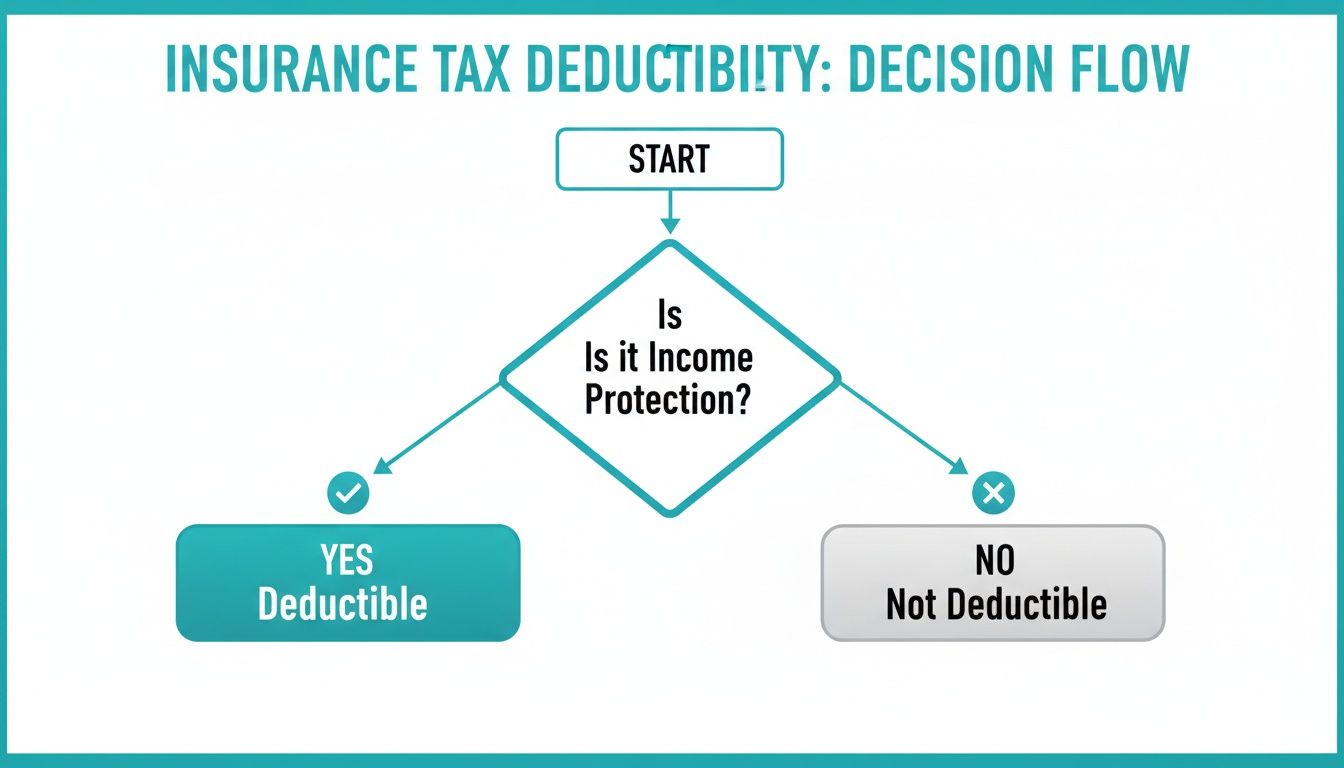

This simple flowchart shows how it typically works for policies you own personally.

As you can see, income protection is the main one you can claim when you own it personally. But this is just the first layer.

Personal vs. Business vs. Superannuation

Let’s dive deeper into the three main ways to structure your cover and what each means for your tax position. Understanding these scenarios is key to building an intelligent financial safety net.

-

Personally Owned Policies: This is the most straightforward setup. As we’ve covered, premiums for life, TPD, and trauma insurance held in your own name are not tax-deductible. The big exception is income protection, which you can claim because it’s designed to replace your personal income.

-

Business Owned Policies: This is where insurance becomes a powerful strategic tool for business owners. If a policy is set up to protect your business—like Key Person insurance to cover a revenue drop if a vital employee can’t work—the premiums can often be claimed as a business expense. The ATO’s main test is whether the policy protects business revenue (making it deductible) or a capital asset (making it non-deductible).

-

Insurance Inside Superannuation: Holding cover inside super is a popular strategy because premiums come from your super balance, not your bank account. However, you cannot claim a personal tax deduction for these premiums. The super fund itself can usually claim a deduction, passing on a benefit within the low-tax super environment. You can learn more in our guide to income protection inside superannuation.

Each of these ownership structures has pros and cons that go beyond tax. The right choice depends entirely on your personal finances, your business, and your long-term goals.

Figuring out the optimal structure is a core part of the Wealth Collective process. We help you make sure your insurance cover is not only solid but also fits intelligently within your broader financial strategy, turning a simple expense into a powerful part of your wealth plan.

Understanding The Income Protection Exception

When it comes to personal insurance, the ATO generally views premiums as a private expense, meaning no tax deduction. But there’s one major exception: income protection insurance.

Why does this specific cover get the green light from the tax man? It all boils down to its fundamental purpose.

Unlike Life or TPD insurance, which pay out a tax-free lump sum, income protection is designed for one thing: to replace your regular pay cheque if an illness or injury stops you from working. Because the monthly benefits you’d receive are considered assessable income (just like your salary), the ATO allows you to claim a deduction on the premiums you pay to secure that income.

This simple tax rule makes a huge difference. It directly lowers the real-world cost of your policy, making it a much more affordable and powerful way to protect your single greatest asset: your ability to earn an income.

How It Works In The Real World

Let’s look at a practical example. Say you’re a professional working hard to support your family. If a sudden illness took you out of work for six months, your income protection policy would kick in to pay the bills. And because you hold the policy personally (outside of super), the premiums are tax-deductible.

This means you get a slice of your premium costs back when you lodge your tax return. The exact amount depends on your marginal tax rate.

For instance, if your annual premium is $2,000 and you’re on a 32.5% tax rate, you could claim back $650. This drops your effective annual cost to just $1,350, a significant saving.

This tax efficiency is a cornerstone of smart financial protection. It’s not just about having a safety net; it’s about weaving that net intelligently so it costs you less while delivering the powerful protection your family deserves.

By turning a potential financial disaster into a manageable situation, a tax-deductible income protection policy acts as a vital lifeline. It ensures your mortgage, bills, and school fees keep getting paid, keeping your long-term goals on track.

Getting the structure right is crucial. To explore this in more detail, see our guide on income protection insurance and tax deductions. A quick, no-obligation chat with our team can also clarify how this powerful strategy can work for you, ensuring your financial plan is both robust and efficient.

Strategic Insurance Planning for Business Owners

For a business owner, the question “is life insurance tax deductible?” is about more than just a personal tax return. It’s a gateway to strategic planning. When your business owns the policy, the focus shifts from protecting your family to safeguarding the business itself—and that completely changes the tax rules.

This is where you get into the nitty-gritty of smart business protection, with things like Key Person insurance and policies set up to fund a Buy/Sell Agreement. These are powerful tools for ensuring your business can weather any storm, and if structured correctly, the premiums can often be claimed as a business expense.

The Revenue Versus Capital Test

When deciding if your insurance premiums are deductible, the ATO uses a straightforward benchmark: the ‘revenue versus capital’ test. Understanding this is key.

Essentially, the ATO wants to know: is this policy designed to protect the business’s income-earning ability (its revenue), or is it meant to protect an ownership stake (a capital asset)?

-

Protecting Revenue: If a policy’s job is to cover a potential loss of income—say, if your top salesperson is out of action and sales plummet—then the premiums are generally a deductible expense. The insurance payout would be treated as taxable income, effectively replacing the revenue you lost.

-

Protecting Capital: On the other hand, if a policy is there to fund a capital event, like giving one partner the cash to buy out another’s share of the business upon death, the premiums are not deductible. Here, the payout is considered capital, not income.

Understanding this difference is the secret to making your insurance work smarter for you. It can turn insurance from a grudge purchase into a tax-effective part of your risk management strategy.

A Real-World Example

Let’s look at Sarah and Tom, partners in a booming marketing agency. The business hinges on their expertise and client relationships.

They wisely decide to set up two different policies:

- Key Person Revenue Policy: This policy is set up to pay the business a monthly sum if either Sarah or Tom can’t work. The money would cover the immediate drop in client billings and help pay for a contractor. Because its purpose is to protect the business’s revenue, the premiums are a deductible business expense.

- Buy/Sell Agreement Policy: This one is different. It’s designed to pay out a lump sum so the surviving partner can buy the deceased partner’s ownership stake from their estate. Since this policy is funding the transfer of a capital asset (the shares in the business), the premiums are not tax-deductible.

This one scenario shows how two policies, on the same people, are treated completely differently by the ATO. It all comes down to purpose, which is why getting the structure right from day one is so important.

At Wealth Collective, our expertise lies in translating these complex rules into clear, actionable advice. We partner with business owners to build sophisticated strategies that ensure continuity and maximise tax efficiency. The journey starts with a simple, no-obligation call to see how we can help protect and grow your business.

Common Misconceptions That Can Cost You Thousands

When it comes to tax time, a few common misunderstandings around life insurance can be costly. The rules can feel like a maze, and a simple slip-up can lead to a missed deduction or, worse, a ‘please explain’ letter from the ATO.

Let’s walk through the most common traps we see so you can sidestep them and ensure your financial strategy is working as hard as you are.

Assuming All Business Insurance Is Deductible

It’s a logical assumption: if the business pays for an insurance policy, it must be a business expense, right? Unfortunately, the ATO applies the ‘revenue versus capital’ test.

Is the policy protecting day-to-day income, or the ownership structure?

- A Key Person policy to replace lost revenue if a crucial employee can no longer work? The premiums are generally deductible.

- A policy funding a Buy/Sell Agreement to allow one partner to buy out another’s shares? That’s protecting a capital asset, so the premiums are not deductible.

This distinction is everything. Getting the structure wrong from the outset can void the tax benefit you were counting on.

Trying To Claim Premiums Paid Through Super

This one catches a lot of people. The thinking goes, “My super fund is paying for my insurance, so I should be able to claim it on my personal tax return.” The answer here is a firm no.

You can’t personally claim a deduction for insurance premiums your super fund pays. The tax relief has already been handled inside the superannuation fund. Your fund is the one that claims the deduction, which helps lower the tax it pays. It’s a perk, just not one you can claim twice.

These nuances are why professional advice is so critical. A small mistake in how a policy is owned or structured can unravel your tax planning. The Wealth Collective process is designed to spot these potential tripwires, ensuring your financial plan is solid and compliant from the start.

Incorrectly Claiming Bundled Policies

Many insurers let you bundle different types of cover together—for example, combining your income protection with life and TPD insurance. The mistake here is thinking you can claim the entire premium.

You can only claim the portion of the premium that pays for the tax-deductible income protection component. Your insurer must provide a policy schedule that clearly breaks down how much of your premium is allocated to each type of cover. Claiming the whole amount is a red flag for the ATO.

Getting this right from the start is simple with the right guidance. At Wealth Collective, we help our clients structure their cover correctly to avoid these headaches. If you’re unsure about your own setup, book a complimentary call with our team. We’ll help you make sure your protection strategy is working for you, not against you.

So, What Does This All Mean For You?

You’ve made it through the nitty-gritty of tax rules and insurance. The big question now is, what do you do with this information? It’s time to move from theory to a practical plan that safeguards your financial world.

Let’s boil it down. The ability to claim a tax deduction comes down to the type of cover and who owns the policy. Most personal life insurance policies won’t get you a deduction, but income protection is a fantastic exception. For business owners, it’s all about passing that crucial ‘revenue vs. capital’ test.

From Theory to Action Plan

It’s easy to feel overwhelmed by financial decisions, but getting started is simpler than you think. The first step is a conversation to see how these rules apply to your specific circumstances. Our job at Wealth Collective is to translate financial complexity into clear, straightforward advice you can use.

A financial safety net isn’t just about buying a policy; it’s about designing a strategy from the ground up. Getting the right advice ensures your plan is not only robust but also structured to be as tax-efficient as possible, helping you avoid costly mistakes.

Your financial future is too important to be left to guesswork. A short chat today can make a world of difference for your family’s security tomorrow and ensure you aren’t paying a dollar more in tax than you have to.

Ready to build a plan that gives you confidence and control? Book your complimentary, no-obligation introductory call with Wealth Collective. Let’s talk about how we can help you build, protect, and grow your wealth with a strategy that’s right for you.

Frequently Asked Questions

It’s only natural for questions to pop up when you’re navigating the crossover between insurance and tax. Let’s walk through some of the most common queries we hear from clients, breaking down the rules in a way that makes sense for you.

Can I Claim a Tax Deduction for Life Insurance Premiums Paid Through My Super Fund?

This is a great question, and the short answer is no. You can’t personally claim a tax deduction for insurance premiums that your superannuation fund pays on your behalf.

The reason is that you’re likely already getting a tax break. The super fund itself usually claims a deduction for the premiums, which helps lower the tax within the fund. That benefit is passed on to you indirectly through the low-tax super environment, but it doesn’t flow through to your personal tax return.

What Happens If My Insurance Policy Is Bundled?

Bundled policies are common, but they can make tax time tricky. If your policy combines something you can’t claim—like life cover—with something you can—like income protection—you can only claim the portion of the premium that pays for the deductible cover.

Your insurer must give you a policy statement that clearly itemises how much of your premium goes to each type of insurance. You’ll need to use this breakdown to work out the exact amount you can claim. Don’t make the mistake of claiming the entire premium.

Getting the structure of your insurance right from the start is fundamental to a sound financial plan. This is a core part of the Wealth Collective process, ensuring you’re protected effectively while maximising any available tax advantages.

Are Payouts From a Tax-Deductible Policy Taxable?

Yes, they are. This is a classic “give and take” from the tax office. Because you get to claim a tax deduction on your income protection premiums, any benefit you receive from that policy is considered assessable income.

Think of it like a replacement for your salary. Just as you pay tax on your regular pay, you’ll need to declare these insurance payments on your tax return. The rule of thumb is simple: you can’t get a tax benefit on both the cost (the premiums) and the payout (the benefits).

Understanding how these rules apply to you is the first step towards building a smarter, more efficient financial strategy. At Wealth Collective, our expert advisers translate these complexities into clear, actionable guidance.

Book your complimentary introductory call today to see how we can help you build, protect, and grow your wealth with confidence.