Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

When you hear about putting money into your super, you probably think of the standard contributions your employer makes. But there’s another powerful way to build your retirement savings: non-concessional contributions (NCCs).

So, what are they?

Think of them as personal top-ups you make from your own bank account. This is money you've already paid income tax on—your after-tax income. Because the tax has already been taken care of, these contributions aren't taxed again when they land in your super fund.

The Two Roads to Your Super Fund

It's helpful to picture two main paths for money to get into your super. The first path is for before-tax money (concessional contributions), like your employer's compulsory payments. The second path is for after-tax money, which is where non-concessional contributions come in.

Let’s break down the key differences.

Concessional vs Non Concessional Contributions At a Glance

| Feature | Concessional Contributions (Before-Tax) | Non-Concessional Contributions (After-Tax) |

|---|---|---|

| Source of Funds | Money from your pre-tax salary (e.g., employer contributions, salary sacrifice). | Money from your personal savings or bank account, which has already been taxed. |

| Tax on Entry | Taxed at a 'concessional' rate of 15% when it enters your super fund. | Not taxed on entry to your super fund because you've already paid income tax on it. |

| Primary Purpose | The standard, compulsory way to build super over your working life. | A voluntary strategy to accelerate your savings and move wealth into a tax-effective environment. |

| Annual Cap (2025-26) | $30,000 | $120,000 |

Understanding this distinction is the first step in taking real control over your retirement outcomes. One is automatic; the other is a deliberate choice you make to fast-track your wealth.

Why Make After-Tax Contributions?

Unlike the mandatory 12% your employer pays, NCCs are entirely voluntary. They represent you actively deciding to invest in your future self, giving you a way to boost your super balance outside of your regular pay cycle.

This is an incredibly useful strategy for moving a lump sum—perhaps from an inheritance, the sale of an investment property, or just accumulated savings—into the low-tax environment of superannuation. It’s particularly effective if you are:

- A pre-retiree wanting to make a final, significant boost to your nest egg before you stop working.

- A high-income earner who consistently maxes out your before-tax (concessional) contribution limits.

- Anyone who receives a windfall and wants to put it to work for their long-term future.

Essentially, non-concessional contributions are your secret weapon for building wealth. They complement the slow-and-steady growth from employer payments with targeted, high-impact deposits that you control.

Of course, there are rules. The Australian Taxation Office (ATO) sets a firm cap on how much you can contribute this way. For the 2026 financial year, the annual NCC cap is $120,000. This limit has been gradually increasing, up from $100,000 back in the 2020-21 financial year.

Navigating these rules and deciding if NCCs are right for you is where our process begins. At Wealth Collective, we start by understanding your goals and financial situation to turn complex contribution strategies into a clear, actionable plan. If you're just starting, it's worth getting your head around the fundamentals in our guide on what is superannuation in Australia.

Navigating the NCC Cap and Bring-Forward Rule

Knowing what non-concessional contributions are is the first step. The real magic happens when you learn how to use them strategically to build serious retirement wealth. To get there, you need a solid grasp of two core rules from the ATO: the annual cap and the bring-forward rule.

Let's start with the basics. The annual non-concessional contributions cap is the standard limit you can put into your super from your after-tax money each financial year. For the 2025-26 financial year, that figure is $120,000. But, it's not a one-size-fits-all rule.

Your ability to make these contributions hinges on your Total Super Balance (TSB), which is just the combined value of all your super accounts. If your TSB was $1.9 million or more on 30 June of the previous financial year, your non-concessional cap for the current year is effectively zero.

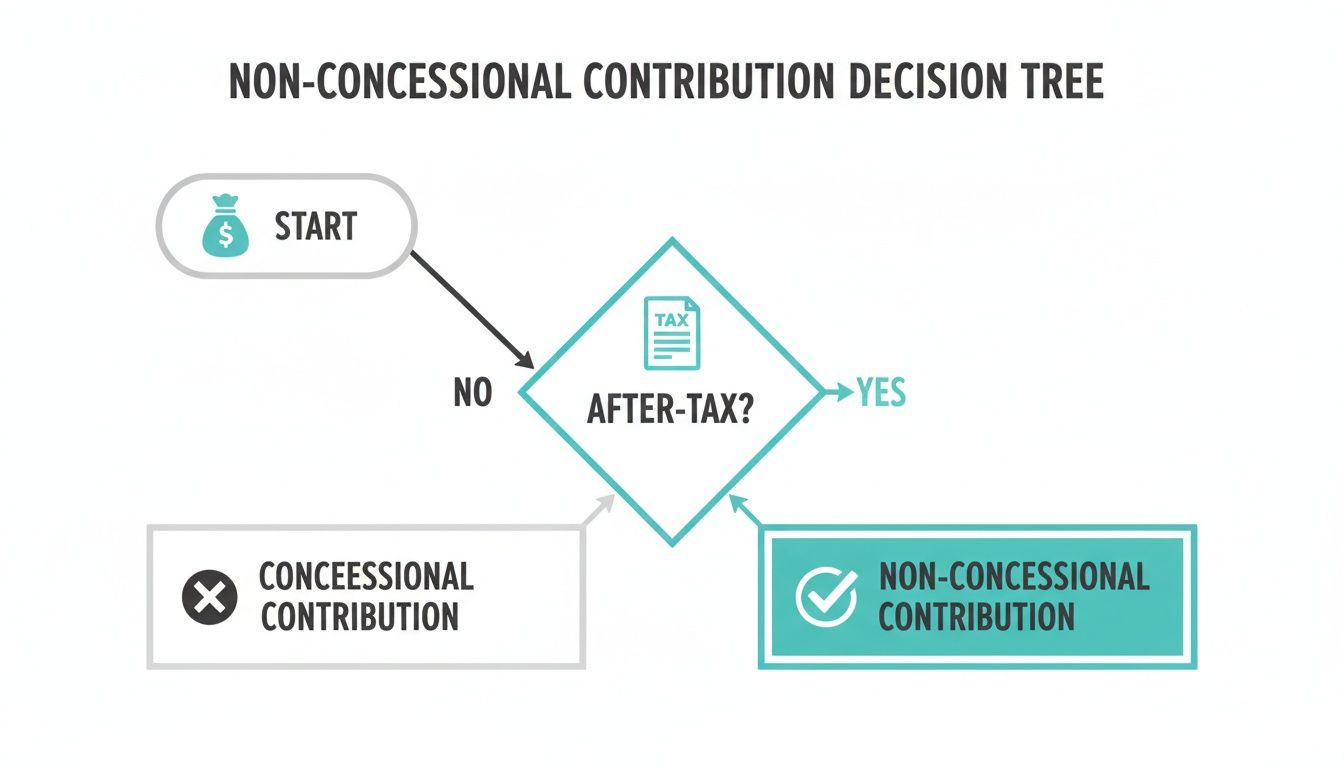

This simple decision tree helps visualise the process.

As you can see, if the money you're contributing has already been taxed (i.e., it's from your bank account), it's automatically an NCC and subject to these specific caps.

The Power of the Bring-Forward Rule

While the annual cap offers a steady way to grow your super, the bring-forward rule is the accelerator pedal. It lets eligible people 'bring forward' future years' NCC caps to make a much larger contribution in one go.

Imagine bundling three years' worth of your contribution allowance into a single, powerful deposit. This is the essence of the bring-forward rule—a way to make significant progress toward your retirement goals in a much shorter timeframe.

This rule can be a complete game-changer. For example, if your total super balance was under $1.76 million on 30 June 2025, you could potentially contribute up to $360,000 in one hit, covering a three-year period. This is a massive opportunity, especially for people who've received an inheritance, sold a business, or simply want to supercharge their savings. You can find the specific TSB thresholds and how they work on the official ATO website.

This is a cornerstone technique in our ‘Retirement Roadmap’ service. By planning the timing perfectly, we help clients make substantial injections into their super, taking a huge leap towards their financial goals. Of course, remember this strategy is all about after-tax money, which works differently from the rules for before-tax contributions. You might also find our guide on how to carry forward concessional contributions useful.

Getting these rules right is absolutely crucial. At Wealth Collective, we can walk you through your eligibility and help you decide if this high-impact strategy is the right move for your financial journey. A great first step is Booking an initial call with us to discuss your personal situation.

Who Benefits Most from Making Non-Concessional Contributions

While anyone can make them, non-concessional contributions (NCCs) are not the right move for everyone. They truly come into their own in a few specific scenarios, and it's our job to help you figure out if you're one of them.

It usually boils down to a handful of key groups. Each has a powerful reason for wanting to shift a significant amount of their after-tax cash into the much friendlier, low-tax environment of super.

Pre-Retirees and Downsizers

For those in the final stretch of their careers, NCCs can provide a powerful last-minute boost to their retirement savings. We often work with Perth-based executives and professionals in their late 50s and 60s who are looking to make one last, big injection into their super. It's their final window to make a substantial contribution that can then compound for years to come.

A classic example we see is someone selling the large family home. Using some of those proceeds to make a non-concessional contribution is an incredibly effective way to park that capital and secure it for your future. Our Retirement Roadmap service is designed to guide clients through this exact process.

High-Income Earners

If you're a high-income earner, you've probably noticed you hit your concessional (before-tax) contribution cap of $30,000 pretty quickly. Once that door closes for the year, your only option for getting more money into super is through non-concessional contributions.

This strategy gives you a path to keep building your nest egg beyond the standard limits, moving wealth from your personal, high-tax name into your super fund.

At Wealth Collective, our process starts with understanding your unique story. We turn complex rules into a personalised action plan, determining if this powerful strategy is the right move for you.

Individuals with a Windfall

Life can sometimes throw you a financial curveball—in a good way. What you do with that sudden influx of cash is crucial. This group often includes:

- Small Business Owners: Selling a business or a major asset often results in a large lump sum. An NCC can be a smart way to invest those proceeds for the long haul in a tax-effective structure.

- Young Professionals with an Inheritance: Receiving an inheritance gives you a rare opportunity to get a massive head start on retirement. A well-timed non-concessional contribution can put a young professional decades ahead, letting that money work for them through the power of compounding.

No matter the situation, the goal is always the same: to move a lump sum of after-tax money into a more favourable investment environment for the long term. Since everyone’s circumstances are different, getting the rules and timing right is absolutely critical. Booking an initial call with us is the first step towards building a plan that truly fits your life and your goals.

Smart Strategies for Getting the Most Out of Your Contributions

Knowing the rules is one thing, but making them work for you is where you really start building serious wealth. Making a non-concessional contribution (NCC) is a fantastic move. But with savvy planning, you can turn a good decision into a brilliant one.

It’s about moving beyond simply what to do and focusing on how and when.

For instance, a simple but powerful tactic is all about timing. Many people scramble to get their contributions in just before 30 June. Instead, making your contribution early in the financial year can give your money an extra 12 months to compound and grow, potentially adding thousands to your final balance over time.

But timing is just the beginning. The most effective retirement plans weave NCCs together with other powerful strategies to create a result that’s much greater than the sum of its parts.

Weaving NCCs Into Your Broader Super Strategy

Looking at your contributions in a vacuum is a classic missed opportunity. The real magic happens when you see them as one part of a much bigger financial picture. Have you ever thought, for example, about how your contributions could also benefit your partner?

- Spouse Contributions: If your spouse earns a low income, you can make non-concessional contributions into their super account. This not only gives their retirement nest egg a healthy boost but could also make you eligible for a handy tax offset.

- Downsizer Contributions: For anyone over 55, selling your family home can unlock a huge opportunity. You may be able to contribute up to $300,000 per person into super, completely separate from the usual NCC caps. It’s a powerful, one-off chance to supercharge your savings.

- Salary Sacrifice Synergy: Why not use both types of contributions? Many people focus on maxing out their before-tax concessional contributions through salary sacrifice, then use their after-tax savings to make NCCs on top of that. Our guide on what is salary sacrifice super dives deeper into how these two approaches can work hand-in-glove.

For pre-retirees, this is where our ‘Guided Growth’ service really comes into its own. The goal is to strategically use NCCs to get your super optimised before your Total Super Balance (TSB) hits the $1.9 million threshold, at which point your ability to make NCCs drops to zero.

Small business owners should also be paying close attention. With total Australian super assets forecast to hit $4.5 trillion by December 2025 (an 8.1% jump), using NCCs is one of the most direct ways to convert business success into personal wealth. You can find more detail on how the caps work on the ATO's official page.

A core part of our process is keeping a close eye on your Total Super Balance and available contribution caps. We monitor this through myGov to make sure your decisions are always fully informed, helping you avoid costly mistakes and ensuring every dollar is working as hard as it can for you.

By looking at your entire financial world, we can help you build a strategy that doesn’t just add to your super—it multiplies its potential. Booking an initial call with us is the first step toward turning these powerful strategies into real-world results for your future.

Common Pitfalls and How to Avoid Them

While non-concessional contributions are a powerful way to boost your retirement savings, it’s surprisingly easy to trip over the rules. An accidental misstep can be both stressful and expensive, but the good news is that these pitfalls are entirely avoidable with the right guidance.

The most common issue we see is people accidentally exceeding their annual cap. This isn’t a disaster, but it does trigger a formal process with the Australian Taxation Office (ATO). Let’s walk through what happens.

What Happens If You Go Over the Cap

If you contribute too much, you’ll eventually receive a formal determination letter from the ATO stating you’ve made an excess non-concessional contribution. This letter will give you a couple of choices on how to fix it.

The key takeaway is that you aren't penalised straight away. You get to decide how to proceed.

It's absolutely crucial to respond to the ATO's notice. Ignoring it is the worst thing you can do, as it leads to a default, and usually much less favourable, outcome. This is where proactive management really pays off.

Your Two Main Options

Once that letter arrives, you have a decision to make. Think carefully about which path makes the most sense for your financial situation.

Release the Excess Amount: You can choose to have the excess funds, plus any associated investment earnings, released from your super. Those earnings are then added to your taxable income for the year, but you get a 15% tax offset to help soften the blow. This is by far the most common and cost-effective solution.

Leave the Excess in Super: Your other option is to leave the money where it is. If you choose this route (or simply fail to respond to the ATO), the entire excess contribution will be taxed at the highest marginal tax rate, which is currently a painful 47%. This tax is typically paid directly from your super fund balance.

This is precisely the kind of situation where having an expert in your corner makes all the difference. Our ‘Protection Plus’ service at Wealth Collective is designed to act as a safeguard against these preventable errors. We monitor your contribution caps and Total Super Balance, ensuring your strategy keeps you well within the rules.

Working with an adviser means you can avoid the stress and expense of a mistake altogether. If you're feeling unsure about your contribution limits or want to build a safe and effective plan, book a quick, complimentary call with our team today.

Ready to Put Your Super Strategy Into Action?

You now have a much clearer picture of how non-concessional contributions can seriously boost your retirement savings. But knowing the rules is one thing; making them work for you is another entirely. That's where we can help.

Everyone’s financial journey is different, and a one-size-fits-all approach just doesn't cut it. The real power of the super rules lies in how you apply them to your specific circumstances—our speciality at Wealth Collective.

From Knowledge to Real-World Results

Deciding to take control and actively build your super is a big move—and you’re not alone. Personal super contributions, which include NCCs, jumped by an incredible 19.2% to $64.5 billion in the year to December 2023. You can see the full breakdown for yourself in the official ATO contribution data.

This isn't just a statistic; it’s a clear sign that people are moving from passive saving to actively building the future they want. Our entire process is built to guide you through that shift, taking the complexity and guesswork out of the equation.

At Wealth Collective, our job is to cut through the jargon and turn complex rules into a clear, effective plan. We want you to feel confident and completely in the driver's seat of your financial life.

It all begins with a straightforward chat to understand where you are today and where you want to be tomorrow. We’ll look at your eligibility, map out the best timing for contributions, and make sure your super strategy fits seamlessly with your bigger life goals—whether through our Guided Growth or Retirement Roadmap service.

This is about more than just ticking boxes; it's about building a future you can truly look forward to.

Your first step toward a successful financial life is just a quick, friendly chat away. We offer a complimentary, no-obligation 10-minute call to see how we can help you build, protect, and grow your wealth.

Got Questions? We've Got Answers

When it comes to non-concessional contributions, a few questions pop up time and time again. Let's tackle some of the most common ones we hear from our clients to clear up any lingering confusion.

Can I Still Contribute to Super If I’m Retired?

Absolutely. You can generally keep making non-concessional contributions right up until you turn 75.

The main thing to watch out for is the 'work test' if you're between 67 and 74. To be eligible, you'll need to have worked for at least 40 hours within a 30-day period during that financial year. Getting these age-based rules right is a cornerstone of our Retirement Roadmap service, helping you maximise contributions in your final working years.

What Actually Counts Towards My Non-Concessional Cap?

This is where a lot of people get tripped up. It’s not just the money you put in from your bank account. Your non-concessional contributions also include any contributions your spouse makes into your super and, in some cases, money transferred from overseas pension funds.

It’s vital to keep an eye on all these potential sources so you don't accidentally tip over your limit. Don't worry, your regular employer contributions (the compulsory ones) don't count towards this particular cap.

Your ability to make these contributions is tied directly to your Total Super Balance (TSB). Knowing this number is non-negotiable for smart super planning, and it's a key part of our Guided Growth approach.

How Do I Check My Personal Contribution Caps?

Thankfully, this part is straightforward. The best way to see where you stand with your contribution caps is by logging into your myGov account and making sure it’s linked to the ATO.

The portal will show you exactly how much room you have left for both concessional and non-concessional contributions for the financial year. It also tells you if you’re eligible to use the bring-forward rule. Keeping tabs on this is a simple but crucial habit—and it’s something we help our clients manage effortlessly as part of our service.

At Wealth Collective, our job is to translate these complex rules into a clear, powerful strategy that works for you.

Ready to see what that looks like? Book your complimentary 10-minute introductory call today and let’s get started.