Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

So, what exactly is mortgage refinancing?

At its core, refinancing is simply replacing your current home loan with a new one. Think of it like swapping your old mobile plan for a better deal. You might get a lower monthly bill or better features that suit your life now—refinancing your mortgage works on the same principle, just on a much larger scale. It's a strategic move to ensure your largest debt is working for you, not against you.

This single decision can unlock serious financial potential, which is a key part of the smart wealth-building strategies we implement at Wealth Collective. Our process is all about making your biggest asset—your home—work much harder for you.

Understanding the Basics of a Mortgage Refinance

When you refinance, you take out a new loan to pay off your existing one. The goal is nearly always to land a better deal that aligns with your current financial situation, whether that means saving money on interest, tapping into your home’s equity, or just getting a loan with more flexible features.

Internal vs. External Refinancing

When you decide to refinance, you generally have two paths:

- Internal Refinance: You stick with your current lender but negotiate for a better interest rate or different loan features. It’s often a simpler process with fewer fees, but you’re limited to the products your existing bank is willing to offer.

- External Refinance: You switch your home loan to a new lender entirely. While this involves a full home loan application, it opens up the whole market of options. This is where the most competitive rates and biggest long-term savings are usually found.

Here in Australia, refinancing has become a go-to strategy for homeowners navigating our dynamic property and interest rate environment. Recent figures show that the average owner-occupier refinances a loan of $613,000, while for investors, that number jumps to an average of $687,000. These big numbers reflect just how many Aussies are taking action to get a better deal on their loans. You can explore more Australian home loan statistics to see these trends for yourself.

To help you see the bigger picture, here’s a quick comparison of what it looks like to refinance versus staying put.

At a Glance: Refinancing vs. Staying Put

| Aspect | Staying with Your Current Loan | Refinancing Your Loan |

|---|---|---|

| Interest Rate | Potentially paying a higher, non-competitive rate. | Opportunity to secure a lower rate, reducing repayments. |

| Loan Features | Stuck with existing features (e.g., no offset account). | Chance to add features like an offset or redraw facility. |

| Cash Flow | Your monthly repayments remain the same. | Lower repayments can free up monthly cash flow. |

| Equity Access | Limited or no ability to access built-up equity. | Can unlock equity to fund renovations, investments, or goals. |

| Effort Required | None—the easiest option in the short term. | Requires an application process and some paperwork. |

Ultimately, while staying with your current loan is the path of least resistance, refinancing is a proactive step that can put you in a much stronger financial position.

Refinancing isn't just about chasing the lowest interest rate. It's about strategically structuring your debt to fuel your long-term financial plan. A well-timed refinance can free up cash flow, cut down your total interest bill, and create new opportunities for investment and growth.

At Wealth Collective, our first step is always to understand your complete financial picture. We help you weigh up both internal and external options to make sure any decision you make directly supports your goals. The best way to get clarity on whether refinancing is the right move for you is by Booking a quick, complimentary call with our team.

Why Australian Homeowners Choose to Refinance

If you ask most people why they’d refinance, they’ll probably say to get a better interest rate. And while that’s a huge motivator, the real reasons go much deeper. For savvy homeowners, it’s a strategic financial move to hit specific goals and build long-term wealth.

Getting a lower interest rate is certainly the most common starting point. A better rate can slash your monthly repayments, which immediately frees up cash. That could mean more money for savings, investments, or just a bit of breathing room in the family budget. Even a small rate cut can add up to tens of thousands of dollars in savings over the life of your loan.

Putting Your Home Equity to Work

Once homeowners understand what a mortgage refinance is, they often realise it can do more than just lower their rate. It's a powerful way to consolidate other, more expensive debts. Many Australians juggle high-interest debts from credit cards or car loans. Rolling these into a new, lower-rate mortgage simplifies your finances into one single, manageable repayment. Because mortgage rates are typically much lower than personal loan or credit card rates, this one move can dramatically speed up your journey to becoming debt-free.

Beyond tidying up finances, refinancing is the main way you can access your home’s equity. Think of equity as the part of your property you truly own—its current market value minus what you still owe the bank. As you pay down your loan and property prices rise, that equity becomes a significant financial resource.

Accessing equity isn't just about borrowing more money. It’s about strategically reinvesting your capital to build your wealth. We see it as a cornerstone of proactive financial management.

Funding Your Next Big Move

A cash-out refinance lets you tap into this equity to pay for major life goals. As part of the Wealth Collective process, we help clients use this strategy for:

- Major Home Renovations: A new kitchen or backyard oasis not only improves your lifestyle but can also add significant value to your property.

- Buying an Investment Property: Using the equity in your home as a deposit for a rental is a classic Australian strategy for building a property portfolio.

- Financing Big Life Events: From university fees for the kids to starting a new business, your equity can provide the funds.

At Wealth Collective, we see refinancing as a key tool for creating wealth, not just managing debt. We work with clients to structure their refinance to support their bigger financial picture, whether that's through smart debt consolidation or advanced strategies like debt recycling. To see how this works, check out our guide on how to debt recycle. Ultimately, refinancing gives you the flexibility to adapt as your life and goals change.

Is Now a Good Time to Refinance in Australia?

Homeowners often ask if now is the right moment to refinance, but the truth is, the answer is always personal. It’s less about picking a perfect day in the market and more about what’s happening in your own financial life.

The most powerful signals to review your mortgage come from your own circumstances. If your fixed-rate period is about to end, your income has gone up, or you simply haven't looked at your home loan in a couple of years, there’s a good chance you’re leaving money on the table. Think of these moments as financial checkpoints. A proactive review can often uncover serious savings, even when the broader market feels uncertain.

A Look at Australia’s Lending Climate

The Australian lending market is constantly on the move, with the Reserve Bank of Australia (RBA) and lender competition setting the pace. Heading into 2026, we’ve seen some significant shifts.

The RBA pushed the cash rate to 3.85% and then to 4.10%, which directly affects the variable-rate loans most Australians have. With fixed-rate loans now making up less than 2% of new lending, most homeowners are feeling the pinch of rising rates. You can get a deeper dive from these expert predictions for RBA rates to see where things might be heading.

So, what does this all mean for you? Put simply, sitting on an uncompetitive home loan is more costly than ever. As rates climb, the gap between a good deal and a bad one gets wider, eating into your budget every single month.

In a shifting market, opportunity doesn't disappear—it just moves. Lenders are still fiercely competing for high-quality borrowers, often offering attractive cashback deals and discounted rates to win your business.

This is where having a clear strategy makes all the difference. It’s not just about finding the lowest rate, but finding the right fit for your goals. At Wealth Collective, our process involves analysing the current market to see which lenders are actively looking for customers like you, pinpointing the offers that align with your long-term wealth-building plans.

When Is It Your Time to Act?

The best time to refinance is when it makes financial sense for you. Market conditions are just one part of the equation. The real question is whether your current loan is still working for you.

Have you hit one of these common life milestones?

- Your fixed-rate period is coming to an end. This is a critical moment. Don’t just roll over onto your bank's standard variable rate—it’s almost never their best offer.

- You've had a change in income. A pay rise or a new job could make you a much more attractive customer to other lenders, giving you more negotiating power.

- Your financial goals have evolved. Maybe you’re ready to renovate, invest, or consolidate personal debts to improve your monthly cash flow.

If any of these sound familiar, it’s the perfect time to be proactive. An initial chat with a Wealth Collective advisor is a simple, no-obligation way to get clear on where you stand and uncover opportunities you might be missing.

Understanding the True Costs and Savings of Refinancing

It’s easy to get excited about a lower interest rate, but switching your home loan isn't free. A successful refinance is one where the long-term gains comfortably cover the initial expenses. Getting a firm handle on these numbers is the first step towards making a smart financial choice. Let's break down what you can expect to pay.

Common Refinancing Costs to Expect

Most expenses are one-off costs at the beginning of the process. While they vary between lenders, you’ll typically need to account for a few standard fees.

- Discharge Fee: This is what your current lender charges to finalise your old mortgage, usually between $250 and $400.

- Application Fee: Your new lender might charge a fee to process your application, ranging from $0 up to $600, though many lenders waive this to win your business.

- Government Charges: These are state-based fees for deregistering the old mortgage and registering the new one, typically costing a few hundred dollars.

You also need to be mindful of Lenders Mortgage Insurance (LMI). If your home equity is below 20% of your property’s value, you might have to pay LMI again. This can be a major cost, which is why refinancing is often best timed for when your equity has passed that crucial 20% mark. For a deeper look at how property can support your financial goals, explore the tax benefits of owning a rental property in our related guide.

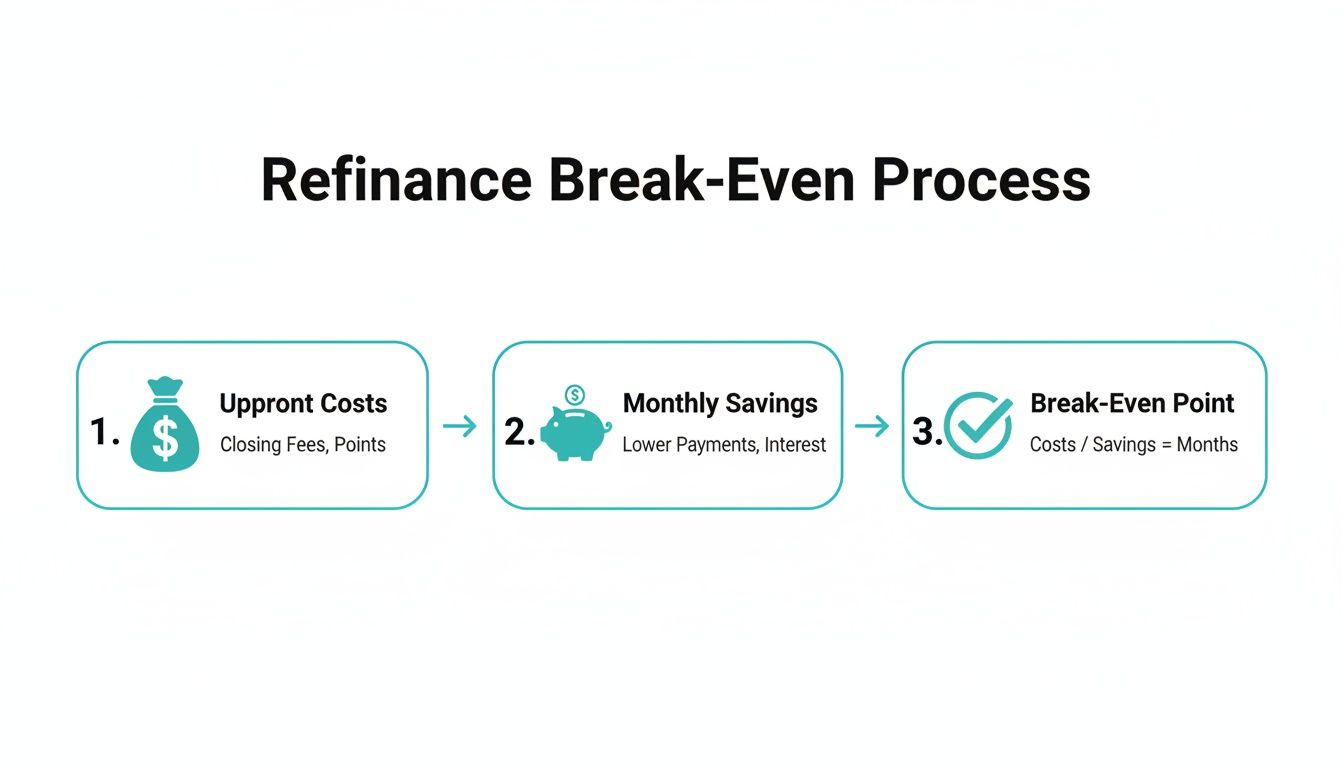

Calculating Your Break-Even Point

The key metric for any refinance is your break-even point: the moment when the money you've saved has completely paid off all upfront costs.

Your break-even point is the tipping point where the refinance stops costing you money and starts putting it back in your pocket. Calculating this before you commit is non-negotiable.

To figure this out, you add up all potential costs and divide that total by your estimated monthly savings. Here’s a simple example.

Example Refinance Calculation: Break-Even Point

| Calculation Step | Example Amount (AUD) | Description |

|---|---|---|

| Total Upfront Costs | $1,500 | This includes the discharge fee, application fee, and government charges all added together. |

| Monthly Savings | $150 | The difference between your old monthly repayment and your new, lower one. |

| Break-Even Calculation | 10 Months | Total Costs ($1,500) ÷ Monthly Savings ($150) = 10 months to recoup the initial outlay. |

In this scenario, it would take just 10 months to recover the costs. From month 11 onwards, every dollar you save is pure gain. This is exactly the kind of analysis our advisors at Wealth Collective perform. We dive into the details to ensure a refinance is right for you, giving you complete confidence before you move forward.

Your Step-by-Step Guide to the Refinancing Process

So, you think refinancing might be a good move. But what does the process actually look like? It can seem intimidating, but it’s really just a series of logical steps. At Wealth Collective, we walk clients through this roadmap every day, handling the heavy lifting and making sure the process is smooth and aligned with your goals.

Stage 1: Strategy and Comparison

Before we even look at an interest rate, our process starts with you. The most crucial part of refinancing is knowing why you're doing it. Is the goal to slash repayments? Pay off your loan faster? Or tap into your home's equity for an investment? Getting this foundation right is everything.

Once your goals are clear, we get to work:

- A deep dive into your finances: We review your income, expenses, assets, and debts to understand your borrowing power.

- Working out your available equity: We organise an estimate of your property's value to calculate your equity.

- Finding the right fit: Armed with this information, we sift through dozens of lenders and hundreds of loan products. We don't just look for the lowest rate; we find the loan that genuinely matches your financial situation and future ambitions.

Stage 2: Application and Approval

After we’ve pinpointed the ideal loan, it’s time to apply. This is where having an advisor in your corner makes a world of difference. We make sure all documents—payslips, bank statements, and IDs—are organised and submitted correctly the first time to avoid frustrating delays.

Next, your potential new lender will arrange a formal property valuation. With the valuation in and your application assessed, you’ll receive formal approval. This is the green light! You'll then sign the official loan documents, making your new, better mortgage a reality.

As you can see, you just weigh the upfront costs against your monthly savings. Once you hit that break-even point, every dollar you save is pure financial gain.

Stage 3: Settlement and What Comes Next

The final piece of the puzzle is settlement day. On this day, your new lender officially pays out your old home loan, and your new mortgage takes its place. The whole journey, from that first application to settlement, typically takes between four to six weeks.

With a clear roadmap and expert guidance, refinancing transforms from a daunting task into a powerful strategic move for your financial future.

Remember, this isn't just shuffling paperwork. It's a strategic upgrade to your financial position. For many of our clients, refinancing is the key that unlocks the funds needed for their next wealth-building move, like securing an investment property. You can find out more in our guide on how to buy an investment property.

Feeling ready to see what’s possible? An initial chat with our team is the best first step.

Let’s Put Your Refinancing Plan Into Action

Understanding what a mortgage refinance is marks a great starting point. But true progress comes from turning that knowledge into a smart, practical plan that’s built around you. That's where the Wealth Collective process begins. We help you cut through the jargon and complexity to make confident financial decisions.

What's Your Next Step?

It’s easy to read an article like this, feel motivated, and then let life get in the way. But your financial future is shaped by the small, proactive decisions you make today. A smarter mortgage strategy is one of the most effective tools you have to get ahead.

The biggest risk in managing your finances is often inaction. A simple mortgage review today could uncover savings and opportunities that you’re currently missing out on.

Let's find out what's possible for you. It all starts with a complimentary, no-obligation 10-minute chat with our team. In that short call, we can quickly assess if refinancing is a viable option for you and outline the next steps in our process. It might just be the best ten minutes you spend on your finances all year.

Common Questions About Mortgage Refinancing

Even with a good grasp of the basics, it’s normal to have a few more questions. When it comes to your home loan—likely your biggest financial commitment—you want absolute clarity. Let's run through some common queries we get from clients.

A big one is about credit history. People often ask, "Can I still refinance if my credit score isn't perfect?" The short answer is yes, it’s often possible. While a stellar credit score opens more doors, a less-than-perfect one doesn’t automatically close them. Some specialist lenders are more flexible, though you might face a slightly higher interest rate. It’s all about finding a lender whose criteria match your situation.

Another point of confusion is the difference between refinancing and a home equity loan. Think of it this way: refinancing is like trading in your old car for a completely new one with a new loan. A home equity loan is like keeping your car and its original loan, but taking out a second loan to tap into its value.

How Long Does It Take to Refinance?

So, how long does this all take? In our experience here in Australia, the refinancing process typically takes between four to six weeks from application to final settlement.

This timeline can vary depending on the complexity of your finances and how quickly both lenders process the paperwork. The best way to keep things moving is to have all your documents organised from day one—something our team at Wealth Collective helps you with as part of our service.

The most important thing to remember is that you don't have to figure all this out on your own. A quick chat with an expert can give you more clarity in 10 minutes than you'd get from hours of searching online.

At the end of the day, every person's refinancing journey is different. Understanding how all these pieces fit together for you is what turns a good decision into a great one that builds your wealth for the long haul.

Ready to get clear, personalised answers? The team at Wealth Collective is here to help you weigh your options and map out a strategy that works for you. Book your complimentary 10-minute chat today and take the first real step towards a smarter financial future.