Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Imagine what life would be like without your single biggest debt. For most Australians, achieving financial freedom starts with cracking one big question: how do I pay off my mortgage early?

The most straightforward answer is to consistently pay more than your minimum repayment. Every extra cent you put in goes straight to your principal balance, chipping away at the loan itself and slashing the total interest you’ll pay over the long run.

The Australian Dream of Mortgage Freedom

In Australia’s economic climate, owning your home outright is a smart, strategic goal. It’s about moving past wishful thinking and taking deliberate steps that deliver real financial—and psychological—wins.

This guide will show you exactly how to do it. We’ll unpack the most effective methods, from simple tweaks to your repayment schedule to more sophisticated financial moves. The payoff for getting this right is genuinely life-changing.

What Owning Your Home Outright Really Means

Paying off your home loan isn’t just about deleting a monthly expense. It opens up a new world of financial security and personal peace of mind.

Think about what you truly gain:

- Massive Interest Savings: Every extra dollar you pay off your principal is a dollar you’re not paying interest on for the next 10, 20, or even 30 years. This can add up to tens or even hundreds of thousands of dollars saved.

- Serious Financial Breathing Room: Once your mortgage is gone, that huge chunk of cash flow is yours again. You can redirect it to build lasting wealth through investments, top up your super, or chase other big goals.

- A Powerful Safety Net: Owning your home outright is the ultimate security blanket. If your income ever takes an unexpected hit, you have a roof over your head, which dramatically lowers your financial stress.

At Wealth Collective, our process is designed to help you create a ‘wildly successful financial life’ by taking decisive control of your biggest debts. A paid-off mortgage isn’t the finish line; it’s the solid foundation for building real wealth.

This guide gives you the practical knowledge to get started. But turning that knowledge into a plan that works for you is where the real progress begins.

Our job at Wealth Collective is to translate complex options into clear, actionable advice that fits your unique situation. It all starts with a simple chat to understand what you’re trying to achieve. From there, we can build the roadmap that leads to your debt-free future.

The Simple Power of Extra Repayments

If you’re looking for the most straightforward way to get ahead on your home loan, making extra repayments is it. It’s incredibly effective because every extra dollar you pay goes straight to your principal balance, not just servicing the interest.

This simple shift means less interest accrues over time, and more of your future payments go towards owning your home outright. Instead of a sacrifice, think of it as a direct investment in your financial freedom.

What a Small Change Can Actually Do

Let’s look at a real-world example to see what this means in practice.

Imagine you have a home loan for $688,036, which is about the average for Western Australia. On a standard 30-year term with an interest rate of 5.50%, your monthly repayments would be around $3,907.

What if you chipped in an extra 10% each month? That’s about $391. By making this small, consistent addition, you could wipe nearly 10 years off your loan term and save a staggering $250,000 in interest. That’s a massive win from a relatively small change.

This is a core principle we build on in our ‘Guided Growth’ service, which is tailored for young professionals and families looking to get ahead. You can find more strategies in our guide on how to pay off debt faster.

A Clever Hack: Change Your Payment Frequency

Here’s another tactic that doesn’t feel like a huge sacrifice: switching your payment schedule. Most loans default to monthly repayments, meaning you make 12 payments a year.

A simple switch to fortnightly payments can make a surprising difference. Here’s why:

- Monthly Payments: 12 payments per year.

- Fortnightly Payments: You pay half your monthly amount every two weeks. Because there are 26 fortnights in a year, this adds up to 13 full monthly payments.

That extra payment is a secret weapon, working silently to eat away at your principal faster. It’s an almost effortless way to accelerate your progress.

A quick word of caution: before you make the switch, check with your lender. Confirm that they apply the extra funds directly to your principal and don’t charge fees for changing your payment schedule.

Extra Repayments Impact on a $688,036 WA Mortgage at 5.50%

The numbers speak for themselves. This table breaks down how powerful chipping in a little extra each month can be on that same average WA mortgage.

| Extra Monthly Repayment | New Loan Term | Total Interest Saved (Approx.) |

|---|---|---|

| $200 | 24 years, 5 months | $144,000 |

| $400 | 20 years, 3 months | $252,000 |

| $600 | 17 years, 3 months | $330,000 |

| $1,000 | 13 years, 3 months | $435,000 |

The results are incredible. Finding an extra $200 a month—perhaps by cutting back on a few takeaways—shaves more than five years off the loan and puts over $144,000 back in your pocket.

That's the power of consistency. It's not about making one huge payment; it's about building a small, sustainable habit that pays massive dividends over time.

Every little bit helps. At Wealth Collective, our process involves analysing your cash flow to find these exact opportunities, building a clear plan to make mortgage freedom a reality sooner. Book a call to find out how.

Using Strategic Tools Like Offset and Redraw Accounts

Making extra repayments is a great start, but to supercharge your progress, you need to use the powerful tools built into modern home loans. The two heavy hitters are the offset account and the redraw facility.

Understanding how these work—and more importantly, which one is right for you—can shave years and tens of thousands of dollars off your loan. These features are especially handy if you have a variable income or want your savings to work harder for you.

How an Offset Account Works

An offset account is a transaction account linked to your mortgage. Its superpower is that any money in the account is "offset" against your loan balance when interest is calculated.

Let's say you have a $500,000 mortgage. If you keep $50,000 in a linked offset account, the bank only charges you interest on $450,000. Every dollar in that account is effectively earning a return equal to your mortgage interest rate—tax-free.

It’s the perfect place to park your emergency fund and regular savings. This way, your cash is constantly chipping away at your interest bill while remaining completely accessible.

The Power of Redraw Facilities

A redraw facility works differently. It gives you the ability to pull back any extra money you've paid into your loan over and above the minimum repayments.

When you make extra payments, you build up a "redrawable" balance. If you need cash down the track, you can dip into that pool. It’s a good safety net, but it's not the same as having your money in a separate account.

An offset account keeps your savings separate from the loan, offering maximum flexibility. A redraw facility absorbs your extra payments into the loan itself, which can be a more disciplined approach but may have different tax implications and accessibility rules.

Figuring out which structure suits your financial habits is a cornerstone of a solid debt reduction plan. As part of the Wealth Collective process, we help clients make this exact choice to fit their cash flow and long-term goals.

Offset vs Redraw: Which Is Right for You?

The best choice comes down to your personality, cash flow needs, and whether the property is your home or an investment.

Here’s a quick breakdown:

| Feature | Offset Account | Redraw Facility |

|---|---|---|

| Flexibility | High. It’s like a normal bank account with a debit card and instant online access. | Lower. You usually need to request to redraw funds, which isn’t always instant. |

| Interest Savings | Excellent. You get the full interest-saving benefit while keeping your cash separate. | Excellent. Also lowers your interest bill by reducing the loan principal directly. |

| Discipline | Lower. The easy access can be a temptation to spend what you’ve saved. | Higher. The extra step of applying to redraw makes you think twice. |

| Tax Implications | Clearer. Keeping funds separate is crucial for investment properties to avoid mixing debts. | Complex. Redrawing money from an investment loan for personal use can get messy at tax time. |

Offset accounts are a game-changer for paying down your mortgage faster. We see this all the time with our clients in Western Australia, where average monthly loan repayments are around $3,907. Parking $50,000 in an offset against an average $688,036 WA loan (at a 5.50% rate) means you’re only paying interest on $638,036. That simple move could save you $2,750 in interest in the first year alone.

This strategy is so effective that extra payments into offsets and redraws have remained well above the historical average, as shown in this detailed report from Roy Morgan.

Making Your Choice a Reality

Choosing the right tool makes a massive difference. For most people, a 100% offset account delivers a winning combination of flexibility and powerful interest savings. It turns your everyday cash into a debt-busting machine.

The Wealth Collective process starts with understanding your financial world. Whether you need the flexibility of an offset or the discipline of a redraw, we’ll provide clear, practical guidance. Our mission is to help you build a wildly successful financial life, and it all starts with an initial call.

Want to Get Ahead Faster? Look at Smart Refinancing

Making extra repayments and using an offset account are fantastic habits. But if you’re serious about making a massive dent in your mortgage, it’s time to consider a smart refinance. This is a powerful move to put the accelerator down on your debt-free journey.

Refinancing is a strategy thousands of Australians use to get ahead. The key is what we call the ‘double-dip’ benefit. First, you lock in a better interest rate, which instantly reduces your minimum repayment. Then, you keep your repayments at the old, higher amount. That difference becomes a powerful, recurring extra repayment that chips away at your principal.

The Double-Dip Effect in Action

Let’s look at how this plays out in the real world. We recently worked with a young professional couple, Tom and Sarah, as part of our Guided Growth service. They had a $650,000 mortgage with an interest rate of 6.2%, meaning their minimum monthly repayment was $3,975.

We helped them refinance to a more competitive rate of 5.5%. Here’s where the ‘double-dip’ kicked in:

- The New, Lower Repayment: Their new minimum monthly payment dropped to $3,691—an immediate saving of $284 every month.

- Maintaining the Old Payment: Instead of lowering their direct debit, they kept paying the same $3,975 they were already used to.

That extra $284 each month now goes straight onto their principal balance. This simple change is set to save them over $80,000 in interest and cut more than four years off their 30-year loan. It’s a perfect example of turning refinancing from a simple cost-saving exercise into a true debt-reduction weapon.

To dive deeper into how this works, read our complete guide to refinancing your mortgage.

Why It’s a Great Time to Review Your Loan

The home loan market is incredibly competitive, meaning there are almost always opportunities to find a better deal. Refinancing is a powerhouse move, with around 34,800 Australian homeowners doing it every month.

Think about the average loan in Western Australia, which is around $688,036. On a 5.50% interest rate, refinancing to a sharper rate of 4.85% could free up over $500 a month. If you plough that extra cash back into the mortgage, you could knock 7-10 years off your loan term.

Refinancing isn’t just about the transaction; it’s a strategic reset. It lets you take advantage of market conditions and your improved financial standing to get a loan that actively helps you pay it off faster.

This is exactly the kind of proactive approach we help our clients with. We don’t just shop for a lower rate; we design a loan structure built around your goal of becoming debt-free sooner.

Get More Control with Advanced Loan Structuring

Beyond just finding a lower rate, refinancing opens the door to smarter loan structures that give you a balance of security and flexibility. One of the most effective strategies we use is splitting a loan.

A split loan allows you to divide your mortgage into two (or more) parts:

- A Fixed-Rate Portion: This part has its interest rate locked in for a set term (usually 1-5 years), protecting you from rate rises on that chunk of your debt.

- A Variable-Rate Portion: This part’s interest rate moves with the market. Crucially, this portion usually comes with an offset account and the ability to make unlimited extra repayments.

This hybrid approach can give you the best of both worlds: stability from a fixed rate and the flexibility to attack your debt on the variable portion.

This kind of tailored loan structuring is a core part of the personalised plans we create for clients in our ‘Guided Growth’ and ‘Retirement Roadmap’ services. It’s about moving beyond a generic loan to a structure that’s perfectly suited to your ambition to own your home outright. When you’re ready to see what’s possible, booking a call is the best way to get started.

Should You Pay Down The Mortgage Or Invest?

You’ve found extra cash in the budget and you’re making great progress. This is where a big question often pops up: do you throw every spare dollar at the mortgage, or is it smarter to start investing in assets like shares?

There isn’t a one-size-fits-all answer. The right move boils down to your personal financial situation, your long-term goals, and how comfortable you are with risk. This is less about simple maths and more about smart wealth strategy.

The Guaranteed Return vs. Potential Growth

Paying down your mortgage gives you a predictable outcome. Every extra dollar you put into your loan delivers a guaranteed, tax-free ‘return’ equal to your interest rate. If your mortgage rate is 5.5%, chipping away at that debt is the same as earning a 5.5% return on your money, with zero risk.

Investing, on the other hand, is about potential. Over the long haul, returns from assets like shares could be much higher. But those returns are never guaranteed. They come with market risk, and any profits you make will likely be taxed.

At its heart, this is a classic tug-of-war: the security of owning your home outright versus the long-term growth potential of investing. It’s a battle between logic and the powerful emotional pull of being completely debt-free.

This is exactly the kind of decision where personalised advice is a game-changer. It ensures the path you choose truly lines up with the financial life you want to build.

A Framework For Making Your Decision

So, how do you work through this? It helps to run through a mental checklist.

- Your Interest Rate: If you’re on a loan with a high interest rate, aggressively paying it down is often a clear winner. It’s tough for any low-risk investment to beat the guaranteed savings.

- Your Risk Tolerance: How would you sleep if your investment portfolio suddenly dropped by 20%? If that thought makes you anxious, the certainty of extra mortgage repayments is probably a better fit.

- Your Time Horizon: If retirement is decades away, you have time to ride out market bumps. This can make investing look more appealing. But if you’re nearing retirement, the security of a paid-off home might be your top priority.

- The Tax Factor: The ‘return’ from paying down the mortgage on your home is tax-free. Investment returns, whether from dividends or capital gains, are usually taxable, which eats into your profit.

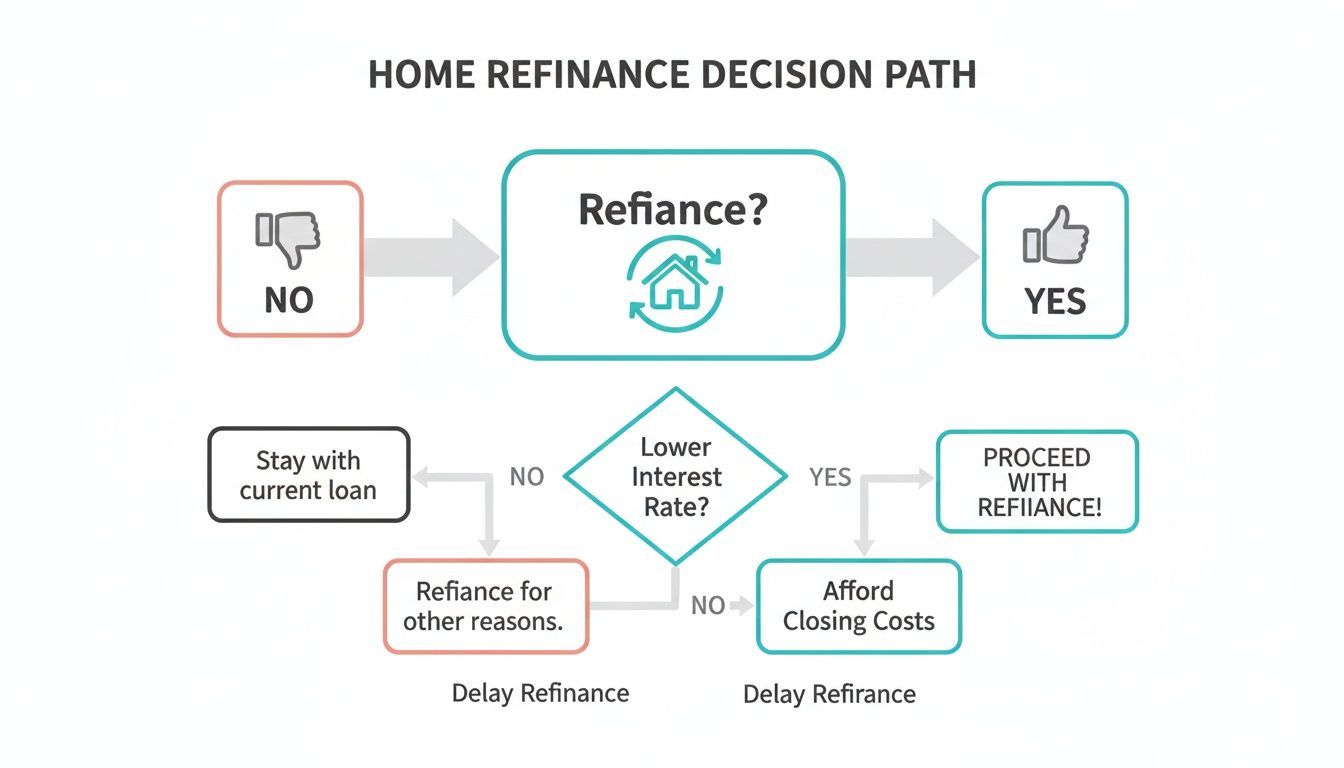

This decision tree helps visualise some of the key factors, particularly when considering refinancing to unlock equity.

As the flowchart shows, it’s not just about a lower rate. The costs involved and your bigger picture plan are just as important, reinforcing why a strategic approach is key.

The Power Of Opportunity Cost

At the centre of this debate is a concept called opportunity cost. In simple terms, by choosing to put your money in one place (your mortgage), you’re giving up the potential returns it could have earned somewhere else (like the share market).

For example, if your mortgage rate is 5% but you feel confident you could earn an average of 8% a year from a diversified portfolio, the opportunity cost of paying down your mortgage is that extra 3% you’re missing out on.

This is where more advanced strategies like debt recycling can be effective. For those with a higher risk appetite, it offers a way to potentially have the best of both worlds. You can learn more in how to debt recycle in our detailed guide.

Finding Your Path With Wealth Collective

Ultimately, the ‘pay mortgage vs. invest’ dilemma is a deeply personal one. There’s a huge emotional reward that comes with being debt-free, a fantastic goal we help many clients achieve through our Retirement Roadmap service.

For other clients, especially younger ones on our Guided Growth plan, using that capital to build an investment portfolio often makes more sense for their long-term wealth creation goals. The most important thing is to make a conscious, informed decision.

Our process at Wealth Collective is designed to bring total clarity to this exact crossroad. It all starts with a complimentary call to understand where you are now and where you want to be. From there, we can help you model different scenarios, weigh the risks and rewards, and build a plan that makes you feel confident and in control of your financial future.

Putting It All Together: Your Personalised Mortgage Freedom Plan

You’ve seen the strategies. You understand the numbers. Now for the most important part: turning theory into a real-world plan that actually works for you.

After all, knowing about offset accounts is one thing; building a clear, actionable roadmap is another. The path for a young professional will look very different from someone planning for retirement. Your strategy must be built around your life. This is where we bridge that gap.

It All Starts With a Quick Chat

Our process begins with a simple, no-obligation 10-minute phone call. This isn’t a sales pitch. It’s a chance for us to listen and understand what you’re trying to achieve, whether that’s getting out of debt as fast as possible or using home equity to build wealth.

A financial plan shouldn’t be a dusty document you look at once a year. It needs to be a living strategy that feels clear, achievable, and gets you excited about your future.

From that first conversation, we start piecing together the puzzle. We’ll help you figure out the right mix of strategies, structure your finances to be as efficient as possible, and ensure you feel in control.

From a Plan on Paper to Real Progress

Once we’ve got a solid plan in place, our job is to make sure it happens. We’re here for the long haul, providing ongoing support and evolving your plan as your life does. Think of us as your financial co-pilot.

We help you get definitive answers to big questions, like:

- What should I do first? We’ll model the outcomes of focusing on extra repayments versus investing, so the best first move becomes obvious.

- How should my loans be set up? Is a split loan the right call? Does an offset account make sense? We’ll find the optimal structure.

- When do I need to change course? Life happens. When your income changes or the market shifts, we’re right there to help you make smart adjustments.

Whether you’re early in your career and a fit for our ‘Guided Growth’ path, or you’re mapping out your next chapter with our ‘Retirement Roadmap’ service, we’ll bring the clarity you need.

A debt-free life isn’t just a dream. It starts by taking that first small step to build a plan that makes it your reality.

At Wealth Collective, we specialise in turning financial complexity into simple, powerful advice. Let’s build the plan that gets you to mortgage freedom, sooner.

Book your complimentary initial call today to start the conversation.