Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

When most people think of investing, they picture the frantic, high-stress world of stock traders glued to their screens. But true wealth isn't built that way. It's built slowly, deliberately, and with a healthy dose of patience.

This is the essence of long-term investing: a strategy focused on buying quality assets and holding them for an extended period, typically five years or more. It’s the cornerstone of the strategies we build at Wealth Collective to help our clients achieve financial freedom.

What Is a Long-Term Investment and Why Does It Matter?

Think of it like planting a tree rather than trying to win the lottery. You're not looking for a one-off jackpot; you're nurturing an asset that will grow steadily, year after year, eventually becoming a source of significant and lasting value. It's a fundamental shift in mindset—from gambling on short-term price swings to strategically owning a piece of a growing business or asset.

At its core, this approach is about letting time become your most powerful ally in wealth creation.

The Real Magic: Patience and Compounding

The secret sauce behind successful long-term investing is compounding. It's a simple but incredibly powerful concept: the returns your investments earn start earning returns of their own. It’s a financial snowball effect that can turn modest, regular savings into a life-changing nest egg over time.

A long-term investment strategy is about giving your money the two things it needs most to grow: time and a clear purpose. It’s the foundation for turning today’s savings into tomorrow’s financial freedom.

This is how disciplined habits create real wealth. What might seem like small contributions today can accumulate into a surprisingly large sum after a decade or two, thanks to the power of compounding.

Riding Out the Market Waves

Financial markets are notoriously jittery. Headlines scream, prices jump up and down, and it's easy to get caught up in the anxiety of it all. But a long-term investor learns to see this daily volatility for what it is: noise.

Instead of reacting emotionally, the goal is to stay focused on the big picture. History has shown time and again that markets reward those who have the discipline to wait out the storms. This disciplined approach is central to how we guide our clients.

To see just how different the mindset is, it helps to compare it directly with the high-octane world of short-term trading.

The Power of Time: Short-Term Trading vs Long-Term Investing

This table highlights the fundamental differences in approach, goals, and likely outcomes between the two strategies.

| Aspect | Short-Term Trading | Long-Term Investment |

|---|---|---|

| Time Horizon | Days, weeks, or months | 5+ years, often decades |

| Goal | Quick profits from market volatility | Substantial wealth growth over time |

| Methodology | Technical analysis, market timing | Fundamental analysis, asset quality |

| Mindset | Speculator / Gambler | Owner / Partner |

| Activity Level | High (frequent buying/selling) | Low (buy and hold) |

| Emotional State | High-stress, reactive, anxious | Calm, patient, disciplined |

| Primary Risk | Timing the market incorrectly | Not giving investments enough time |

As you can see, these are two completely different worlds. One is a high-stress sprint, while the other is a steady, well-paced marathon where time does most of the heavy lifting.

Beyond just reducing stress, a long-term approach comes with very real, practical advantages:

- Lower Costs: The less you trade, the less you pay in brokerage fees and other transaction costs that slowly chip away at your capital.

- Greater Tax Efficiency: In Australia, holding an asset for more than 12 months means you could be eligible for a 50% discount on any Capital Gains Tax (CGT) you owe when you sell.

- Proven Historical Returns: You participate in the market’s long-term upward trend instead of trying to guess its next move.

The proof is in the numbers. Over the 126 years to 2026, the Australian sharemarket delivered an impressive average annual return of 13.0% when dividends were reinvested. You can dive into the specifics by checking out the full historical market returns and performance data.

This long-term perspective is the bedrock of our philosophy at Wealth Collective. We focus on building clear, actionable plans that harness the power of time, turning your patience and discipline into tangible financial success.

Building Your Wealth with Key Australian Asset Classes

When you’re starting to invest for the long term, it’s helpful to think of it like building a well-balanced team. You wouldn’t rely on just one star player; you need a mix of different skills and strengths working together. In the world of investing, these players are your asset classes, and each has a specific role to play in growing your wealth.

Getting to know these core building blocks is the first real step towards putting together a portfolio that’s not only strong and diversified, but also makes sense for your personal goals. Let’s break down the main options you’ll come across on the Australian investment scene.

Shares: Owning a Piece of the Action

Buying shares (often called stocks or equities) is simply buying a small slice of a publicly listed company. You become a part-owner in a business you believe has a bright future, whether that’s a big bank, a household-name retailer, or an up-and-coming tech firm.

If the company does well and its value grows, so does the value of your shares. On top of that, many companies share their profits with their owners through regular payments called dividends. The big drawcard for shares is their potential for strong capital growth over many years. But this potential for higher returns comes with higher risk, as share prices can be volatile and bounce around day-to-day.

Exchange Traded Funds (ETFs): The All-in-One Basket

If picking individual shares feels a bit daunting, an Exchange Traded Fund (ETF) might be a great fit. Think of it like this: instead of buying individual ingredients, an ETF lets you buy a whole basket of them at once. It’s a single fund that holds a huge range of investments—like shares in hundreds of different companies—but you can buy and sell it on the stock exchange just like a single share.

This is the easiest way to achieve instant diversification, which is the golden rule of managing investment risk.

- Broad Market Access: With one transaction, you can invest in an entire market index, like Australia’s top 200 companies (the ASX 200).

- Lowered Risk: Because your money is spread across so many companies, the failure of one or two won’t sink your entire portfolio.

- Cost-Effective: ETFs generally have much lower management fees than old-school managed funds, so more of your money stays invested and working for you.

For many people, ETFs are the perfect foundation for a long-term portfolio. They offer a simple, powerful way to get broad market exposure without having to become an expert stock-picker.

Investment Property: The Tangible Asset

For many Aussies, nothing feels more real than bricks and mortar. Buying an investment property means you own a physical asset that can generate a steady stream of rental income while hopefully growing in value over the long term.

An investment property provides a tangible sense of ownership and can offer unique benefits like rental income and tax advantages. However, it’s a significant commitment that requires careful planning and a clear understanding of its role in your wider financial strategy.

The catch? Property is ‘illiquid’, meaning you can’t just sell off a bedroom if you need quick cash. It also demands a large upfront investment and comes with ongoing costs like council rates, maintenance, and property management fees. If you’re considering this path, it’s crucial to do your homework. You can learn more in our detailed guide on how to buy an investment property in Australia.

Superannuation: Your Hidden Investment Powerhouse

It’s easy to forget about your super, but it’s probably one of the most powerful investment tools you have. It’s not just a retirement savings account; it’s a highly effective, low-tax environment designed specifically to grow your wealth over your entire career.

Inside your super fund, your money is already invested across a mix of assets like shares, property, and bonds. The biggest advantage is the tax treatment. Investment earnings inside super are taxed at a maximum of just 15%, which is a huge discount compared to the marginal tax rates most of us pay on other income. Over decades, that tax saving massively boosts the effect of compounding.

The default investment option your fund puts you in might not be the best fit for your age or goals. Taking control of your super’s asset mix is one of the smartest financial moves you can make. At Wealth Collective, our Guided Growth service is all about helping you build a cohesive strategy across all your investments—inside and outside of super. We turn financial complexity into a clear, actionable plan to make sure every dollar is working hard for you.

To start building a portfolio that truly reflects your ambitions, book a complimentary 10-minute introductory call with our team today.

Matching Your Strategy to Your Life Stage

A good investment strategy isn’t a static document you file away and forget. It needs to live and breathe with you. After all, the plan that makes sense for a 25-year-old starting out is going to be wildly different from what a 60-year-old needs as they eye retirement.

Think of it this way: you wouldn’t use a street map of Sydney to navigate the Melbourne CBD. In the same way, your investment approach has to match your specific circumstances—your age, your goals, and how much time you have on your side. Getting this right is what separates a generic, off-the-shelf plan from a strategy truly built for you.

At Wealth Collective, we don’t believe in one-size-fits-all advice. We start with where you are right now and where you want to be, then build a plan that gets you there.

For Young Professionals: Time Is Your Superpower

If you’re in your 20s or 30s, your biggest asset isn’t your current bank balance. It’s the decades of time stretching out in front of you.

With such a long runway, you can afford to take on more calculated risks to chase higher growth. The market will inevitably have its ups and downs, but when you have 30 or 40 years to let your money work, those bumps in the road become far less terrifying. The focus here is all about accumulation.

- Go for Growth: Your portfolio can be heavily weighted towards assets like shares and ETFs. The aim is to get the magic of compounding working for you over the longest possible timeframe.

- Get Consistent: Forget trying to perfectly time the market. The simple habit of investing a set amount regularly—even a small one—is infinitely more powerful over the long haul.

- Handle Debt Smartly: It’s a balancing act. You need to weigh up investing against paying down any high-interest debt, like credit cards or personal loans.

Our Guided Growth service is built for this exact stage of life. We work with young professionals and families to build a rock-solid financial base, get their superannuation firing on all cylinders, and turn their long time horizon into a massive financial advantage.

For High-Income Earners: The Focus Shifts to Efficiency

As your income climbs, so does your tax bill. For high earners and executives, a sharp investment strategy is as much about what you keep as what you earn. The game shifts from simple accumulation to building a sophisticated, tax-efficient portfolio.

Suddenly, you can’t just look at an investment’s potential return; you have to analyse it through a tax lens.

For high earners, every investment decision must be viewed through a tax lens. The right structures can dramatically accelerate wealth creation by minimising tax drag and maximising your net returns year after year.

This is where strategies like using investment trusts or companies come into play. It’s about maximising your concessional super contributions and choosing assets that come with tax perks, like shares paying franked dividends. The goal is to build a structure that protects your wealth from being needlessly eroded by tax.

For Small Business Owners: Integrating Business and Personal Wealth

When you run your own business, the lines between your personal and company finances can get pretty blurry. A smart long-term plan has to acknowledge this, working to protect the business while tax-effectively pulling wealth out to build personal assets completely separate from the company.

The strategy is twofold: de-risk and diversify. Betting your entire future on the success of your business is a huge gamble. The smarter approach is to systematically build a personal investment portfolio that grows on its own, giving you financial security no matter how the business performs. This often involves careful structuring, succession planning, and funnelling profits into personal investments and super.

For Pre-Retirees: Protecting Your Capital and Creating Income

As you get closer to retirement, the mission changes completely. After decades spent growing your wealth, the new priorities are capital preservation and generating a reliable income to live on. The last thing you want is a sudden market crash to undo years of hard work right on the cusp of retirement.

This means rebalancing your portfolio to dial down the risk. You’ll likely shift away from high-growth assets and towards more stable, income-producing ones like quality bonds, blue-chip dividend shares, and annuities. Your superannuation strategy also pivots from accumulation to decumulation—that is, structuring it to pay you a tax-effective pension. Our Retirement Roadmap service is designed specifically for this critical transition, giving you a clear, stress-free plan to make your nest egg last a lifetime.

These personal strategies also exist within a wider economic context. For instance, Australia’s balance of payments data shows how long-term capital from overseas has always been a key ingredient in our nation’s growth. In 2024, foreign portfolio inflows hit a massive $191.6 billion. For our clients, whether they’re young professionals in WA or pre-retirees finalising their Retirement Roadmap, it means we can position their strategies to benefit from these powerful macroeconomic currents. You can dive into how international investment shapes our economy with the latest insights from the Australian Bureau of Statistics.

No matter your life stage, the right advice makes all the difference. To discuss a strategy that fits your personal circumstances, book a complimentary 10-minute introductory call with our team.

Getting Smart With Australian Tax and Superannuation

When it comes to long-term investing in Australia, understanding the tax and superannuation rules isn’t just about ticking boxes for the ATO. It’s about playing the game intelligently. Knowing how to use these rules to your advantage can be the difference between your wealth growing steadily and it taking off.

This is where our process at Wealth Collective adds significant value. We help our clients navigate this complexity, turning tax from a drag on their returns into a tailwind that accelerates their wealth creation.

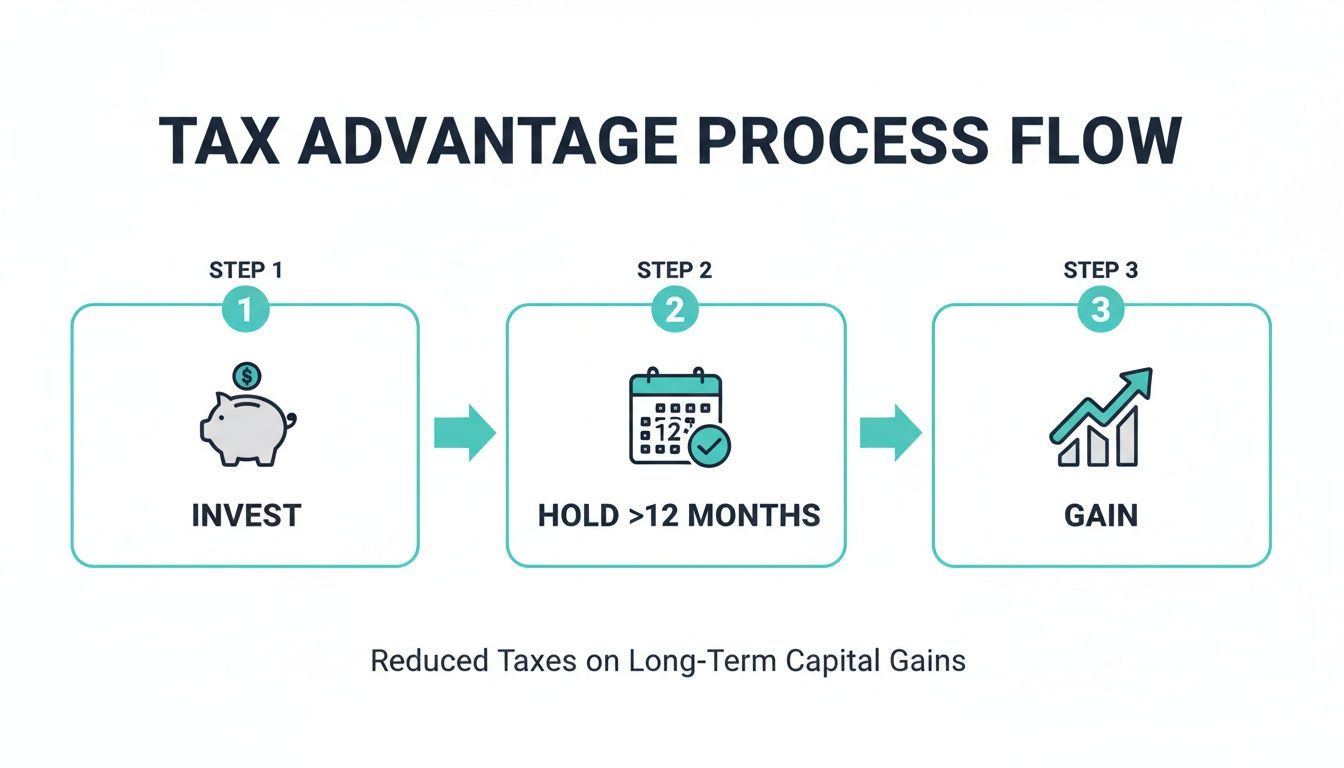

The 12-Month Rule: A Long-Term Investor’s Best Friend

One of the most significant perks for long-term investors in Australia is the Capital Gains Tax (CGT) discount. The concept is refreshingly simple: hold an asset for more than 12 months before you sell it, and you could cut your taxable profit in half.

Imagine you bought some shares and made a $20,000 profit. If you sell them after 11 months, that entire $20,000 gets added to your income for the year and taxed at your marginal rate. But if you just wait a little longer and sell after the 12-month mark, only $10,000 is considered taxable. Patience literally pays.

This isn’t just a tax break; it’s a built-in incentive that rewards a long-term, buy-and-hold approach and discourages reactive, short-term trading.

Why You Should Care About Franking Credits

You’ve probably heard the term franking credits (or imputation credits) mentioned alongside Aussie shares. It’s a clever system designed to stop company profits from being taxed twice—once when the company earns them, and again when you receive them as dividends.

Think of a franking credit as a tax voucher. The company has already paid tax on its profit on your behalf, and this voucher passes that credit on to you.

When you do your tax return, you can use these credits to lower your own tax bill. If your personal tax rate is below the company rate (currently 30%), you might even get a cash refund from the ATO. For anyone in a lower tax bracket, particularly retirees, this can turn franked dividends into a seriously attractive source of income.

Superannuation: The Ultimate Low-Tax Investment Vehicle

Your super fund is far more than just a nest egg for retirement. It’s arguably the most powerful long-term investment structure available to Australians, primarily because it’s a low-tax environment. While you’re working and growing your wealth, any investment earnings inside super are typically taxed at a maximum of just 15%.

Compare that to personal income tax rates, which can climb as high as 45% (plus levies), and you can see the enormous advantage. Over decades, that tax difference allows your money to compound much more aggressively than it ever could outside super.

Knowing how powerful your super is is the first step; taking active control of it is the next. You can get a clearer picture in our guide on what superannuation is and how it works in Australia.

This low-tax vehicle is the perfect place to capture long-term growth trends. For instance, foreign investment in Australia recently hit $4.97 trillion, growing at an average of 7.7% annually since 2003. Much of this capital is flowing into sectors like mining and renewables—opportunities that can be held within a super fund to turn global trends into personal retirement wealth. You can explore the full report on Australia’s investment profile for a deeper dive.

Making these rules work for you can feel overwhelming at first. A quick, no-obligation 10-minute introductory call is an easy way to see how professional guidance can help you protect and grow your wealth the smart way.

Your Step-by-Step Plan to Begin Investing

It’s one thing to read about investing, but it’s another thing entirely to put your money to work. This is where the rubber meets the road—moving from theory to action is how wealth is actually built.

To make it less intimidating, we’ve boiled it down to a simple, five-step process. This framework is the foundation of the Wealth Collective client journey, providing a clear path forward. Whether you’re starting from scratch or just want to make sure your current plan is on track, these steps show how we turn goals into reality.

Step 1: Define Your Financial Goals

Before you invest your first dollar, you need to know what you’re aiming for. Investing without a goal is like driving without a destination—you’re moving, but you have no idea if you’re getting any closer. Your goals are the ‘why’ that will keep you on track.

Are you aiming to buy a house in five years? Maybe you’re putting money aside for your kids’ education in 15 years’ time? Or is this all about building a nest egg for a comfortable retirement in three decades?

- Be Specific: Don’t just say, “I want to be wealthy.” A real goal sounds more like, “I want a $1.5 million portfolio by the time I’m 60 to fund my retirement.”

- Set a Timeline: Every goal needs a deadline. This timeframe determines your investment horizon and will heavily influence how much risk you can comfortably take on.

- Make It Measurable: Put a clear dollar figure on it. This is how you’ll track your progress and stay motivated when you see the numbers climbing.

Step 2: Honestly Assess Your Risk Tolerance

This part requires some real honesty. Your risk tolerance is basically your gut-check reaction to the market’s ups and downs. If your portfolio suddenly dropped by 15%, would you be up all night worrying, or would you see it as a chance to buy more at a discount?

There’s no right or wrong answer when it comes to risk. The only wrong answer is one that isn’t true to you. For a long-term plan to work, it has to be one you can actually stick with when things get choppy.

Getting this right helps us figure out the perfect mix of assets for you, balancing the need for growth with your desire for a good night’s sleep. It’s a non-negotiable part of our process here at Wealth Collective.

Step 3: Build a Diversified Portfolio

You’ve heard it a million times: “don’t put all your eggs in one basket.” That old wisdom is the absolute bedrock of smart investing. We call it diversification, and it just means spreading your money across different types of investments—like shares, property, and bonds—to cushion the ride. The idea is that when one part of your portfolio is having a bad month, another part might be doing well.

This is where all the different assets we’ve talked about come into play. For most people just getting started, a well-rounded portfolio of low-cost ETFs is a fantastic way to get instant diversification. If you want to dig a bit deeper into this, our guide on how to start investing covers these initial steps in more detail.

Step 4: Automate Your Contributions

Consistency is the superpower of any successful long-term investor. And the easiest way to be consistent? Make it automatic. Set up a recurring transfer from your bank account to your investment account for every time you get paid.

This simple habit, known as dollar-cost averaging, takes all the guesswork and emotion out of investing. You invest the same amount on a regular schedule, whether the market is up or down. You end up buying more units when prices are low and fewer when they’re high, which is a disciplined and powerful way to build wealth over time.

Step 5: Schedule Regular Reviews

Your life isn’t static, so your investment plan shouldn’t be either. Big life events—a promotion, a new baby, or simply getting closer to retirement—often mean your strategy needs a tune-up. Plan to sit down and review your portfolio at least once a year.

During this check-in, you’re just asking a few simple questions:

- Are my goals still the same?

- Does my mix of investments still suit my timeline and risk tolerance?

- Is my portfolio still balanced, or do I need to re-adjust it?

Speaking of strategy, one of the key advantages for long-term investors in Australia is how the tax system rewards patience. This is how it works.

The process is a powerful reminder that a simple buy-and-hold approach has real, tangible benefits built right into our system.

Working through these steps can feel like a lot, but you don’t have to figure it all out on your own. The team at Wealth Collective is here to give you clear, practical guidance.

Book a complimentary 10-minute introductory call today, and let’s start building a plan that’s right for you.

Your Top Questions About Long-Term Investing, Answered

It’s completely normal to have a few nagging questions, even when you feel ready to start investing. In fact, it’s a good sign—it shows you’re taking it seriously. We’ve heard just about every question in the book, so we’ve put together some straight-talking answers to the ones that come up most often.

How Much Money Do I Really Need to Get Started?

There’s a persistent myth out there that you need a huge lump sum to even think about investing. Thankfully, that’s just not true anymore. With the rise of Exchange Traded Funds (ETFs) and micro-investing apps, the barrier to entry has all but disappeared.

The secret to building real wealth over time isn’t how much you start with, but the power of consistent contributions. It’s all about creating a habit. Think of it like a tiny snowball at the top of a very long hill; your regular additions are what keep it rolling, gathering size and speed as it goes.

Honestly, the most important thing you can do is simply begin. A quick, complimentary chat with a Wealth Collective adviser can help you work out a comfortable starting point and turn that ‘one day’ idea into a solid plan you can act on today.

The question isn’t how much you need to start, but how soon you can begin. Time is the most valuable asset in any long-term investment strategy, and the sooner you start, the more of it you have on your side.

What if the Market Crashes Right After I Invest?

This is a big one, and it’s a fear that holds a lot of people back. Here’s where your long-term mindset becomes your superpower. Market dips, corrections, and even full-blown crashes aren’t a sign of failure; they are a completely normal and expected part of the investing cycle. What feels like a disaster in the heat of the moment is usually just a temporary blip on a multi-decade timeline.

History has shown us, again and again, that markets don’t just recover—they push on to new highs. For a disciplined investor, a downturn is actually a chance to buy quality assets while they’re on sale. The biggest mistake is to panic and sell, which locks in what was only a temporary paper loss.

This is exactly why having a robust financial plan is so crucial. A well-constructed strategy, like those we create with our Guided Growth service, is designed to ride out this kind of turbulence. It gives you the confidence to stick to the plan, knowing your portfolio was built for the entire journey, not just the sunny days.

Is Property a Better Long-Term Investment Than Shares?

Ah, the great Australian dinner party debate. The truth is, one isn’t inherently “better” than the other. It’s like asking if a hammer is better than a screwdriver—it all depends on the job at hand.

Property gives you something you can see and touch, and it offers the unique benefit of leverage (using borrowed money to invest). But it’s not without its challenges. It requires a massive amount of capital, it’s highly illiquid (you can’t just sell off a bedroom if you need cash), and the ongoing costs can be a real drain.

Shares, on the other hand, are incredibly flexible. You can invest with small amounts, diversify easily, and sell your holdings quickly if your circumstances change. The trade-off is that they can be more volatile in the short term. The most successful investors we see often use a smart combination of both.

The right mix for you comes down to your personal goals, your cash flow, your comfort with risk, and your timeframe. A Wealth Collective adviser can help you cut through the noise and weigh the pros and cons for your specific situation.

When Is the Right Time to Get Professional Financial Advice?

Many people assume financial advice is only for those who are already wealthy or on the cusp of retirement. In our experience, getting advice early is one of the most powerful things you can do to accelerate your wealth creation.

It’s the perfect time to speak with an adviser when you’re going through a major life event—a new job, getting married, starting a family—or when your finances just start to feel a bit too complicated to manage on your own. Sometimes, you just want a professional to look under the hood and make sure you’re still on the right track.

Our job is to bring clarity and confidence to your financial life. We take the complexity and translate it into a simple, actionable plan that puts you firmly in control.

At Wealth Collective, our entire purpose is to help you build your own wildly successful financial life. We do this by providing clear, jargon-free guidance that’s tailored to you. A free, no-obligation 10-minute introductory call is the easiest way to see if our approach is the right next step for you.