Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Refinancing your investment property isn’t just about shuffling paperwork. It’s a strategic decision that can seriously change how your portfolio performs. At its core, you’re swapping your current investment loan for a new one, hopefully one with better terms to reduce your repayments, unlock some equity, or even consolidate other debts.

Is Now the Right Time to Refinance?

For most Aussie property investors I speak with, the real question isn’t what refinancing is, but when to pull the trigger. And honestly, the economic climate in 2026 is creating a pretty interesting window, particularly for those of us here in Western Australia.

After a rollercoaster period of rate hikes, we’re finally seeing interest rates begin to stabilise. That stability gives investors a bit of breathing room to properly assess their loans, without the constant fear that another rate rise will immediately chew up any potential savings.

At the same time, property values across WA have been incredibly resilient. This growth has handed many investors a healthy chunk of equity in their properties—a powerful resource that’s just sitting there, waiting to be put to work.

Seizing the Moment in a Shifting Market

The decision to refinance is always a personal one, driven by your own goals. But the current market conditions are opening up some distinct opportunities.

I see investors taking advantage of this in a few key ways:

- Easing the Financial Squeeze: Think of a dual-income family in a Perth suburb. With the cost of living still high, refinancing their investment property to a lower rate can free up hundreds of dollars a month. That’s real money back in their budget.

- Fuelling Portfolio Growth: I have clients who’ve watched their property’s value soar. A cash-out refinance lets them tap into that new equity. They can then use that cash as a deposit to buy another investment property, using one asset to help secure the next.

- Boosting Retirement Cash Flow: Picture a pre-retiree in Dunsborough looking to step back from work. Refinancing can drop their monthly loan repayments, which means the net rental income supplementing their retirement nest egg gets a welcome boost.

This is the kind of strategic thinking that sets successful investors apart. It’s about seeing refinancing as a proactive tool for building wealth, not just a reaction to market news.

A savvy investor doesn’t just chase a lower interest rate. They use refinancing as a strategic tool to align their property debt with their life goals, whether that’s growing their portfolio or funding a better retirement.

The Numbers Driving the Trend

This isn’t just a gut feeling; the data backs it up. The Reserve Bank of Australia (RBA) reported that the average variable investment loan rate was sitting around 6.8% in late 2025—a huge jump from the historic lows we saw during the pandemic. Unsurprisingly, this has triggered a wave of refinancing activity.

Here in Western Australia, where we at Wealth Collective are based, we saw applications to refinance investment properties jump by 24% year-on-year in the third quarter of 2025. Investors are moving to tap into a national pool of home equity that has hit a record $1.2 trillion.

But getting this right is about more than just filling out a form. It demands a clear strategy. A proper loan review, guided by an expert, ensures your finance structure is actually supporting your goals. At Wealth Collective, whether you’re part of our Guided Growth or Retirement Roadmap service, our process always starts with understanding your specific situation. We take the complex market data and turn it into a clear, actionable plan so you can make decisions with confidence. Booking an initial call is the first step to making sure your property portfolio is working as hard as you are.

What a Smart Refinance Can Do For You

Refinancing your investment property isn’t just about chasing a headline interest rate. When done right, it’s a strategic move that can seriously turbo-charge your portfolio. A smart refinance makes your existing assets work much harder, unlocking benefits that go far beyond a slightly smaller monthly repayment.

Let’s look at what’s really on the table.

Secure a Lower Interest Rate

This is the most obvious win, and for good reason. Nailing a lower interest rate immediately cuts your monthly mortgage repayments, which directly boosts your property’s cash flow. Think of it as giving your investment a pay rise.

That extra cash each month isn’t just pocket money. You could use it to hammer down the loan principal faster, build a healthy cash buffer for those inevitable maintenance surprises, or even channel it into your next investment. It transforms a passive asset into an active part of your wealth creation strategy.

Access Equity to Fuel Your Next Move

As your property appreciates in value, so does your equity—the portion of the property you actually own. Refinancing is the key to unlocking that wealth, often through what’s known as a “cash-out” refinance. This is one of the most powerful plays for growing an investment portfolio.

We recently helped a small business owner through our Guided Growth service who did exactly this. They used a cash-out refi on their investment property to inject vital capital into their business, allowing them to buy new equipment and expand. This move saved them from taking out a separate, high-interest business loan. It’s a perfect example of using one asset to create another opportunity.

This strategy is incredibly common among savvy investors. With property values climbing, there’s a lot of equity sitting untapped. CoreLogic data from 2025 showed a national investment property value increase of 7.2%, which created a staggering $450 billion in new equity. Western Australia was a standout, with growth hitting 9.4%. It’s no surprise, then, that 72% of refinanced investment loans in Q2 2025 were cash-out refis, with investors pulling out an average of $120,000. You can dig into more of these trends in ICE Mortgage Technology’s August 2025 report.

By accessing equity, you’re not just taking out cash. You are strategically redeploying your capital from a dormant state into an active role, potentially funding your next property purchase or another high-growth investment.

Consolidate and Simplify Your Finances

Many investors are also juggling other debts like personal loans or credit cards, which almost always come with much higher interest rates. A refinance can be a great opportunity to roll these high-interest debts into your single, lower-rate investment loan.

The logic is simple and powerful:

- Massive Interest Savings: You’re swapping high-rate debt (like a credit card at 18%) for much cheaper mortgage debt (say, 6%).

- Easier Management: Instead of juggling multiple due dates, you have just one repayment to manage, making your finances much cleaner.

A word of caution here: it’s crucial to get this right. Mixing personal and investment debt has tax implications you need to understand. As we cover in our guide, you should always be aware of the tax benefits and rules for a rental property.

Switch to a Loan With Better Features

Sometimes, the rate isn’t even the main driver for a refinance. It’s about getting a loan with smarter features. Older loans are often bare-bones, but modern products have powerful tools that can save you a fortune over the long run.

The king of these features is the offset account. It’s a simple transaction account linked to your mortgage, but its effect is profound. Any money sitting in your offset account is subtracted from your loan balance before the bank calculates your interest. For a landlord with rental income flowing in every month, this is an incredibly effective way to slash interest costs.

To put it all together, here’s a quick worked example showing the clear financial impact of a strategic refinance.

Worked Example Refinance Savings Scenario

The table below shows a typical before-and-after scenario, illustrating how even a small rate change can add up to significant savings.

| Metric | Original Loan | New Refinanced Loan | Savings |

|---|---|---|---|

| Loan Amount | $500,000 | $500,000 | N/A |

| Interest Rate | 6.5% | 5.8% | 0.7% |

| Monthly Repayment | $3,160 | $2,935 | $225 per month |

| Annual Repayment | $37,920 | $35,220 | $2,700 per year |

As you can see, a modest 0.7% rate cut unlocks $2,700 in savings every single year. We often find our clients can put this money to much better use—whether it’s topping up their super, investing in the share market, or simply building a bigger safety net. It’s all about making your money work smarter for you.

Your Step-by-Step Guide to the Refinancing Process

Thinking about refinancing can feel overwhelming, but it doesn’t have to be. When you break it down into a clear, manageable path, you can approach the whole thing with a solid strategy. This is the exact process we walk our clients through, making sure we cover all the bases.

Let’s pull back the curtain on what’s really involved when you refinance an investment property.

Get a Clear Snapshot of Your Financials

Before you even start looking at new loans, you need a crystal-clear picture of where you stand right now. This is the bedrock of your entire application. Lenders will put your financial health under a microscope, so it pays to know your numbers first.

Get a handle on these three key areas:

- Your Equity: This is simply the difference between your property’s market value and what you owe. Most lenders want to see at least 20% equity to let you avoid paying Lenders Mortgage Insurance (LMI).

- Loan-to-Value Ratio (LVR): Think of this as the flip side of your equity. If you have 20% equity, your LVR is 80%. The lower your LVR, the more lenders will like what they see.

- Your Credit Score: Your credit history is a huge piece of the puzzle. A clean record and a strong score signal that you’re a reliable borrower, which can unlock the door to much better rates.

Taking stock of these figures gives you a realistic idea of what’s possible. It stops you from wasting time on applications that are dead in the water from the start.

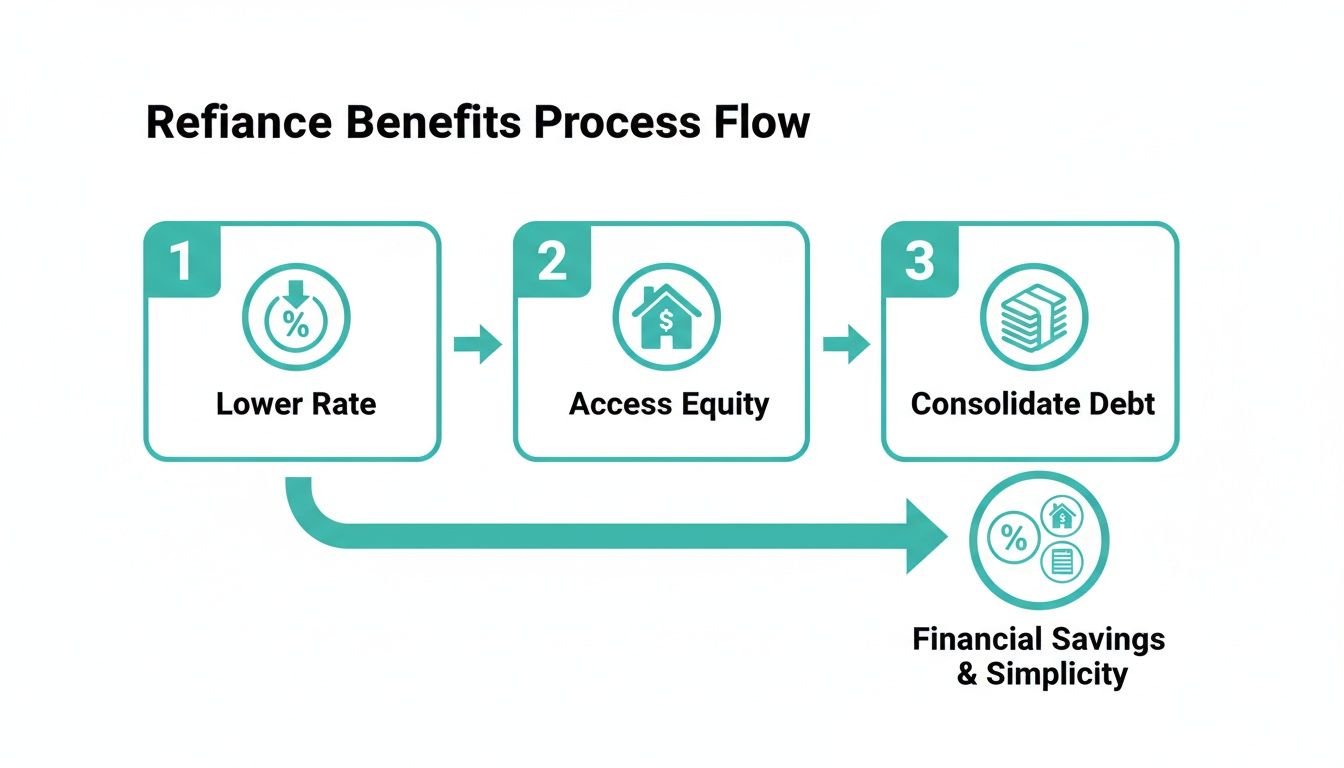

This is a great visual of the key benefits you can unlock with a smart refinance.

As you can see, it’s about more than just a lower rate. A good refinance can be a powerful tool for accessing equity to grow your portfolio or simplifying your finances by consolidating other debts.

Pinpoint Your Refinancing Goal

Once you know your numbers, you need to figure out what you actually want to achieve. A refinance without a specific goal is a recipe for getting a loan that doesn’t really serve your long-term strategy.

What’s the primary driver for you?

- Chasing a lower interest rate? This is all about improving your monthly cash flow and cutting down your total interest bill.

- Accessing cash-out? You might want to tap into your equity to fund a deposit for your next property, pay for renovations, or invest somewhere else.

- Getting better loan features? Maybe you’re after a loan with an offset account, so your rental income can work harder to reduce your interest payments.

Clarifying your main objective is crucial. It dictates which lenders and loan products are even worth looking at. For example, some lenders advertise amazing rates but have incredibly tight restrictions on cash-out. Knowing your goal helps you cut through the noise. You can dive deeper into the basics in our article that asks, what is a mortgage refinance?

Get Your Paperwork in Order

With a clear goal in mind, it’s time to start gathering your documents. Lenders need to verify everything, and having your paperwork ready from the get-go will make the entire process faster and smoother. A messy application is the quickest way to cause delays or even get a flat-out rejection.

Here’s an insider tip: Present your loan application like you’re applying for your dream job. A complete, organised, and professional submission tells the lender you’re a serious, low-risk borrower they want to work with.

You’ll need to pull together a file with things like:

- Income Verification: Recent payslips, your last two years of tax returns, and the corresponding Notice of Assessments.

- Property Details: A copy of the council rates notice for the investment property.

- Rental Income Proof: The current tenancy agreement and bank statements showing rent hitting your account.

- Existing Loan Statements: The last six months of statements for the mortgage you want to refinance.

- Other Financials: Statements for any other debts you have (like a car loan or credit cards) and your savings accounts.

Compare Lenders and Apply

Now for the exciting part—finding the right loan and submitting your application. It’s easy to get drawn in by the lowest advertised interest rate, but for an investor, that can be a costly mistake.

You need to look beyond the headline rate. Always compare the comparison rate, which factors in most of the ongoing fees. Also, watch out for application fees, discharge fees from your old lender, and make sure the new loan actually has the features you need.

Once you’ve picked your lender, you’ll submit the application along with all your documents. The lender then does their full credit assessment and, most importantly, orders a valuation on your investment property. This valuation confirms its market worth and locks in your final LVR.

After approval, loan documents will land in your inbox for you to sign and return. The final step is settlement. This is where your new lender pays out your old one, and your new loan officially kicks off. Having an adviser in your corner here is invaluable, as they’ll manage the back-and-forth between both banks to ensure it all happens smoothly.

Getting Real About the Costs and Risks of Refinancing

Refinancing an investment property can be an incredibly smart move for building wealth, but let’s be honest—it’s not a magic wand. Before you jump at a headline interest rate, it’s crucial to look past the marketing and understand the real costs and potential traps involved. Getting this wrong can turn a would-be win into a costly mistake.

First up, the fees. They aren’t hidden, but they can easily catch you off guard if you haven’t budgeted for them.

You’re typically looking at a few key expenses:

- Mortgage Discharge Fees: Your old lender won’t let you go for free. Expect a fee of a few hundred dollars to release their claim on your property title.

- Application Fees: The new lender might charge a fee to get your loan application processed. This can be anything from $0 to over $1,000, so it pays to ask upfront.

- Government Charges: Each state and territory has its own fees for registering the new mortgage and discharging the old one. Again, this usually adds up to a few hundred dollars.

These costs are exactly why chasing a tiny rate reduction doesn’t always make sense. You have to do the maths. A quick break-even calculation will tell you how long it’ll take for the savings from your new, lower rate to cover these initial outlays.

Don’t Fall Into These Common Refinancing Traps

Beyond the fees, there are a couple of major pitfalls I see investors fall into time and time again.

The biggest one? Accidentally extending your loan term. When you refinance, most banks will try to put you on a fresh 30-year loan by default. Say you’re already 10 years into your mortgage. Resetting the clock means you’ll be paying off your property for a total of 40 years. Even with a lower rate, you could pay tens of thousands more in interest over the long haul.

The fix is simple, but you have to be firm. Either tell your new lender to match your remaining loan term (in this case, 20 years), or commit to making higher repayments to stick to your original payoff date.

When you refinance an investment property, you’re not just tweaking your rate. You’re signing a brand-new legal contract. The details in the fine print—from the loan term to exit fees—can make or break the deal.

The Tax and LMI Headaches You Need to Avoid

Tax is another area where you need to be extremely careful. The Australian Taxation Office (ATO) is very clear on this: the interest on your investment loan is only tax-deductible if the borrowed funds are used for an income-producing purpose.

This gets tricky with a “cash-out” refinance. If you pull out $50,000 in equity to buy a car or renovate your own home, the interest on that $50,000 portion of the loan is not tax-deductible. You absolutely must keep clean records and separate your loan portions correctly to stay on the right side of the ATO.

Finally, don’t forget about Lenders Mortgage Insurance (LMI). If your refinance means your Loan-to-Value Ratio (LVR) creeps above 80%, you’ll probably have to pay for LMI all over again. This one-off premium can cost thousands and could completely wipe out any savings you hoped to gain from a better rate.

Juggling all these moving parts is genuinely complex. This is where getting professional advice is so important. A good mortgage broker or financial adviser can model the different outcomes, run a proper break-even analysis, and help you structure your loans to keep the ATO happy. Making sure your refinance is a clear financial win from day one is the only way to do it.

Your Refinancing Checklist and Next Steps

Alright, you’ve done the research and you’re seriously considering a refi for your investment property. Before diving in, it pays to get all your ducks in a row. A little prep work now can save you a world of hassle later.

Think of this as your pre-application game plan.

- Define Your “Why”: What’s the end goal here? Are you hunting for a sharper interest rate, or do you need to pull out equity for your next purchase? Your objective will shape the entire loan structure.

- Know Your Equity: Get a realistic valuation of your property to figure out your exact equity position and Loan-to-Value Ratio (LVR). This number is the bedrock of any refinance application.

- Check Your Credit Score: A healthy credit history is your golden ticket to the best rates and terms. It’s smart to know exactly where you stand before any lender runs a check.

- Do the Maths on Costs: Tally up all the potential expenses—discharge fees from your current lender, application costs, and any government charges. You need to be sure the long-term savings will make these upfront costs worthwhile.

- Get Your Paperwork Ready: Start pulling together payslips, tax returns, recent rental statements, and details of your existing loan. Being organised from the get-go will dramatically speed up the whole process.

Getting this right has never been more important. After the rate stabilisations of 2025, we’ve seen a huge return of investors looking to refinance as a wealth-building tool. Data from SQM Research shows rental yields for investment properties in WA averaged 4.8% in late 2025, a healthy jump from 4.1% in 2024. This has fuelled a refinancing boom, with 41% of recent transactions involving investors switching lenders to boost their returns.

The numbers back this up. ABS housing finance stats reported a 19% national increase in investment refi commitments in November 2025 alone. Perth was even hotter, with a 27% jump as savvy investors and dual-income families put smart debt reduction strategies into action.

How Wealth Collective Can Help

Once you’ve ticked off the items on that checklist, it’s time to bring in an expert. At Wealth Collective, our job is to cut through the complexity. We turn what can feel like an overwhelming task into a clear, strategic move that fits perfectly with your financial life.

It all starts with a simple, free, no-obligation 10-minute introductory call. This is just a chat—no pressure, no hard sell. It’s our chance to hear about your situation and your chance to see if we’re the right fit to help.

A refinance is more than a transaction; it’s a strategic part of your wealth journey. We make sure every decision serves your bigger picture, whether that’s expanding your portfolio, securing your retirement, or protecting your family.

We’re all about connecting the dots between your loan structure and your long-term ambitions. Here’s a glimpse of how a smart refinance aligns with our core services to help you build that wildly successful financial life.

- Guided Growth: Looking to expand your portfolio? A strategic cash-out refinance can unlock the deposit for your next property. We’ll guide you on structuring the debt correctly to maximise your borrowing power, which might involve a debt recycling strategy, which you can learn more about here.

- Retirement Roadmap: As you get closer to retirement, refinancing can be a powerful move to lower your monthly repayments. This instantly improves your cash flow by increasing the net rental income you can rely on, giving you more freedom and flexibility.

- Protection Plus: Any time you change your debt structure, it’s the perfect opportunity to review your personal insurances. We’ll make sure your new loan and overall financial position are properly protected, so your family and assets are secure no matter what comes your way.

Taking the next step is easy. Let us handle the complexity so you can focus on what matters.

Book your complimentary 10-minute call with the Wealth Collective team today and get personalised, actionable guidance to make your next financial move your best one yet.

Your Top Refinancing Questions, Answered

Deciding to refinance an investment property is a big move, and it’s completely normal to have a few lingering questions, no matter how solid your strategy feels. Let’s walk through some of the most common queries we get from property investors, clearing up the confusion so you can make your next move with confidence.

How Much Equity Do I Really Need?

As a general rule, lenders feel most comfortable when you have at least 20% equity in your investment property. This gets your loan-to-value ratio (LVR) down to that magic 80% mark, which is the key to avoiding Lenders Mortgage Insurance (LMI).

Can you do it with less? Sometimes. A handful of lenders might look at an application with as little as 10% equity (a 90% LVR), but you have to be prepared for the trade-offs. These loans almost always come with higher interest rates and a hefty LMI premium, which can quickly erode any savings you were hoping to make.

And if you’re looking to pull cash out, lenders get even stricter. Most will cap your LVR at 80% post-cash-out to maintain a safe buffer. This is where getting the right advice is crucial to figure out your true usable equity and find a lender whose policies align with what you’re trying to achieve.

How Does Refinancing Affect My Tax Deductions?

This is a big one, and getting it wrong can cause major headaches with the ATO. The interest on your investment loan is only tax-deductible when the funds are used for an income-producing purpose—in this case, your investment property.

If you pull out equity and use it for something personal, like a family holiday, a new car, or renovating your own home, the interest on that portion of the loan is not tax-deductible.

It’s vital to keep crystal-clear records that separate the investment and private portions of your loan. This can get complicated fast, and it’s one of the most important areas to seek professional advice. Getting it right means you can maximise every legitimate deduction without falling foul of the tax office.

What’s a Realistic Timeline for the Whole Process?

From start to finish, you should plan for the refinancing process to take around four to six weeks. That’s from the moment you submit your application to the day your new loan is officially settled.

This timeline isn’t set in stone, though. It can speed up or slow down depending on:

- The complexity of your finances and loan structure.

- How busy both your old and new lenders are.

- How quickly you can gather and provide all your documents.

Typically, the application review takes a week or two, followed by the valuation, formal approval, and finally, the settlement between the banks. An experienced broker or adviser can be your best friend here, helping you package your application perfectly to avoid unnecessary back-and-forth and keep things moving.

Is It Worth the Hassle for a Tiny Rate Reduction?

It absolutely can be, but you have to run the numbers. A small rate drop might not seem like much on paper, but when you’re dealing with a large investment loan, the savings add up fast.

Think about it: a 0.5% rate reduction on a $600,000 loan saves you $3,000 a year in interest. That’s an extra $250 in your cash flow every single month.

The key is to weigh those potential savings against any upfront costs of refinancing, like discharge fees or new loan establishment fees. A good adviser can run a quick break-even analysis for you, showing you exactly how many months it will take for the refinance to pay for itself. And remember, it’s not always just about the rate. Moving to a loan with better features, like an offset account, can offer a different kind of value that boosts your long-term financial position.

At Wealth Collective, we specialise in translating these complex financial decisions into clear, straightforward guidance. Our entire process is built to give you clarity and confidence.

Ready to find out if a strategic refinance could work for you? Book your complimentary 10-minute call with our team to get the conversation started.