Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

A lot of Western Australians reach the same point at the same time. The business is finally profitable, the mortgage is under control, there is money going into investments, and the family balance sheet looks stronger than it did five years ago. Then the harder questions arrive.

What happens if the business hits trouble. What happens if one family member earns far more than the others. What happens when investment income starts to build. What happens when you want to pass wealth to children without creating tax drag, avoidable risk, or a mess for the executor later.

The phrase family trust then often enters the conversation, followed by confusion. People hear that trusts help with tax, asset protection, and estate planning. They also hear that trusts are complicated, heavily scrutinised, and easy to get wrong if they are treated like a template instead of a strategy.

Both things are true.

A family trust can be one of the most useful structures available to a Perth professional, a Dunsborough family, or a WA business owner. Used properly, it can create flexibility around income, place a legal barrier between family wealth and outside risk, and make long-term wealth transfer cleaner. Used poorly, it becomes paperwork, cost, and compliance exposure.

The question is not whether trusts are “good” or “bad”. The essential question is how does family trust work in your circumstances, with your assets, your family, and your future plans.

Building and Protecting Your Family’s Wealth

For many WA families, wealth does not arrive as one lump sum. It builds in layers.

A couple in Perth might start with salaries, then add an investment portfolio. A business owner in Bunbury or Dunsborough might reinvest profits, buy premises, and accumulate surplus cash. A resources-sector executive may move from high PAYG income into shares, property, and retirement planning.

Over time, the same three concerns keep surfacing.

- Tax pressure: More income often means more of it lands in higher personal tax brackets.

- Risk exposure: Business ownership, directorships, and guarantees can place personal wealth in the firing line.

- Legacy planning: Families want control over who benefits, when they benefit, and how smoothly assets pass through generations.

A family trust sits at the intersection of all three. It is not a magic shield. It is a legal structure that can hold assets, receive income, and distribute that income under the terms of a trust deed. That combination is why it is widely used by business owners, investors, and higher-income households.

The value of a trust is not in the label. It is in the design.

Why families look beyond personal ownership

Owning everything personally is simple at the start. Salary lands in your own name. Shares are held in your own name. The investment property is in your own name.

That simplicity fades once wealth grows. Personal ownership can concentrate tax, expose assets to personal legal risk, and create less flexibility when family circumstances change.

A trust can improve that position because the trustee controls trust assets for a defined group of beneficiaries, rather than one individual owning everything outright. That separation is where the planning opportunities begin.

Practical takeaway: A trust works best when it is set up before the pressure point arrives. It is harder to retrofit protection after litigation, relationship breakdown, or a tax review is already on the horizon.

Where a trust fits in real advice

A trust is rarely the whole plan. It usually sits alongside super, insurance, personal ownership, companies, and estate planning documents.

That is why the best trust decisions are rarely product decisions. They are strategic decisions. The family trust should match the family’s income pattern, asset mix, risk profile, and succession goals. If it does not, the structure becomes more burden than benefit.

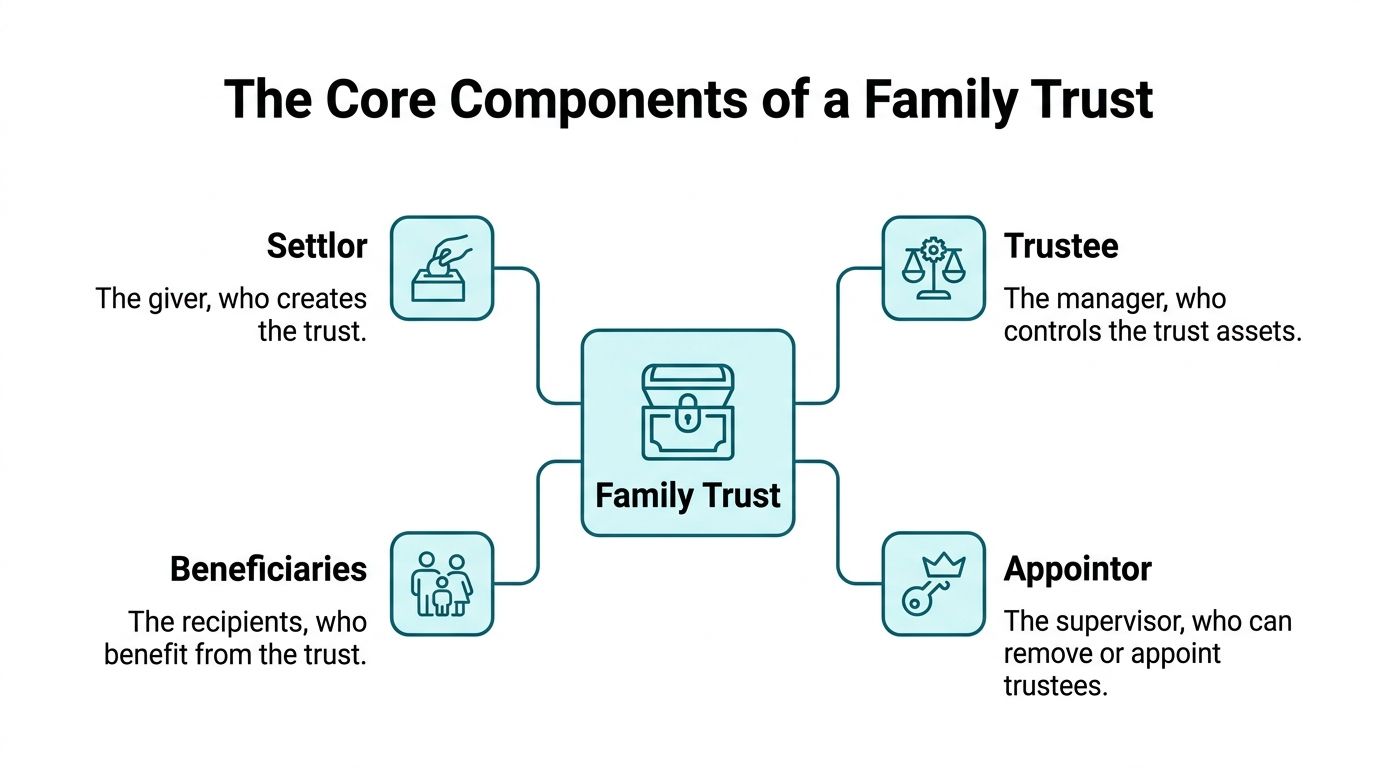

The Core Components of a Family Trust

A family trust only works as intended when each role is set up properly from day one. In practice, the strength of the structure comes from who holds power, what the deed allows, and how those decisions are documented.

For Perth families, Dunsborough property investors, and WA business owners with uneven income from construction, transport, or mining services, these details matter more than the name of the structure. A trust with the wrong controller or an outdated deed can create tax risk, family disputes, and avoidable compliance problems. The ATO has become more focused on trust distributions, trust losses, and unpaid present entitlements, so setup quality now matters just as much as tax planning.

The trust deed

The trust deed is the legal document that governs the trust.

It sets out the trustee’s powers, the range of beneficiaries, how income and capital can be appointed, how a trustee can be removed, and when the trust vests. It also determines whether the trust has enough flexibility to deal with future changes such as a new business venture, a family loan, or an adult child joining the investment structure.

This is one of the first areas I review in advice work because many problems start here. A deed drafted cheaply, copied from another state, or never updated can limit distribution options or create ambiguity at exactly the point the family wants flexibility. Good trust administration and tax planning for family groups and business owners starts with a deed that matches the actual strategy.

The key people in the structure

Four roles usually carry the structure.

- Settlor: The settlor starts the trust, usually by contributing a nominal settlement sum and signing the initial documents. After establishment, their involvement is generally very limited.

- Trustee: The trustee manages the trust, holds legal title to the assets, and makes decisions allowed by the deed. This can be an individual or a company.

- Appointor: The appointor usually has the power to remove and appoint the trustee. In many family groups, this is the primary control point.

- Beneficiaries: Beneficiaries are the people or entities eligible to receive income or capital, subject to the deed and the trustee’s decisions.

Each role should be chosen deliberately. In a WA family business, for example, parents may want one person handling day-to-day decisions while keeping long-term control tied to succession planning. If those roles are blurred, the trust can become difficult to manage when retirement, incapacity, or a family breakdown enters the picture.

Why control matters more than labels

Beneficiaries do not automatically control the trust just because they are intended to benefit from it. Control usually sits with the trustee and, one step above that, the appointor.

That distinction matters in real life. If a family trust owns a workshop in Malaga, a share portfolio, or an investment property near Busselton, the practical question is not who expects to benefit one day. The practical question is who can sign, decide, replace the trustee, and influence distributions under the deed.

A corporate trustee is often the cleaner option because it separates the trust role from the individuals involved and can simplify record-keeping when ownership changes over time. It also brings setup costs and annual ASIC obligations, so it is not automatic. For many WA families with meaningful assets or a trading business, though, the extra cost is often justified by better control and cleaner succession.

Key point: In a family trust, legal ownership, practical control, and economic benefit sit in different places. The structure works best when those positions are chosen deliberately, documented properly, and reviewed before family or business circumstances change.

How Income Tax and Distributions Work

A Perth couple with a family trust might finish June with rental income from an investment property, profits from a business in Osborne Park, and dividends from an ETF portfolio. The tax result does not depend on the trust alone. It depends on who is made presently entitled to that income under the deed, and whether the trustee records that decision properly before the deadline.

A discretionary family trust is usually not taxed like an individual when trust income is validly distributed. Instead, the trustee allocates income or capital gains to eligible beneficiaries for that financial year, and those beneficiaries are generally assessed on their share.

That flexibility is one of the main reasons family trusts remain common across WA, especially where household income is uneven from year to year. Mining contractors, medical specialists, and business owners often have one family member on a high marginal rate while another has lower taxable income. A trust can allow income to be directed more efficiently within the family group, but only within the limits of the deed and tax law.

What distribution really means

A distribution is a legal and tax decision, not a casual transfer between bank accounts.

The trustee must act within the trust deed, identify the beneficiaries who are to receive trust income or gains, and document the decision correctly. In many cases, that means trustee resolutions must be prepared by 30 June, although the deed can affect the timing and method. If the resolution is late, vague, or inconsistent with the deed, the tax outcome can unravel quickly.

This is an area where the ATO has paid close attention. Trustees need to be able to show that resolutions, accounts, beneficiary entitlements, and actual conduct all line up.

A practical example

Assume a family trust in WA earns $90,000 of net income from a share portfolio and a small commercial property. One beneficiary is a business owner already earning a strong salary. Another is a spouse working part-time. An adult child may also be within the beneficiary class, depending on the deed and the surrounding facts.

The trustee may decide to allocate more of that income to the lower-income adult beneficiaries if that is permitted and commercially sensible. Done properly, that can reduce the overall tax paid by the family group compared with holding the same assets personally in one name.

The attraction is simple. The trust gives the family options each year.

What happens if income is not distributed

Trustees regularly underestimate this point.

If trust income is not effectively distributed by the required time, the trustee can end up assessed on that income at the top marginal rate. For WA families running a trust alongside a business, that can turn a useful planning structure into an expensive compliance failure. The problem is often not the strategy. It is poor execution in late June, unclear deed wording, or accounts that do not match the resolution.

Adult beneficiaries and minor beneficiaries also need to be treated carefully. Distributions to minors can trigger penalty tax rates on unearned income, and arrangements that exist only on paper can attract ATO scrutiny.

Where a bucket company may help

Some family groups include a bucket company as a beneficiary. The idea is straightforward. If the deed allows it, part of the trust income can be distributed to that company, which may cap the immediate tax rate lower than leaving income taxed at the top individual rate.

That approach can be useful for Perth business owners with lumpy profits or families building capital for future investment. It also creates extra moving parts. Division 7A, unpaid present entitlements, and the later extraction of company profits all need careful handling. Used badly, a bucket company defers a problem instead of solving it.

For families weighing trust distributions against year-end cash flow, super contributions, and business structuring, a proper taxation and tax planning strategy usually matters more than any single distribution tactic.

Practical takeaway: The tax value of a family trust comes from valid annual resolutions, accurate records, and distributions that match both the deed and the family’s real financial position.

Protecting Your Assets and Planning Your Legacy

Tax starts the conversation. Asset protection is often what makes families keep the structure for decades.

The central legal idea is straightforward. Trust assets are held by the trustee for beneficiaries under the deed. That separation means assets are not automatically treated the same way as personally owned assets when a beneficiary faces business risk, personal liability, or family law pressure.

That is one reason trusts remain common among business owners, professionals, and families with meaningful investment holdings.

How the protection works in practice

A trust is not a force field. Courts and regulators look at substance, timing, control, and intent.

Still, a properly established and administered trust can create a strong protective boundary. In Australia, family trusts protect a substantial amount of assets. Following amendments to the Bankruptcy Act, assets held in a properly structured trust for more than two years are approximately 92% protected from creditors’ claims, and 78% of related WA Supreme Court cases from 2018-2023 were decided in favour of the trust, according to Australian Unity’s discussion of asset protection with a family trust.

That does not mean every trust wins. It means timing and structure matter.

Where WA families often see the value

A trust can be useful when one family member carries elevated commercial risk. That might be because they run a business, sit on boards, sign guarantees, or operate in an industry where claims and disputes are not unusual.

Holding selected assets outside personal ownership can reduce the chance that those assets are exposed in the same way as assets owned directly. The family home and personal protection strategies still need separate consideration, but for investment assets and business interests, the trust can be a valuable layer.

A trust can also create a better framework where there are concerns about future relationship breakdown within the family. The deed may give the trustee discretion over who receives distributions and when. That control can be useful, especially where parents want flexibility rather than fixed entitlements.

Estate planning without forcing everything through the estate

Trust-held assets do not pass under a will in the same way personally owned assets do. The estate planning focus shifts from “who inherits the asset” to “who controls the trust after death or incapacity”.

That distinction is critical.

If the succession of trustee and appointor roles has been thought through, a family can maintain continuity without disrupting the trust’s ownership of assets. This can help preserve privacy, reduce administrative friction, and keep the investment structure intact.

For some families, trust planning works best alongside a testamentary trust strategy for assets that will pass via the estate rather than sit inside an existing family trust.

Key takeaway: The trust does not replace estate planning. It changes what must be planned. Control succession becomes just as important as asset succession.

Real-World Scenarios for WA Families

The mechanics make more sense when you attach them to real life. These are the kinds of situations where a family trust often moves from abstract idea to useful structure.

The Perth business owner with uneven risk

A small business owner in Perth has spent years building a profitable operation. Most of the family wealth now sits outside the business itself, in cash reserves and investments. The problem is obvious. The business creates opportunity, but it also creates exposure.

Holding future investment assets in a discretionary trust can separate part of the family’s growing wealth from the day-to-day commercial risks tied to personal ownership. It can also give the family flexibility around distributions if the spouse or adult children have lower taxable income in future years.

This does not remove every risk. Personal guarantees, poor timing, and sloppy administration can still undo good intentions. But as part of a broader protection strategy, it can create a cleaner boundary between trading risk and long-term family capital.

The Dunsborough dual-income family building investments

A couple in Dunsborough both earn solid incomes. They are saving aggressively and want to build a portfolio of shares and managed investments. Their issue is not immediate asset protection. Their issue is future flexibility.

If they invest personally, each asset sits rigidly in one name or the other. If one person later takes time out of work, if income levels diverge, or if they sell assets with capital gains attached, personal ownership can become less efficient than it first appeared.

A trust can work well in this setting because it keeps options open. The family is not locking future investment income into one tax profile forever. It also creates a cleaner structure if the goal is to grow assets for children or future generations without handing over direct control too early.

The high-income executive preparing for retirement

A senior executive in WA often has a different profile. High PAYG income today. Strong super balances. Non-super assets building outside retirement savings. A desire to reduce complexity, not increase it.

For this client, the trust question is about how non-super wealth should be held as retirement approaches. A trust may sit alongside super to hold investments that need flexibility, family access, or a different estate planning path from the super system.

The benefit here is not only tax management. It is control. The executive may want a structure that can continue to hold assets, distribute income within the family group where appropriate, and support a smoother handover over time.

This is often where trust strategy intersects with wider succession planning for business owners and family wealth planning, even if the person is no longer actively running a business.

What these scenarios have in common

The details vary, but the pattern is consistent.

- They are solving a specific problem: risk isolation, tax flexibility, or generational planning.

- They are not using a trust in isolation: other structures still matter.

- They need good governance: the deed, the controller roles, and yearly resolutions all matter.

A family trust is most useful when it is tied to a clear purpose. If the answer to “why are we setting this up?” is vague, the structure usually is too.

Comparing a Family Trust to Other Structures

A family trust is powerful, but it is not always the best answer. Sometimes a company is cleaner. Sometimes super is the key engine room. Sometimes the right trust is a testamentary trust created through the estate plan rather than a discretionary trust created now.

The primary task is matching the structure to the job.

Family Trust vs. Other Structures at a Glance

| Feature | Family Trust (Discretionary) | Company (Pty Ltd) | SMSF | Testamentary Trust |

|---|---|---|---|---|

| Primary use | Family wealth holding, tax distribution flexibility, asset separation | Trading, retaining profits, business operations | Retirement savings and investment under super rules | Estate planning after death |

| Who controls it | Trustee, with oversight often sitting in the appointor role | Directors and shareholders | Individual or corporate trustees under super law | Trustee appointed under the will |

| Tax flexibility | High, if deed and beneficiary class support it | Lower flexibility for distributing profits personally | Governed by super rules, not family discretion | Flexible within estate planning terms after death |

| Asset protection | Often strong when properly structured and administered | Can protect company assets from shareholder personal ownership issues, but not a substitute for trust planning | Strong regulatory environment, but funds are preserved for retirement purposes | Useful for protecting inheritances and managing distributions to beneficiaries |

| Profit retention | Awkward if income is left in trust without planning | Simpler for retaining profits in the company | Not designed for business profit retention | Not relevant during the asset owner’s lifetime |

| Succession planning | Good if trustee and appointor succession is handled well | Requires share and directorship succession planning | Requires death benefit and trustee planning | Designed specifically for post-death control |

| Compliance feel | Moderate to high, depending on complexity | Moderate and familiar to many business owners | High and heavily regulated | Part of estate administration rather than annual operating structure |

| Best fit | Families wanting flexibility and protection around investments or business wealth | Businesses needing a trading vehicle or retained earnings | People focused on retirement savings strategy | Families wanting control over inheritances after death |

When a company may be better

A company makes more sense where the goal is active trading, straightforward profit retention, or a familiar governance structure. If the business needs a vehicle to operate in, invoice from, employ staff through, and retain profits within, a company is often the cleaner commercial tool.

What it does not offer is the same level of discretionary distribution flexibility to family members.

When super should lead the strategy

An SMSF can be useful where control over retirement assets is the priority. But super has its own legal environment, preservation rules, and benefit payment framework. It is not a general-purpose family wealth structure.

That is why many high-net-worth families use both. Super for retirement capital. Trusts for non-super assets and family flexibility.

When a testamentary trust is the right answer

A testamentary trust does not operate during your lifetime in the same way a family trust does. It is created through a will and comes into effect after death.

That makes it a succession tool, not an operating structure for current income and investments. It can be ideal for inheritance management, vulnerable beneficiaries, or blended family planning, but it solves a different problem.

Decision rule: If you need flexibility now, a family trust may fit. If you need retained business profits, a company may fit. If you need retirement regulation and concessional treatment, super may fit. If you need post-death control, a testamentary trust may fit.

Your Setup Checklist and Common Pitfalls to Avoid

A Perth couple buys an investment property through their family trust, but the loan documents go in their personal names, the bank account is used for school fees, and the distribution resolution is signed after 30 June. On paper, they have a trust. In practice, they have handed their accountant and lawyer a clean-up job.

That is how trust problems usually start in WA. Not with fraud or aggressive tax planning, but with rushed setup, borrowed documents, and administration that never matches the deed.

A practical setup checklist

Set the trust up for the job it needs to do.

-

Define the purpose before the deed is drafted

A trust for a Dunsborough holiday home, a Perth share portfolio, and a family business in the resources supply chain may need different powers and control settings. If the objective is unclear, the deed often ends up too generic. -

Choose the trustee with succession in mind

Individual trustees can look cheaper at the start. A corporate trustee usually gives cleaner separation, simpler control changes, and fewer problems when someone dies, loses capacity, or exits the business. For many established WA families, that extra setup cost is money well spent. -

Get the deed drafted for current law and your family group

The deed governs who can benefit, who controls the trust, how income is appointed, and what happens if relationships change. A basic online deed can miss practical points such as streaming powers, backup appointors, and succession mechanics. -

Confirm the appointor and control chain

I see this missed often. Clients focus on beneficiaries because that is where the money goes. Control usually sits elsewhere. If the wrong person holds appointor power, the family can face a serious dispute at exactly the wrong time. -

Open separate accounts and register properly

The trust needs its own TFN, and often its own ABN if it carries on an enterprise. It also needs a dedicated bank account. If trust income and personal spending run through the same account, record-keeping becomes unreliable fast. -

Transfer assets correctly

A trust only holds assets that are legally transferred to it. That means checking stamp duty, CGT, loan terms, and ownership records before anything moves. In WA property matters, this step deserves care because a bad transfer can trigger tax or duty costs that were avoidable with proper advice. -

Set an annual compliance process before year end

Do not leave trust resolutions until the last week of June. Accountants need time to review income, trust law issues, unpaid present entitlements, and beneficiary positions. Families with business income that swings from year to year need this discipline even more.

Common pitfalls that create expensive problems

Some mistakes stay hidden until a divorce, creditor claim, family fallout, or ATO review.

-

Old deeds that no longer support the strategy

A deed signed years ago may not allow the distribution approach the family now wants to use. It may also be silent on newer drafting issues that advisers now treat as standard. -

Late, vague, or invalid distribution resolutions

This is one of the most common trust failures. If the resolution is not made on time and in the form the deed requires, the intended tax outcome can unravel. -

Using trust money like a personal wallet

Paying private expenses from the trust account without proper recording is a red flag. It weakens the discipline that gives the structure value in the first place. -

Ignoring the ATO’s current trust focus areas

The ATO has increased scrutiny on trust distributions, especially where income is appointed to one person but another person enjoys the economic benefit, or where arrangements appear to exist mainly for tax reduction. Tax advisers should be reviewing trust arrangements against the ATO’s trust guidance, including section 100A reimbursement agreement concerns and Division 7A issues where companies are involved. -

Assuming the accountant can fix legal defects after year end

Accountants can often help with tax reporting. They cannot rewrite history if the trustee lacked power under the deed, the asset transfer was defective, or the control structure was wrong from the start.

What careful families do better

The families who use trusts well are rarely flashy about it. They document decisions, keep control roles current, review the deed after major life events, and treat 30 June as a deadline that matters.

For WA business owners, especially those dealing with contract income, lumpy profits, or asset exposure tied to mining and services work, that discipline matters more than the trust itself. A good structure badly run creates false comfort. A well-run trust can protect flexibility for years.

Practical takeaway: A family trust is precise legal machinery. Set it up carefully, keep the records clean, and review it before problems force the issue.

Is a Family Trust Right for Your Financial Plan?

A family trust can be one of the smartest structures available to an Australian family. It can improve tax flexibility, strengthen asset protection, and support cleaner intergenerational planning. For the right client, those benefits are substantial.

It is also a structure that demands respect.

A trust works well when the family has growing investments, uneven incomes, business risk, or clear legacy goals. It works less well when there is no real strategy behind it, no discipline around administration, or no willingness to maintain it properly year after year.

If you are a business owner in WA, a high-income professional building non-super assets, or a family thinking about how wealth should be protected and passed on, the question is worth asking early. Good trust planning is proactive. It is rarely at its best when done in a rush after a problem has already appeared.

The best next step is not to download a deed and hope for the best. It is to test whether a trust fits your broader financial plan, your tax position, your family dynamics, and your succession intentions.

That is the difference between owning a trust and using one well.

If you want clear advice on whether a family trust belongs in your strategy, speak with Wealth Collective. Their Perth and Dunsborough team helps Australians build, protect, and transfer wealth with practical guidance across tax-aware structuring, retirement planning, and family wealth strategy. A free 10-minute introductory call is a simple way to test whether a trust fits your situation before you commit to the wrong structure.