Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You’ve probably had this thought already.

Your super balance has grown, your income is solid, and the standard fund options are starting to feel restrictive. Maybe you want more control. Maybe you want to hold different assets. Maybe you’re tired of feeling disconnected from one of the biggest pools of money you’ll ever own.

That’s usually where the question starts: should I set up my own super fund?

It’s a fair question. Self-managed super funds can be powerful, but they are not a shortcut and they are not a hobby. If you want to learn how to start a self managed super fund, you need to think like a trustee before you think like an investor. Control is the attraction. Responsibility is the trade-off.

The SMSF Question Are You Ready to Be Your Own Super Fund Manager

An SMSF suits people who want active control and are prepared to carry legal responsibility for that control.

That second part matters more than many individuals realise.

A lot of Australians are clearly attracted to the structure. As of June 2025, Australia had 653,062 SMSFs, with over 1.2 million members and $1.05 trillion in assets, representing 24% of the $4.33 trillion super market, according to SuperGuide’s SMSF statistics. This is not a fringe strategy. It is a major part of the retirement system.

But popularity is not a reason to start one.

What people usually want from an SMSF

Many individuals who ask about an SMSF want one or more of these:

- More control over investments rather than choosing from a menu inside a retail or industry fund

- Better alignment with family goals when a couple wants to manage super together

- A clearer retirement strategy instead of leaving super on autopilot

- Flexibility around how the fund is structured and managed over time

Those are good reasons. “My friend has one” is not.

What you are really signing up for

The moment you become a trustee, the job changes. You are no longer just a member of a super fund. You are responsible for running one.

That means making decisions, keeping records, maintaining compliance, arranging annual audits, and making sure every action stays inside super law. If you want a simple overview first, this guide on what is a SMSF is a useful starting point.

My view: if you want control but not responsibility, don’t start an SMSF.

That is the line many need to hear early.

The honest readiness test

Before you go any further, ask yourself three blunt questions:

- Do I want to manage this structure, not just own it?

- Am I comfortable being accountable for compliance?

- Do I have a clear reason for needing an SMSF, beyond curiosity?

If the answer to any of those is no, stop there.

An SMSF works best when it sits inside a broader financial plan. That means your cash flow, debt position, insurance, tax position, retirement timing and investment strategy all need to line up. Starting the fund first and hoping clarity arrives later is the wrong order.

A Realistic Look at SMSF Viability Costs and Responsibilities

The biggest mistake people make is asking how to start an SMSF before asking whether it should exist at all.

That question comes down to two things. Scale and discipline.

The balance threshold is not optional in practice

The commonly recommended minimum threshold for cost-effectiveness is $200,000, and 87% of SMSFs exceed that level, according to SuperGuide’s SMSF statistics. That matters because SMSF costs are not purely percentage-based. A lot of them are fixed.

If your balance is too low, those fixed costs take a bigger bite.

There is also a broader industry view that SMSFs become cost-effective from around $250,000 or more, but even that is debated, and the more useful question is the one most guides avoid: what are the actual setup and ongoing costs, and do they justify the complexity for your situation?

Setup costs are only the beginning

The setup benchmark often cited for establishing an SMSF is $1,500 to $5,000 upfront, with viability usually discussed for balances above $200,000 to $500,000, according to Guided Investor’s SMSF establishment guide.

That upfront figure is only the entry ticket.

You still need to account for the ongoing work involved in:

- administration

- accounting

- independent audit

- tax reporting

- investment records

- insurance review

- trustee minutes and documentation

Some people can handle parts of that process themselves. Many should not.

SMSF Costs vs. APRA-Regulated Funds A Realistic Comparison

| Fee Type | Typical SMSF Cost (Annual) | Typical Industry/Retail Fund Cost (Annual) |

|---|---|---|

| Establishment | Upfront setup benchmark of $1,500 to $5,000 | Usually not a separate establishment cost |

| Administration and compliance | Often fixed annual administration costs. Guides commonly note a percentage range for annual admin fees as a benchmark when outsourced | Usually bundled into percentage-based fund fees |

| Audit | Separate annual audit required | Included within overall fund structure |

| Accounting and tax return | Separate cost | Usually bundled into fund fees |

| Investment management | Self-directed or adviser-supported cost | Included in fund options and fee structure |

| Insurance | Separate policy decisions and premium costs if held | Often easier to keep default cover in place |

The key difference is not just cost. It is cost structure.

An industry or retail fund generally wraps administration into a percentage fee. An SMSF often brings more visible line items and more direct responsibility. For higher balances, that can work well. For lower balances, it often does not.

Practical rule: if your balance is near the minimum and your main reason is “lower fees”, you probably do not have a strong enough case yet.

Viability is about time as much as money

People often focus on the investment freedom and ignore the workload.

An SMSF asks you to be organised. You need to keep records clean, make decisions properly, document them, and stay alert to super rules. If that sounds annoying, that feeling is useful. It means you are assessing the structure realistically.

A simple self-qualification test

You are more likely to be a good SMSF candidate if most of these are true:

- Your balance is already at a sensible level rather than still building from a low base

- You want a specific strategy that your current fund does not handle well

- You are willing to review the fund regularly instead of treating it as a one-off setup task

- You value structure and documentation rather than avoiding admin

- You understand that trustee duties sit with you, even when professionals help

If you need a broader decision framework first, this look at self-managed super fund pros and cons can help sharpen the decision.

My recommendation

Do not start an SMSF because it sounds complex.

Start one only if the fund will be large enough, the strategy is clear enough, and the members are committed enough to justify the extra complexity. The right SMSF can be efficient and flexible. The wrong SMSF is just an expensive admin project with legal consequences.

Laying the Groundwork Your Trustee Structure and Trust Deed

The first big decision is structural. Get this wrong and you build unnecessary friction into the fund from day one.

Choose the trustee structure carefully

When establishing an SMSF, you must choose between individual trustees and a corporate trustee, and a corporate structure is often preferred for flexibility in member changes and succession planning, while also avoiding the issue that a single-member individual fund requires a non-member co-trustee, as outlined in Guided Investor’s SMSF setup guide.

Here is the plain-English version.

Individual trustees

With individual trustees, each member is a trustee personally.

This can work, but it is usually clunkier when life changes. If a member joins, leaves, dies, or loses capacity, the paperwork tends to become more awkward because legal ownership details often need to be updated across assets and documents.

Corporate trustee

With a corporate trustee, a company acts as trustee, and the fund members are directors of that company.

For most couples, families and business owners, this is the cleaner structure. It tends to make succession, administration and membership changes easier to manage.

My recommendation: if you are serious about running an SMSF for the long term, lean toward a corporate trustee unless there is a strong reason not to.

Think beyond setup day

A lot of people choose a structure based only on today.

That is lazy thinking.

Your SMSF needs to survive real-life events such as retirement, illness, death, separation, adding a member, or removing one. Corporate trustees usually handle those transitions more smoothly. That is why they are often the better fit for people building long-term family wealth.

Your trust deed is not a template exercise

The trust deed is the fund’s rulebook. If the trustee structure is the skeleton, the deed is the operating manual.

It sets out how the fund can run, what powers trustees have, how members are dealt with, and whether the fund has the flexibility for certain strategies. If you expect to explore more complex options later, the deed needs to support that.

What the deed should cover

A properly prepared trust deed should address matters such as:

- Fund identity and purpose so the structure is clearly defined

- Trustee powers including how decisions are made

- Member rules for adding or removing members

- Investment powers so the fund can operate as intended

- Special provisions if you may eventually consider borrowing or property strategies

Off-the-shelf deeds can miss important details. Cheap documents often become expensive problems later.

The practical standard to use

Ask one question before signing anything.

Does this structure still make sense if our circumstances change?

If the answer is uncertain, do not guess. Fix it before you proceed.

An SMSF should be built to last. That means the legal framework needs to be deliberate, not improvised.

Making It Official ATO Registration and Opening Accounts

Once the legal foundation is in place, the fund needs to be recognised and operational.

At this point, many people assume the hard part is over. It isn’t. This is the stage where sloppy admin creates avoidable compliance problems.

As of June 2025, Australia had 653,062 SMSFs holding $1.05 trillion in assets, and to initiate one you must register with the ATO to obtain an ABN and TFN, open a dedicated bank account, meet residency requirements, and accept that trustees bear full legal responsibility for compliance, according to SuperGuide’s SMSF statistics and setup overview.

Register with the ATO promptly

After executing the trust deed, the fund needs to be registered with the ATO.

The establishment guidance in the verified data states you should apply for the ABN and TFN within a specific timeframe after execution. That deadline matters. Early delays can create unnecessary trouble before the fund has even started investing.

Get the residency settings right

An SMSF must satisfy Australian residency requirements.

That includes central management and control being in Australia and the fund being run in a way that remains compliant with residency rules. This is one area where people can trip up when work, travel or family arrangements shift across borders.

If your circumstances are straightforward, the process is manageable. If they are not, get advice before you register.

Open a dedicated bank account

Your SMSF needs its own bank account in the trustee name as trustee for the fund.

That account is not optional. It is the core transaction account for contributions, rollovers, expenses, investment activity and record-keeping. Mixing personal money with fund money is one of the fastest ways to create audit headaches.

The bank account should be used for

- Incoming contributions from employers or members

- Rollovers from existing super funds

- Investment transactions in the name of the fund

- Fund expenses such as audit and administration costs

Clean separation is one of the simplest ways to keep the fund defensible.

Set up an ESA as well

The SMSF also needs an Electronic Service Address, or ESA.

This allows the fund to receive employer contributions and rollovers through the SuperStream system. It sounds technical, but in practice it is just part of making the fund capable of receiving money properly.

Tip: do not tell your employer to start paying into the SMSF until the fund is fully registered, the bank account is open, and the ESA is ready.

Keep the process orderly

A practical checklist helps:

- sign the deed

- register the fund with the ATO

- obtain the ABN and TFN

- open the SMSF bank account

- arrange the ESA

- only then start the rollover and contribution process

This stage is admin-heavy, not intellectually difficult. People still get it wrong because they rush. Slow down and do it in order.

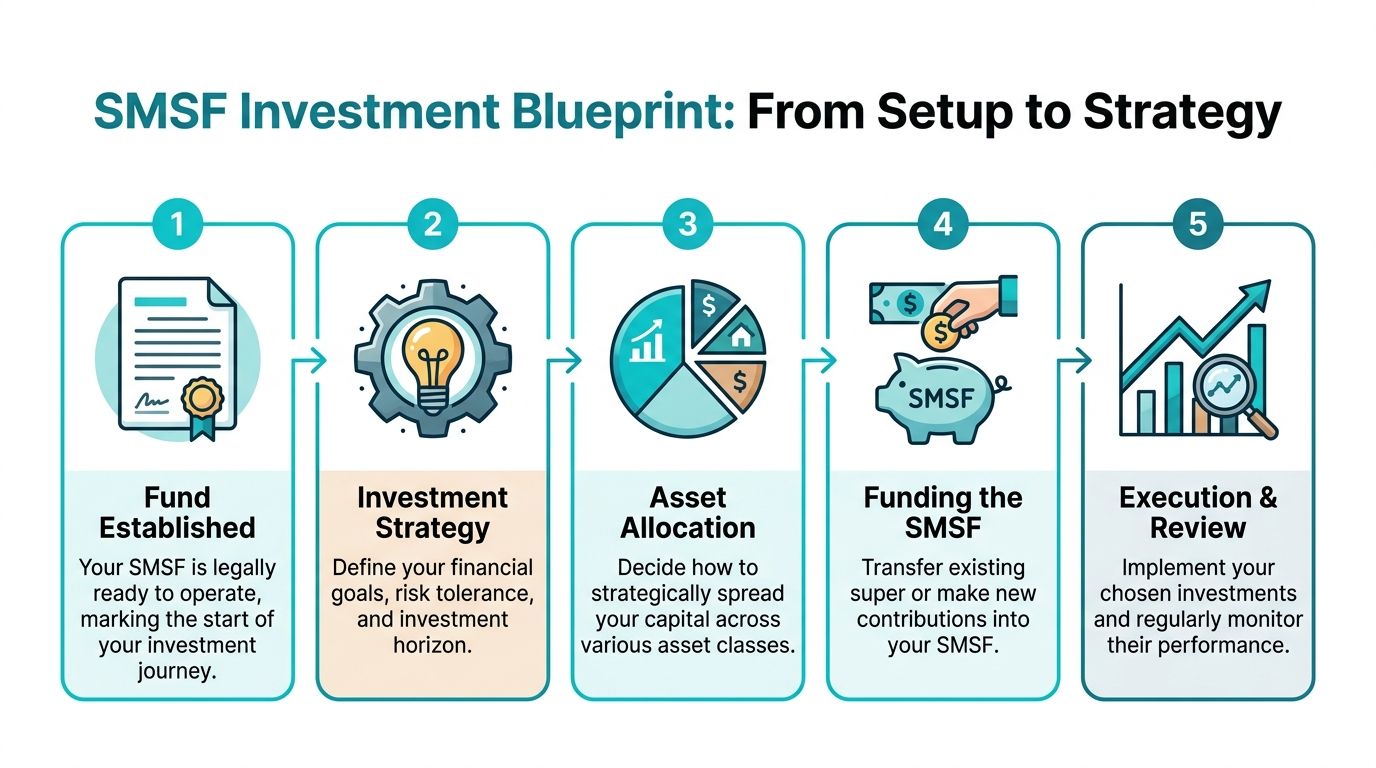

Creating Your Investment Blueprint and Funding Your SMSF

At this point, the fund starts to justify its existence.

An SMSF is not there to give you a fancy structure. It is there to support retirement outcomes. That only happens when the investment plan is written clearly and followed properly.

A compliant investment strategy must be documented, covering retirement goals, asset allocation, liquidity, risk tolerance and insurance holdings, and trustees remain solely accountable for it. The sole purpose test also applies, meaning decisions must be for retirement benefit, as set out by the ATO’s SMSF setup guidance.

Your strategy must exist before real investing begins

A proper investment strategy is not a vague note saying “buy growth assets” or “invest for retirement”.

It needs to connect member circumstances with decision-making. For a couple with different retirement timeframes, that means balancing growth, liquidity and risk in a way both members can justify. For a pre-retiree, it usually means being more explicit about cash flow needs, time horizon and downside tolerance.

The strategy should deal with

- Goals and what the fund is trying to achieve over time

- Risk and how much volatility the members can realistically tolerate

- Liquidity so the fund can pay expenses and future benefits when required

- Diversification rather than overloading one idea or asset type

- Insurance and whether the fund should hold cover for members

The sole purpose test is where people get careless

Trustees often focus on what they can buy and ignore why they are buying it.

That is dangerous.

Every investment decision needs to be defensible as a retirement decision. If the motivation is personal convenience, private use, helping a relative, or blurring personal and fund interests, you are stepping into the wrong territory.

Practical test: if you would struggle to explain an investment choice to an auditor in one clear paragraph, revisit it before proceeding.

Funding the SMSF properly

Once the structure and strategy are ready, the fund needs money.

That usually happens in two ways:

- rolling over existing super balances from other funds

- directing future employer contributions into the SMSF

Both sound simple. Both need care.

Rollovers

Rolling over existing super into the SMSF is common, but the move should not happen on autopilot. Review what sits inside the old fund first, especially any insurance attached to it.

The setup guidance in the verified data specifically warns that trustees can lose existing cover during rollover, including life, TPD and income protection arrangements. If the insurance matters, deal with that before transferring everything out.

Employer contributions

If you want your employer to pay into the SMSF, give them the correct fund details only after the fund is fully operational. That includes the ABN, bank account and ESA.

Property should be strategy-led, not trend-led

A lot of SMSF enquiries eventually lead to property.

That can be valid, but only when the asset fits the fund’s written strategy, liquidity needs and member goals. Too many people start with the property idea and try to reverse-engineer the strategy afterwards. That is backwards. If this is on your radar, this guide on whether it is worth buying property with super is a useful next read.

My recommendation

Write the strategy like you will have to defend it in writing every year.

Because you might.

If the strategy is thoughtful, practical and aligned with member needs, the fund has a solid backbone. If it is generic, copied, or disconnected from how you will invest, the SMSF is already weaker than it looks.

Your Ongoing Duties Avoiding Common and Costly Pitfalls

A lot of trustees treat setup as the main event.

It isn’t.

Running the fund well, year after year, is the primary job. The people who struggle with SMSFs are rarely defeated by the initial paperwork. They are defeated by maintenance, disagreement, poor records and casual rule breaches.

Annual compliance is not optional

An SMSF needs ongoing administration and oversight.

That includes maintaining records, preparing annual financial information, arranging an independent audit and lodging the required annual return. Trustees can outsource tasks, but they cannot outsource responsibility.

If that distinction bothers you, pay attention to it. It is one of the defining realities of the structure.

The human side is where many funds crack

Existing guides often focus on structure and legal setup but ignore the practical human element. Members may have different risk tolerances, retirement timelines or views on investment direction, and that is a real source of disputes and compliance issues, as noted in Green Associates’ discussion of setting up and winding down an SMSF.

This is especially relevant for:

- Couples with different retirement horizons

- Business partners with different attitudes to risk

- Families where one member is engaged and the other is passive

An SMSF with multiple members needs governance, not just goodwill.

Build decision rules early

Do not rely on “we’ll work it out when it comes up”.

That is how trustee disputes turn messy.

Put these governance habits in place

- Document decisions clearly so there is a record of why the fund acted

- Agree on an investment process before markets become volatile

- Review member goals regularly because retirement timing and income needs change

- Set boundaries around contributions, withdrawals and strategy changes so surprises do not derail the fund

Tip: if one member is driving every decision and the others are just signing forms, the governance model is already weak.

Common breaches are usually boring, not dramatic

Most SMSF problems do not begin with some elaborate scheme.

They start with ordinary sloppiness. Poor documentation. Unclear valuations. Payments made from the wrong account. Decisions that are never recorded. Assets that do not match the written strategy. Loans or financial help that drift too close to related parties.

Those mistakes are avoidable, but only if trustees stay disciplined.

Insurance and succession should stay on the agenda

Trustees often focus heavily on investments and neglect protection.

That is short sighted.

An SMSF should also account for what happens if a member dies, loses capacity, retires earlier than expected, or wants to exit the fund. Clean succession planning and regular insurance review are part of responsible fund management, not side issues.

The set-and-forget mindset is the wrong mindset

If you want a hands-off experience, an SMSF is probably the wrong vehicle.

The fund needs active stewardship. Not frantic trading. Not constant changes. Just consistent oversight, proper records, and decisions that can be explained and defended.

That is what keeps the structure useful instead of stressful.

Your Path to SMSF Success with Wealth Collective

A good SMSF is built on clarity.

Not excitement. Not trends. Not the idea that more control automatically means better outcomes.

If you want to know how to start a self managed super fund the right way, the decision checklist is simple.

The decision checklist

You are in a stronger position to proceed if you can answer yes to most of these:

- I have a clear reason for wanting an SMSF, beyond curiosity or hype

- My super balance is large enough to justify fixed costs

- I am comfortable taking trustee responsibility seriously

- I am willing to keep records and review the fund regularly

- All members are aligned on goals, risk and decision-making

- I understand that setup is only the beginning

- I am prepared to get professional help where the fund needs it

If several of those answers are no, pause.

That does not mean an SMSF is permanently off the table. It may mean the timing is wrong, the balance is not there yet, or the strategy is not defined enough.

My direct view

An SMSF is a strong structure for the right household.

It can suit pre-retirees who want more oversight. It can suit couples who want to coordinate retirement planning. It can suit business owners who need a more customized approach to super. But it only works well when the members are organised, engaged and realistic about the workload.

If you are still unsure, that is normal. Many individuals should not make this decision from a blog post alone.

There is a practical difference between understanding the rules and knowing how those rules apply to your own super balance, tax position, insurance setup, retirement timeline and family circumstances. That is where advice becomes useful.

One option is to use a structured advice process that can assess SMSF suitability, model the implications, and help with setup, rollover and ongoing compliance support where appropriate. Wealth Collective provides that kind of planning through its broader superannuation and retirement advice process.

The goal is not to push everyone into an SMSF.

The goal is to help you decide properly.

If you want clarity on whether an SMSF fits your situation, book a free introductory call with Wealth Collective. It’s a simple conversation to work out whether this structure makes sense for your balance, goals and lifestyle, and what the next step should be if it does.