Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Many individuals don’t feel poor on paper. They feel squeezed in real life.

It’s the Perth couple with good salaries who still wonder why the account balance never stays high for long. It’s the Dunsborough professional in their 50s who has built plenty, owns assets, and still isn’t sure whether retirement is properly funded. It’s the business owner who has poured years into growth but knows one bad event could undo a lot of work.

That tension usually comes from one problem. Money decisions are happening in isolation. The mortgage sits in one corner. Super sits in another. Insurance gets reviewed only when premiums arrive. Investments get treated as a separate project. A proper wealth creation strategy ties those parts together so each decision supports the next one.

From Financial Stress to Strategic Success

A familiar WA story goes like this. Two incomes are coming in, school fees or childcare are being managed, the mortgage has become heavier, and every month feels busy enough that long-term planning keeps slipping. They’re not reckless. They’re just reacting.

Another version shows up later in life. A senior employee or small business owner has done well, built equity, added to super here and there, maybe bought an investment property, maybe not. But there’s still a persistent question. Are we organised, or have we just been making decent money?

That distinction matters.

Financial progress usually doesn’t stall because people are lazy. It stalls because they’re carrying too many moving parts without a single framework. When cash flow gets tight, good habits disappear first. Extra super stops. Investments pause. Debt reduction becomes inconsistent. Protection gets ignored because it doesn’t feel urgent.

That’s where clarity starts paying for itself. A working strategy gives every dollar a job. Some dollars reduce stress now. Some build tax-effective wealth. Some protect the whole structure if life turns sideways. Good planning is less about complexity and more about order.

For many households, the first improvement isn’t a new product. It’s control over cash flow and decision-making. A disciplined approach to cash flow management often reveals what’s possible without changing your lifestyle as much as you’d expect.

Financial confidence rarely arrives because income rises. It arrives when decisions stop competing with each other.

The shift from stress to momentum happens when you stop asking, “What should I do with this spare money?” and start asking, “What role should this money play in the plan?”

The Three Pillars of Your Financial Future

A solid wealth creation strategy works like a well-built home. If one part is weak, the rest becomes harder to trust.

Earn and save as the foundation

You can’t build from ambition alone. The foundation is surplus cash flow.

That doesn’t mean hoarding cash forever. It means creating enough breathing room each month to direct money with purpose. A household with strong income and weak surplus often feels richer than it is. A household with moderate income and disciplined surplus usually builds faster.

The foundation comes from:

- Knowing your true fixed costs so the mortgage, rent, utilities, education, and recurring lifestyle expenses are visible.

- Separating short-term buffers from long-term investing so emergency money doesn’t end up trapped in growth assets.

- Automating good behaviour because manual discipline fades when work, family, and life get busy.

Individuals often want the exciting part first. They ask about shares, property, or tax structures before they’ve made room in the monthly cash flow. That’s backwards. If the base is unstable, every market wobble feels bigger and every strategy gets abandoned too early.

Grow with intention through investing

Growth is the structure of the house. Wealth starts compounding here rather than just accumulating.

Investing can happen through super, direct property, managed funds, exchange-traded funds, business assets, or a mix. The right choice depends on your timeframe, tax position, debt load, and tolerance for volatility. There isn’t one perfect vehicle. There is only a better fit for your situation.

A useful test is simple. Ask whether your current investments are doing a specific job.

| Decision area | Useful question |

|---|---|

| Timeframe | Is this money needed soon, or can it stay invested for years? |

| Tax | Is the asset held in the most sensible tax environment? |

| Liquidity | Can I access funds if priorities change? |

| Diversification | Am I relying too heavily on one asset or one outcome? |

Growth matters because saving alone usually won’t do all the heavy lifting. But growth without discipline tends to become speculation.

Protect what you’ve built

Protection is the roof. People don’t value the roof much on sunny days.

Insurance and risk management are often treated as optional because they don’t feel productive. But one illness, one accident, one extended interruption to income can force the sale of good assets at the wrong time. That’s how strong balance sheets start leaking.

A practical strategy includes reviewing:

- Personal cover such as income protection, life, trauma, and total and permanent disability where appropriate.

- Debt exposure so repayments remain manageable if income changes.

- Ownership structures and beneficiaries so wealth transfers cleanly and intentionally.

Practical rule: If a single event could force you to stop contributing, sell assets, or redraw debt just to stay afloat, protection isn’t a side issue. It’s part of the wealth strategy.

The strongest plans don’t just aim for upside. They reduce the chance that one bad year wipes out a decade of good decisions.

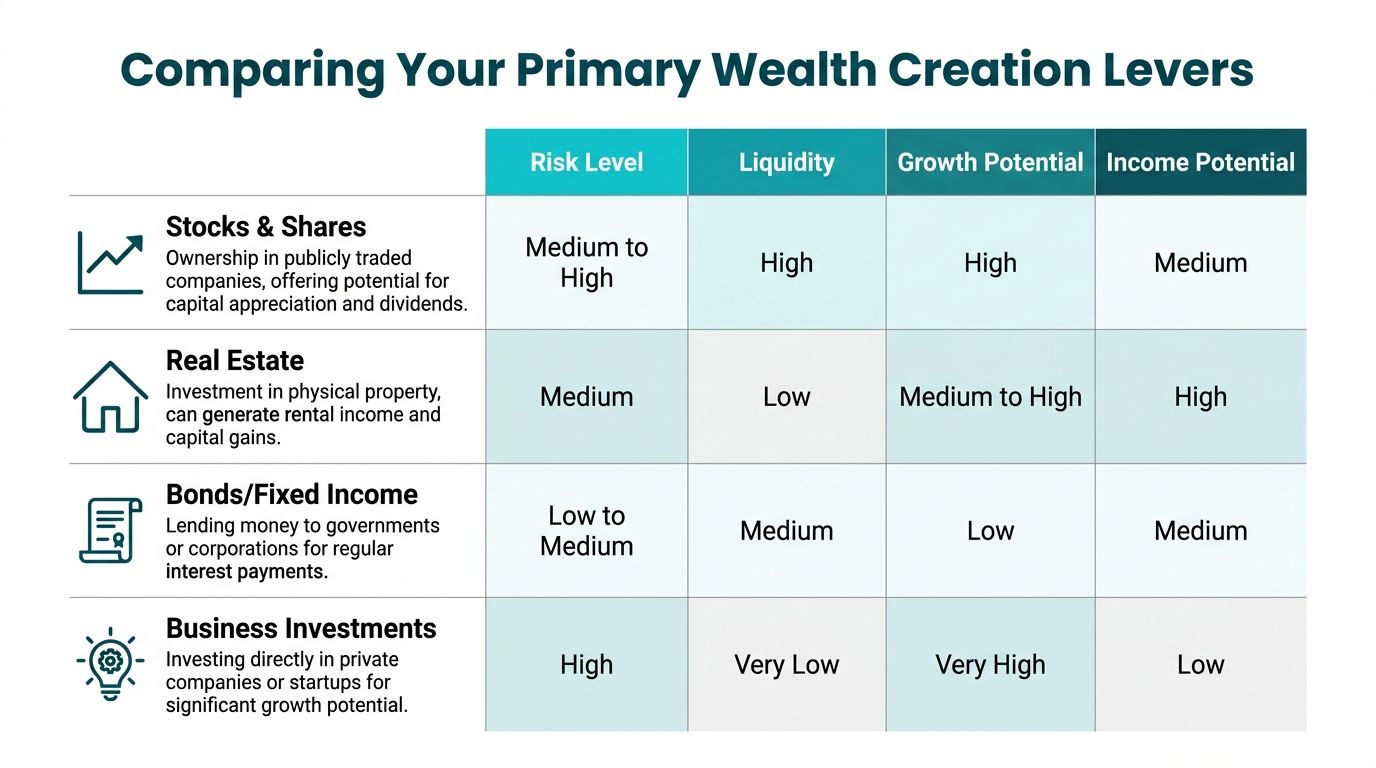

Comparing Your Primary Wealth Creation Levers

Many individuals don’t need more options. They need a clearer way to judge the options already in front of them.

Shares and managed investments

Listed investments offer one thing many Australians underestimate. Flexibility.

You can build diversified exposure, add regularly, reinvest income, and adjust over time without needing a bank, a tenant, or a renovation budget. Liquidity is the major strength. That matters when life changes quickly.

The trade-off is behavioural. Because prices move daily, people are tempted to react daily. Good listed investment strategies usually reward patience, not constant intervention.

Shares and managed investments tend to suit people who want:

- High liquidity for flexibility

- Broad diversification across sectors and markets

- Regular investing from salary or surplus cash flow

- Lower administrative load than direct property or private business interests

They don’t suit people who panic when markets move or who chase trends instead of following an allocation.

Direct property in WA

Property remains attractive in WA for good reason. It’s tangible, familiar, and can work well when matched to the right balance sheet and borrowing capacity. In local conditions, the appeal has been reinforced by price growth. Perth’s median house price growth reached 8.2% in 2025, ahead of the national 5.7%, according to the REIWA Perth market snapshot.

Tax settings add to that appeal. Negative gearing can allow rental losses to offset other taxable income, and the capital gains tax discount can improve the after-tax outcome when an asset is held long enough and sold under the right circumstances.

That said, property isn’t automatically superior. It’s concentrated, illiquid, and expensive to transact. It can also create false confidence because financial gearing amplifies outcomes in both directions. A strong property decision depends on cash flow resilience, debt discipline, and a willingness to hold through cycles.

Consider this practical comparison:

| Lever | Strength | Weakness | Best fit |

|---|---|---|---|

| Shares and funds | Liquidity and diversification | Visible volatility | Long-term disciplined investors |

| Direct property | Financial gearing and tangible asset exposure | Concentration and low liquidity | Households with strong borrowing capacity |

| Debt reduction | Guaranteed improvement to cash flow | Lower long-term growth than growth assets in some cases | Risk-aware households under repayment pressure |

One strategy many households explore alongside property is debt recycling, which can help restructure debt more efficiently when implemented carefully.

Aggressive debt reduction

This lever gets underestimated because it’s not glamorous.

Paying down bad debt or reducing non-deductible home loan debt can produce a result that feels slow at first and powerful later. It improves cash flow, lowers risk, and gives you more room to invest with confidence. For households under pressure from repayments, this can be the right first move even if investing looks more exciting on paper.

Debt reduction tends to be strongest when:

- Interest costs are restricting cash flow

- You want certainty rather than market volatility

- You’re preparing for a major transition, such as one income dropping away or retirement approaching

What doesn’t work is treating debt reduction as an all-or-nothing ideology. Some people throw every spare dollar at the mortgage for years, then realise they’ve neglected super, diversification, and tax efficiency. Others invest aggressively while carrying debt that is causing stress every month. Balance matters.

Business investment and reinvestment

For business owners, the highest-returning asset is often the business itself. That can be true. It can also become a blind spot.

Reinvesting in operations, staff, systems, or expansion may create substantial value, but it also ties personal wealth to one economic engine. If business conditions weaken, both income and asset value can come under pressure at once.

That’s why owner-led wealth creation usually works best when business reinvestment is paired with assets outside the business. Otherwise, a person can look wealthy for years and still be highly exposed.

The best wealth creation strategy isn’t the lever with the highest upside. It’s the mix you can hold through pressure, not just in good conditions.

The right answer is rarely “all in on one thing”. It’s usually a coordinated blend of property, market exposure, super, debt management, and protection, adjusted to the stage of life you’re in.

Turn Your Superannuation into a Wealth Engine

Super is often treated as a boring account in the background. That’s a mistake.

For high-income earners and pre-retirees in particular, super can be one of the most effective parts of a wealth creation strategy because of the tax environment around contributions and long-term compounding.

Why salary sacrifice matters

Superannuation optimisation through salary sacrifice remains one of the clearest tax levers available. Concessional contributions are generally taxed at 15% instead of marginal tax rates up to 45%, and for the 2024-25 financial year the concessional cap is $30,000, as set out by the ATO super contributions caps guidance.

That gap matters because the money you don’t lose to tax stays invested. Over time, that can change the outcome significantly.

The same ATO guidance notes a projection where a 40-year-old WA executive consistently maximising concessional contributions could accumulate an extra $1.2 million by age 65. That’s not because super is magical. It’s because tax efficiency plus consistency is powerful.

A helpful primer on the mechanics sits in this guide to salary sacrifice super.

The practical moves that make super work harder

Many individuals don’t need a complicated super plan. They need a deliberate one.

Focus on the practical levers:

- Salary sacrifice regularly rather than waiting for a late-year scramble.

- Check your concessional cap position so employer contributions and personal deductible contributions are counted properly.

- Use carry-forward rules where eligible if you’ve left concessional cap space unused in prior years and your balance allows it.

- Review investment mix inside super because contribution strategy and portfolio strategy need to work together.

- Consider spouse contribution strategies where the household, not just the individual, is the planning unit.

A common error is over-funding super too early when cash flow is tight outside the fund. Another is under-using it for years because retirement feels distant. The right level depends on age, debt, liquidity needs, and tax position.

Where people get super wrong

The biggest mistake isn’t usually choosing the wrong fund. It’s treating super as disconnected from the rest of the plan.

If your mortgage is causing strain, if your cash buffer is weak, or if major expenses are looming, then pushing too hard into super can create pressure outside the fund. On the other hand, if you’re earning well and parking surplus cash in low-purpose accounts, ignoring super can mean missing one of the most efficient long-term levers available.

Good super strategy isn’t about maxing contributions at any cost. It’s about using the super environment when it improves the whole plan.

For pre-retirees, the stakes are even higher. The years leading into retirement are often the last window to make large, intentional moves while employment income is still strong. That’s when contribution strategy, investment allocation, retirement timing, and income planning need to line up.

Building Your Personalised Wealth Roadmap

A proper roadmap should feel personal because it is. Two households can earn similar money and need very different decisions.

The Perth young family or professional household

This group often looks fine from the outside. Good incomes. Good prospects. Plenty of effort. But the pressure points are obvious. Mortgage repayments, childcare, rising living costs, and the constant feeling that every spare dollar already has a destination.

The roadmap here usually starts with sequencing.

First, stabilise cash flow. Then decide how much surplus should reduce non-deductible debt, how much should build super, and how much should go into flexible long-term investments. Trying to do everything at full speed often leads to inconsistency in all of them.

For this household, a practical roadmap often includes:

- Clean up cash flow first so there’s a visible monthly surplus.

- Protect the downside with appropriate personal cover and a cash buffer.

- Split surplus strategically between mortgage reduction and long-term wealth building.

- Use tax-effective opportunities carefully rather than chasing every available strategy at once.

The trap here is copying someone else’s plan. A household with one young child, one variable income, and a large mortgage shouldn’t run the same strategy as two senior earners with stable bonuses and no dependants.

The WA small business owner

Business owners usually tolerate more complexity than employees. They also carry more hidden risk.

Many owners invest heavily back into the business, assume that’s enough, and leave their personal structure underdeveloped. Then a health issue, business interruption, or key person problem exposes how much of the household balance sheet was relying on one operating asset.

Here, protection stops being theoretical. WA small business owners hold 35% less income protection than national averages, and APRA reported a 15% SME failure rate spike in 2025, according to APRA news and publications. In practice, uninsured disruption often leads to avoidable wealth erosion.

A stronger owner roadmap typically combines:

- Risk cover that reflects business dependence, not just personal expenses

- Clear separation between business assets and personal wealth goals

- Tax-aware contributions and investment structures

- A plan to diversify beyond the business over time

For owners, one of the biggest strategic shifts is moving from “the business is my wealth plan” to “the business funds my wealth plan”. Those are not the same thing.

A healthy business can create wealth. It can also create concentration risk if you never move value out of it.

The South West pre-retiree

This household often has a different issue. They’re asset-rich but decision-poor.

There may be equity in the family home, a reasonable super balance, perhaps an investment property, maybe some cash sitting idle because retirement feels close and caution feels safer. They don’t need hype. They need clarity around what to optimise before work stops.

The roadmap usually centres on alignment:

- Retirement timing and spending needs

- Super contribution opportunities while income is still strong

- Portfolio positioning for the next stage, not the last one

- Debt reduction where it improves retirement flexibility

- Estate and beneficiary settings that are current

This is also where many people discover that their assets are fine, but their structure is messy. Accounts are scattered. Risk settings are outdated. There’s no clear drawdown approach. The strategy exists in fragments rather than as a coordinated whole.

What a real roadmap should answer

A useful wealth roadmap doesn’t just list products or investments. It answers the big operational questions.

| Planning question | Why it matters |

|---|---|

| What should happen with the next dollar of surplus? | Stops drift and conflicting decisions |

| Which risks could derail the plan? | Helps prioritise protection and liquidity |

| What belongs inside super and what doesn’t? | Improves tax efficiency and access |

| How much debt is helpful versus harmful? | Keeps financial gearing from becoming stress |

| What changes when work income slows or stops? | Prepares the household for transitions |

Good advice turns those questions into a roadmap you can follow. Not a generic checklist. Not a stack of products. A sequence.

What usually works is simple enough to repeat. It reflects the household’s stage of life, local realities, tax position, and risk tolerance. What usually fails is complexity for its own sake. Too many moving parts. Too little follow-through. No coordination between debt, super, investing, and protection.

Key Metrics and Common Mistakes to Avoid

People often track the wrong things. They watch their bank balance, glance at market headlines, and judge progress by whether the month felt expensive.

A better wealth creation strategy uses a smaller set of metrics, reviewed consistently.

Metrics worth paying attention to

Start with what changes outcomes:

- Net worth trend because wealth is built across assets and liabilities, not just cash in the offset.

- Monthly surplus because strategy needs funding.

- Debt mix because deductible and non-deductible debt play very different roles.

- Super contributions and investment progress because these are easy to neglect when life gets busy.

- Protection gaps because risk doesn’t announce itself in advance.

For younger households, integration matters more than intensity. ABS data from 2025 shows 28% of Perth dual-income families face mortgage stress, and combining super optimisation with debt reduction can save over $15,000 in interest over 5 years, based on the ABS housing costs data. That’s a useful reminder that progress isn’t only about chasing returns. It’s also about reducing friction.

Mistakes that repeatedly derail good plans

Some mistakes are technical. Most are behavioural.

The common ones are:

- Set and forget. A strategy that worked three years ago may not fit your income, family, debt, or retirement timeline now.

- Overcommitting to one asset. Too much property, too much business risk, or too much cash can all become expensive in different ways.

- Ignoring tax location. The same dollar can behave very differently depending on where it is invested.

- Using emotion as a trigger. People buy after confidence rises and pull back after fear rises. That cycle damages outcomes.

- Confusing activity with progress. More accounts, more products, and more complexity do not mean a better plan.

Review your plan when life changes, not only when markets move.

The households that stay on track usually aren’t the ones with perfect discipline. They’re the ones with a framework, a review rhythm, and someone willing to challenge bad decisions before they become expensive.

What works better

Good execution is boring in the right way.

It looks like regular reviews, measured changes, sensible contribution patterns, and decisions that reflect the whole balance sheet. It avoids swinging between extremes. It gives each part of the plan a purpose and checks whether that purpose still holds.

That’s why accountability matters so much. Left alone, individuals often overreact or delay. Neither helps.

Take Your First Step Towards Financial Clarity

Financial stress usually comes from fragmentation. Too many decisions. No clear order. No confidence that the moving parts are working together.

A strong wealth creation strategy fixes that by connecting the essentials. Cash flow supports debt reduction. Debt reduction creates flexibility. Super improves tax efficiency. Investments build long-term growth. Insurance protects the ability to keep going. When those elements are coordinated, progress becomes much easier to see and much easier to sustain.

That’s especially true in WA, where property opportunities, business ownership, rising living costs, and retirement planning all create very local trade-offs. Generic advice rarely handles those trade-offs well because it looks at one issue at a time.

You don’t need to solve everything in one sitting. You do need to stop letting the important decisions compete with each other.

If you’re building wealth, protecting what you’ve built, or preparing for retirement, the most useful next step is clarity. Know where you stand. Know what each dollar should do next. Know which strategies fit your life now, not the life you had five years ago.

If you want that clarity, book a complimentary introductory call with Wealth Collective. It’s a simple way to talk through your situation, identify the biggest gaps or opportunities, and see what a practical plan could look like for your next stage.