Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Rent v buy usually gets framed as a maths problem. It isn’t. It’s a money decision, a lifestyle decision, and for a lot of West Australians, a retirement decision wearing a property hat.

I see the same scene often. Two people sit at the table after dinner, one scrolling listings in Perth, the other looking at the bank balance and asking the uncomfortable question: are we better off buying, or are we just chasing an idea we grew up with?

That uncertainty is fair. Rent keeps rising. Property feels expensive. Interest rates have changed the tone of every conversation. And if you live in WA, the answer isn’t the same as it is in Sydney, Melbourne, or a generic national article written for everyone and no one.

The right way to handle rent v buy is to stop asking, “What is the common approach? ”and start asking, “What gets me the best outcome for my next phase of life?” For some people, that’s buying and getting serious about debt reduction and equity. For others, it’s renting strategically while they build super, keep flexibility, or avoid buying at the wrong stage.

The Rent vs Buy Question in Today’s Australia

A couple in their early 30s rents a decent place close to work. Their lease is up soon. The landlord has flagged another increase. They’ve saved well, but not so well that buying feels easy. One of them wants stability. The other hates the idea of sinking cash into a property and then feeling trapped.

This is the core rent v buy question in today’s Australia. It isn’t about proving one side “wins”. It’s about choosing the option that fits your time horizon, your cash flow, your job security, your family plans, and your tolerance for risk.

If you’re a young professional in Perth, the pressure usually comes from two directions. Rent keeps chewing through income, while purchase prices make the deposit feel painfully slow. If you’re a family, the issue becomes space, school zones, and the desire to stop moving every time a lease changes. If you’re a pre-retiree, the stakes are even higher because the wrong housing decision can distort your retirement timeline.

A good decision starts with three questions:

- How long are you likely to stay put? Buying usually needs time to work in your favour.

- How stable is your income? A mortgage rewards consistency and punishes chaos.

- What’s the bigger goal? Lifestyle freedom, wealth building, debt reduction, or retirement readiness.

Practical rule: If you treat rent v buy as a pure monthly repayment comparison, you’ll make a shallow decision. You need to compare cash flow, flexibility, equity, and long-term wealth together.

That’s a common pitfall. They compare rent to mortgage repayments and stop there. That’s not enough. Buyers need to consider ownership costs and time horizon. Renters need to consider rent inflation and the fact that rent never builds ownership. Both sides need to look at what else their money could be doing.

Rethinking the Great Australian Dream

A Perth couple on good incomes can still feel stuck. They can cover rent, save steadily, and still watch the deposit target drift as prices move, lending rules tighten, and life gets more expensive. That gap between doing well and feeling behind is why the old homeownership script deserves a serious rethink.

Australians were raised to see homeownership as the clear marker of financial success. That idea still carries weight, but WA households deal with a different set of pressures than the glossy version of the dream admits. Our property market has a history of sharper cycles than the east coast. Mining, construction, and small business income can be strong one year and less predictable the next. If you buy at the wrong time, in the wrong suburb, with the wrong loan structure, the cost is real.

Why the old script no longer works

The old model assumed a stable job, a straightforward upgrade path, and steady property gains. Plenty of West Australians do not live that way.

A FIFO worker may earn excellent money but face income volatility. A medical professional may want flexibility before committing to one suburb. A business owner may be better off keeping cash available for the business than pouring every spare dollar into a deposit. A pre-retiree may want security, but still needs to think carefully before tying too much capital into a home that weakens retirement flexibility.

That is the part generic rent v buy advice misses. In WA, the decision is not just about getting into the market. It is about surviving the cycles without damaging your broader financial position.

Loan structure matters here too. Buyers who expect volatile income or changing rates should sort that out before they get emotionally attached to a property. The wrong mortgage setup can turn a manageable purchase into ongoing stress, which is why it helps to understand how fixed and variable home loan rates work before you commit.

Strategic renting is a valid WA wealth strategy

Renting can be the smarter move if it gives you room to build strength elsewhere. I see this most often with clients who are still building career certainty, expect to relocate within a few years, or can get better long-term results by directing surplus cash into super and other investments first.

That matters more in WA than many people realise.

If you are paying rent but also salary sacrificing into super, investing consistently, and keeping your options open until your location and income are stable, you are not falling behind. You are choosing flexibility while building assets in a tax-effective environment. For high earners, concessional super contributions can do more for after-tax wealth than rushing into a property purchase that leaves no room to invest.

Renting becomes a problem when it is passive. Renting with a plan is different.

A strategic renter usually has three clear habits:

- Keeps liquidity high: cash stays available for career moves, family changes, or a better buying opportunity later.

- Uses tax-effective investing: extra cash goes to super, debt reduction, or investments instead of disappearing into lifestyle creep.

- Avoids expensive timing mistakes: they do not buy just to satisfy a cultural milestone.

Buying still makes sense for many households

I still recommend buying for plenty of WA clients. The reasons are practical. Stability matters. Control matters. Owning your home can reduce housing risk later in life, and over time it can become a strong retirement asset because you are not carrying rent into your later years.

But sentiment is not a strategy.

Buy because the property suits your expected time horizon, your cash flow can handle ownership costs, and the purchase does not crowd out every other financial goal. Buy because it fits your retirement plan, your tax position, and the way WA markets behave. If those pieces are missing, waiting is the better call.

The Great Australian Dream is no longer a rule. It is one option. In WA, the smart move is the one that protects your cash flow now and strengthens your position later.

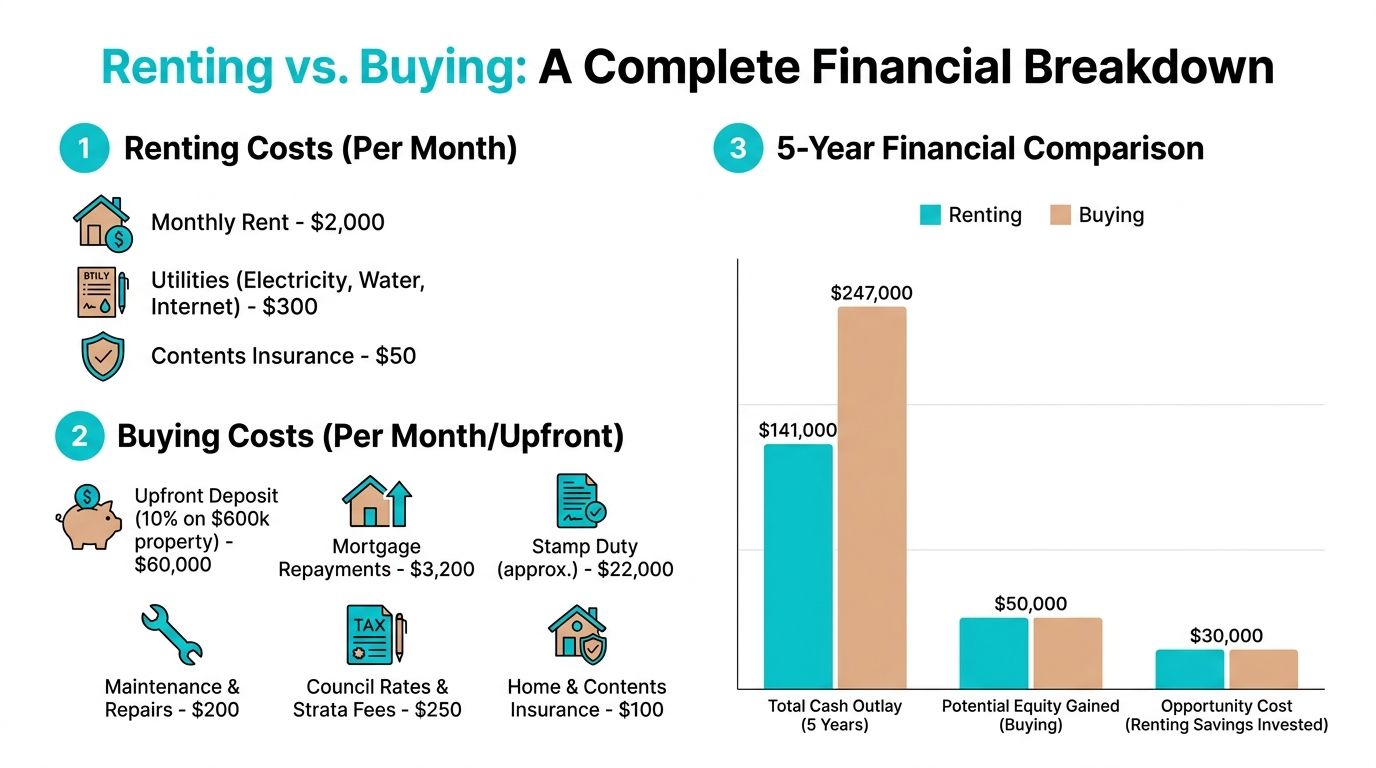

A Complete Financial Breakdown Renting vs Buying

A Perth renter paying $650 a week can feel like they are treading water. A Perth buyer taking on a large mortgage can feel like they are overcommitting. Both reactions are understandable. Both can be wrong if you only compare rent to the monthly loan repayment.

A proper rent versus buy analysis has to include cash tied up in a deposit, purchase costs, tax treatment, ongoing ownership costs, the value of flexibility, and what that money could be doing elsewhere. In WA, that matters more than generic national guides admit because Perth property cycles can move hard and fast, and the wrong timing decision can cost real money.

| Cost Category | Buying (Estimated 5-Year Total) | Renting (Estimated 5-Year Total) |

|---|---|---|

| Housing payments | Ongoing mortgage repayments | Ongoing rent payments |

| Upfront costs | Deposit, purchase costs, setup costs | Bond, moving costs |

| Property running costs | Rates, insurance, maintenance, possible strata | Contents insurance, utilities |

| Flexibility cost | Lower mobility, harder exit | Easier relocation at lease end |

| Wealth effect | Equity build-up if held long enough | No ownership equity from rent |

| Investment opportunity | Capital tied to home | More capital potentially available elsewhere |

What buying really costs

Buying gives you stability and control. It also gives you a stack of costs that are easy to understate.

The mortgage is only one line item. You also have stamp duty, conveyancing, inspections, loan setup costs, council rates, building insurance, maintenance, and possibly strata levies. Then there is the opportunity cost. A deposit locked into a home cannot sit in an offset, build your emergency reserve, or go into super where concessional contributions may deliver a better after-tax result for some WA professionals.

Holding period does the heavy lifting here. The shorter you stay, the harder it is for buying to work financially because transaction costs take a big bite upfront. The longer you stay, the more likely principal repayment and capital growth can outweigh those costs.

Buyers need to price in all of this

- Mortgage interest and principal: principal builds equity, interest is a pure cost

- Purchase friction: stamp duty and buying costs are expensive and unavoidable

- Ongoing ownership costs: rates, insurance, repairs, maintenance, and strata can be material

- Liquidity trade-off: your cash buffer shrinks once the deposit goes in

- Market risk: WA prices can move quickly, but they do not move in a straight line

What renting really costs

Renting is simpler to manage month to month. It is not automatically cheaper over time.

The cost of renting is the combination of ongoing rent, future rent resets, and the fact that your housing payment does not build home equity. Perth renters have felt this sharply because the local market has tightened hard over recent years, and low vacancy puts landlords in a stronger position at renewal time.

That said, renting has one major financial advantage. It preserves flexibility. If your job, family plans, suburb preference, or relationship status could change within a few years, flexibility has genuine value and should be treated as part of the financial equation, not as an emotional side note.

Renters usually miss two things

- Rent rises compound: a manageable lease today can look very different after two renewals

- Unused surplus disappears easily: if the savings from renting are not invested, the strategy fails

Reality check: Renting only comes out ahead if the money you do not sink into a deposit and purchase costs is used well. If it drifts into lifestyle spending, you get the downside of renting without the upside of investing.

The price-to-rent ratio is useful in Perth

One of the cleaner ways to assess the decision is the price-to-rent ratio. It compares local home values with annual rent and gives you a quick sense of whether buying is stretched or relatively reasonable.

Analysts at CoreLogic put Perth’s price-to-rent ratio at 19.9 in late 2023, as noted in CoreLogic's Housing Affordability Report. That is a useful WA-specific signal because Perth often looks more affordable on this measure than Sydney or Melbourne, even after recent price growth.

Do not treat that figure as a rule. Use it as a filter. A ratio around that level can support buying for households planning to stay put for years. It does not rescue a rushed purchase, a poor-quality property, or a mortgage that crushes your cash flow.

Time horizon matters more than many buyers think

Interest rates matter. Time in the property matters more.

If you are likely to move in two or three years, buying often loses once you factor in entry and exit costs. If you expect to stay through several lease cycles, want more control over the property, and can carry the full ownership bill without stress, buying starts to look stronger.

| Time Horizon | Usually Favours | Why |

|---|---|---|

| Short term | Renting | Lower entry and exit friction |

| Medium term | Depends | Cash flow, suburb choice, and stability matter |

| Long term | Often buying | Equity, principal reduction, and housing certainty improve the case |

Loan structure changes the outcome

If you buy, the loan setup is part of the strategy, not admin. Offset accounts, redraw access, repayment flexibility, and the split between fixed and variable can materially change your cash flow and risk profile. If you are weighing that choice, read this guide on fixed or variable home loan rates before you commit.

My direct view on the numbers

For many Perth households, buying wins if three conditions are met. You expect to stay put. You keep a real cash buffer after settlement. You are not sacrificing every other financial goal just to get through the front door.

Renting wins when your time horizon is short, your employment or family situation is still shifting, or buying would force you to stop investing, stop contributing strategically to super, and run with no margin for repairs or rate changes.

That is the part generic rent versus buy guides often miss. In WA, the right decision is not just about house prices and rent. It is about whether the property fits the way Perth markets move, whether your tax position makes investing elsewhere more efficient for now, and whether your retirement plan improves from owning this particular home on this particular timeline.

Real-World Scenarios for West Australians

A couple in Mount Lawley can afford the mortgage on paper, but they still hesitate because one of them may take parental leave next year. A family in Joondalup is tired of lease renewals and school-zone uncertainty. A pre-retiree pair looking at Dunsborough wants lifestyle without locking too much wealth into the wrong property at the wrong time.

Those are three very different WA decisions. Generic national advice usually flattens them into the same spreadsheet. That is a mistake.

A dual-income couple in Perth

This is the classic household that can buy, but should not rush.

Perth apartments and smaller inner-city properties can look like an easy first step. Sometimes they are. Sometimes they become an expensive placeholder that stops fitting within a few years. If this couple already suspects they will outgrow the property, I would tell them to wait rather than force a purchase that creates two rounds of stamp duty, selling costs, and disruption.

The better question is not whether they can get approved. It is whether the property fits the next five to seven years of their life.

I would push this couple on four points:

- How stable is their income if one person cuts back work?

- Do they want flexibility on suburb and commute, or are they settled?

- Will buying drain cash they could otherwise direct to super or investments?

- Are they choosing a home, or reacting to fear of missing the market?

That last point matters in WA. Perth does not move like Sydney or Melbourne. It can run hard, cool off, then split sharply by suburb and dwelling type. A rushed purchase in the wrong pocket of the market can leave a professional couple stuck in a property that is neither a great home nor a great asset.

My advice is straightforward. Buy if they have stable jobs, a proper cash buffer after settlement, and a property they can live in for years without resentment. Rent if life is still shifting, but only with a clear plan to invest the savings gap. If they need help pressure-testing that choice, this guide to the best financial advisors in Perth is a sensible place to start.

A growing family in the northern suburbs

For a family, renting often becomes harder than the raw numbers suggest.

A primary cost is disruption. Every lease renewal carries risk. Every forced move can mean a new school route, a longer commute, and another year of living around a landlord’s decisions. In Perth’s outer and middle-ring family suburbs, that instability can do more damage than a slightly higher monthly housing cost.

Buying usually starts to make sense here because the benefit is practical, not just emotional.

Where buying often works well for families

- School-zone stability: You reduce the risk of moving because the landlord sells or changes plans.

- A better fit for family life: You can choose bedrooms, storage, outdoor space, and layout with the next stage in mind.

- More predictable routines: Childcare, commuting, and household logistics get easier when the home base is fixed.

I still would not tell a family to stretch to the edge. If the mortgage leaves no room for repairs, insurances, rising council rates, sport, transport, and a decent emergency fund, the house becomes another stress point.

A family home should create breathing room. It should not eat all of it.

In WA, this decision also has a longer-term tax and super trade-off that families often miss. If buying the home means stopping salary sacrifice, ignoring super contribution caps, and leaving no investable cash outside the house, the family may improve housing stability while weakening retirement outcomes. The right home purchase should support both.

A pre-retiree couple eyeing Dunsborough

This group needs sharper advice than “own your home before retirement.”

A couple in their late 50s or early 60s might be deciding between downsizing into a home they own outright, continuing to rent in a lifestyle location, or selling a larger Perth property and keeping more capital in super and liquid investments. In WA coastal and regional markets, price swings, limited stock, and resale risk can matter more than people expect, especially if health, mobility, or family support needs change later.

Sentiment is expensive at this stage.

I focus on three questions.

- How much of their wealth would end up trapped in the home?

- Would the property still suit them in ten or fifteen years?

- Does buying improve retirement cash flow, or just make them feel safer today?

For some pre-retirees, buying a lower-maintenance home before work stops is the right move because it cuts future rent risk and simplifies living costs. For others, renting first in a regional area is the smarter call because it lets them test the lifestyle before committing capital and paying transaction costs.

This is also where WA retirees need to think carefully about the interaction between housing, super, and Age Pension strategy. The family home is treated differently from super and other investments. That can make owning attractive, but it can also leave people asset-rich and cash-poor if they overcommit to the property itself.

My recommendation is simple. If retirement is close, buy the property that reduces pressure, protects cash flow, and will still work if life gets smaller, slower, or more complicated.

Beyond the Numbers Lifestyle and Long-Term Goals

A Perth couple gets offered a transfer to Bunbury, loves the idea of more space and less traffic, and starts browsing listings that weekend. That decision is not just about mortgage repayments. It affects job options, family support, school continuity, retirement timing, and how much cash stays available if life changes.

This part of the rent versus buy decision is where people make expensive mistakes. They treat lifestyle as a soft issue and assume the hard numbers matter more. I disagree. If the property locks you into the wrong suburb, the wrong commute, or the wrong stage of life, the spreadsheet has missed the point.

Flexibility versus control

Renting suits people whose next five years are still shifting. That includes households expecting career moves, relationship changes, school transitions, or a trial run in a regional WA town before committing. In places like Busselton, Albany, or Geraldton, that trial period matters because resale can be slower and local demand can change faster than Perth buyers expect.

Buying suits people who know what they want and are prepared to stay long enough to justify stamp duty, moving costs, and the effort of ownership. Control matters. You can renovate, keep pets without asking permission, settle the kids properly, and stop worrying about a landlord selling underneath you.

That stability has financial value, even if it does not fit neatly into an online calculator.

The lifestyle risk that calculators miss

Renting is only flexible if you can move on your terms. If each lease renewal brings stress, your child may need to switch schools, or suitable rentals are scarce in your part of WA, the practical cost is real.

Owning has its own pressure. A mortgage can limit career choices. Maintenance can absorb money you would rather direct to super or other investments. In older Perth suburbs and many regional areas, repair bills are not occasional annoyances. They are part of the ownership budget.

The right question is simple. Which option gives you more control over your life, not just your housing?

Pre-retirees and regional WA need a sharper filter

For pre-retirees, housing decisions need to match the next stage of life, not the current one. A large home in a beautiful location can become hard work if mobility changes, health needs increase, or adult children live far away. In regional WA, those trade-offs can be sharper because medical services, transport, and buyer depth are not the same as metro Perth.

This also affects how you split wealth between your home and retirement savings. WA households nearing retirement often focus on owning outright for peace of mind, but overcommitting to the property can leave too little in super and liquid assets. The Department of Social Services explains the Home Equity Access Scheme, which exists for retirees who are asset rich and need to draw on home equity later. That is a fallback, not a plan.

If selling later is part of your strategy, understand how the main residence exemption on your home may affect the tax outcome before you buy.

Pressure-test the decision with these questions:

- Will this home still suit you if work, health, or family circumstances change?

- Are you buying because it fits your next ten years, or because owning feels safer?

- If you rent, will you invest the difference through super or other assets?**

- If you buy in regional WA, how confident are you that you could sell without strain if plans change?

My view is straightforward. Buy when the property supports the life you want to live and leaves enough financial breathing room to handle change. Rent when flexibility, cash reserves, and optionality matter more than control.

Tax Super and Retirement Implications

A Perth couple in their mid-50s can look strong on paper, decent income, a good house, and growing super, then hit retirement with a problem they did not see coming. Too much wealth is tied up in the home, not enough is accessible for income, and the tax settings around each asset class work very differently.

WA households need to treat this as a three-part decision. Your home, your super, and your tax position all interact. Generic rent versus buy guides usually miss that, especially in a state where mining cycles, regional property swings, and uneven growth between Perth suburbs can change the outcome.

Your home and your super do different jobs

A paid-off home protects cash flow in retirement. That matters because rent keeps rising long after wages stop.

Super does a different job. It produces retirement income, gives you investment diversification, and can be managed tax-effectively as you move from accumulation into pension phase. If you pour every spare dollar into the mortgage and neglect super, you may reach retirement with housing security but limited income flexibility. If you keep renting and fail to build super aggressively, you create the opposite problem. Ongoing housing costs and inadequate retirement savings.

My advice is simple. Avoid ending up rich in one bucket and weak in the other.

Why this matters more in WA

WA property does not move in a straight line. Perth has had long flat periods, sharp rebounds, and major differences between inner, outer, and regional markets. That means home equity can grow well over time, but it can also disappoint for years if you buy the wrong property or buy at the wrong point in the cycle.

Super is usually steadier from a portfolio construction point of view because it is spread across asset classes. That makes it a useful counterweight to concentrated housing risk. For WA households with a large exposure to one property and one local job market, that diversification matters.

This is one reason I push clients to look beyond the headline question of rent or buy. The core question is whether your retirement plan is balanced enough to survive a property downturn, a health issue, or an earlier-than-expected finish to work.

Tax rules can tilt the decision

The family home gets favourable treatment in Australia. For many households, that makes ownership attractive over the long term. Capital gains tax generally does not apply to your principal home if it qualifies, and this guide to the main residence exemption on your home is worth reading before you buy, sell, or rent the property out later.

Super also comes with strong tax advantages, particularly if you contribute consistently and use the rules properly in the years before retirement. That can include concessional contributions, contribution timing, and drawing income tax-effectively after preservation age. The mistake is treating the home as a tax winner and super as secondary. In practice, both can be powerful if you use each for the right purpose.

Rent vesting sits in the middle. It can work well for higher-income WA professionals who want location flexibility in Perth but still want exposure to the property market. It can also become messy fast if you do not understand deductibility, future capital gains consequences, and how a later move into the property changes the tax outcome.

Retirement decisions I’d make in your shoes

If you are within 10 to 15 years of retirement, I would focus on these priorities:

- Aim to enter retirement with low housing costs. Owning outright is ideal. A modest remaining mortgage can be manageable. Ongoing full-market rent is harder to absorb.

- Keep building super while you work. A home reduces costs. Super pays the bills.

- Be careful about overspending on the house. In WA, an expensive home in a slower-moving market can leave you asset rich and cash poor.

- Treat rent vesting as a strategy, not a compromise. It only works if the cash flow, tax treatment, and long-term plan all stack up.

One more point. Downsizing is not a retirement plan by itself. It is an option. Sale timing, transaction costs, available buyer demand, and where you intend to live next all matter, especially outside metro Perth.

A suitable home and a healthy super balance usually beat trying to maximise one at the expense of the other. That is the combination I would target.

Your Decision Framework and Next Steps

If you’re still stuck, good. That usually means you’re taking the decision seriously.

Here’s the framework I’d use.

Buy if most of these are true

- You expect to stay put for years, not just until the next life change.

- Your income is stable enough to carry repayments without stress.

- You have cash left after the deposit, not just enough to scrape through settlement.

- The property fits your next chapter, whether that’s children, remote work, or retirement.

- You want housing certainty and value control over flexibility.

Rent if most of these are true

- You’re still testing location or lifestyle.

- Your career or business income is variable.

- You may move in the near future.

- Buying would overstretch cash flow.

- You have a real investment plan for the surplus.

Avoid both bad versions

There’s a bad version of buying and a bad version of renting.

The bad version of buying is stretching too far, buying the wrong property, and hoping time fixes a weak decision.

The bad version of renting is telling yourself you’re “being flexible” while doing nothing useful with the extra cash and watching rent rise around you.

Don’t choose the option that sounds smartest. Choose the one you can execute consistently.

My bottom-line recommendation

For many WA households, especially those with stable income and a longer time horizon, buying is the stronger wealth-building move. For people in transition, people with uncertain job paths, or pre-retirees testing a new location, renting can be the smarter temporary move.

Temporary is the key word. Drift is expensive.

A proper decision needs modelling around cash flow, time horizon, super, debt, risk, and retirement impact. Generic calculators won’t do that well enough. You need the numbers, but you also need judgement.

If you want specific help with the rent v buy decision, Wealth Collective can help you model the trade-offs properly.co) can help you model the trade-offs properly. Their Perth and Dunsborough advisers work across debt reduction, super, retirement planning, and long-term wealth strategy, so the housing decision fits the rest of your financial life instead of derailing it. Start with a free 10-minute introductory call and get clear on what buying, renting, or rentvesting would mean for your cash flow, your retirement timeline, and your next move.