Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

If you’re living in Perth, Dunsborough, Bunbury or anywhere else in WA with a UK pension sitting offshore, you’re probably asking the same blunt question: should you leave it alone, or bring it across to Australia?

The right answer depends on timing, structure and whether you can satisfy the rules without triggering avoidable tax. That’s why moving uk pension to australia isn’t a paperwork exercise. It’s a strategy decision. Get it right and your retirement assets can sit in the same system you plan to retire in. Get it wrong and you can create tax, delays and a compliance mess that follows you for years.

WA residents face an extra layer of friction. The advice market here is smaller than the east coast, and specialist support for UK pension transfers, especially where an SMSF is involved, is harder to find. That doesn’t make the process unworkable. It just means you need to be organised early and make the key decisions in the right order.

Is Your UK Pension Eligible for a Move to Australia?

You’re in Perth, your retirement is going to be spent in WA, and a UK pension is still sitting on the other side of the world. Before you look at forms, providers or transfer timelines, answer one question clearly. Is the pension eligible to move without creating a bigger problem than it solves?

That decision rests on four things. Your age, your residency position, the type of UK pension you hold, and whether the receiving structure in Australia can legally accept it. If one of those is off, the transfer can be blocked, delayed, or taxed badly.

Age comes first

Start with the UK pension rules, not the Australian ones. HMRC’s pension tax manual makes the access point clear. The minimum pension age is 55 and is scheduled to rise to 57 from April 2028, subject to the current legislative timetable, as outlined in the HMRC guidance on normal minimum pension age.

That matters for WA clients in their mid-50s. If you are 55 or 56, timing is not a side issue. It affects whether a receiving Australian structure can satisfy UK rules and whether you should act now or wait.

Australia runs on a different system. Preservation age, retirement condition of release, and age 65 access rules do not line up neatly with the UK framework. If you do not already understand the destination fund rules, read how superannuation works in Australia before making transfer decisions.

Residency decides the tax risk

A transfer that suits a settled WA resident can be the wrong move for someone still splitting time between Australia and the UK.

If you live in WA permanently, pay tax here, and plan to retire here, the advice is usually more straightforward. If your residency is still shifting, or a move back to the UK remains on the table, stop and sort that out first. I would not recommend starting a transfer strategy until your tax residency position is clear.

This is especially important in WA, where clients often arrive after years of cross-border work in mining, engineering, healthcare, or small business. Those careers create messy residency histories. Clean that up early.

Pension type matters more than people expect

Defined contribution pensions are usually the cleanest cases. There is an account balance, an investment mix, and a transfer value that can be assessed against Australian rules.

Defined benefit schemes need much more care. They often include guarantees, protected benefits, or income rights that are hard to replace once surrendered. A transfer can still be possible, but the right test is not whether it can be done. The right test is whether giving up those benefits improves your retirement outcome in WA.

That is where many generic articles fail. They treat every UK pension like a portable cash balance. It is not.

Size still affects eligibility in practice

Large balances often run into Australian contribution and structuring issues, even when the pension itself is transferable.

That does not always mean the move is off the table. It means the transfer has to be planned properly. Timing, tax treatment, fund design, and the amount being moved all need to line up. For West Australians using specialist local support, this is usually where the essential work begins.

Use this checklist before you spend money on setup or advice letters:

- Age: Are you old enough under current UK rules, and have you allowed for the scheduled rise to age 57?

- Residency: Are you clearly an Australian tax resident, with WA as your long-term base?

- Pension type: Is it defined contribution, or a defined benefit scheme with guarantees worth preserving?

- Transfer size: Can the amount be received in a way that fits your Australian retirement structure?

- End goal: Are you transferring for a better retirement outcome in Australia, or just because the pension feels inconvenient sitting in the UK?

If any of those answers are unclear, pause. The best result is not the fastest transfer. It is a transfer that leaves you in a stronger position for retirement in WA.

Choosing Your Pension's New Home SIPP vs QROPS

You are back in Perth, your UK pension is still sitting offshore, and you want your retirement money organised around the life you are now building in WA. That usually leads to one decision. Keep the pension in the UK through a SIPP, or move it into an Australian structure that can receive a UK transfer.

For West Australians, this choice is rarely about paperwork alone. It is about control, cost, local support, and whether you want your retirement assets governed under the same system you expect to retire under.

The Australian route is usually an SMSF

If you want to transfer a UK pension into Australia, the receiving fund usually needs to be set up very carefully. In practice, that often points to an SMSF rather than a large retail or industry fund. HMRC’s rules on when benefits can be accessed have narrowed the field, and Australian public offer funds generally do not suit these transfers. The ATO’s guidance on self-managed super funds is a good starting point if you want to understand the trustee obligations that come with that structure.

That matters more in WA than generic national guides admit. Perth has fewer advisers, accountants, and deed providers who regularly handle HMRC-sensitive pension transfer work. Fewer specialists means higher risk if you choose the wrong firm, and slower setup if documents need to be redone.

An SMSF can work very well. It is not the default answer for everyone.

SIPP versus QROPS. Make the decision on fit, not fashion

A SIPP keeps the pension in the UK system. That can be the right call if you want lower administration, fewer moving parts, and no trustee responsibilities in Australia.

A QROPS-style transfer into Australia, which for many WA clients means a correctly structured SMSF, suits people who want their retirement savings based here, reported here, and invested within their broader Australian plan.

Here is the practical comparison.

| Feature | UK SIPP (Self-Invested Personal Pension) | Australian QROPS (via SMSF) |

|---|---|---|

| Location of assets | Remains in the UK pension system | Sits inside an Australian super structure |

| Administration | Usually simpler if the pension already exists | Higher, because the SMSF has its own trustee, audit, tax and deed requirements |

| Control over investments | Depends on the SIPP provider | High, if the SMSF is set up and run properly |

| Costs | Ongoing platform and advice costs depend on the provider | Setup, annual accounting, audit, tax return and administration costs apply |

| WA support availability | Less dependent on Perth-based specialists | More dependent on local professionals who understand both Australian super rules and UK transfer conditions |

| Retirement alignment | Pension stays offshore | Retirement assets sit in the country where many WA returnees plan to retire |

My advice

If you expect to stay in WA long term, want your retirement assets consolidated in Australia, and have enough in the pension to justify SMSF costs, the Australian route deserves serious attention.

If your pension is smaller, your future country of residence is still unclear, or you do not want the work that comes with being an SMSF trustee, keep the pension in the UK and manage it properly there.

That is the right filter. Outcome first. Structure second.

What often gets missed in WA

Local execution matters. A technically valid strategy can still become expensive if your Perth accountant does not understand UK transfer reporting, or your SMSF deed is drafted without the restrictions needed for a compliant receiving fund.

That is why I tell WA clients to decide two things at the same time. First, does the transfer improve your retirement position? Second, do you have the right local team to set it up and keep it compliant?

Before you commit, read our guide to what an SMSF is and how it works, then test your plan against these questions:

- Do you want your retirement assets based in Australia for the long term?

- Are you willing to act as an SMSF trustee and handle the responsibilities that come with that role?

- Will the pension balance justify setup and ongoing SMSF costs?

- Do you have WA-based professionals who understand both Australian super and UK pension transfer rules?

Choose the structure that fits your retirement in WA. Do not choose the one that sounds more impressive.

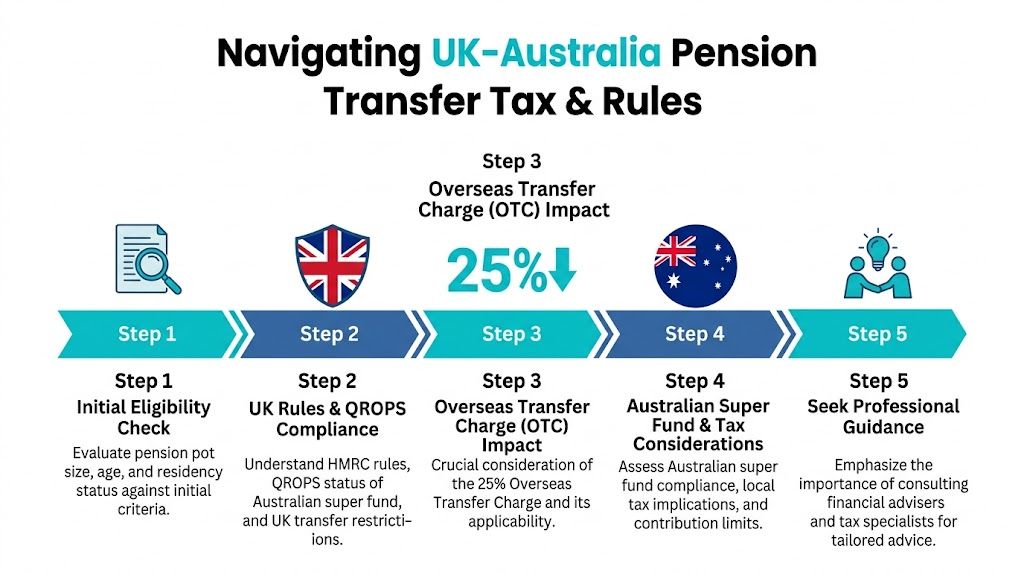

Understanding the Critical Tax and Transfer Rules

A Perth couple can get the structure right, sign every form correctly, and still lose a painful amount to tax because they transferred at the wrong time or ignored one UK rule. That is why I treat tax timing as the decision point, not admin.

The 25 percent charge you must avoid

The first rule is simple. Do not trigger the Overseas Transfer Charge.

HMRC sets out when a transfer to a QROPS can attract a 25% charge in its guidance on the overseas transfer charge. For WA clients, the practical test is straightforward. You want to be an Australian tax resident when the transfer happens, and you need a plan to stay based in Australia for the required period after the transfer.

People get this wrong when they focus on today’s address and ignore what happens next. If there is a real chance you will leave Australia again, pause. Review the transfer before a provider sends a dollar.

The allowance limit matters for larger pensions

Large balances need special care. Since April 2024, the old lifetime allowance framework has been replaced, and cross-border transfers now sit alongside the UK’s updated lump sum and overseas transfer rules. HMRC explains the current position in its Pensions Tax Manual.

For clients in WA with substantial UK pension rights, this is where strategy matters. A full transfer is not always the best answer. In some cases, keeping part of the pension in the UK protects flexibility and avoids an unnecessary tax hit.

The six-month window can save tax

Australian tax treatment changes once you become an Australian resident, and the timing of the transfer can materially change the result. The ATO explains this under foreign transfers to Australian super funds.

The short version is this. If you transfer within six months of becoming an Australian resident, you may avoid Australian tax on the growth component that would otherwise be assessed after that date. Miss that window, and the transfer can still work, but you need the numbers done properly before you proceed.

If you have recently returned to Perth, Busselton, Albany or anywhere else in WA, act early. That six-month period disappears faster than people expect.

How Australian tax applies to growth

Australian tax does not usually apply to the full value of the pension transfer. It generally applies to the growth that accrued after you became an Australian tax resident and before the money entered the Australian super environment. The ATO refers to this as applicable fund earnings in its guidance on transfers from foreign super funds.

That distinction matters. A pension that built up over many years in the UK does not suddenly become fully taxable in Australia because you moved to WA. The taxable slice is usually much narrower. The problem is that many people only discover the amount after the transfer paperwork has started, which is far too late.

Where the receiving Australian fund is structured correctly, there may be options for the fund to pay tax on that growth at the concessional super rate rather than having it taxed personally at your marginal rate. This is exactly why the transfer should sit inside a broader taxation and tax planning strategy, especially if you are coordinating an SMSF, UK advice, and your long-term retirement income plan in Western Australia.

The right way to assess the tax position

Use this order.

- Confirm Australian tax residency before any transfer date is locked in.

- Check your future residency plans. A WA base only works if it is likely to last.

- Review the size of the pension against the current UK transfer and allowance rules.

- Test the timing against the six-month Australian residency window.

- Calculate post-residency growth so you know what may be taxed in Australia.

That is the clean approach. WA clients do best when they treat the transfer as part of their retirement plan, not as a paperwork exercise.

The Pension Transfer Process from Start to Finish

Once the strategy is right, the mechanics are manageable. They’re detailed, but manageable.

Most delays happen because people start paperwork before the receiving structure is ready, or because one document is missing and nobody notices for weeks.

The order matters

The transfer usually begins with an eligibility and structure check. If an Australian QROPS pathway is being used, the receiving fund has to be ready before the UK provider releases anything. That means the SMSF, deed wording and compliance settings need to be in place first.

After that, you request transfer information from the UK pension provider. In many cases, that includes a Cash Equivalent Transfer Value, often called a CETV. Treat that valuation as time-sensitive. Providers usually issue it for a limited period, and if it expires, you may need an updated figure before the transfer can move forward.

The paperwork is not optional

The core documents typically include:

- HMRC Form APSS 263: This is part of the transfer administration for a ROPS-compliant move.

- Certified identification: Commonly passport and address evidence.

- UK pension scheme details: The provider needs enough information to process the transfer accurately.

- Receiving fund evidence: The Australian arrangement must be able to demonstrate the required status and structure.

One overlooked point is ongoing reporting. The Australian receiving fund may need to report to HMRC for years after the transfer. That’s one reason DIY transfers often unravel later, even if the money arrives successfully.

Expect patience, not speed

The practical timeline can be slow. A compliant transfer can take months, especially where there are UK provider delays, deed corrections, AML checks, residency evidence requests or foreign exchange decisions still unresolved.

A useful working mindset is this: if your retirement depends on the transfer landing by a specific date, you’re already too tight on time. Build slack into the plan.

The transfer process rewards clients who prepare early. It punishes clients who rush because a tax deadline is close.

Currency handling deserves more respect

Your UK pension is denominated in pounds. Your Australian retirement spending is likely in Australian dollars. That gap creates one of the most frustrating parts of the transfer.

Exchange rates can move while the paperwork crawls through providers and administrators. You can’t control the market, but you can control your process. Lock down who is handling the FX side, when conversion will happen and how that decision fits your broader retirement cash needs.

A sensible transfer process usually follows this sequence:

- Confirm suitability of the transfer

- Set up the correct receiving structure

- Collect provider information and transfer values

- Prepare HMRC and fund documentation

- Submit and monitor the transfer

- Coordinate foreign exchange carefully

- Record all transfer and tax documents for future compliance

Clean administration won’t make a bad strategy good. But poor administration can absolutely ruin a good one.

Common Transfer Pitfalls and How to Avoid Them

A Perth couple transfers a UK pension into Australia, assumes the hard part is over, then starts talking about a possible move back to Britain to be closer to family. That is the kind of ordinary decision that turns a good transfer into an expensive one.

The biggest mistakes happen after people convince themselves the transfer is just paperwork. It is not. A successful move depends on where you expect to live, how you want your estate handled, and which Australian structure you chose at the start.

Returning to the UK can change the result

This catches West Australians more often than it should. Many people settle in WA, transfer their pension, then a few years later reassess because children, parents, health, or work pull them back to the UK.

That possibility needs to be tested before any transfer begins.

HMRC explains that an Overseas Transfer Charge can apply in some circumstances, including cases where the member and the receiving arrangement are not in the same country after the transfer or where conditions later change within the relevant period, as set out in its guidance on the Overseas Transfer Charge. From April 2027, UK pensions are expected to be included in UK Inheritance Tax calculations. That makes future location and estate planning more important, not less.

If there is a real chance you will return to the UK, model that first. Do not transfer now and hope the residency question sorts itself out later.

WA clients often underestimate estate planning risk

For many people in Western Australia, the transfer decision gets framed as a tax question or an investment question. That is too narrow.

If your spouse, children, or intended beneficiaries are split between Australia and the UK, the structure of the pension matters. So does your long-term residency path. So does whether your broader retirement assets sit inside super, outside super, or partly in both systems.

A transfer can improve one part of the plan while creating a problem somewhere else. I see this with clients in Perth who have UK family ties, Australian property, and no current estate plan that reflects both countries. Fix that before money moves.

Judge the transfer by the retirement outcome it creates in WA, not by how satisfying it feels to get the pension out of the UK.

Four mistakes that are easy to avoid

- Transferring before your residency position is clear. If your tax residency and long-term home are still uncertain, wait until the strategy is clear.

- Using the wrong receiving structure. A standard super setup or generic SMSF deed can be a poor fit for a UK pension transfer.

- Ignoring the chance of a future move back to the UK. This is common among returning Australians and UK-born WA residents with family overseas.

- Looking only at transfer tax. Withdrawal rules, death benefits, and estate consequences can matter just as much.

What to do instead

Start with the end point. If you plan to retire in Western Australia, build the transfer around that outcome, your local super structure, and the way your family will use the money. If your future is split between WA and the UK, be honest about that and get advice that tests both paths.

Good clients do three things well. They confirm the likely country of retirement. They check the estate position before choosing where the pension should sit. They keep every transfer, tax, and residency record in order.

That discipline saves money. It also saves stress, which matters just as much when your retirement plan crosses two countries.

Build Your Retirement Roadmap with Wealth Collective

A UK pension transfer can absolutely be done well. But it should never be treated as a simple admin task.

You’re dealing with UK access rules, Australian super law, transfer allowances, tax residency, possible SMSF setup, estate planning and timing pressure. A mistake isn’t just annoying. It can change the amount that lands in your retirement plan.

That’s where clear advice matters. Not generic guidance. Not a half-read forum thread. Actual strategic advice specific to your life in Western Australia.

At Wealth Collective, the focus is simple. Help clients make smart decisions with confidence. For people returning from the UK or settling permanently in WA, that means looking beyond the transfer form itself and building a workable retirement structure around it.

A proper plan should answer questions like these:

- Should you transfer at all, or leave the pension in the UK?

- Does an SMSF make sense for your balance and goals?

- How should the transfer timing fit with your residency and retirement date?

- What does this mean for your wider super, tax position and estate planning?

That’s the difference between isolated advice and a retirement roadmap. One gets the form lodged. The other helps you retire with fewer loose ends.

If you want straight answers about your options, start with a short conversation and get your position clarified before you make a move you can’t easily unwind.

Book a complimentary introductory call with Wealth Collective if you want experienced, WA-based guidance on moving uk pension to australia. We’ll help you work out whether a transfer suits your goals, what structure fits best, and how to build the move into a practical retirement plan.