Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

A pay rise should feel simple. More money lands in your account, you breathe easier, and you move on.

In practice, that’s rarely how it feels. A higher salary often brings a bigger question. Should you take the extra cash now, push some of it into super, or use a salary packaging option that looks tax-effective on paper but could clash with the rest of your plans?

That’s why people ask, is salary sacrifice worth it. The honest answer is that it can be. It can also be the wrong move at the wrong time.

The clients who get the most value from salary sacrifice usually don’t look at it as a tax trick. They treat it as part of a broader strategy. That means weighing the tax benefit against cash flow, home ownership plans, insurance settings, debt reduction, and how soon they may need access to the money.

Starting Your Financial Strategy

A common version of this starts with a new role or an annual review. Your employer offers a stronger package, and payroll mentions salary sacrifice as an easy way to “save tax”. That part is true, but it’s only part of the story.

If you’re in that position now, slow the decision down just enough to make it useful. The right question isn’t whether salary sacrifice is good in general. It’s whether it helps the life you’re building.

A young professional might use salary sacrifice to build super earlier and create a habit of investing before money hits their spending account. A couple with children might be more cautious because their budget is already carrying a mortgage, school costs, and insurance premiums. A pre-retiree may see it very differently again, especially if they want to make the most of the concessional cap while they still have strong income.

Before changing your pay structure, get clear on your monthly cash flow. If you haven’t mapped that out recently, it helps to create a household budget before making any salary sacrifice election. That gives you a practical view of what your reduced take-home pay would feel like.

Salary sacrifice works best when it supports the next major goal in your life, not when it competes with it.

That’s the lens worth using throughout this decision. Tax matters. So does flexibility.

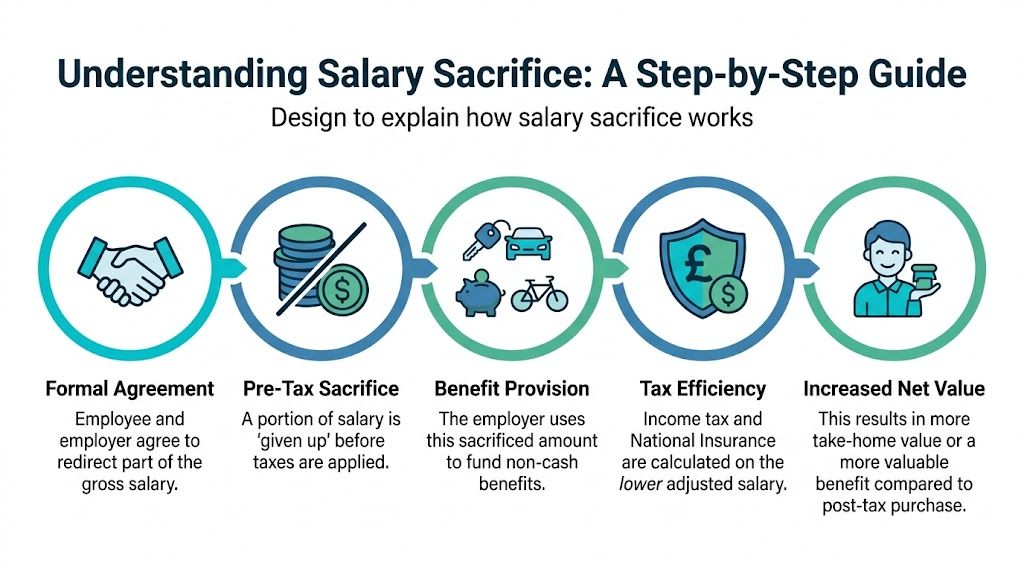

What Is Salary Sacrifice and How Does It Work

You agree to a lower cash salary in exchange for your employer directing part of that amount to an approved benefit before tax. In Australia, that usually means extra contributions to super. For some workers, it can also include a novated lease or other packaged benefits offered through payroll.

The practical effect is simple. Less of your pay lands in your bank account each cycle, and more is redirected to a purpose you have chosen under a formal arrangement. That can improve tax efficiency, but it also changes how your income looks on paper and how much cash you have available for current goals.

The basic mechanics

For super, the arrangement usually works like this:

-

You nominate an amount with your employer

This is usually a fixed dollar amount each pay cycle. -

Payroll reduces your pre-tax salary by that amount

The contribution is made before your income tax is worked out. -

Your employer sends the amount to your super fund

It is treated as a concessional contribution and counts toward your concessional cap. -

Your payslip and take-home pay both change

You see lower net pay, but more money is going to long-term retirement savings.

This is different from transferring money into super yourself after you have been paid. In practice, that timing difference is the whole point. Salary sacrifice changes the path the money takes before it reaches your account.

If you want a broader refresher on how super fits into your financial life, this guide on superannuation in Australia is a useful starting point.

Why super is the most common option

Super is the version I discuss most often with clients because it is straightforward, widely available, and usually easy to set up through payroll. It also creates a useful discipline. Money that never reaches your everyday account is less likely to be absorbed into restaurants, subscriptions, school costs, or a larger mortgage repayment than you planned.

That discipline can be helpful, but it comes with a trade-off. Once the money goes into super, it is generally preserved until you meet a condition of release. That is why salary sacrifice can look excellent on a tax summary and still be the wrong move for someone trying to build a home deposit, keep borrowing capacity strong, or maintain flexibility over the next few years.

Other forms of salary sacrifice

Super is not the only option. Some employers offer salary packaging for cars through novated leases, where lease payments and some running costs are handled through your salary package under a documented agreement.

In real advice conversations, the two options that come up most often are:

- Extra super contributions for retirement planning and tax management

- Novated car leases for employees who were already planning to run a vehicle and want to compare the full after-tax cost carefully

Practical rule: If payroll has not documented the arrangement in advance and it does not show clearly on your payslip, it is not salary sacrifice in the usual sense.

Timing matters. Once salary has already been earned and become payable as cash, you generally cannot decide after the fact to treat it as sacrificed income.

The Major Benefits of Salary Sacrificing

The strongest case for salary sacrifice is simple. It can direct more of your income toward goals that matter to you, while reducing the drag of tax along the way.

That doesn’t mean every salary sacrifice option is automatically worthwhile. It means the strategy can be very effective when the benefit aligns with something you already intended to do.

Better tax efficiency on super contributions

For people building retirement wealth, salary sacrificing into super can improve tax efficiency because the contribution is made from pre-tax income rather than from money that has already landed in your account after tax.

That creates a clear behavioural advantage too. Saving becomes automatic. You don’t need to rely on willpower at the end of the month, after the mortgage, school fees, travel, and impulse spending have taken their share.

For some clients, that discipline is more valuable than the tax outcome itself. They’ve always meant to contribute more to super. Salary sacrifice is the first system that gets it done.

Stronger long-term compounding

The second benefit is what happens after the contribution goes in. Money inside super remains invested for the long term, and regular pre-tax contributions can help build momentum earlier.

This becomes especially relevant for people who have moved through the expensive early years of adulthood and now have surplus income. If you’ve recently paid off consumer debt, received a promotion, or moved into a higher bracket, salary sacrifice can be a clean way to redirect part of that surplus before lifestyle inflation absorbs it.

Useful for carry-forward strategies

This matters most for people nearing retirement or with uneven income from year to year. If you have unused concessional cap amounts available, salary sacrifice can work alongside a larger contribution strategy rather than sitting in isolation.

The detail matters here because contribution caps can create expensive mistakes if ignored. If this is relevant to you, review the rules around carry forward concessional contributions before changing payroll instructions.

Novated leases can work in the right case

Salary sacrifice isn’t only about super. Vehicle packaging through a novated lease can also produce savings for some employees.

According to this novated lease overview, salary sacrifice cars in Australia can deliver 25% to 35% cost savings for some employees, driven by GST exemptions and Fringe Benefits Tax concessions. The same source notes that SG Fleet reports average client savings of around $4,200 per annum, with benefits often stronger for eligible electric vehicles.

That doesn’t mean every novated lease is good value. It means there are situations where the packaging structure is worth modelling, especially if the car was already part of your plan and you were going to fund running costs anyway.

Where the upside is strongest

Salary sacrifice tends to work best when these conditions line up:

- You have surplus cash flow and won’t feel squeezed by a lower pay packet.

- You’re in a higher marginal tax bracket and want to improve how extra income is directed.

- Retirement savings are an active priority, not something you’ll “get to later”.

- You’re not planning a near-term loan application where taxable income is central to serviceability.

- You’ve checked your contribution limits before increasing super deductions.

The benefit is real. The key is making sure the tax gain isn’t coming at the expense of something more urgent.

Key Risks and Downsides You Must Consider

The biggest mistake people make with salary sacrifice is treating tax savings as the only score that matters.

It isn’t. Tax is one part of the picture. Your borrowing power, liquidity, insurance, and day-to-day cash flow can matter just as much. Sometimes more.

Reduced take-home pay is the first pressure point

This sounds obvious, but it’s where many strategies fail in practice. A pre-tax contribution still reduces the amount that arrives in your bank account. If your budget is already tight, salary sacrifice can create stress quickly.

That stress usually shows up in predictable ways. You rely more on credit cards. You stop saving for short-term goals. You pull money from offset or emergency savings to manage regular bills. At that point, the strategy may still look efficient on paper while weakening your actual financial position.

If salary sacrifice leaves you short every month, it’s not disciplined investing. It’s an avoidable cash flow problem.

This is why the right amount matters more than the theoretical maximum.

Borrowing power can fall sharply

This is the overlooked issue I’d want most clients to understand before they sign anything with payroll. Lenders often assess serviceability using your reported taxable income. If you sacrifice part of your salary, your on-paper income may look lower when you apply for a home loan.

That can reduce what a bank is willing to lend, even if your long-term strategy is sensible.

According to this analysis of salary sacrifice disadvantages, sacrificing $20,000 from a $120,000 salary could reduce borrowing capacity by $80,000 to $100,000 under typical lender stress tests. For anyone trying to enter the Perth market or upgrade homes, that’s not a minor side effect.

Super contributions are preserved

Money salary sacrificed into super isn’t sitting in a flexible savings account. It becomes part of your super balance and is generally preserved until you meet a condition of release.

That makes the strategy structurally different from investing outside super or building cash reserves in an offset account. The tax outcome may be stronger, but access is restricted.

If access rules are part of your decision, this explanation of when you can access your super is worth reading before you commit to a larger salary sacrifice arrangement.

High-income earners need to watch tax traps

Salary sacrifice often appeals most to executives and business owners because the tax difference can be meaningful. That’s true, but high-income earners also need to watch additional tax complexity.

The verified data notes that Division 293 tax adds an extra 15% on contributions for incomes above $250,000. That doesn’t mean salary sacrifice stops being useful. It means the margin for error gets smaller, and the strategy needs to be modelled properly rather than guessed.

There’s also the concessional contributions cap to watch. The verified data notes that the cap is $30,000, with unused amounts able to be carried forward for up to five years from 2018-19 onwards, based on the ATO details summarised in this article. Exceeding caps or misunderstanding what your employer is already contributing can turn a tax-effective idea into an admin and tax headache.

Insurance and benefits can be affected

This is another issue that rarely gets enough attention. Some insurance arrangements and benefit assessments depend in part on salary definitions, reportable income, or taxable income. The exact impact depends on the insurer, policy wording, lender, and agency involved.

A lower reported income can affect how others assess your capacity, entitlement, or replacement income. That doesn’t mean salary sacrifice should be avoided. It means you should check the definitions before you reduce your salary on paper.

A sensible review usually includes:

- Income protection settings so you know how benefits are calculated

- Mortgage plans over the next few years

- Cash reserves for emergencies and upcoming expenses

- Current employer super contributions so you don’t accidentally exceed limits

- Any means-tested entitlements that could be affected by income changes

The downside of salary sacrifice isn’t that it’s bad. The downside is that it can solve the tax problem while creating a different problem somewhere else.

Worked Examples Who Benefits Most?

Salary sacrifice becomes easier to judge when you stop asking whether it’s good in theory and start asking who it suits.

Below is a practical comparison built around three common client situations. Only one scenario has a verified numerical case study attached, so the other two are assessed qualitatively rather than with invented numbers.

Three common profiles

Sarah is in the accumulation phase. She’s earning well, but she also wants flexibility. Her questions are usually about balancing super with travel, saving, or a future property purchase.

David is the classic high-income earner weighing tax efficiency against contribution caps, insurance structure, and possible loan applications.

Jane is closer to retirement. Her attention is on making the most of remaining working years and using available contribution rules carefully.

| Scenario (Income) | Annual Sacrifice | Annual Tax Saved (Approx.) | Annual Take-Home Pay Reduction | Net Annual Benefit |

|---|---|---|---|---|

| Sarah, young professional | Modest amount that fits cash flow | Qualitative benefit only | Lower take-home pay, but manageable if budgeted | Best when retirement saving matters more than short-term access |

| David, WA executive on $200,000 | $20,000 | $9,500 avoided income tax, with around $6,500 net annual tax saving compared with after-tax investing | Reduced pay packet, partly offset by tax efficiency | Strong for long-term wealth building if caps and lending plans are managed |

| Jane, pre-retiree | Higher amount only if cap space and cash flow allow | Qualitative benefit only | Noticeable reduction in cash salary | Can be compelling when retirement is close and access to funds is less of a concern |

The executive example is the clearest numerical case

For a Western Australian executive earning $200,000 and sacrificing $20,000 into super, the pre-tax contribution avoids approximately $9,500 in income tax, and because the contribution is taxed at 15% inside super, the net annual tax saving is around $6,500 compared with investing after-tax, according to this salary sacrifice example.

That’s the kind of scenario where salary sacrifice often has obvious appeal. The tax position is stronger, and the contribution is directed to a long-term structure many executives already want to build.

Why Sarah may still say no

For someone earlier in their career, salary sacrifice can be sensible, but it isn’t automatically the top priority. If Sarah wants to buy a home, maintain flexibility, or build a larger emergency fund, locking extra money into super may be less useful than keeping cash accessible.

In such instances, advice often becomes less about maximising tax savings and more about sequencing goals. A strategy can be mathematically attractive and still be mistimed.

Client lens: The best salary sacrifice strategy is the one that leaves your next major goal easier to reach, not harder.

Why Jane may benefit for a different reason

For a pre-retiree, the question often changes. Flexibility still matters, but immediate access may matter less than boosting retirement readiness while employment income is still strong.

Where unused concessional cap amounts are available, salary sacrifice can become part of a final contribution strategy rather than a permanent payroll habit. The client isn’t just “saving tax”. They’re repositioning assets for retirement.

That distinction matters. The same tool serves different purposes at different stages of life.

Your Decision Checklist Before You Commit

A good salary sacrifice decision usually survives a few uncomfortable questions. If the strategy still makes sense after that, it’s often worth pursuing. If it falls apart under basic pressure testing, that’s useful to know before payroll locks it in.

Ask yourself the cash flow questions first

Start with your bank account, not the tax outcome.

-

Can your household comfortably absorb lower take-home pay?

If the answer is “maybe”, the amount is probably too high. -

Do you already have an emergency buffer?

Preserved super doesn’t help when the hot water system fails or your car needs urgent work. -

Will this force you to use debt for regular expenses?

If salary sacrifice leads to revolving card balances, the strategy is misfiring.

Then check your next major life goal

Here, many people change their answer.

-

Are you planning to apply for a mortgage soon?

If yes, reduced taxable income may matter more than the tax benefit. -

Will you need access to this money before retirement?

If you need flexibility, super may be the wrong destination for the next dollar. -

Are you also trying to reduce bad debt or build an offset?

Sometimes the better financial move is outside super, at least for now.

Finally, review the technical settings

The details aren’t exciting, but they matter.

-

What is your employer already contributing to super?

You need the full picture before adding more. -

Are you close to the concessional cap?

Don’t assume you have unlimited room. -

Could Division 293 tax affect you?

Higher-income earners should check this before increasing contributions. -

Have you reviewed insurance and any income-linked arrangements?

Policy definitions and lending calculations don’t always line up with your assumptions.

A quick self-check won’t replace advice, but it does reveal whether salary sacrifice belongs in your plan now, later, or not at all.

How to Get Started and When to Seek Advice

If salary sacrifice still looks sensible after that checklist, the first steps are straightforward.

The practical setup steps

-

Ask payroll or HR whether your employer offers it

Most employers that support salary sacrifice already have a standard process and forms. -

Confirm what can be packaged

Typically, that means super. In some workplaces, novated leasing is also available. -

Choose an amount that fits your actual budget

Start with a figure you can sustain, not the highest number that looks good on a calculator. -

Check what your employer is already paying into super

This matters before you add extra concessional contributions. -

Review the decision after a few pay cycles

If cash flow feels tighter than expected, adjust early rather than forcing it.

When advice becomes important

Salary sacrifice is easy to set up. That’s exactly why people can underestimate the consequences.

Advice matters when the decision touches multiple goals at once. Buying a home soon, managing debt, trying to catch up on super, navigating higher-income tax issues, reviewing insurance, or weighing a novated lease against other uses of cash all call for proper modelling.

One option is to speak with an adviser who can place salary sacrifice inside a broader plan rather than treating it as a standalone tax tactic. Wealth Collective helps clients work through those trade-offs across super, debt reduction, insurance, investment strategy, and retirement planning so the decision fits the whole household balance sheet.

The value of advice here isn’t complexity for its own sake. It’s avoiding a situation where a smart tax move undermines something more important.

For some people, salary sacrifice is absolutely worth it. For others, the better answer is to wait, reduce the amount, or direct surplus cash somewhere else first. The difference usually comes down to timing, structure, and what you need your money to do next.

If you want clarity on whether salary sacrifice fits your wider plan, book a conversation with Wealth Collective. A short initial call can help you weigh the tax upside against cash flow, borrowing power, super caps, and your next major financial goal.