Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Tax time often lands with the same punch. You earn well, you work hard, then your return or PAYG summary reminds you how much of your income never stayed in your hands.

Many individuals react ineffectively. They look for one-off deductions in June, ask a mate what they claimed, or hope their accountant can magically “find more.” That’s not tax planning. That’s cleanup.

If you’re asking how can you reduce taxable income, the answer is simpler and more strategic than one might expect. You reduce it by directing money into the right structures, claiming what the ATO allows, and making investment and business decisions with tax consequences in mind before the financial year ends.

That’s how we approach it in Perth and Dunsborough. Good tax planning isn’t about chasing loopholes. It’s about using the rules properly so more of your money goes toward retirement, debt reduction, investing, and protecting your family instead of disappearing unnecessarily.

Your Guide to Smarter Tax Planning

A common scenario goes like this. A Perth executive gets a pay rise, lands a bonus, and assumes they’re moving ahead quickly. Then tax time arrives and the extra income has pushed more of their earnings into a higher marginal bracket. They’ve earned more, but they don’t feel much richer.

The fix usually isn’t some exotic strategy. It’s tightening the basics and integrating them properly. Super contributions. Valid deductions. Investment structuring. Business concessions where they apply. The issue isn’t lack of options. It’s that these options are used in isolation.

Young professionals often focus only on take-home pay. Pre-retirees often focus only on super balances. Business owners often focus only on year-end tax. That fragmented approach leaves money on the table.

Good tax planning should improve two things at once. Your current tax position and your long-term wealth position.

That’s the lens you should use. If a strategy cuts tax but weakens cash flow, creates poor debt, or locks you into a bad investment, it’s not smart planning. If it legally lowers taxable income while building assets and improving flexibility, it’s worth serious attention.

The best results usually come from joining the moving parts together:

- Income strategy that manages salary, bonuses, and business profits properly

- Super strategy that reduces tax now and boosts retirement capital

- Investment strategy that considers deductions, CGT, and timing

- Protection strategy that keeps setbacks from wrecking the plan

That’s where most Australians need help. Not because the ideas are impossible, but because the execution matters.

Use Superannuation to Lower Your Tax Bill

A Perth engineer gets a pay rise, picks up a bonus, and watches more of their income disappear to tax. The cleanest fix is often super. Done properly, it lowers taxable income now and strengthens the asset that will do the heavy lifting later.

Why concessional contributions matter

Concessional contributions are one of the few tax strategies that improve today’s tax position and tomorrow’s retirement balance at the same time. For the 2025-26 financial year, the concessional contributions cap is $30,000, and those contributions are generally taxed at 15% inside super instead of your personal marginal rate, according to the ATO’s super contributions caps, limits and tax rules.

If you’re on a higher marginal rate, that gap is meaningful. Redirecting income into super can cut the tax drag on earnings you were unlikely to spend anyway. That is why this strategy sits early in our Wealth Collective process, especially in Guided Growth for young professionals and in Retirement Roadmap for pre-retirees who need to build retirement capital efficiently.

Two ways to contribute before tax

You have two main options.

-

Salary sacrifice through your employer

Part of your pre-tax salary goes straight into super. That reduces assessable income during the year and removes the temptation to spend the cash first. If you want the mechanics explained clearly, start with how salary sacrifice super works. -

Personal deductible contributions

You contribute from your own bank account, then claim a deduction if you complete the notice of intent process correctly and your fund acknowledges it in time. This suits business owners, contractors, and employees with uneven cash flow who want more control late in the financial year.

For self-employed clients, this often pairs well with broader business tax planning. If that’s your situation, this guide to self-employed tax deductions is a useful companion read.

Match the strategy to your stage of life

Young professionals usually need structure more than complexity. If your income is rising fast and lifestyle costs keep expanding to match it, regular salary sacrifice is usually the right move. It builds the habit, trims taxable income, and keeps your long-term plan progressing without relying on perfect discipline.

Pre-retirees need a different approach. The tax saving still matters, but the bigger issue is contribution timing, cash reserves, and how super fits with your retirement date, debt position, and access to capital. Pushing too much into super too quickly can create pressure outside super, which defeats the purpose.

That’s why we do not treat super as a standalone tax trick. We fit it into the full plan. Income. Debt. Investments. Retirement timing. Cash flow.

What good super planning actually looks like

A senior mining executive in Perth might receive salary, bonuses, and incentive payments at different times through the year. A fixed salary sacrifice arrangement can reduce tax on core income, while a personal deductible contribution later in the year can top up the strategy once total income is clearer.

A dual-income couple in Dunsborough might use the higher earner’s cash flow to make deductible contributions while preserving flexibility in the household budget. The tax result matters, but so does keeping enough liquidity for school fees, mortgage repayments, and emergencies.

Those details matter more than people think.

Common mistakes that cost people money

Super is simple in concept. Execution is where people come unstuck.

| Issue | What it means |

|---|---|

| Ignoring the cap | Going over the concessional cap can create avoidable tax consequences and admin |

| Waiting until late June | Processing delays can mean the contribution misses the financial year |

| Using super without a cash flow plan | The tax benefit looks good on paper but creates pressure in day-to-day finances |

| Separating tax strategy from retirement strategy | You miss the real value, which is lower tax now and a stronger future balance |

My view is straightforward. If you’re earning solid income and not reviewing your concessional contributions every year, you are probably paying more tax than necessary. The right super strategy does not just reduce this year’s bill. It builds wealth in a way that fits the rest of your financial life.

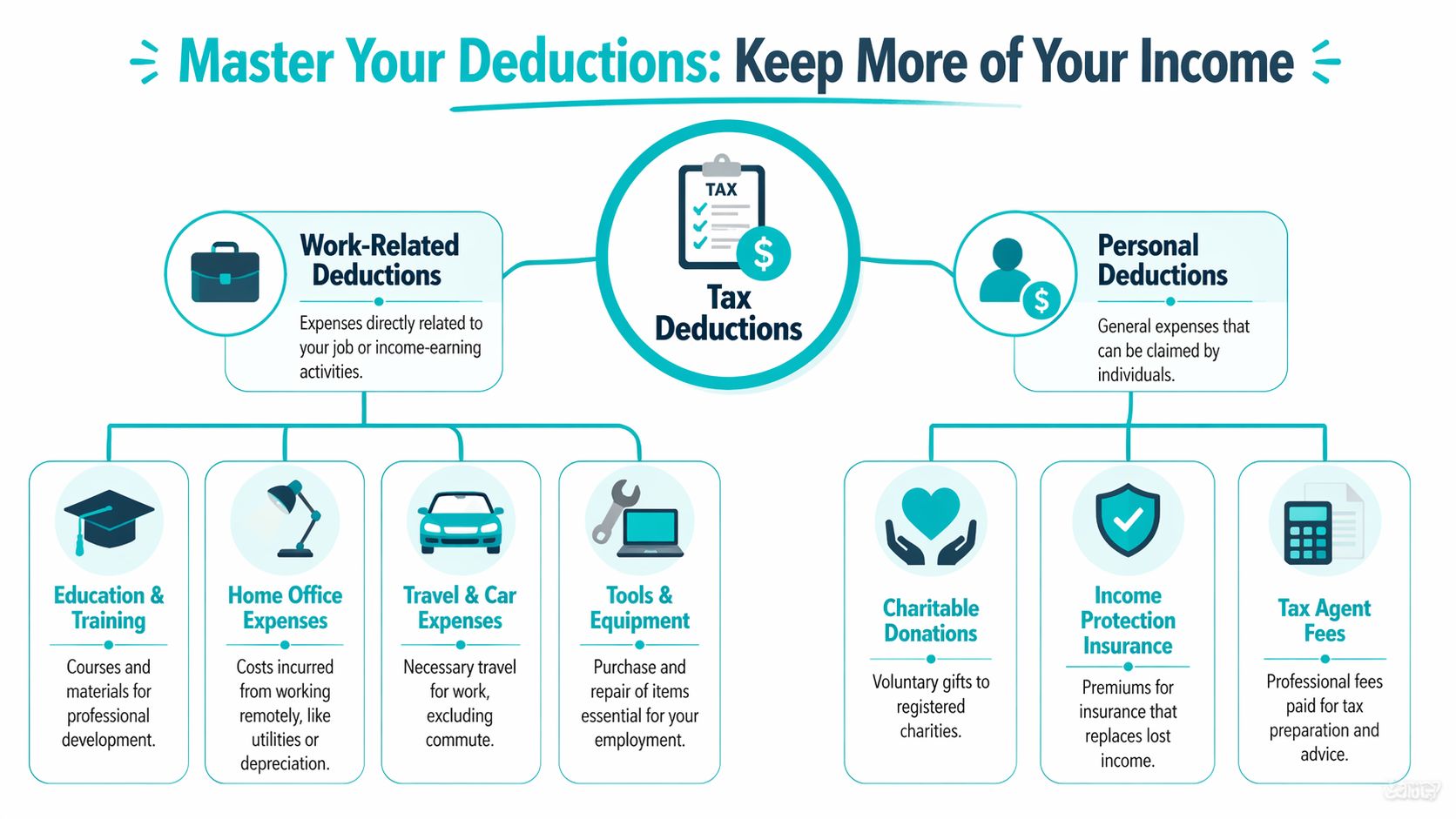

Master Your Deductions to Keep More of Your Income

A West Perth professional on a strong salary can still hand over too much tax because their deductions are scattered across bank statements, email receipts, and half-finished notes on their phone. The problem usually is not a lack of deductible expenses. It is a lack of structure.

That is why we do not treat deductions as a once-a-year scramble at Wealth Collective. We build them into the client’s broader plan, alongside cash flow, super, debt, insurance, and investing. For a young professional in our Guided Growth process, that often means setting up clean record-keeping and claiming the right work-related costs. For a pre-retiree in a Retirement Roadmap, it means tightening every legitimate claim while protecting the lifestyle and asset base they have spent years building.

Start with deductions that match how you actually earn

In 2022-23, 14.6 million taxpayers claimed $24.6 billion in work-related deductions, averaging $1,680 per claimant, according to the ATO’s Taxation Statistics 2022-23.

Deductions are common. Sloppy claims are common too.

The right approach is simple. Match your claims to your current role and keep evidence as you go. For salaried employees and professionals, the categories that usually deserve attention are:

- Home office costs if you work from home and keep the required records

- Self-education expenses where the study directly supports your current job

- Professional memberships and subscriptions connected to your role

- Tools, equipment, and other work expenses you paid for yourself to earn income

- Tax advice and eligible insurance-related costs where the rules clearly allow a claim

Home office claims are straightforward if your records are not a mess

Home office deductions trip people up because they assume regular work from home automatically creates a valid claim. It does not. The ATO expects records.

Under the fixed rate method, the rate is 70 cents per hour from 1 July 2022. If you worked 1,000 hours from home over the year, the deduction would be $700. The same ATO data reinforces the bigger point. Home office claims are legitimate, but only if you can show the hours and the work connection.

Keep a running log. Do not try to rebuild a year of working-from-home hours in late June from memory.

The deductions people miss are usually ordinary, not exotic

Missed claims often sit in plain sight. Registration fees, annual licences, subscriptions, union fees, small equipment purchases, and tax agent fees get overlooked because they are paid at different times and stored in different places.

That is why I want clients reviewing deductions by category, not by whatever receipt happens to surface at tax time.

Employment and professional costs

Start with the expenses tied directly to your role. If you changed employers, picked up extra responsibility, or moved into hybrid work, your deductible costs may have changed too. Review them properly.

Education tied to current income

The ATO draws a hard line here. If your course maintains or improves the skills you use in your current job, the expense may be deductible. If the study is aimed at getting you into a different occupation, the answer is often no.

That distinction matters for ambitious young professionals. Plenty of study feels career-related. The tax treatment depends on whether it supports the income you earn now.

Insurance and advice costs

Some financial costs are deductible in the right structure. Income protection is the example many people ask about first. If you want the rules explained clearly, start with this guide to income protection insurance tax deductibility.

For sole traders and side-hustle operators, clean separation between business and personal expenses matters even more. If that is your situation, this guide to self-employed tax deductions is a practical checklist.

Use a simple filter before you claim anything

Good deduction strategy is disciplined. It is not creative.

| Check | Why it matters |

|---|---|

| You paid for it yourself | Reimbursed expenses are generally not deductible |

| It directly relates to earning your income | Personal spending does not become deductible because you wrote a note on the receipt |

| You kept records | Weak evidence creates weak claims |

| You can explain the connection clearly | If the work link is vague, the claim is vulnerable |

For pre-retirees, this discipline protects against expensive mistakes at a stage where every dollar counts. For younger clients, it creates habits that make future tax planning cleaner and far more effective.

People rarely miss out because the tax law is too hard. They miss out because their financial life is disorganised. Fix that, and deductions stop being a guessing game and start becoming part of a smart long-term plan.

Implement Tax-Efficient Investment Strategies

A Perth couple on strong incomes buys an investment property in June because they want a tax deduction before 30 June. Six months later, the cash flow is tight, the loan structure is wrong, and the tax saving is nowhere near enough to justify the stress.

That mistake is common. Tax should shape your investment decisions, but it should never drive them on its own.

At Wealth Collective, we build tax planning into the full advice process. Asset choice, ownership, debt, cash flow, and exit timing all need to work together. That is how you reduce tax without damaging long-term wealth.

Property can help, but only if it fits the plan

Negative gearing is a tax outcome, not an investment strategy. If deductible costs exceed rental income, the loss may reduce your taxable income. That can be useful for high-income professionals, especially younger clients in our Guided Growth process who are still building assets and can absorb short-term holding costs.

The problem is simple. Plenty of investors buy poor property because they are chasing a deduction.

A deduction only reduces the cost of a loss. You still need a quality asset, a manageable loan, and a clear reason for owning it. If the property relies on aggressive rent assumptions or future growth to survive, the tax benefit will not save the decision.

Holding an asset for more than 12 months can also improve the capital gains tax result. Timing matters, especially if you are planning a sale around a bonus year, parental leave, retirement, or a business transition.

Shares and funds often give you more control

Listed investments usually offer cleaner tax management than property because you control what you sell and when you sell it. For pre-retirees working through a Retirement Roadmap, that flexibility can be extremely valuable. You can realise gains gradually, use capital losses more deliberately, and avoid being forced into one large taxable event.

That control also helps younger professionals who want to invest consistently without locking up all their cash flow in one asset.

Tax treatment should never be the only reason to prefer shares over property. But liquidity, diversification, and sale timing often make listed investments easier to manage inside a broader financial plan.

Focus on the three decisions that change the result

Before you buy anything, get these settings right.

-

Ownership structure

The same asset can produce very different tax outcomes depending on whether it is held personally, jointly, or through another structure. This decision affects tax now, tax on sale, estate planning, and access to income later. -

Debt structure

Interest deductibility depends on how the borrowing is set up and what the borrowed money is used for. If you are carrying a home loan and building investments at the same time, this guide on how debt recycling works shows how to improve the structure without guessing. -

Sale timing

Selling in the wrong financial year can create a larger tax bill than necessary. A well-timed sale can preserve concessions, improve cash flow, and keep you in control of your marginal tax rate.

Use tax strategy at portfolio level

The right question is not whether property or shares are “better for tax.” The right question is whether your full portfolio is doing its job.

For one client, that may mean a property with strong long-term fundamentals, concessional super contributions, and a disciplined loan strategy. For another, it may mean a lower-maintenance portfolio of ETFs and managed funds with selective realisation of gains over time. Business owners may also have separate tax planning opportunities through their companies.

Good tax planning connects the pieces. It does not treat each asset as a separate decision.

If you are investing mainly because someone told you it is “good for tax,” reconsider the move. The Wealth Collective approach is stricter than that. We start with your goals, pressure-test cash flow, choose the right structure, and then use the tax rules to improve the outcome. That is how smart investors keep more of what they earn and build wealth with fewer expensive mistakes.

Use Powerful Tax Concessions for Your Business

A business sale can look outstanding on paper and still leave you with a disappointing result after tax. I see this regularly with Perth business owners who spent years building value, then made one late structuring decision that cut their after-tax proceeds.

Business tax planning needs to sit inside the bigger plan. At Wealth Collective, we do not treat concessions as isolated wins. We tie them to cash flow, super, entity structure, exit timing, and what happens after the sale. For a younger founder in Guided Growth, that may mean keeping more capital inside the right structure to reinvest. For a pre-retiree in our Retirement Roadmap, it often means turning a business exit into tax-effective retirement funding.

Small business CGT concessions can materially change your outcome

Many eligible owners fail to use the full range of concessions available under the ATO’s overview of small business entity concessions. The problem is rarely the value of the rules. The problem is leaving the work too late.

The small business CGT concessions can reduce or eliminate tax on a sale if you meet the conditions. In the right case, the retirement exemption can also support a super contribution strategy. That is where tax planning becomes genuine wealth planning. You are not just reducing tax on a transaction. You are improving the funding for the next stage of life.

This matters most when the sale is close. By then, poor records, the wrong entity, or assets that fail the active asset test can limit what is available.

Ask the right questions before any deal is signed

The sale price matters. The after-tax amount matters more.

Before a transaction moves too far, get clear answers on these points:

- whether the asset and business structure meet the concession rules

- whether the timing of the sale works for your personal tax position

- whether sale proceeds should be directed into super under the relevant rules

- whether your accountant, lawyer, and adviser are working from the same plan

If those conversations start after contracts are drafted, you are already behind.

Business owners need more than a year-end tax mindset

CGT is only one part of the picture. Equipment purchases, profit retention, trust distributions, and how you pay yourself all affect the final outcome.

The point is straightforward. Good business tax planning is built into how you operate, grow, and prepare for exit. That is the Wealth Collective process. We connect the tax rules to your broader financial life so the business supports your long-term wealth, not just this year’s tax return.

Gain the Expert Edge with Smart Financial Planning

A Perth professional on a strong salary can claim a few deductions and still overpay tax for years. A business owner can run profits through a company and still create a Division 7A problem that lands on their personal return. The difference is not effort. It is having a plan that connects tax decisions to the rest of your financial life.

That is the standard I expect clients to work to.

Know the line between smart planning and bad tax advice

Legal tax planning uses the rules properly. Illegal tax avoidance relies on arrangements with little real substance and a tax outcome that does not match the commercial reality.

You should be able to explain any strategy in plain English. If your adviser cannot explain how it works, what records are required, what the ATO will expect to see, and how the strategy fits your wider goals, do not proceed.

Tax savings are only useful when they stand up to scrutiny and improve your position after tax, after risk, and after cash flow pressure.

Complex structures need active oversight

Division 7A catches plenty of business owners because they blur the line between company money and personal money. The ATO’s guidance on Division 7A loans makes the point clearly. If a company loan is not documented and managed correctly, it can be treated as a deemed dividend.

That result is expensive. It can increase personal tax, reduce flexibility, and create a mess that should have been prevented well before year end.

Pre-retirees with private companies need to be especially careful here. A poorly handled loan can disrupt retirement contribution plans, investment funding, and the timing of drawing income from the business.

The best tax strategy is built into the financial plan

This is the gap in a lot of tax advice. You get a tactic, but no framework.

At Wealth Collective, we build tax planning into the broader advice process because each decision affects something else. Extra super contributions affect cash flow. Debt recycling changes deductibility and investment risk. Trust distributions affect family tax outcomes, borrowing capacity, and long-term wealth transfer. None of these should be handled in isolation.

For young professionals in Guided Growth, the focus is often on using super, investment structure, and debt strategy together so early tax savings turn into long-term compounding.

For pre-retirees in Retirement Roadmap, the focus shifts. We look at contribution timing, pension strategy, asset ownership, and the tax position of both partners so the next decade is planned properly, not patched together one June at a time.

Do not chase deductions for their own sake

A deductible expense is still an expense. Giving money away, buying something you do not need, or locking cash into the wrong structure just to reduce taxable income is poor planning.

Use a simple filter:

- Does this strategy improve my after-tax position?

- Does it support my cash flow over the next 12 months?

- Does it fit my retirement, investment, or business goals?

- Can I defend it with proper records?

If the answer is no, skip it.

The clients who get better results usually do the same few things well. They plan early. They keep clean records. They make tax decisions in the context of super, investing, debt, insurance, and retirement, not as isolated transactions.

That is how you reduce tax properly and build wealth at the same time.

Build Your Wildly Successful Financial Life

Reducing taxable income is not the finish line. It’s one part of building a stronger financial life.

Used properly, the right strategies can do several jobs at once. Super contributions can lower tax while building retirement capital. Deductions can stop you paying tax on valid income-earning costs. Investment planning can improve after-tax returns. Business concessions can protect the value you’ve spent years creating.

The advantage comes when those pieces work together. That’s when tax planning stops feeling reactive and starts becoming part of a deliberate wealth plan.

If you’re serious about answering how can you reduce taxable income, don’t settle for random tips at tax time. Get clear on what applies to your situation, what needs action before 30 June, and what fits your bigger goals around retirement, debt, investing, and family security.

A good financial life shouldn’t feel messy or mysterious. It should feel organised, practical, and pointed in the right direction.

If you want clarity on which tax strategies suit your situation, book an initial call with Wealth Collective. A short conversation can help you identify the most useful opportunities across super, deductions, investments, and business planning, then decide what to act on next.