Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You’re probably in one of two places right now. You’ve started looking at homes around Perth or Dunsborough and felt your stomach drop when you saw the asking prices, or you’ve been “saving for a deposit” for a while but the money keeps getting pulled into life, travel, rent increases, weddings, or just expensive weekends.

That’s normal. It’s also fixable.

The best way to save for a house in Western Australia isn’t to rely on motivation, cut coffee, or hope property prices pause long enough for you to catch up. It’s to build a proper savings system around the WA market, your borrowing capacity, and the incentives most buyers either miss or use badly. If you do that well, home ownership stops being a vague goal and becomes a project with numbers, dates, and clear decisions.

Your Starting Point Laying the Foundation for Your House Deposit

You spot a place in Innaloo listed in a range that feels possible. Then you add the deposit, stamp duty, legal fees, and moving costs, and the numbers stop feeling casual. That is the moment to get specific.

If you’re buying in WA, your starting point is the local market. Perth and Dunsborough behave differently from the eastern states, and generic saving advice misses the details that change your timeline, especially WA stamp duty concessions and suburb-by-suburb price gaps.

Start with the property, not the savings account

Set your target property range first. Then calculate the cash you need.

Plenty of buyers start with, “How much can I save each month?” That approach is too loose. A deposit goal only works when it matches the kind of property you plan to buy, the suburb you want, and what a lender is likely to approve based on your income and debts.

A practical guide used by many buyers is the 5x income rule of thumb. It is not a lending promise, but it gives you a fast reality check before you waste a year saving for the wrong number. For an extra sense check, use a practical tool like this first-time homebuyer affordability guide.

My recommendation is simple. Pick a price bracket, then build your deposit plan around that bracket.

Practical rule: Set a buying range before you set a savings target. Buyers who reverse that order usually save the wrong amount, either too little to act or so much that they delay a purchase they could have made earlier.

Stop treating 20 per cent as the only acceptable deposit

A 20 per cent deposit is strong. It can reduce risk, improve loan options, and help you avoid Lenders Mortgage Insurance.

It is not the only workable path.

In WA, the better question is whether buying earlier with a smaller deposit puts you in a stronger position once you factor in local purchase costs, state concessions, and the pace of the market you want to enter. A buyer aiming for a Perth apartment has a very different savings task from someone chasing a family home in the northern suburbs or a property in Dunsborough.

Use these questions to frame the decision properly:

| Question | Why it matters |

|---|---|

| What suburb or region am I targeting? | Different WA markets create very different deposit targets and timelines. |

| Am I trying to avoid LMI, or buy sooner? | Both can work. You need to choose deliberately. |

| What purchase costs apply in WA? | Stamp duty concessions and thresholds can materially reduce the cash you need upfront. |

| How stable is my income? | Reliable PAYG income gives you more room to buy earlier. Variable income usually calls for a larger buffer. |

Give the plan a deadline

A deposit goal without a date stays vague for too long.

You need three numbers:

- Your target property range

- Your estimated cash required, including deposit and upfront costs

- Your monthly surplus available for saving

Once those numbers are clear, the goal stops floating around in your head. It becomes a timeline.

If you’re still deciding whether to buy soon or keep renting while you build a stronger position, read this local rent versus buy guide for WA property decisions. It gives you a WA-specific frame instead of generic commentary that ignores Perth conditions.

Get clear on the two things that decide whether your plan holds

First, know your borrowing position. There is no value in chasing a price point that does not line up with lender assessment.

Second, know your actual cash flow. If your spending swings all over the place, your deposit plan will keep getting reset.

The buyers who get into the market are rarely the ones making dramatic short-term sacrifices. They are the ones who chose a realistic WA target early, accounted for costs properly, used the incentives available to them, and stuck to the plan.

Build Your Savings Engine With Smart Budgeting and Automation

It’s Tuesday, payday hit overnight, and by Friday you’ve already spent part of the money that was supposed to go toward your deposit. That’s how Perth buyers drift for years.

A deposit plan works when the system does the hard part for you. Set it up once. Let it run every payday.

Use the Australian 50 30 20 split properly

Start with a simple structure. The 50/30/20 rule gives you one. The MoneySmart budget planner is a practical reference point for setting those limits and seeing where your money is going: ASIC’s MoneySmart budget planner.

For a house deposit, I’d use it as a base, then tighten it.

- Needs: Rent, utilities, groceries, transport, insurance, HECS or HELP, and minimum debt repayments

- Wants: Eating out, subscriptions, weekends away, shopping, gifts, sport, entertainment

- Savings and debt: Deposit savings, emergency cash, and extra debt repayments

If you want to buy in Perth or Dunsborough within the next few years, your wants category cannot stay bloated. Perth is still more affordable than Sydney or Melbourne, but that does not make sloppy spending harmless. Every extra $150 a week that leaks into meals out, Ubers, and subscriptions is money that could be building your deposit or reducing the loan size you’ll need later.

Clear expensive debt first

High-interest debt drags your plan backwards.

If you’re carrying a credit card balance or personal loan at a high rate, attack that before you congratulate yourself on saving for a deposit. The most efficient method is the avalanche approach. Pay the minimum on every debt, then direct every spare dollar to the highest interest rate first. Consumer guidance from NerdWallet’s explanation of the debt avalanche method outlines why this approach cuts interest costs faster than spreading your effort around.

Here’s the practical point. A buyer trying to save for a home in WA needs momentum. Expensive debt kills it because interest keeps taking a slice of the cash that should be building your deposit.

High-interest debt sabotages deposit saving. Every month you carry it, more of your income goes to the bank instead of your future home.

Automate the flow on payday

Do not save what is left at month end. There is rarely much left.

Move the money as soon as your income lands. A clean setup looks like this:

- Income lands in your main account

- Bills account is funded

- Deposit transfer goes out automatically

- Extra debt repayment goes out

- Your weekly spending amount stays in the everyday account

That separation matters. If your deposit account sits in the same place as your card spend, it becomes too easy to raid for Bali flights, furniture, or a long weekend down south.

Apps can help with visibility and habit-building. Some tools can help Australians save effortlessly by flagging spending leaks and automating round-ups or transfers. Use them if they make your system easier to follow. Just do not confuse the app with the plan.

Build a routine that catches problems early

Buyers who reach their deposit target usually have a boring money routine. That’s a good thing.

A ten-minute weekly review is enough:

| Weekly check | What to look for |

|---|---|

| Fixed costs | Did any direct debits increase? |

| Variable spending | Are takeaways, drinks, or convenience spending creeping up? |

| Debt progress | Is your extra cash still hitting the highest-rate debt first? |

| Deposit transfer | Did the automatic transfer happen on time? |

| Upcoming costs | Is there a bill or event this month that needs to be planned for now? |

Buyers stay on track not with a dramatic reset every three months, but with regular course correction before a bad month becomes a bad year.

Give each dollar a clear job

If you’re renting in Perth, paying HECS, trying to keep a social life, and saving for a home at the same time, vague budgeting falls apart fast. You need separate buckets.

Your core buckets should look like this:

- Deposit fund: Left alone until purchase

- Emergency reserve: Kept separate so one surprise expense does not wipe out your progress

- Annual costs: Rego, insurance, gifts, work costs, medical bills

- Lifestyle spending: Deliberate and capped

That structure becomes even more important in WA because your savings plan needs to line up with how you’ll buy. A first home buyer aiming for an entry-level Perth apartment will have a different timeline and cash target from a couple aiming for a house in Dunsborough, where values and holding costs are higher. Good budgeting is not generic. It should match the local market you’re targeting.

If you want a practical framework for setting up those buckets and managing the flow each month, this cash flow management approach gives a useful overview.

What disciplined budgeting actually looks like

It looks ordinary. That’s why it works.

For a motivated young professional in WA, it usually means:

- fewer impulse weekends away

- fewer food delivery defaults

- less subscription waste

- more planned social spending

- a fixed transfer into house savings every payday

You do not need to strip all enjoyment out of life. You do need to stop funding a lifestyle that delays the home you say you want. The best deposit plans are repetitive, automated, and a bit boring. That’s exactly the point.

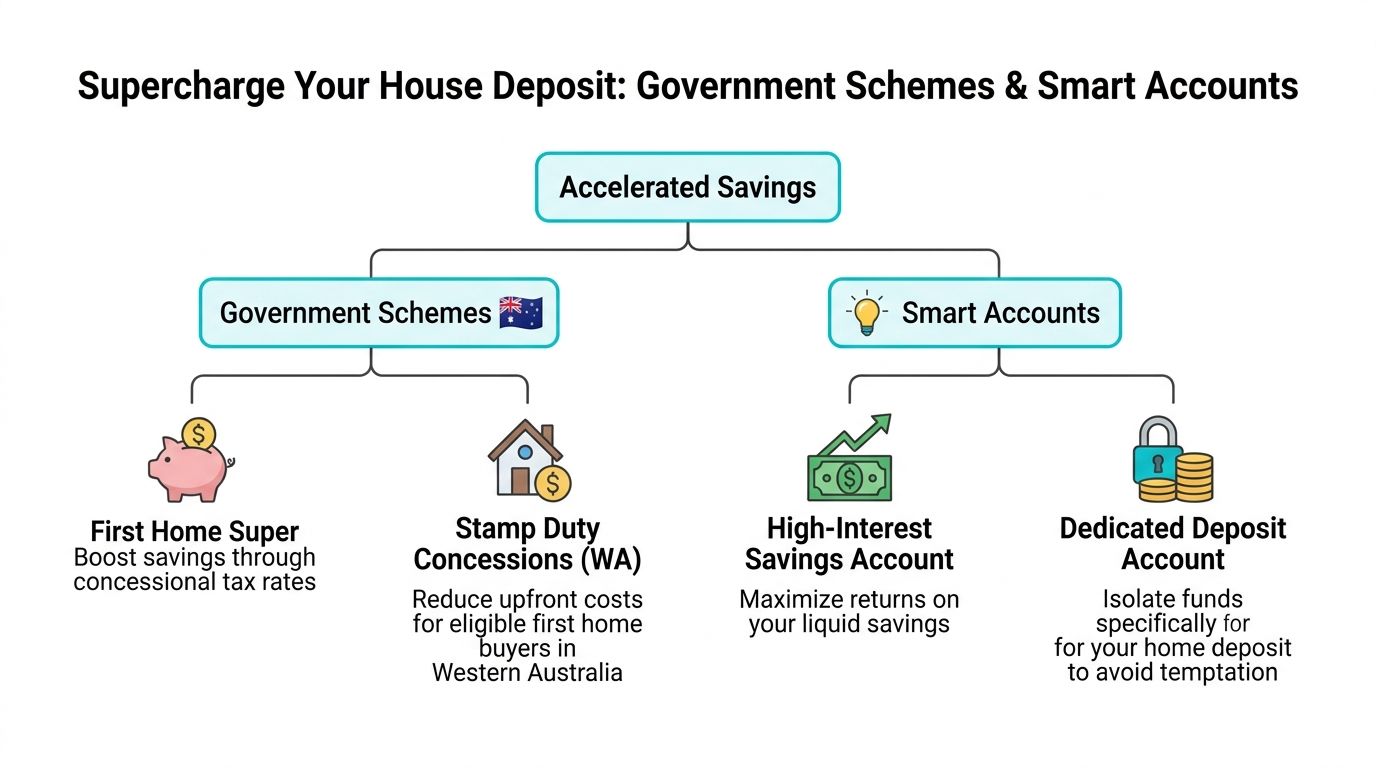

Supercharge Your Savings With Government Schemes and Smart Accounts

You can do everything right with budgeting and still take longer than necessary to buy if you ignore the rules that apply in WA.

A Perth buyer chasing a first apartment in the low to mid-$500,000s needs more than discipline. They need a structure that cuts tax, protects cash, and reduces upfront costs. That is where WA-specific planning beats generic national advice.

Use the First Home Super Saver Scheme properly

The First Home Super Saver Scheme is one of the best tools available for first home buyers who still have a year or two before purchase.

The ATO explains that eligible buyers can apply to release voluntary super contributions, along with associated earnings, under the First Home Super Saver Scheme rules. Used properly, this lets you build part of your deposit through a more tax-efficient path than saving from after-tax pay alone.

For a motivated WA professional on a decent salary, the practical move is usually simple. Start salary sacrificing early. Keep it consistent. Know your contribution caps. Apply for release before you sign a contract, not after you fall in love with a property in Mount Lawley or Scarborough.

Timing matters here. A rushed FHSSS setup creates admin stress at exactly the wrong moment.

Why FHSSS suits Perth buyers

Perth is still more accessible than Sydney or Melbourne, but that does not mean the deposit task is easy. Entry prices have moved, rents are high, and many buyers are trying to save while living a fairly normal life.

FHSSS helps because it improves how part of your savings is built. You are not relying only on whatever is left in your transaction account at month-end. You are using the super system on purpose.

Keep the approach clean:

- make voluntary contributions as part of your payroll setup

- track how much is eligible for release

- check the process with your accountant or adviser before you start house hunting

- avoid treating FHSSS as a last-minute form submission

Buyers who set this up early usually have a smoother path.

WA stamp duty concessions deserve more attention

This is the part too many buyers in WA miss.

RevenueWA sets out the first home owner rate of duty, including thresholds for full and partial duty relief. That concession can materially reduce the cash you need at settlement, which is exactly why it should be part of your savings target from day one.

If you are buying in Perth, this can be the difference between stretching for extra cash and getting the deal done comfortably. If you are buying in a higher-priced market like Dunsborough, the thresholds matter even more because they affect whether the concession is available at all.

Do not treat stamp duty as an afterthought. Build your target around the likely duty position on the exact price range you are considering.

The strongest approach is to stack the tools

WA buyers get the best result when they combine the right tools instead of relying on one account and good intentions.

| Lever | What it does |

|---|---|

| FHSSS | Improves the tax efficiency of saving part of your deposit through super. |

| WA stamp duty concession | Lowers upfront purchase costs if you meet the eligibility rules and property thresholds. |

| Dedicated deposit account | Keeps accessible cash separate so your deposit does not get mixed with spending money. |

That combination works well for a Perth buyer saving for an apartment and for a couple aiming at a house in a pricier pocket of the South West. The amounts change. The structure should not.

Where to hold the rest of your cash

Not every deposit dollar belongs in super. You still need accessible money for the part of the deposit outside FHSSS, plus costs like inspections, conveyancing, and moving.

Use a separate account for that cash. Keep it visible. Keep it boring. Keep it away from everyday spending. If you want a cleaner setup for separating purchase funds from your normal banking, this guide to a cash management account for structured savings is a useful starting point.

That separation matters more than people think. A deposit account should not be absorbing dinners out, Bali flights, or car repairs.

Common mistakes that slow buyers down

I see the same errors repeatedly:

- Starting FHSSS too late: payroll changes and contribution timing need lead time

- Ignoring contribution caps: one bad assumption can create tax problems

- Forgetting the release process: sort the admin before making an offer

- Using one account for everything: that invites spending leakage

- Guessing the WA duty outcome: check the concession rules against your actual price range

A strong savings plan is not just about reaching a number. It is about arriving at settlement with the right money in the right place, under the right structure, without scrambling in the final week.

Advanced Strategies for High-Income Earners and Partners

Once your income rises, the game changes. You usually don’t have a savings problem anymore. You have a structure problem.

High earners, dual-income couples, and business owners often waste time using basic savings tactics long after they’ve outgrown them. At that point, the focus should shift to efficiency, liquidity, and decision quality.

Offset accounts are powerful when used properly

For high-income earners in WA, the offset account is one of the most practical tools available once you’re close to buying or already structuring finance.

The verified data states that following the RBA’s late 2025 rate cuts, variable mortgage rates in WA dropped to about 5.9%, making offset accounts superior to term deposits averaging 4.2% p.a. It also states that a $100,000 balance can save about $4,500 in annual interest compared with earning taxable interest in a savings account, and that only 15% of under-40s use them, according to this offset account comparison.

That matters because offset returns are effectively tied to your mortgage rate and are generally tax-effective in a way ordinary savings interest is not.

Who should prioritise an offset

An offset strategy tends to suit people who value flexibility and already have or are about to have mortgage debt.

It’s especially useful for:

- Dual-income professionals who can build cash quickly and want liquidity

- Small business owners with uneven income patterns

- Executives and higher-rate taxpayers who don’t love earning taxable interest in a regular savings account

- Pre-retirees balancing access to cash with broader planning needs

For these households, an offset often beats chasing slightly better-looking advertised savings rates that don’t hold up after tax or when access matters.

Keep cash where it reduces debt and stays available. That combination is hard to beat.

Be careful with short-term investing for a deposit

I take a firm view. If your buying horizon is short, don’t get cute with your deposit.

Using ETFs, LICs, or other growth assets for a house deposit can work if your purchase timing is flexible and your risk tolerance is real, not imagined. But plenty of buyers say they’re comfortable with volatility until the market drops right when they want to make an offer.

A short decision framework helps:

| If this sounds like you | Better home for your deposit |

|---|---|

| Buying soon and need certainty | Cash, structured savings, or offset-style liquidity |

| Buying timing is flexible | A limited growth allocation may be reasonable, but only if you can delay purchase |

| You’ll panic if values fall | Stay out of growth assets for deposit money |

| You have variable income | Prioritise liquidity and control |

If the money has a job in the near term, protect it.

Buying with a partner needs structure, not just optimism

Buying with a partner can be excellent for borrowing power and deposit speed, but shared income doesn’t automatically mean shared financial discipline.

Before you buy together, get clarity on:

- Who contributes what

- How bills are handled before and after purchase

- What happens if one person wants out

- Whether you’ll run joint savings or separate accounts with a common target

- How existing debts affect the plan

This matters just as much for couples as it does for friends or siblings buying together. The emotional side of a home purchase gets plenty of attention. The legal and cash flow mechanics often get ignored until there’s friction.

For dual-income buyers, the strongest setup is usually simple. Shared target, agreed transfers, visible tracking, and a documented understanding of who’s responsible for what.

A Real-World Example A Perth Couple’s Journey to a $130,000 Deposit

Saturday morning in Perth. One couple is at a home open in Mount Hawthorn, doing the maths in their heads and hoping they are closer than they feel. They earn good money, around $160,000 combined, and want to buy a $650,000 home. Their deposit target is $130,000. The income is there. The problem is structure.

What they do first

They get specific.

That means choosing a suburb range, a price ceiling, and a purchase window. A buyer looking at apartments in East Perth needs a different savings plan from a couple aiming for a house in Dunsborough. Broad goals produce slow progress. Clear targets produce decisions.

They also check WA first home buyer concessions early. In Western Australia, transfer duty concessions can make a meaningful difference for eligible buyers, and that changes how much cash they need to bring to settlement. The point is simple. If you are buying in WA, you do not wait until you have found a property to work out whether the state can reduce your upfront costs. You check at the start through the WA first home owner rate of duty page.

How they organise the cash flow

They stop relying on good intentions and build a system.

Their pay goes into one main account. Fixed costs are carved out straight away. The house deposit transfer happens automatically on payday. Daily spending sits in a separate account with a hard cap. That one change usually tells you the truth about whether you are saving or just planning to save.

They set one more rule. Bonuses, tax refunds, and extra income go to the deposit unless there is a real emergency. That rule matters because lump sums are where many professional couples lose months of progress.

Where the acceleration comes from

Their savings rate improves once they use the right tools, not just more willpower.

Each partner uses the FHSSS if it fits their situation, which improves the tax treatment of part of their deposit strategy. They also keep some money accessible in cash so they are not forced to unwind a plan at the wrong time. If they buy well and keep a cash buffer after settlement, an offset account can become the next priority because it cuts interest while keeping their money available.

This is how a Perth-specific plan beats generic advice. It combines state concessions, super strategy, and practical cash management instead of treating the deposit as one big savings bucket.

Why this couple gets there faster

Plenty of dual-income households on similar money stay stuck for one reason. Their income is strong, but their process is loose.

This couple avoids the usual traps:

- inconsistent transfers

- deposit money mixed with everyday spending

- no early check on WA concessions

- no plan for bonuses or irregular income

- no coordination between two incomes

They treat the deposit like a project with deadlines, rules, and visible numbers. That is why they build momentum.

The bigger lesson

A motivated Perth couple can get to a serious deposit faster than they expect. The path is realistic if the target matches the local market and the strategy matches WA rules.

Homeownership does not become achievable because you want it badly enough. It becomes achievable when your cash flow, account structure, and incentives are all pointed at the same outcome.

Your Next Step From Blueprint to Personalised Plan

At this point, the pattern should be clear.

The best way to save for a house is not one trick. It’s a sequence. Set a realistic WA-specific target. Build a budget that reflects your purchase goal. Automate the savings. Use the FHSSS properly if it fits. Check WA concessions early. Use account structure that protects your progress.

That’s the blueprint.

The harder part is making it fit your situation. That’s where people often get stuck. Maybe your income is strong but irregular. Maybe you’re juggling HECS, bonuses, business income, or a partner with different money habits. Maybe you’re trying to save for a home without neglecting super, insurance, or longer-term wealth building.

Those are the moments when generic content stops being enough.

You’ll probably benefit from personal advice if any of these sound familiar:

- Your income isn’t straightforward: contractor, business owner, executive bonuses, or multiple income sources

- You want to combine goals: house deposit, debt reduction, super optimisation, and investment planning

- You’re buying with a partner: and want the structure clean before the property search gets serious

- You’ve got good income but poor visibility: money comes in, but it doesn’t seem to accumulate the way it should

- You want to avoid expensive mistakes: especially around timing, account structure, and WA incentives

This is also where a structured advice process is useful. Within the broader market, one option is working with an adviser that covers cash flow management, debt reduction, superannuation strategy, and home-buying preparation in one plan. For example, Wealth Collective works with Perth and Dunsborough clients across those areas, which is relevant when the house deposit goal sits alongside other financial priorities.

You do not need more scattered tips. You need your numbers organised into one coherent strategy.

If you’re serious about buying, book the conversation. A good first call should tell you very quickly whether your target is realistic, which savings levers are worth using, and what needs fixing before you start making offers.

If you want a clearer path to buying your home in WA, book an initial call with Wealth Collective. It’s a practical way to turn a general savings plan into a personalised strategy that fits your income, goals, and timeline.