Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You’ve probably landed here because something important is on the horizon. A mortgage refinance. A first home purchase. A business loan. A better rate on existing debt. Or maybe you’ve been knocked back for credit and you’re trying to work out what went wrong.

The good news is that your credit score isn’t random, and it isn’t permanent. If you take the right actions in the right order, you can improve it.

If you want the short version of how to improve your credit score australia, here it is. Check your reports, fix anything wrong, pay down the right debts first, and build positive history without taking on pointless new liabilities. Don’t waste time doing this backwards.

Demystifying Your Australian Credit Score

Your credit score is a number built from the information in your credit report. In Australia, the main credit reporting bodies are Equifax, Experian, and illion. Lenders use that report and score to help decide whether you’re a safe borrower.

That’s why a credit score matters far beyond borrowing. It affects how easily you can refinance, whether a lender wants extra documents, and how much scrutiny your application gets. A stronger file gives you more options. A weak one forces you onto the back foot.

What sits inside your report

Under Australia’s Expanded Credit Reporting, your file can include both negative and positive information. That means lenders aren’t only looking for mistakes or defaults. They’re also looking at how you manage current accounts over time.

A report can include things like:

- Personal details such as your name, date of birth, and address history

- Credit accounts including credit cards, personal loans, car finance, and mortgages

- Repayment behaviour on accounts that report under CCR

- Credit enquiries from applications you’ve made

- Negative listings such as defaults or other adverse events where applicable

That last part matters. A lot of people think their score is only damaged by “big” events. In reality, the report tells a broader story about how consistently you handle credit.

Your score is not a moral judgment. It’s a record. Records can be checked, cleaned up, and improved.

Why clarity beats anxiety

Most clients I speak with are more stressed by uncertainty than by the score itself. They don’t know what lenders can see. They don’t know what’s hurting them. They don’t know which action will move the needle fastest.

Once you replace guesswork with a proper review, things become manageable. That’s also where day-to-day money habits start to matter. Better spending control, cleaner direct debits, and fewer avoidable missed payments all support a healthier file. If cash flow is the weak link, this practical guide to cash flow management is worth your time.

If you’re interested in the connection between financial wellbeing and credit habits, I also recommend this piece on Workplace financial wellness on credit. It’s useful because it frames credit as part of overall financial stability, not just loan approval.

The key point is simple. Stop treating your score like a mystery. Treat it like a financial metric you can influence through deliberate action.

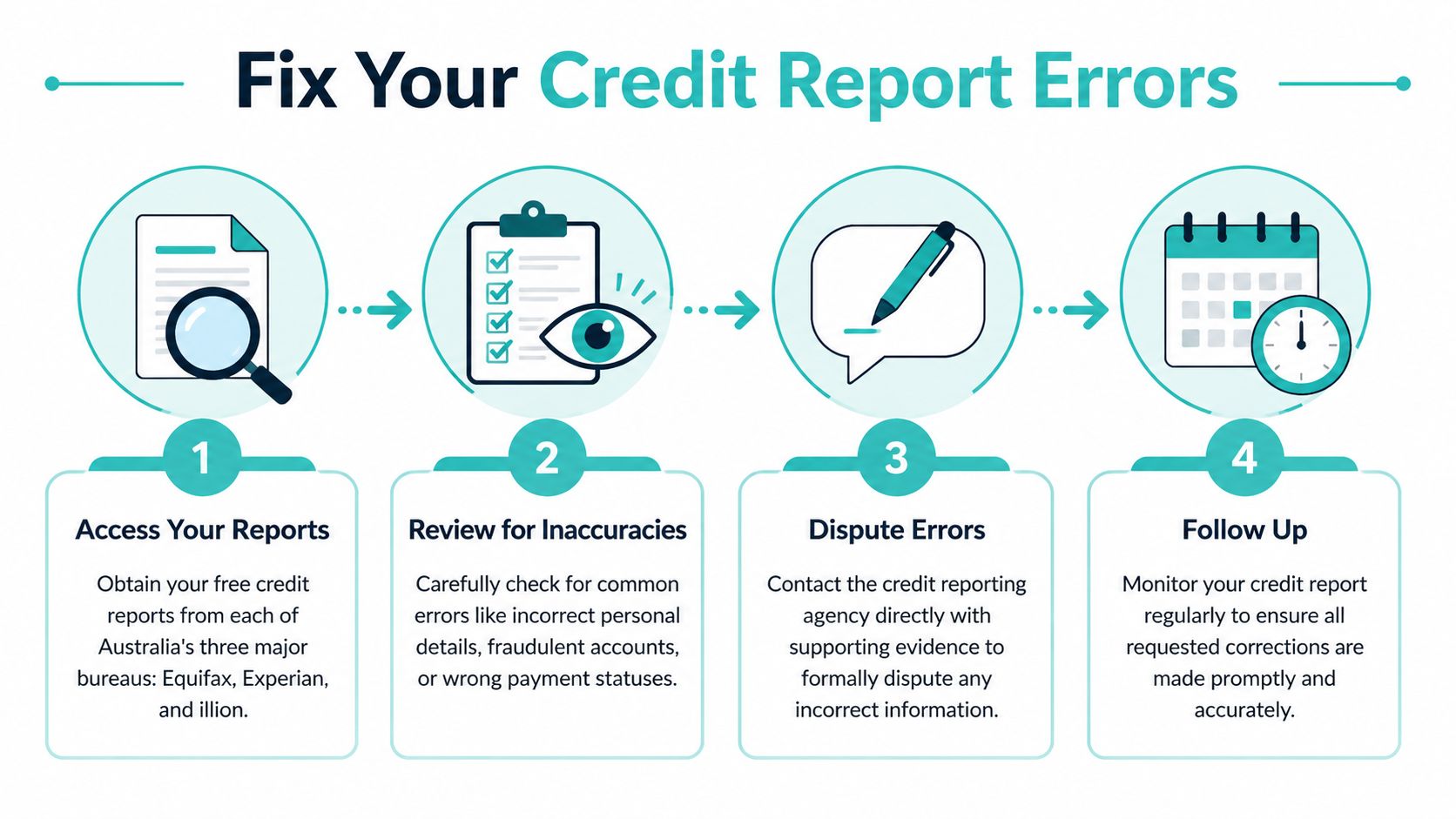

Your First Move Find and Fix Report Errors

Start here, before you pay extra on debt or apply for anything new.

If your credit file is wrong, you can spend months doing the right things and still get judged on bad data. I see this with Perth clients all the time. A missed update after a refinance, a default that should never have been listed, or an enquiry that does not belong to them. For migrants, young families, and anyone juggling a move, a new job, or a growing household, these admin errors can slow down bigger goals like a first home, a better loan, or an investment plan.

Check all three credit reports and dispute anything inaccurate. In Australia, you can access a free report every three months from each major bureau. As noted earlier, professional credit repair providers report that removing incorrect negative listings can lead to meaningful score improvements and relatively quick dispute outcomes in the right cases.

What to review line by line

Go through each report carefully. Side by side is best.

| Check Area | What to Look For | Action if Incorrect |

|---|---|---|

| Personal details | Wrong name spelling, date of birth, address, employer details | Contact the bureau and request correction with ID documents |

| Credit accounts | Accounts you don’t recognise, duplicated loans, closed accounts still shown as active | Dispute with the bureau and provide supporting records |

| Repayment history | Late payment markers that don’t match your records | Ask the provider to verify the entry and challenge it if unsupported |

| Defaults | Defaults listed in error, outdated, or not properly supported | Lodge a formal dispute and request investigation |

| Credit enquiries | Applications you didn’t make or repeated enquiries from one event | Raise it immediately, especially if fraud is possible |

| Account status | Incorrect credit limits or wrong open and close dates | Provide statements or lender correspondence to correct the record |

High-Impact Errors to Prioritise

Some mistakes are minor. Others can cost you years.

Defaults, repayment history errors, and enquiry issues deserve immediate attention. A wrong default can affect borrowing power long after the original problem should have been fixed. Repeated enquiries can make a lender think you are scrambling for credit. Late payment markers can drag down an otherwise solid file.

Credit providers and bureaus have to verify disputed information. If they cannot support the listing, it should be corrected or removed. That is why a precise dispute works better than an emotional complaint.

Practical rule: challenge each incorrect item separately, state exactly what is wrong, and attach documents that prove your case.

How to dispute properly

Use a simple process and keep records from day one.

-

Get all three reports

Check Equifax, Experian, and illion. Errors do not always appear across all three. -

Highlight every item that needs proof

Pull statements, loan contracts, payout letters, settlement confirmations, and email trails. -

Write to the bureau or credit provider

Explain what is wrong, why it is wrong, and what correction you want. -

Track every response

Save emails, complaint reference numbers, screenshots, and dates. -

Check the update yourself

Never assume it was fixed properly. Confirm the change on the report.

If your file is complicated, treat it like a project, not a quick admin task. A clean report gives every other strategy a fair chance to work. Once the errors are removed, you can make real progress with a repayment plan that improves cash flow and supports your wider wealth goals. Our guide on how to pay off debt faster without wrecking your budget is the right next read if you want to tighten the rest of the picture.

Prioritise Your Debts for Maximum Score Impact

Once your report is clean, turn to the debts you control right now.

Two repayment methods are commonly known. The snowball method starts with the smallest balance first. The avalanche method starts with the highest-interest debt first. If your main goal is motivation, snowball has merit. If your goal is stronger financial efficiency and a cleaner credit profile, I prefer avalanche.

Why? Because the debts charging the highest interest are often the same debts creating the most pressure on your monthly cash flow. They’re also frequently revolving debts, which tend to signal financial strain when left high for too long.

Snowball versus avalanche

Here’s the clean comparison.

| Method | Best for | Main drawback |

|---|---|---|

| Snowball | People who need quick psychological wins from clearing smaller balances | It can leave expensive debt hanging around longer |

| Avalanche | People who want to reduce interest pressure and improve financial efficiency | It requires discipline because the first debt may take longer to clear |

In practice, I see dual-income households around Perth make the same mistake again and again. They clear a small store card, feel productive, but leave a high-rate credit card untouched because the balance looks intimidating. That keeps repayments tight and limits flexibility.

A WA family example

Take a household with a car loan, a personal loan, and credit card debt. They’re paying everything on time, but they’ve got no breathing room. School costs, insurance, and everyday living keep eating up surplus cash.

If they use snowball, they might wipe out the smallest balance first. That feels good, but the high-cost card still chews through cash every month.

If they use avalanche, they throw every spare dollar at the highest-cost debt while keeping minimums on the others. That usually frees cash faster once the expensive balance comes down. More breathing room means a lower chance of missed payments, less need to lean on credit again, and a cleaner path forward.

If you’re serious about improving your score, don’t just ask which debt is smallest. Ask which debt is keeping you financially stuck.

What to do this month

Keep it simple and ruthless:

- List every debt with the balance, interest rate, minimum repayment, and whether it’s revolving or fixed.

- Stop adding to old balances where possible. Paying down a card while still using it heavily is slow and frustrating.

- Target the highest-cost debt first while staying current on everything else.

- Remove temptation by lowering available access to unused credit where appropriate, especially if spending habits are part of the problem.

- Review refinancing options carefully once your position improves, not as a shortcut before habits change.

If you need a practical framework, this guide on how to pay off debt faster gives a solid starting point.

The big mistake is treating all debt as equal. It isn’t. Some debt is just sitting there. Some debt is actively damaging your flexibility every month. Hit the second category first.

Build a Positive Credit History Responsibly

A stronger credit file is built in the ordinary weeks, not in one big reset. The clients I see in Perth improve their scores by making credit look predictable, controlled, and easy to manage over time.

That matters even more if you are early in your financial life. Young families trying to buy in outer-metro Perth, migrants building an Australian record from scratch, and professionals planning their next property move all face the same issue. Lenders want proof of steady behaviour.

Build history with boring habits

The right approach is simple:

- Pay on time, every time, especially for credit cards, loans, and phone plans

- Keep card balances low rather than running close to the limit each month

- Apply for credit only when there is a real purpose

- Keep older, well-managed accounts open if they still suit your budget and spending habits

- Set up direct debits or reminders so a busy month does not turn into a missed payment

Boring works.

A credit score improves when your report shows calm, repeatable behaviour. Opening accounts just to appear active is poor strategy. So is chasing a perfect “credit mix” with products you do not need.

Be careful with BNPL

Buy now, pay later can look harmless because the repayments are small. Lenders do not always see it that way. Frequent BNPL use can suggest cash flow pressure, especially if you are also carrying card debt or applying for a home loan.

Use BNPL only for planned purchases you could afford without it. If you rely on it for groceries, school costs, or day-to-day gaps, fix the cash flow problem first. As noted earlier from Oracle Advisory Group’s article on enhancing your credit score, BNPL use and rent reporting can both affect how some lenders assess your file, especially for borrowers with a thin history.

If your file is thin, make regular payments count

This is a common WA problem. A migrant can have strong income, stable rent payments, and sensible savings, yet still look unproven to an Australian lender. The same applies to younger borrowers who have avoided debt but now want to qualify for a mortgage.

If you rent and have little local credit history, ask whether your repayments can be reported through services such as SNAP or Equifax RentCheck. That can help turn a payment you already make into something visible on your file.

For a broader consumer-focused read, this guide to a better credit score covers the basics well.

If you already own property, your credit profile should also support your wider plan, not just your next application. Reviewing what mortgage refinancing is can help you connect day-to-day credit behaviour with lower lending costs, better structure, and a stronger long-term wealth plan.

Your Path to a Better Score and a Richer Life

A stronger credit score is useful. But it’s not the finish line.

The point is what that stronger score lets you do. Refinance expensive debt. Put yourself in a better position for a mortgage. Reduce financial friction. Create room to invest, save, or plan for retirement with less stress.

The sequence is straightforward. Review your reports. Repair anything inaccurate. Repay debts in an order that improves control, not just motivation. Rebuild with responsible credit behaviour over time.

That approach matters whether you’re a young family in Perth trying to clean up consumer debt, a migrant building a local financial footprint, or someone heading toward retirement who wants lending options sorted before the next chapter. Better credit supports better decisions across your whole financial life.

There’s also a line you shouldn’t cross. If your situation is severe, don’t assume extreme solutions will “reset” everything neatly. Bankruptcy has long-term consequences, and anyone considering that path should first understand the trade-offs.

Clean credit gives you leverage. Leverage gives you choices. Choices are what build financial freedom.

If you’ve been trying to improve your score without a system, start with the basics above and act on them this week. Credit improvement rewards action, not intention.

If you want help connecting your credit score to a bigger financial plan, book a complimentary introductory call with Wealth Collective. It’s a simple way to get clear on your next move, whether that’s reducing debt, improving borrowing options, or building a stronger long-term strategy.