Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

A lot of people only think about income risk after something goes wrong.

You wake up with a serious back injury. Or your doctor tells you to stop work while you deal with treatment and recovery. Your mortgage doesn’t pause. Groceries still need buying. School fees, rent, car repayments, subscriptions, rates, and power bills keep arriving as if nothing has changed.

That’s the gap salary continuance insurance is designed to fill.

For many Australians, income is the engine room of the whole financial plan. It funds daily life now and future goals later. If that income stops for a period because illness or injury keeps you from working, the pressure can spread quickly across savings, debt, superannuation, and family decisions. Salary continuance insurance gives you a structured way to soften that blow.

People often get stuck because the language sounds technical. They hear terms like waiting period, benefit period, inside super, condition of release, own occupation, and underwriting, then put the issue aside for another day. That’s understandable. Insurance wording can feel like reading a manual for something you hope you’ll never need.

This guide is for that exact moment. Not when you want marketing spin, but when you want a clear explanation from someone who deals with these questions every day.

Your Income Is Your Greatest Asset Protect It

Take a common situation. A couple is managing their household well. One income covers most of the fixed bills. The other helps with savings, family spending, and getting ahead. Then one partner gets sick and can’t work for months.

The first few weeks often feel manageable. There may be sick leave. Maybe there’s a bit of cash in the offset account. But significant stress usually appears when people realise the interruption may last longer than they hoped.

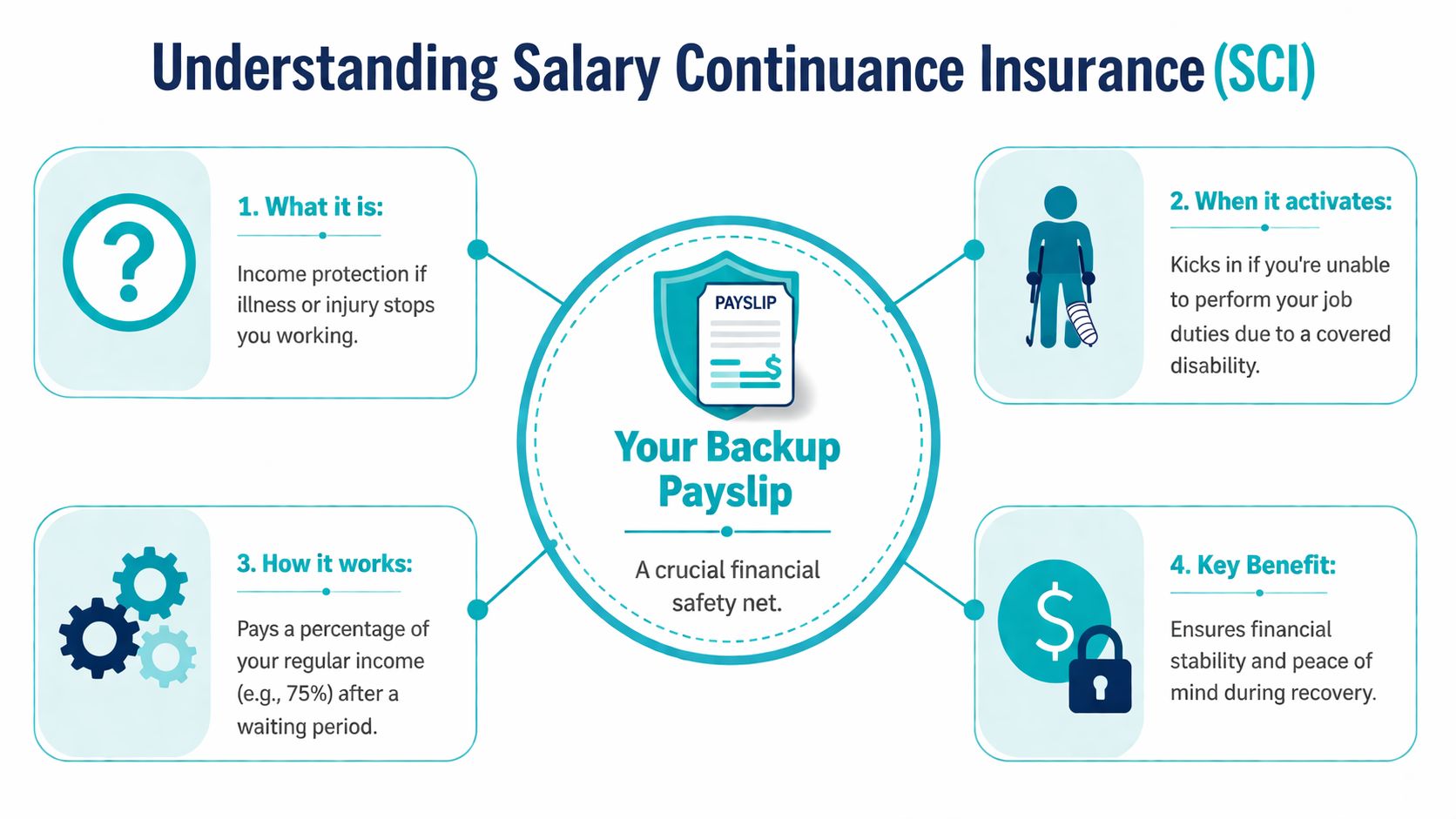

That’s where salary continuance insurance matters. In plain language, it acts like a backup payslip when a health issue stops you from earning your normal wage. It’s not there to make you better off. It’s there to help stop a temporary or extended health problem from turning into a financial crisis.

Why this matters more than most people think

Many individuals insure assets they can see. Their home. Their car. Their contents.

But your income often funds everything else. If your earnings disappeared for a stretch, the knock-on effects could include:

- Using savings too quickly for everyday expenses rather than planned goals

- Falling behind on debt repayments and creating avoidable pressure

- Reducing super contributions because cash flow has become tight

- Relying on family support when you’d rather stay independent

Your house may be your biggest expense, but your income is usually your biggest financial asset because it pays for everything else.

A practical way to think about it

Think of your financial life like a household built on pillars. One pillar is cash flow. If that pillar cracks, the rest of the structure starts carrying extra load. Savings get drained. Investments may need to be sold at the wrong time. Retirement planning gets pushed back.

Salary continuance insurance is one of the tools that helps support that pillar.

This isn’t only relevant for high-income earners. It matters for anyone whose lifestyle depends on regular pay coming in. If you have dependants, a mortgage, shared expenses, or long-term goals, your income probably does more heavy lifting than you realise.

What Is Salary Continuance Insurance and How Does It Work

The simplest definition is this. Salary continuance insurance is income protection cover that usually sits inside your superannuation fund. If illness or injury stops you from working, the policy may pay a regular benefit after a waiting period.

Think of it as a backup payslip linked to your super, rather than a separate standalone policy in your own name.

The core mechanics

Many Australian super funds include this type of cover for eligible members. According to NobleOak’s explanation of salary continuance insurance, it’s primarily held within superannuation funds, can cover up to 75% of pre-disability salary, commonly has benefit periods to age 65, and may offer insured percentage options of 50%, 60%, 75%, or 87% where the higher figure includes a 12% superannuation contribution benefit. The same source notes waiting periods can range from 30 days to 180 days, and eligibility often requires permanent employment of at least 15 hours per week.

Those details sound technical, but the basic flow is straightforward:

- You become unable to work because of a covered illness or injury.

- You serve the policy’s waiting period.

- If the claim is accepted, a monthly benefit is paid.

- Because the cover sits inside super, the payment generally goes to the fund first, then to you if the release rules are met.

If you want a broader plain-English primer on how disability insurance works, that resource can help frame the general idea before you drill into the super-specific rules in Australia.

Why super changes the picture

Many people get confused. They assume the insurer pays them directly, like a private health rebate or a simple refund. That’s not usually how salary continuance insurance works when held through super.

The policy is often owned through the super structure. So the money path matters. The insurer assesses the claim under the policy terms. Then the super fund has to release the benefit under the relevant rules.

That doesn’t automatically make salary continuance insurance bad or cumbersome. It just means the process has an extra layer compared with some policies held outside super.

Practical rule: If your cover is inside super, always ask two questions. What does the insurance policy require, and what does the super fund require before money can be released?

What it’s trying to do

The purpose isn’t to replace every dollar you earn. It’s to help keep your financial life functioning while you recover.

A simple example helps. If your usual salary pays your mortgage, food, utilities, insurance, and school costs, then a reduced but regular benefit can stop you from burning through savings immediately. It gives you breathing room. That breathing room is often the difference between a manageable disruption and a long-term setback.

For a broader look at the differences between cover types available in Australia, income protection insurance in Australia gives useful background on where salary continuance insurance fits.

Salary Continuance vs Income Protection and Other Covers

The biggest source of confusion isn’t what salary continuance insurance does. It’s how it compares with other insurance people already have, or think they have.

Many people use salary continuance insurance and income protection as if they mean exactly the same thing. They overlap, but they aren’t always structured the same way. Then you add TPD and life insurance to the mix, and it’s easy to see why people feel unsure.

The biggest distinction

The key difference is usually where the cover sits.

Salary continuance insurance is commonly held inside super. Standalone income protection is usually held outside super in your own name. That single difference affects acceptance, flexibility, and how benefits are paid.

According to Canstar’s guide to salary continuance insurance, eligible super fund members may receive automatic acceptance without full underwriting, and group pricing can mean premiums are often 20-30% less than individually underwritten standalone cover. The same source notes that this lower-cost structure can come with less flexibility, ties cover to ongoing super membership, and means benefits flow first to the super fund and require a condition of release to be met.

Side-by-side comparison

| Feature | Salary Continuance Insurance (Inside Super) | Standalone Income Protection (Outside Super) |

|---|---|---|

| Where it sits | Usually through your super fund | Usually owned personally outside super |

| How you join | May be offered automatically to eligible members | Often requires a separate application |

| Underwriting | Can be lighter because of group cover | Often more tailored to your personal circumstances |

| Premium style | Group pricing can make it cheaper in some cases | Can cost more, but may offer more customisation |

| Flexibility | Often more standardised | Often broader in design options |

| Benefit payment path | Usually through the super fund first | Usually paid more directly under the policy structure |

| Dependency | Linked to super fund membership | Not dependent on staying in a specific super fund |

That table isn’t a verdict. It’s a trade-off map.

Why cheaper doesn’t always mean better

Inside-super cover can be attractive because it’s simpler to start with and may cost less. That suits many people, especially early in their working life or when they want basic protection without a complex application process.

But lower cost can come with less room to tailor the policy around your occupation, your income structure, or the finer points of claim definitions. For some clients, that’s acceptable. For others, especially if they have specialised jobs or more complex finances, it may leave gaps.

If you want an outside perspective on long-term disability concepts and how legal wording can affect claims, UL Lawyers’ disability insurance guide is useful reading for understanding how definitions and policy wording shape outcomes.

How it differs from TPD and life insurance

People also confuse salary continuance insurance with TPD and life insurance. They solve different problems.

- Salary continuance insurance is generally designed to provide regular payments when illness or injury stops you from working for a period.

- TPD insurance is generally designed for permanent disability scenarios and often pays a lump sum rather than an ongoing monthly benefit.

- Life insurance usually pays a lump sum on death.

A simple analogy helps. If your financial risks were tools in a shed, salary continuance insurance is the tool for a pay interruption. TPD is for a far more serious long-term capacity loss. Life cover is there for the financial impact of death.

If you’d like a clearer picture of how these protections fit together, different life insurance types in Australia can help you place each one in the right category.

Salary continuance insurance protects cash flow. TPD usually addresses permanent loss of earning capacity. Life insurance supports those left behind.

Understanding Key Policy Features and Fine Print

Once people grasp the broad idea, the next challenge is the wording. The wording itself can make good cover and disappointing cover look similar on a super statement, even when they’re not.

The fine print matters because claims are assessed against definitions, waiting periods, exclusions, and eligibility rules. If you only remember one thing, remember this. Insurance is easiest to buy when you’re healthy, but easiest to judge when you imagine making a claim.

Waiting periods and benefit periods

A waiting period is the time you need to be off work before benefits start. A useful way to think about it is an excess, but paid in time instead of dollars.

If you have strong sick leave, a healthy emergency fund, or a partner’s income that can carry the household for a while, a longer waiting period may be manageable. If cash flow is already tight, a long waiting period can create stress before the policy even begins paying.

A benefit period is how long payments can continue if the claim remains valid. Some people only focus on the monthly amount and forget that duration matters just as much. A shorter benefit period may be enough for a straightforward recovery. A longer one matters more when the medical issue drags on or recovery becomes uncertain.

Disability definitions matter

This is one of the most important areas in any policy.

Policies use definitions to decide whether you qualify for benefits. Two phrases often come up:

- Own occupation generally focuses on whether you can do your usual job

- Any occupation generally looks at whether you can do another job suited to your background, training, or experience

That difference can be critical. A specialist professional may be unable to perform their exact role but still technically capable of doing some other form of work. The wording in the policy can shape the claim outcome.

Good insurance isn’t just about having cover. It’s about having wording that still makes sense on a bad day.

Common areas to review carefully

When you check your super statement or policy document, pay close attention to these points:

- Eligibility rules. Cover may depend on being in active employment or meeting minimum work requirements.

- Definitions of disablement. Often, misunderstandings stem from this.

- Partial disability provisions. Some policies may respond when you can return to work only in a limited capacity.

- Pre-existing condition wording. Past health issues can affect claims depending on the policy rules.

- Exclusions. Every policy has boundaries. You need to know what sits outside them.

A simple checklist for your own review

If you’re looking at your current cover, try this checklist:

- Find the waiting period and ask yourself how you’d pay the bills during that gap.

- Check the benefit period and think about whether it would support a longer recovery.

- Read the disablement definition slowly. Don’t assume you know what it means.

- Confirm how the benefit is paid and whether the super fund has extra release requirements.

- Look for exclusions and limitations that might affect your circumstances.

Most confusion comes from assuming all income-style cover works the same way. It doesn’t. The wording decides whether your policy behaves like a strong safety net or a thin one.

The Costs Tax Rules and Superannuation Impact

People usually ask three money questions about salary continuance insurance. What does it cost. Is it tax-effective. What does it do to my super.

Those questions belong together because the inside-super structure changes all three.

Why premiums move around

Premiums aren’t random. They’re shaped by factors such as your age, occupation, health profile, and the design of the cover itself. In general, more generous terms tend to cost more than narrower ones.

There’s also a broader market factor. In Marsh’s paper on the affordability of salary continuance cover, the Australian group salary continuance insurance market entered a hard phase in 2015, with standard premium increases of 20-40% across the board, and increases of up to 100% for some long-term covers to age 65 or policies with poor claims experience. The paper says this affected over 70% of Australian companies that provided this cover to employees. It also notes salary continuance insurance typically covered up to 75% of pre-disability salary.

That history matters because it reminds people of something easy to miss. Group insurance can feel stable until claims experience and insurer pricing shift.

The tax side in plain language

For cover inside super, premiums are usually funded through your super balance rather than paid personally from your bank account. That can make the cover feel less noticeable in your monthly budget, but it doesn’t make it free. The cost still comes from your money. It just comes from a different pocket.

The tax treatment also differs from personally owned cover. The fund generally handles the premium payments within the super environment, and benefit payments received by you are generally treated as assessable income. That means the structure may help with affordability, but it doesn’t remove the need to understand after-tax outcomes.

The retirement trade-off

This is the part people often skip.

Every premium paid from super is a premium not left invested for retirement. That doesn’t mean you shouldn’t hold salary continuance insurance through super. It means there’s a trade-off between current protection and future accumulation.

Here’s the practical tension:

- More cover can improve resilience if you can’t work

- More premiums from super can reduce long-term retirement savings

- Cheaper group cover may help affordability now

- Less customized design may leave gaps for some people

That’s why the right answer isn’t always “maximise cover” or “minimise cost”. The better question is whether the cover fits the rest of your financial system.

If you’re weighing whether inside-super cover aligns with your broader retirement planning, superannuation income protection considerations are worth understanding before you make changes.

Insurance inside super can be efficient, but efficiency and suitability aren’t the same thing.

Making a Claim and Real World Scenarios

A policy only proves its value when a claim is made. That’s why claims thinking is so useful when reviewing salary continuance insurance. If you can’t picture the process, it’s hard to know whether the cover will work the way you expect.

In broad terms, a claim usually starts when illness or injury prevents you from working and your likely time off extends beyond ordinary leave arrangements. At that point, timing and paperwork start to matter.

What a claim often involves

The steps vary by fund and insurer, but the process typically includes:

- Notify the insurer or super fund early. Don’t wait until you’re already under financial pressure.

- Complete claim forms carefully. Small errors can slow things down.

- Provide medical evidence from your treating doctor or specialist.

- Show your work details and income information if required under the policy.

- Stay in contact during assessment and respond quickly to requests for extra documents.

People often assume the hard part is proving they’re unwell. Sometimes the harder part is making sure the paperwork, dates, job description, and medical wording all line up properly.

Scenario one with a shorter disruption

A younger professional injures their shoulder and can’t perform the practical parts of their role for a period. They expect to recover, but not quickly enough to rely only on leave balances.

The useful role of salary continuance insurance here is simple. It helps bridge the gap between work stopping and work resuming. The person still needs to manage the waiting period first, so emergency cash remains important. But once the claim is accepted, the policy can reduce the need to raid savings or fall behind on fixed costs.

In this kind of situation, the main pressure points are usually:

- Getting forms in promptly

- Making sure the doctor describes work restrictions clearly

- Understanding whether partial return-to-work arrangements affect benefits

Scenario two with a longer illness

A pre-retiree develops a serious health condition that keeps them away from work for much longer than expected. The household isn’t just worried about current bills. They’re also worried about preserving savings and not derailing retirement plans close to the finish line.

The design details matter more. A long benefit period may become far more valuable than it looked on paper when the cover was first chosen. The person also needs to understand how the super fund release process works, because benefit timing matters when cash reserves are under strain.

Keep a file with every medical certificate, form, email, and phone note. Claims move more smoothly when your records are organised.

Practical ways to make the process easier

A smoother claim usually comes down to good preparation:

- Tell your doctor what your actual job involves. A vague medical note can create problems if your work is specialised.

- Keep copies of everything. Don’t rely on systems being perfect.

- Ask questions early. If you don’t understand the waiting period, offsets, or partial disability rules, clarify them before assumptions become mistakes.

- Track dates carefully. In claims, timing can influence both eligibility and payment flow.

Many clients feel overwhelmed because they’re dealing with health issues and administration at the same time. That’s normal. It’s another reason not to leave policy review until after a problem starts.

Is Salary Continuance Insurance Right for You?

Salary continuance insurance isn’t automatically right for everyone. But it deserves serious attention from anyone whose financial life depends on steady earnings.

If you could stop working for an extended period and comfortably cover expenses from savings without disrupting long-term plans, your need may be lower. If your household relies heavily on your salary, the need is usually much stronger.

People who should look closely at it

This cover often matters most if you fall into one or more of these groups:

- Mortgage holders who need regular cash flow to meet repayments

- Parents and couples with shared commitments where one income supports a large part of household spending

- Professionals with specialised roles whose ability to work depends on their health and capacity

- Business owners and self-employed people who may have less built-in leave protection

- Pre-retirees who can’t easily afford a major interruption close to retirement

A quick self-check

Ask yourself these questions:

| Question | Why it matters |

|---|---|

| How long could I cover expenses without income? | This shows whether your emergency buffer is strong or thin |

| Who depends on my earnings? | Dependants increase the financial impact of time off work |

| Is my current cover inside super, outside super, or both? | Structure affects flexibility and claims flow |

| Would a health event disrupt retirement plans? | Protection and long-term wealth goals need to work together |

| Do I understand my policy wording? | If not, you may not know what you actually own |

The right decision usually sits at the intersection of risk, cash flow, and long-term planning. A cheap policy that doesn’t match your needs can disappoint. No cover at all can leave a much bigger problem.

The practical conclusion

The purpose of salary continuance insurance isn’t to create complexity. It’s to protect your ability to keep your financial life intact while your health recovers.

If you already have cover through super, the next step is to check whether it’s suitable, not just whether it exists. If you don’t have cover, the question becomes whether your current savings, leave, debt levels, and family responsibilities would carry you through a prolonged interruption.

Additional jargon is unhelpful. What’s needed is clarity on three points:

- What would happen if my income stopped

- What cover do I already have

- Is that cover enough for my real life

Those answers are rarely obvious from a super statement alone.

If you want help reviewing your existing cover, comparing it with your broader financial goals, or working out whether salary continuance insurance belongs in your plan, book an initial call with Wealth Collective. A good conversation can turn a confusing policy into a clear decision.