Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You open an insurance renewal notice after work, skim a page of exclusions, loadings, limits and optional extras, and end up with a common question. “Do I have the right cover, or am I just paying for paperwork?”

That confusion is normal. Insurance language often makes a practical money decision feel like a legal exam.

The problem is that risk doesn’t wait for clarity. A bushfire, injury, lawsuit or long period off work can hit your finances whether you understand your policy or not. That’s why learning the types of risk in insurance matters. Not because you need to become an underwriter, but because you need to know what could damage your income, assets and long-term plans.

Once you understand the main risk categories, better decisions follow. You can spot where your financial life is exposed, where insurance fits, and where planning matters more than a policy.

Why Understanding Insurance Risk Is Key to Your Financial Success

A Perth professional recently described their insurance file as “something I keep meaning to deal with.” That’s common. Insurance isn’t ignored out of carelessness. It’s often neglected because it feels technical, repetitive, and disconnected from everyday life.

But insurance risk isn’t abstract. It’s the question behind a lot of your biggest financial decisions.

Risk decides what needs protection

If you’re building wealth, paying down a mortgage, growing a business or preparing for retirement, the central issue is simple. What could interrupt that progress?

For some people, the biggest threat is a loss of income after illness or disability. For others, it’s damage to a home in a high-risk area, or a liability claim that forces them to use savings to pay legal costs. The policy is just the tool. The risk is the reason the tool exists.

Practical rule: Don’t start with the product. Start with the financial damage you couldn’t comfortably absorb on your own.

That shift matters because it helps you filter out noise. You stop asking, “Should I have this policy?” and start asking, “What would happen to my family, business or retirement plan if this event occurred?”

Clarity helps you avoid two expensive mistakes

Most insurance errors fall into two camps:

- Underinsuring real risks: You protect the obvious things, but leave major gaps around income, liability or rebuilding costs.

- Overinsuring minor risks: You pay for cover that doesn’t meaningfully change your financial position if a claim happens.

Neither is efficient.

Understanding the types of risk in insurance gives you a practical framework. You can see which risks are personal, which attach to property, which arise from legal responsibility, and which influence the insurer’s pricing decisions behind the scenes. That makes it easier to ask better questions at renewal time and far easier to build a protection plan that matches your stage of life.

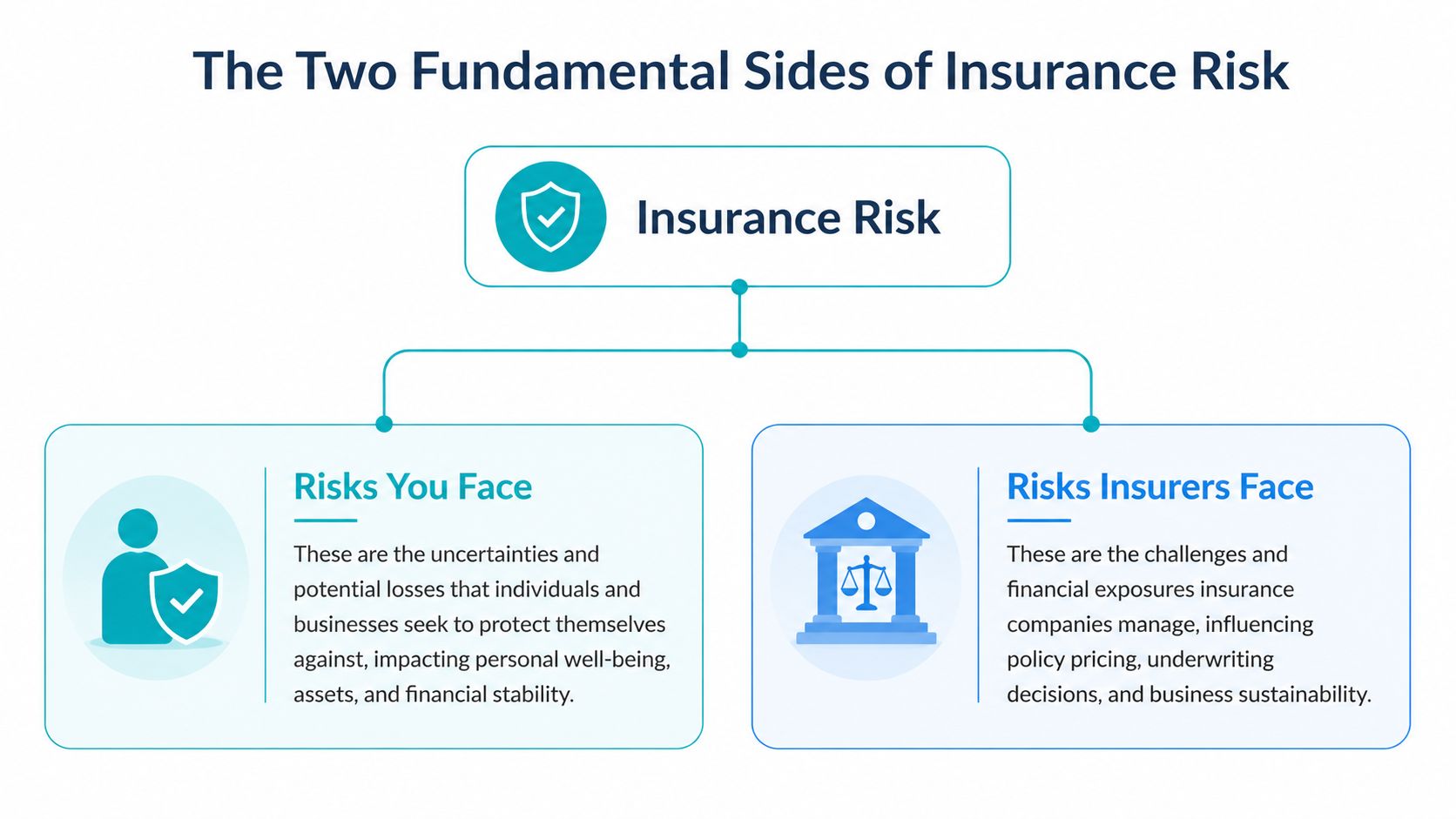

The Two Fundamental Sides of Insurance Risk

A common perception is that insurance risk means one thing. It means two different things, and mixing them up causes a lot of confusion.

On one side are the risks you face. These are the events that could hurt your finances. On the other side are the risks insurers face. These are the business risks an insurer must manage so it can price policies, pay claims and remain financially stable.

Risks you face

Think of a café customer. They’re worried about whether they’ll spill coffee on their laptop, slip on a wet floor, or lose their wallet. Those are direct losses to them.

In insurance, your main risk categories usually sit here:

- Personal risk: Your health, life, earning capacity and ability to support dependants.

- Property risk: Damage to things you own, such as your home, contents, investment property or business assets.

- Liability risk: Claims made against you because someone says you caused injury, loss or damage.

These are the risks widely understood in the context of insurance. They’re the threats to your balance sheet, cash flow and long-term plans.

Risks insurers face

Now think about the café owner. They’re looking at a different set of problems. How often do accidents happen? How much could one claim cost? What if many claims arrive at once? What if they price the menu too low to cover costs?

That’s similar to how insurers think. They manage risks such as:

- Underwriting risk: Pricing a policy too low for the likelihood of claims.

- Catastrophe risk: Facing many large claims from one major event.

- Operational risk: Problems in systems, processes or claims handling.

- Credit and investment risk: Managing reserves, reinsurance and capital responsibly.

These insurer-side risks affect your experience as a policyholder. They shape premiums, exclusions, acceptance criteria and the insurer’s willingness to cover certain exposures.

A useful rule of thumb is this. If the question is “What could financially hurt me?”, you’re looking at policyholder risk. If the question is “Why does the insurer price or restrict cover this way?”, you’re looking at insurer risk.

Why the distinction matters

This split helps explain why two policies that sound similar can behave very differently. It also explains why some covers are easy to buy while others involve more detailed medical questions, property reports or liability disclosures.

Business owners feel this most clearly. A café owner may need cover for customer injuries and stock damage, while a consultant may need cover for bad advice claims. If you want a simple primer on that distinction, this guide to compare professional and general liability is a useful companion.

Once you see both sides, the insurance system becomes easier to read. You stop seeing premiums as arbitrary and start seeing the logic behind them.

Personal and Health Risks Affecting Your Financial Future

A Perth couple can spend ten years doing everything right. They buy a home, build savings, contribute to super, and plan a family holiday. Then one partner develops a health condition and cannot work for eight months. The bills keep arriving on schedule, but the income does not.

That is how personal risk affects financial security. It rarely begins as a single dramatic loss. It usually starts as pressure on cash flow, then spreads into savings, debt, investments, and long-term plans.

Disability and illness can undo years of progress

For many Australian households, the bigger financial threat is not a one-off medical bill. It is losing earning capacity while everyday expenses continue. Mortgage repayments, rent, childcare, groceries, insurance premiums, and school costs do not pause because your health does.

A short interruption may be manageable from an emergency fund. A longer one can force harder choices. You might reduce super contributions, sell investments at the wrong time, redraw on the home loan, or rely on a partner’s income that was never meant to carry the whole household.

That is why personal insurance is best understood as a cash flow protection tool. It helps preserve the financial structure you have already built.

The main personal risks to think about

Morbidity risk

Morbidity risk is the chance that illness, injury, or a medical condition affects your ability to work and earn.

This risk often causes more strain than people expect because it does not need to be permanent to be expensive. Six months off work can be enough to disrupt debt repayments, pause savings goals, and create a gap that takes years to rebuild. Mental health conditions can also fit into this category, which catches many otherwise healthy professionals off guard.

For a mining worker in regional WA, an injury may stop physical work immediately. For a self-employed consultant in Perth, a health issue may not stop work completely, but it can reduce billable hours enough to damage income all the same. The label changes. The financial effect is similar.

Mortality risk

Mortality risk is the chance of dying earlier than planned while other people still depend on your income or unpaid work.

If you have a partner, children, business debts, or a mortgage, this becomes a capital problem for the family. Someone needs money to replace lost income, repay debt, fund future living costs, and keep longer-term goals such as education or retirement on track. A plain-English overview of different policy structures can help here. This guide to life insurance types explains how cover can be set up for different needs.

The key question is simple. If your income disappeared tomorrow, what financial obligations would remain?

Longevity risk

Longevity risk is the opposite problem. You live a long life, but your money has to last for longer than expected.

This matters in Western Australia because retirement costs are not just about day-to-day spending. Healthcare, aged care support, housing choices, and inflation can all change the picture. A pre-retiree in Dunsborough may own their home and feel secure, but a 25 to 30 year retirement can still put pressure on super and savings if drawdowns are too high early on.

Longevity risk is easy to miss because it does not arrive as a single event. It works more like a slow leak in a water tank. If withdrawals, fees, and rising costs keep draining the balance, the problem may not become obvious until there is less flexibility left.

Matching risk to your life stage

Your biggest personal risk changes as your life changes.

- Early career and young families: Your future income is often your largest asset, so protecting earning power usually deserves close attention.

- Peak earning years: Debts, dependants, and lifestyle commitments are often at their highest, which increases the impact of illness, disability, or death.

- Pre-retirement: The focus shifts toward preserving capital, managing drawdown rates, and preparing for a retirement that may last decades.

Location matters too. A family in Perth with a large mortgage has a different pressure point from a semi-retired couple in Busselton or a sole trader in the Pilbara whose income depends on staying fit enough to work. Good risk planning reflects your stage of life, your work, and your local cost realities.

For homeowners, personal risk and asset risk often overlap. If illness or injury reduces income, keeping up with repayments on the family home can become harder even if the property itself is undamaged. That is one reason it helps to review personal cover alongside home and contents insurance, rather than treating them as separate decisions.

A sound plan protects more than a policyholder. It protects your ability to keep your household running, your savings strategy intact, and your future choices open.

Protecting Your Assets from Property and Liability Risks

A storm tears part of your roof off in winter. A customer slips outside your shop the next week. Neither event has anything to do with your health or your income directly, yet both can pull money out of your household or business very quickly.

That is the practical difference between property risk and liability risk.

Property risk affects the things you own or rely on. Liability risk affects what you may have to pay if someone says your property, actions, advice or business caused harm. One threatens your assets. The other can threaten your savings, cash flow and future borrowing capacity.

In Western Australia, these risks are rarely abstract. A family in the Perth Hills may worry about bushfire exposure and rebuilding costs. A landlord in Bunbury may be more concerned about tenant damage or loss linked to a rental property. A trades business in the Pilbara may depend on vehicles, tools and a workshop staying operational. The risk changes with your postcode, your stage of life and how you earn your income.

Property risk is about replacement cost, not just ownership

Many people hear “property risk” and think only about the family home. The category is wider than that. It includes contents, holiday homes, rental properties, business premises, stock, tools, machinery and equipment.

The key question is simple. If this asset were damaged, destroyed or stolen, how would you pay to repair or replace it?

That is where underinsurance causes trouble. Market value and insurance value are not the same thing. A home may sell for one figure because of its land value and location, while the cost to rebuild it after a major loss could be very different. The same logic applies to contents and business assets. Furniture, electronics, specialist tools and fit-outs are often underestimated because people price them one item at a time instead of as a full replacement exercise.

A useful way to view property cover is as a financial reset button. You hope not to use it, but if something serious happens, it helps you get back to where you were without draining savings meant for school fees, retirement, debt reduction or business growth.

Liability risk is the legal cost of being held responsible

Liability risk works differently. The loss is not always something you own. The loss may start with an allegation.

A visitor could be injured on your property. A client could claim your advice caused financial loss. A contractor could damage someone else’s premises while working. Even if the claim is weak, legal defence costs can still be expensive.

Liability claims can cross into personal finances faster than people expect. A sole trader and their business are often closely connected in practice. A landlord may face a claim linked to property maintenance. A professional easing into consulting before retirement may assume the work is low risk because it is part-time, but one dispute can still create legal bills and settlement pressure.

Property loss usually asks, “How much would it cost to replace what I have?” Liability loss asks, “How much would it cost to defend myself and pay if I am found responsible?”

Both questions matter for long-term financial security.

A quick audit by life stage

| Client Profile | Common Property/Liability Risk | Insurance Focus |

|---|---|---|

| Young professionals and dual-income families | Damage to home or contents, accidental loss, legal exposure linked to property or lifestyle | Building and contents cover that matches current replacement costs, plus a check on any relevant personal liability protection |

| Pre-retirees and retirees | Underinsured home, holiday property exposure, landlord risk, liability linked to downsizing or side consulting | Updated sums insured, landlord cover where relevant, and liability cover suited to any ongoing business or advisory work |

| Small business owners and executives | Damage to premises, stock, equipment or vehicles, claims tied to customer injury or professional services | Commercial property cover, public liability, and professional indemnity where advice or specialist services are provided |

A sensible review starts with your balance sheet. List the assets you could not easily replace. Then list the situations where a claim against you could force you to use savings, sell investments or take on debt.

That exercise turns insurance from a generic purchase into a financial protection strategy.

How Insurer Risks Influence Your Policy and Premiums

A Perth family updates their home insurance after a renovation, then sees the renewal jump. A small business owner in Bunbury adds a new service line and gets new exclusions at the next review. In both cases, the insurer is reacting to risk on its side of the table, not just yours.

That distinction matters because your premium is not merely a price tag. It is the insurer’s estimate of how likely a claim is, how large it could be, and how that claim fits into the rest of its book in Western Australia and beyond.

Underwriting risk changes what you pay

Underwriting is the insurer’s filtering and pricing process. It works like a lender assessing a loan application. The insurer is asking, “What are the odds of loss here, and what terms make sense if we accept that risk?”

For personal cover, that can include age, occupation, smoking status, medical history, travel, and hazardous hobbies. For business cover, it may include industry, staff duties, turnover, claims history, contracts, and the specific work you perform. Small changes can shift how an insurer prices the policy or whether it adds exclusions, loadings, or extra questions.

That is why two people with the same type of cover can receive different terms.

If you want a plain-English explanation of the health assessment side of this process, this guide on what is medical underwriting is a useful starting point.

Insurers also price the risk around you

An insurer is not only assessing you as an individual policyholder. It is also managing exposure across a suburb, town, profession, or industry class.

A simple way to view this is to picture a boat, not a single passenger. Even if your seat is dry, the insurer still needs to know whether too many passengers are sitting on the same side. In insurance, that “same side” problem shows up when many policyholders in one area face the same bushfire, storm, flood, theft trend, or liability pattern at the same time.

That is why postcode can affect pricing. It also helps explain why two similar homes in different parts of WA, or two businesses with similar revenue but different activities, can attract very different premiums.

Why premiums rise even when you did not claim

This is one of the most common frustrations clients raise.

A higher premium does not automatically mean the insurer is acting unfairly. It often means one of the inputs behind the pricing has changed:

- Your personal risk changed. Health details, occupation, income, or pastimes may now look different to the insurer.

- Your business risk changed. New services, more staff, interstate work, or larger contracts can increase claim size or legal complexity.

- Your area changed. Local claim frequency, rebuilding costs, weather exposure, or crime patterns may have shifted.

- The insurer’s portfolio changed. If the insurer has too much exposure in one category, it may tighten terms even for good customers.

This is also why policy wording matters as much as premium. A cheaper policy with tighter limits or broader exclusions can leave a larger gap in your financial safety net. For income protection in particular, it helps to review what income protection does not cover before you compare policies on price alone.

The practical question to ask at review time

Start with this: what has changed since this policy was first set up?

That question gets to the heart of insurer pricing faster than arguing with the renewal notice. If your health, property, business activities, location, or replacement costs have changed, the insurer will usually adjust terms to match. Understanding that logic puts you in a stronger position to compare insurers, challenge outdated assumptions, and choose cover that still protects your financial future in WA.

Strategic Planning for Uninsurable Business and Personal Risks

A lot of people assume every serious risk can be solved with an insurance policy. It can’t.

Some risks are uninsured because a person chooses not to cover them. Others are uninsurable because standard insurance typically won’t take them on in a meaningful way. That difference matters.

What insurance usually won’t solve

For business owners, executives and professionals, some of the biggest threats sit outside normal policy design:

- Reputational damage: A policy may help with certain legal costs, but it usually won’t restore trust or lost future opportunity.

- Regulatory change: New rules can reshape profitability or business structure without triggering an insurable event.

- Strategic business risk: Expanding too fast, relying on one major client, or entering a weak market isn’t the kind of loss standard insurance was built for.

- Pandemic-style disruption or trade secret loss: These are often limited, excluded or only partially addressed depending on the policy wording.

That’s why insurance should never be your only risk strategy.

The better response is financial design

When a risk can’t be transferred to an insurer, you need a different defence. Usually that means combining cash buffers, legal structure, debt management, diversification and succession planning.

A practical approach might include:

- Building a contingency reserve: Separate from everyday savings and sized for genuine disruption.

- Reducing concentration risk: Avoiding dependence on a single income source, client or asset.

- Reviewing policy gaps carefully: Knowing where cover stops is just as important as knowing where it starts. This guide on what income protection does not cover is a useful example.

- Using advice across insurance and planning: Insurance handles transfer. Financial planning handles resilience.

For clients who need both insurance structure and broader planning, Wealth Collective provides advice across personal cover, retirement planning and strategy for broader financial resilience. That matters because some of the most important risks in your life won’t appear neatly inside one product category.

Build Your Personalised Risk Protection Plan Today

The value in understanding the types of risk in insurance is that it gives you control. You can separate the risks that threaten your income, the ones that threaten your assets, the ones that create legal exposure, and the ones no insurer will fully absorb for you.

That changes the conversation from fear to planning.

A strong plan usually does three things

- Protects cash flow: So illness, injury or death doesn’t immediately destabilise the household.

- Protects assets: So property loss or legal claims don’t force the sale of investments or retirement capital.

- Protects long-term strategy: So uninsurable risks are managed with reserves, structure and disciplined planning.

If you’re a young family, that may mean focusing on income and debt protection first. If you’re approaching retirement, it may mean placing more attention on longevity, capital preservation and the role of insurance inside a broader drawdown plan. If you run a business, it often means reviewing liability and strategic gaps together rather than treating them as separate issues.

One of the simplest ways to test whether your current setup still fits is to review what your existing policies cover in plain language. This explainer on what life insurance covers can help clarify one important piece of that picture.

You don’t need a perfect insurance strategy on day one. You do need a deliberate one. The biggest financial setbacks often come from risks people assumed were already handled.

If you want help turning this into a practical plan, book a short introductory call with Wealth Collective. It’s a simple way to clarify your biggest risks, identify gaps in cover, and decide what belongs in insurance and what belongs in broader financial planning.