Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

A tpd insurance claim usually starts at the worst possible time. Work has stopped or is about to stop. Medical appointments are piling up. Your income may have dropped, but the bills haven't. Claimants often come to this process already exhausted, then discover that insurance decisions turn on paperwork, timing, and definitions they've never had to think about before.

That's why good claims aren't built by rushing forms out the door. They're built by slowing down, checking exactly what cover exists, and preparing evidence the way an insurer will assess it. The people who do this well don't just ask, “Am I covered?” They ask, “What will the insurer need to see to approve this?”

Facing the Unexpected When Lodging a TPD Claim

One of the hardest client conversations usually starts the same way. Someone has stopped work because of a serious illness or injury, the household budget is tightening, and they are trying to work out whether insurance will step in. At that point, the pressure is not only medical. It is financial, administrative, and intensely personal.

TPD insurance, or Total and Permanent Disability insurance, is meant to provide a lump sum if your condition meets the policy definition and leaves you unlikely to return to work in the required capacity. That payment can reduce debt, fund treatment, protect the family home, or replace part of the income your household expected to rely on over many years.

What catches people off guard is the standard of proof involved.

A tpd insurance claim is assessed against policy wording, medical evidence, work history, and often the detail of what you could reasonably do in the future, not only what you cannot do today. Data from 2024 showed acceptance rates were lower than they had been in earlier years, which is a useful reminder that insurers are scrutinising claims closely. In practice, that means the outcome often turns on preparation, consistency, and whether the evidence answers the exact questions the insurer will ask.

Practical rule: Treat a TPD claim like a case you need to prove, not a form you need to submit.

That distinction affects the result. I have seen valid claims delayed because the treating doctor described the diagnosis well but did not explain work capacity in terms the policy required. I have also seen claims improve once the medical records, employment history, and policy definition were lined up properly from the start. The trade-off is simple. Rushing can feel productive, but a hurried claim often creates gaps that take months to fix.

Many policyholders also do not realise their cover sits inside super and may sit alongside other benefits that shape how the claim should be handled. If you are still working out what protection you hold, it helps to understand the broader types of life insurance cover available in Australia, because TPD is often one part of a wider insurance structure.

The strongest claims usually begin before lodgement, with a clear strategy about what the insurer will need to see and where the weak points are likely to be.

First Steps Confirming Your TPD Cover and Eligibility

Before you complete a single claim form, confirm exactly what cover you have and whether it was active when work stopped. Many claims go off course if this step is overlooked. People assume they know which fund holds the cover, or they begin a claim without understanding the policy wording that will decide the outcome.

Many Australians don't realise they hold TPD cover through superannuation, and ASIC data cited by WKB Lawyers on “secret insurance” in super shows high withdrawn claim rates in some funds because people don't understand their eligibility or policy terms before they start.

Where to look first

Start with the documents closest to the cover itself:

Your super statements

Look for insurance entries, cover amounts, premium deductions, and the insurer name. If you've changed jobs several times, check older funds too.Your myGov and ATO records

Lost or inactive super accounts can still hold insurance history, although cover may have lapsed if premiums stopped or the account became inactive.Any retail policy schedule

If you took cover through an adviser or directly with an insurer, locate the policy schedule and Product Disclosure Statement.The date you last worked

Insurers pay close attention to this. Your cover generally needs to have been in force at the relevant time, and that date often shapes the rest of the claim.

Don't rely on memory. Pull the actual documents. A claim can turn on one policy endorsement, one cancellation notice, or one definition buried deep in the wording.

If you're still unsure what TPD cover does, this guide on what total and permanent disability insurance is is a useful starting point before you compare policies.

The definition matters more than the label

Most claimants focus on the diagnosis. Insurers focus on the definition. Two people with the same medical condition can have very different claim outcomes because their policies use different tests.

Here's the comparison that matters most:

| Criteria | Own Occupation | Any Occupation |

|---|---|---|

| Core test | Whether you can return to your specific occupation | Whether you can work in any occupation suited to your education, training, or experience |

| Typical outcome standard | Usually narrower to your actual role | Usually broader and tougher to satisfy |

| Example for a surgeon | Inability to continue practising as a surgeon may be central | Insurer may ask whether the person could work in another medically related role |

| Example for a tradesperson | Focus stays on the trade they performed | Insurer may consider supervisory, training, or other related work if realistically suitable |

| Where commonly found | More often in retail cover outside super | More commonly attached to super-based policies |

| Claim strategy | Evidence must show why your own role can't be resumed | Evidence must address why alternative suitable work isn't realistic |

What eligibility really comes down to

Eligibility usually turns on a small group of practical issues:

- Active cover: Was the policy in force when you stopped work?

- Correct occupation category: Was your job classified properly when the cover was issued?

- Relevant definition: Are you being assessed under own occupation, any occupation, or another wording such as ADL?

- Medical permanence: Do your treating doctors support that the impairment is not temporary?

- Work capacity evidence: Can you show how the condition prevents a return to suitable work?

If any of those points are unclear, slow the process down and verify them before you lodge. Starting fast feels productive. Starting accurately is what usually matters.

Building Your Case with Strong Medical and Financial Evidence

Most tpd insurance claim problems aren't caused by one dramatic issue. They're caused by weak evidence spread across multiple documents. A GP certificate says one thing. A specialist report says something less definite. Employer information is vague. Tax records don't match the income claimed. The insurer then sees uncertainty where the claimant sees an obvious disability.

That's why the evidence stage deserves the most care.

Mental health claims show this clearly. Mental health has become a leading cause of TPD claims paid, yet these claims also face one of the highest decline rates at 16.9%, as outlined in Curo Financial Services' review of TPD claims statistics. In practice, these claims often succeed or fail on whether the medical material properly explains severity, duration, treatment history, and why a return to work isn't realistic.

What strong medical evidence looks like

A short doctor's note rarely carries enough weight on its own. Insurers usually want a coherent file that answers the same question from several angles.

Strong medical evidence often includes:

- Treating GP records that show the history of symptoms, treatment, time off work, referrals, and functional decline.

- Specialist reports from the clinicians most relevant to the condition, such as psychiatrists, psychologists, orthopaedic surgeons, neurologists, rheumatologists, or rehabilitation specialists.

- Hospital and imaging records where relevant, especially when they support diagnosis or progression.

- Medication history and treatment attempts showing what has been tried and with what result.

- Capacity commentary that explains practical limitations, not just diagnosis. Can you sit, concentrate, drive, lift, manage deadlines, interact with clients, or sustain attendance?

The key point is alignment. The report has to address the policy test, not just confirm you're unwell.

A diagnosis is only the starting point. The insurer wants evidence of functional loss and permanence.

For example, if the policy uses an any occupation test, your evidence should deal with more than your old role. It should address why work suited to your education, training, or experience is not realistic. If the issue is cognitive fatigue, your doctor should say how that affects reliability, decision-making, pace, and persistence. If the issue is pain, the report should explain how pain limits sitting tolerance, movement, concentration, and work attendance.

The documents insurers compare against each other

Insurers don't read each item in isolation. They compare them. That means your file should be internally consistent.

Use a working checklist like this:

| Document | Why it matters |

|---|---|

| Claim form | Sets out your account of the condition, work history, and timeline |

| Employer statement | Confirms duties, hours, income, and the date work ceased |

| Position description | Shows the real demands of the role, including physical and cognitive requirements |

| Payslips and tax returns | Supports earnings and work pattern before disability |

| Medical reports | Proves diagnosis, treatment, restrictions, and permanence |

| Super or policy schedule | Confirms cover type, insurer, and applicable definition |

A practical example helps. If a client says they could no longer manage a senior professional role because of impaired concentration, but the treating reports only discuss mood symptoms in broad terms, the file is incomplete. The better approach is to ask the treating psychiatrist or psychologist to address work function directly. How does the condition affect judgment, deadlines, meetings, phone calls, client management, and sustained focus across a normal working week?

Financial evidence is not a side issue

People often think the medical records do all the heavy lifting. They don't. Financial documents help establish what you were doing before disability and how your earning capacity has been affected.

Useful records include:

- Recent payslips

- Tax returns and notices of assessment

- Business financials, if you're self-employed

- Employment contracts

- Leave records

- Job descriptions or performance documents that show the nature of the role

For business owners and professionals, it's especially important to present a clean picture of duties. If you performed a mix of technical, managerial, and client-facing tasks, the insurer needs to understand which parts of the job mattered most and which parts the condition now prevents.

What works and what doesn't

What works: carefully selected treating reports, a clear timeline, and medical opinions that speak directly to the policy wording.

What doesn't: generic certificates, inconsistent accounts, or assuming the insurer will “figure out” how your condition affects work.

If the evidence file feels repetitive, that's often a good sign. Repetition across records creates consistency. Consistency creates credibility.

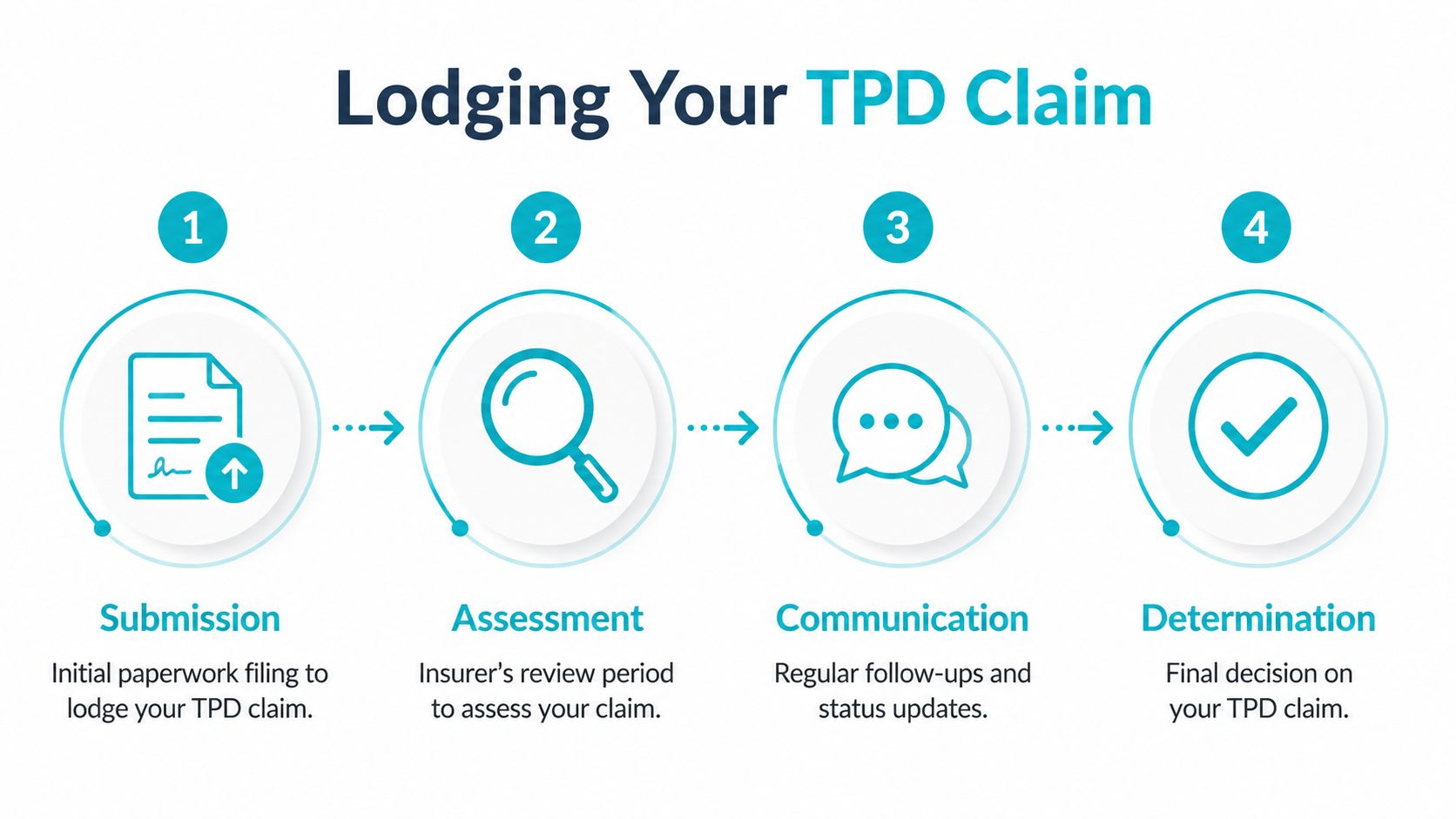

Lodging Your Claim and Managing Insurer Timelines

You submit the forms, expect movement within a few weeks, and then hear very little. That stage catches many people off guard. By the time a TPD claim reaches lodgement, the outcome often depends less on whether the condition is serious and more on whether the file is clear, consistent, and easy for the insurer and trustee to assess.

In practice, a lodged tpd insurance claim usually involves two decision-makers. The insurer assesses the medical and occupational evidence. The super fund trustee often has to approve the release of any insured benefit through super. That is one reason claims can take months rather than weeks, particularly where extra reports, employment clarification, or specialist reviews are needed.

The best claims are organised before they are submitted. I tell clients to assume that every form will be compared against medical notes, employer records, and prior statements. Small discrepancies can slow the assessment and sometimes trigger extra questions that were avoidable.

How to lodge the claim cleanly

A disciplined process helps:

Request the full claim pack early

Check whether the insurer and super fund need separate forms, certified ID, or release authorities.Prepare one master chronology first

List diagnosis dates, treatment history, changes in duties, periods of leave, and the date you last worked in your usual role. Then complete every form from that chronology.Lodge a complete file where possible

If a key specialist report is still pending, decide strategically whether to wait or submit and flag that the report will follow. There is no single rule here. Early lodgement can start the clock, but an incomplete file can also create avoidable back-and-forth.Keep a record of everything sent and received

Save emails, upload confirmations, signed forms, and attachments. If there is later a dispute about timing or missing documents, your file matters.

What the insurer is actually doing during assessment

Assessment is not just paperwork. The insurer is testing the claim against the policy definition and looking for gaps it may need to resolve before making a decision.

That often includes:

- Requests for additional treating doctor reports

- Employer questionnaires or payroll confirmation

- Independent medical examinations

- Vocational or functional assessments

- Questions about education, training, or alternative work capacity

None of those steps automatically signal a problem. They do tell you what the insurer sees as the pressure points in the claim. If the questions focus on duties, the occupational evidence may need strengthening. If they focus on treatment, the insurer may be testing permanence, compliance, or whether further recovery is possible.

Respond promptly, but with care. A quick answer that is incomplete or inconsistent can create a problem that stays on the file for the life of the claim.

Managing timelines without losing control

Waiting is part of the process, but passive waiting is risky. A better approach is to track the claim the way an adviser would. Know what is outstanding, who is responsible for it, and what happens if it is delayed.

Use a simple follow-up system:

- Set diary dates for updates so you are not relying on the insurer to contact you first

- Ask specific questions such as whether the file is waiting on a trustee review, specialist report, IME booking, or claims officer assessment

- Reply in writing where possible so there is a clear record

- Tell treating doctors the claim is active so they expect report requests and understand why work capacity needs to be addressed carefully

- Review any related cover at the same time, including superannuation income protection options, because cashflow pressure during a TPD assessment can affect the wider strategy

One practical point matters more than many claimants realise. Delays are often caused by third parties, not the insurer alone. Specialists take time to prepare reports. Employers can be slow to confirm duties. Trustees may review matters on a separate timeline. Once you know where the bottleneck is, you can decide whether to chase it yourself, have an adviser do it, or adjust expectations.

A long assessment period is frustrating, especially when work has already stopped and finances are under strain. Clients usually cope better when they treat lodgement as an active phase of the claim rather than the end of the hard work. That mindset often leads to cleaner responses, fewer contradictions, and a stronger position when the decision is finally made.

Common TPD Claim Pitfalls and How to Avoid Them

Most denied or delayed claims don't fail because the unwellness was not genuine. They fail because the file gave the insurer room to doubt the claim. Some of those issues are technical. Others are entirely avoidable.

One of the biggest is incomplete medical information, which is identified as a primary factor in an estimated 40% of initial claim rejections in Townsville Compensation Lawyers' explanation of the TPD claim process. That figure tracks with what many advisers and claim specialists see in practice. Claims often stall because the medical evidence doesn't answer the actual test in the policy.

The mistakes that cause the most damage

Here are the issues I'd watch for first.

Inconsistent timelines

If your claim form, GP records, and employer statement show different dates for when work stopped or symptoms escalated, the insurer may question the reliability of the whole file.Downplaying symptoms in treatment, then overstating them in the claim

Many people try to be stoic with doctors. That can backfire. Insurers read treatment notes closely.Using generic medical certificates

A certificate saying you're unfit for work doesn't explain permanence, functional loss, or inability to return to suitable work.Ignoring related cover

A TPD claim often sits alongside super strategy, cashflow pressure, and other insurance considerations such as superannuation income protection cover. If these pieces aren't considered together, people can make rushed decisions.Posting carelessly on social media

Photos and comments without context can be read in the worst possible light during a claim.

The better approach

A stronger method is to pressure-test the file before submission. Read every form side by side. Do the dates match? Do the treating doctors describe the same functional problems you've listed? Does the employer statement reflect what the role involved?

If a stranger read only your documents, would they understand exactly why you can't return to work under this policy definition?

That question is useful because insurers don't know your day-to-day reality. They only know what the paperwork shows.

A simple pre-lodgement check

Before lodging, review these points:

| Check | What to confirm |

|---|---|

| Dates | Same date last worked across all forms and reports |

| Duties | Employer statement matches the real role and its demands |

| Medical narrative | Reports explain severity, treatment, prognosis, and work capacity |

| Policy fit | Evidence addresses the actual wording, not a generic idea of disability |

| Public profile | Social media and public activity won't create unnecessary questions |

Claims are easier to defend when they're built carefully at the start. Fixing avoidable mistakes later is usually slower, more expensive, and more stressful.

Responding to a Denied Claim and Getting Expert Help

A denied claim feels final when the letter arrives. In many cases, it isn't. A rejection often means the insurer says the evidence, wording, or process didn't support approval at that point. That's different from saying no claim could ever succeed.

Start by reading the reasons carefully. Was the issue medical evidence, policy definition, work capacity, disclosure history, or something procedural? The next step depends on the reason given.

Your first move after a refusal

Generally, the practical path is:

Request the full basis of the decision

Ask for the documents or reasons relied on if they aren't already clear.Review the evidence gaps

Sometimes the answer is a better specialist report. Sometimes it's correcting the insurer's understanding of your occupation or work history.Use the insurer's internal dispute process

A structured review can succeed where the original claim failed, especially if the file is strengthened properly.Escalate externally if needed

If the dispute remains unresolved, AFCA may be available depending on the circumstances.

Why outside perspectives help

People often assume appeals are just about arguing harder. They're usually about arguing better. The strongest challenges focus on the exact reason for refusal and answer it with targeted evidence.

A useful way to think about it is this. Even though Australian super and insurance disputes have their own legal framework, broader claim-denial guidance can still help you understand how insurers build and defend refusal decisions. This article on appealing an insurance denial in Kentucky is a worthwhile example because it shows the value of reading the denial closely, preserving records, and responding methodically rather than emotionally.

A rejection letter is not the end of the process. It's the start of a more precise one.

When expert help makes sense

Professional help is worth considering when:

- the denial reasons are unclear

- your medical evidence needs tighter coordination

- the policy definition is difficult to interpret

- the trustee and insurer are taking different positions

- the stakes are too high to manage informally

The central issue is rarely just paperwork. It's strategy. A good response identifies what the insurer relied on, what's missing, and what evidence can realistically change the result.

If you're dealing with a tpd insurance claim and want a clear second opinion before you lodge, or after a delay or denial, Wealth Collective can help you understand your cover, pressure-test your claim position, and work out the smartest next step. Start with a simple conversation and get practical guidance specific to your policy, your super, and your circumstances.