Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Perth business owners with profits building up outside their homes, or Dunsborough couples considering how assets will pass to children without chaos, often find that a family trust enters the conversation quickly. The problem is that the term is frequently heard long before there is an understanding of what it does.

A family trust is a legal structure that holds assets for the benefit of nominated beneficiaries, with a trustee making decisions under the rules set out in the deed. In practice, it can sit at the centre of a broader plan around tax, asset protection, succession, and control. It can also be badly set up, poorly funded, and expensive to unwind.

That's why the question isn't just whether a trust sounds useful. It's whether it fits your goals, your family dynamics, and your asset base. When clients ask us about how to set up a family trust, the right starting point is rarely the paperwork. It's the strategy.

Your Guide to Australian Family Trusts

A common WA scenario looks like this. One spouse runs a growing business. The other has a strong PAYG income. They've built some equity, maybe bought investments, and want more control over how future wealth is held. They're also worried about personal exposure if the business hits trouble, or about making sure assets pass cleanly to the next generation.

That's where a family trust starts to make sense. It gives a formal structure for holding selected assets and distributing income according to the trust deed and the law. Used properly, it can support tax planning, asset separation, and succession planning. Used casually, it becomes a folder of documents with no practical value.

What a family trust really is

People often assume a trust is an account or a company. It isn't. It's a legal relationship.

The trust deed sets the rules. The trustee manages the assets. The beneficiaries are the people who may benefit. The appointor usually holds ultimate control over who can replace the trustee. Once you understand those moving parts, the structure becomes much less mysterious.

A well-run family trust doesn't fix a weak financial plan. It supports a strong one.

Why clients usually ask about one

In Western Australia, the people who raise this most often tend to fall into a few groups:

- Business owners: They want to separate investment assets from trading risk where appropriate.

- High-income households: They want flexibility around future income distribution and family wealth planning.

- Pre-retirees: They're thinking about control, legacy, and how trusts fit with super and estate planning.

- Families with growing assets: They want an orderly structure before complexity builds.

The detail matters. A trust can be appropriate for one family and unnecessary for another with a simpler balance sheet and straightforward estate plan.

What works and what doesn't

What works is a trust built around a clear purpose, the right control chain, and proper administration from day one. What doesn't is downloading a generic deed, naming the wrong people, and assuming the structure will somehow “protect assets” on its own.

If you're considering how to set up a family trust, treat it as a legal and financial project. The form matters. The funding matters. The ongoing management matters just as much.

Is a Family Trust Right for Your Wealth Goals

A family trust is most useful when it solves a specific problem. If your affairs are simple, your assets are modest, and there's no real tax, business, or succession complexity, a trust can add administration without adding much value. But for many WA families, that's not the situation.

When a trust usually makes sense

For business owners, the attraction is often risk separation. If you're building wealth outside the trading entity, the question becomes where future investments should sit and who controls them.

For pre-retirees, the conversation is broader. Trusts often sit alongside super, estate planning, and intergenerational transfer. ATO statistics from 2024-25 show that 68% of family trusts hold superannuation assets, which highlights how often they're used as part of integrated wealth planning for Australians nearing retirement, according to this family trust overview.

For high-income households, flexibility matters. A discretionary trust can create options around how trust income is distributed, subject to the deed and tax law. That doesn't mean a trust is a magic tax shortcut. It means the structure can be useful when the family group, income streams, and asset ownership are planned properly.

If you want a plain-language comparison of structure and mechanics, our guide to how a family trust works in Australia is a good place to fill in the basics.

When it may be the wrong fit

There are also cases where a trust is too much structure for too little benefit.

- Simple personal finances: If most of your wealth is your home, super, and standard personal investments, other planning tools may be enough.

- Short-term thinking: A trust is better suited to long-term strategy than a quick reaction to a tax year.

- Poor admin habits: If records, separate accounts, and formal decisions are likely to be neglected, the structure can create more risk than value.

The right trust structure should match the family's actual behaviour, not the version of themselves they hope they'll become once the documents are signed.

Why context matters

A lot of trust content online is written for other legal systems. That can be useful for concepts, but not for implementation. For example, if you want to compare the broader rationale behind trusts in a US setting, this article on establishing a family trust in Texas helps show how similar goals can play out differently across jurisdictions.

In Australia, especially for WA families, the better question is practical. What are you trying to protect, who needs control, and when do you want the structure to start doing real work? If you can answer that clearly, you're in a much better position to decide whether a family trust belongs in your plan.

Assembling Your Trust Key Players

The biggest mistakes in trust setup usually don't start with tax. They start with control. Families often choose people for trust roles based on convenience, habit, or sentiment. That's risky, because each role carries legal and practical consequences.

The roles that matter

Here's the simplest way to think about the trust structure.

| Role | Key Responsibility |

|---|---|

| Settlor | Establishes the trust by settling it with the initial sum and is usually independent of ongoing control |

| Trustee | Holds and manages trust assets according to the deed and legal duties |

| Appointor | Holds the power to remove and appoint the trustee |

| Beneficiaries | The people or entities who may receive income or capital from the trust |

The trustee does the operational work. The appointor usually holds the key control lever. That distinction is often missed, and it matters a lot in succession planning and family disputes.

Choosing the right trustee is a risk management decision, not an admin task. A 2025 report noted a 25% rise in trustee disputes in WA, often driven by family dynamics and misunderstandings about legal duties, as outlined in this discussion of family trust risks.

Individual trustee or corporate trustee

This is one of the most important design choices.

Practical rule: If the trust is likely to hold meaningful assets or operate for many years, don't choose the trustee structure casually.

An individual trustee can be simpler at the start. It may suit a smaller, lower-complexity arrangement where the family understands the risks and the trust's role is narrow.

A corporate trustee usually gives cleaner administration and clearer separation between personal and trust capacity. It can also make succession simpler because the company remains trustee even if directors change.

Individual trustee

Lower initial complexity. More direct involvement. But personal capacity and trust capacity can become muddled, especially when assets, signatures, and succession records aren't handled properly.

Corporate trustee

Better separation of roles. Cleaner paperwork. Usually easier when control changes over time. But it involves extra setup and ongoing company obligations.

Who should actually hold these roles

Family politics often enters the room at this stage.

- Settlor: Use an independent person. They shouldn't be someone intended to benefit from the trust if the deed structure makes that problematic.

- Trustee: Choose the person or company that can act consistently, keep records, and follow advice.

- Appointor: Give this role to someone who understands its power. In many trusts, this is the ultimate control position.

- Beneficiaries: Define the family group carefully so the deed reflects who should be included now and later.

If you're weighing who should hold authority and who shouldn't, it helps to get outside input before the deed is drafted. A good adviser can pressure-test whether your proposed structure is practical, stable, and aligned with your wider plan. That's the same discipline we'd apply in any major financial decision, and it's why choosing the right professional support matters. If you're still deciding who should guide the strategy, this article on how to choose a financial advisor is a useful starting point.

Creating and Settling Your Family Trust Deed

The trust deed is the rulebook. It sets out who controls the trust, who can benefit, what powers the trustee has, and how decisions must be made. If the deed is poorly drafted, the trust may still exist, but it may not do what you intended.

Why the deed should be professionally drafted

This is not the place for a generic template. The deed needs to match Australian law, your state requirements, and the family group you're planning for.

A lawyer drafting the deed should understand how the trust will be used. Holding investments, managing business-related assets, planning around future succession, and allowing for tax-effective distributions can all affect the wording. A deed that's too narrow causes problems later. One that's too broad without clear control can also create risk.

What settling the trust means

To create the trust, an independent settlor usually provides the initial settled sum and signs the relevant documents. That act establishes the trust relationship under the deed.

The amount itself is not the strategic issue. Independence is. You want a clean establishment process and a clear paper trail showing who created the trust and who controls it after settlement.

Execution and stamping in WA

Once the deed has been drafted, it must be signed correctly and dealt with properly under WA requirements. This isn't a formality to leave until later.

In Western Australia, standard discretionary trust deeds typically incur stamp duty of around $200 to $500, and that step helps ensure the trust is legally enforceable under the WA Duties Act 2008, according to the ATO's guidance on trusts.

A practical sequence looks like this:

- Confirm the final parties: Make sure the trustee, appointor, settlor, and beneficiary definitions are all correct before signing.

- Execute the deed properly: Follow the signing requirements exactly. Don't improvise the process.

- Attend to stamping: Complete the WA duty requirements promptly and keep evidence with the trust records.

- Store the original securely: Keep the signed deed where it can be located quickly when banks, brokers, accountants, or lawyers need it.

If the deed is the operating manual, execution is the moment it becomes live. Sloppy signing creates expensive questions later.

The setup stage feels document-heavy, but this is the foundation for everything that follows. Good trust administration is much easier when the deed was right from the start.

Funding the Trust and Navigating Tax Obligations

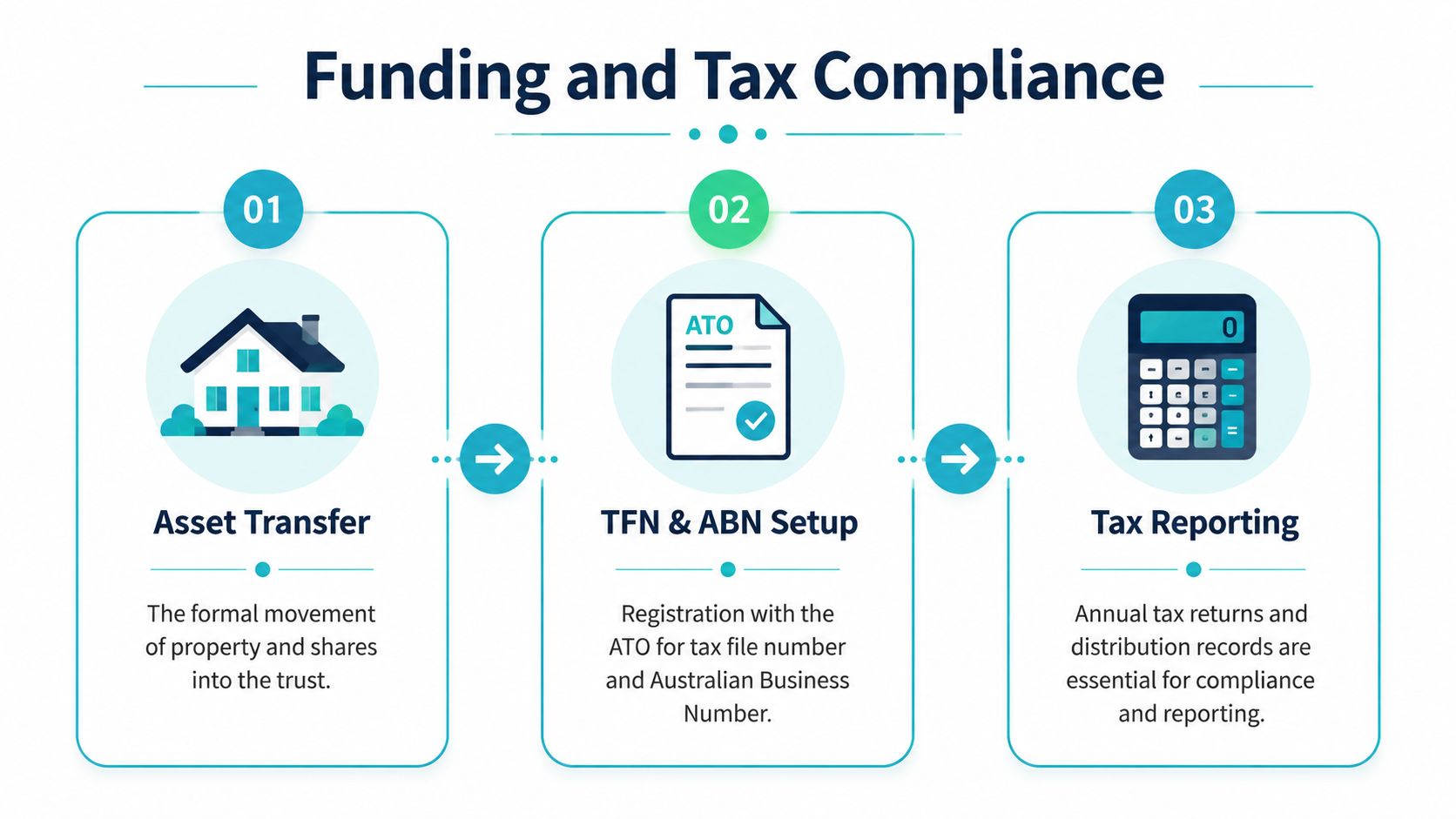

A trust can be perfectly drafted and still fail in practice. That happens when the assets never move into it.

Estate planning surveys indicate that around 40% of trust failures in Australia stem from improper funding, where assets were never formally transferred into the trust's name, leaving them exposed, as noted in this guide to setting up a family trust. That's the most common disconnect I see between intent and reality. People think the deed did the job. It didn't.

What funding actually involves

Funding means legally transferring selected assets so the trustee holds them on trust under the deed. Depending on the asset, that might involve title changes, off-market transfer forms, updated ownership records, or moving cash into a dedicated trust bank account.

Typical assets may include:

- Cash: Usually the first practical funding step, because it allows a bank account to be opened and trust expenses to be paid properly.

- Shares or managed investments: These need ownership records updated correctly. Don't assume the broker account alone proves trust ownership.

- Property: This requires careful legal and tax review before transfer because the mechanics and consequences can be significant.

- Business interests: These can be appropriate in some cases, but only after proper legal, tax, and succession advice.

The trust's tax identity starts immediately

Once the trust exists and is intended to operate, the administration needs to catch up fast. In practical terms, that usually means applying for the trust's TFN and, where relevant, ABN, then opening a bank account in the trustee's name as trustee for the trust.

People often blur lines between personal money and trust money. Don't. Mixed banking and unclear records create avoidable tax and legal problems.

A clean operating setup usually includes:

- A dedicated bank account: All trust receipts and payments should run through the trust account, not through a personal offset or business operating account.

- Clear asset register: Maintain a simple record of what the trust owns and when each asset was transferred.

- Consistent document naming: The trustee should sign documents in the correct capacity every time.

Why annual distribution resolutions matter

The tax effectiveness of a discretionary family trust depends heavily on process. Each year, the trustee generally needs to determine how distributable income will be allocated to beneficiaries and record that decision properly before the relevant deadline.

If that resolution isn't handled correctly, the intended tax outcome can fall apart. The trust may lose flexibility, and the tax treatment may not reflect what the family expected.

Good trust tax planning is usually quiet. The records are clear, the resolutions are timely, and the accountant isn't trying to reconstruct decisions after year-end.

This is also where legal wording and tax administration meet. The deed must permit the relevant distribution approach, and the trustee must follow the deed. One without the other isn't enough.

For households where the trust sits inside a broader strategy involving personal tax, investment structures, and super, it helps to review the setup through a wider planning lens. Our work in taxation and tax planning often intersects here because a trust doesn't operate in isolation. It affects how the rest of the plan behaves.

What doesn't work

Several patterns tend to cause trouble:

- Untransferred assets: The deed exists, but the property, shares, or cash still sit in personal names.

- Shared accounts: Personal and trust transactions run through the same banking setup.

- Backdated thinking: Decisions about distributions are discussed after the deadline rather than documented on time.

- Deed blind spots: The trustee assumes the trust can do something the deed never authorised clearly.

A family trust can be a very effective structure. But only when the legal ownership, tax registration, and annual decision-making all line up.

Your Ongoing Trust Management Checklist

Setting up the trust is only the opening move. After that, the trustee needs to keep the structure alive with records, resolutions, and reviews. When that discipline slips, the trust becomes harder to defend, harder to administer, and less useful to the family it was meant to help.

The annual jobs that matter

Every trust should have a regular compliance rhythm. That usually includes preparing accounts, reviewing what the trust owns, documenting trustee decisions, and lodging the trust tax return properly.

Professional oversight materially improves compliance. A 2025 survey found that trusts with professional administrators or trustees had a 92% audit pass rate compared with 68% for entirely self-managed trusts, according to ATO material on trusts and obligations.

That doesn't mean every trustee needs to outsource everything. It means self-management only works when the trustee treats the role as a real governance job.

Wealth Collective action checklist

Use this as a practical review list.

- Define the purpose: Be clear on why the trust exists. Asset protection, family wealth planning, tax flexibility, succession, or a combination.

- Confirm the control chain: Review the trustee and appointor positions. Make sure the people in control are still the right people.

- Check ownership records: Verify that each intended asset is held by the trustee in the correct capacity.

- Maintain separate banking: Keep trust money separate and easy to trace.

- Prepare annual resolutions: Document trustee decisions on time and in line with the deed.

- Lodge returns and keep records: Retain minutes, financial statements, tax documents, and key correspondence in one organised place.

- Review after life changes: Marriage, divorce, a business sale, retirement, or a death in the family can all change whether the trust structure still fits.

Where outside support helps

Trusts often break down in admin rather than strategy. The family had the right idea, but nobody kept the books properly, nobody reviewed the deed after major changes, and nobody noticed control issues building in the background.

That's why even strong trustees usually need a support team around them. Your lawyer, accountant, and adviser should each be clear on their role. For small business owners who want a sense of how disciplined back-office support can improve visibility and consistency, this article on how Book Tech LLC handles bookkeeping is a useful example of the operational mindset involved.

A family trust should get simpler to manage over time, not messier. If each year feels improvised, the process needs fixing.

The true test of a trust isn't whether the deed was signed correctly years ago. It's whether the structure still works when the family changes, the asset base grows, or control needs to pass smoothly to the next person.

If you're weighing whether a family trust fits your broader plan, or you want a current trust reviewed before small issues become expensive ones, Wealth Collective can help you think it through clearly. A short initial call can identify whether a trust is appropriate, what roles need attention, and where legal or tax advice should come in before anything is signed.