Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

A redundancy often lands in the middle of ordinary life. You might be planning school fees, thinking about retirement timing, or expecting the year to unfold in a predictable way. Then a meeting appears in the calendar, a letter follows, and suddenly you're trying to understand what your payout means, how much tax will come out, and how long the money needs to last.

That's why the tax treatment of redundancy matters so much. A redundancy payout isn't just a final pay packet. It can include several different payment types, each taxed under different rules, and the difference between them can materially affect what you keep.

People often make one of two mistakes at this point. They either assume the whole payment is taxed the same way, or they focus only on the immediate cash amount and miss the planning decisions around timing, super, and retirement. Both can be costly.

Handled well, redundancy can become a turning point rather than just a disruption. The starting point is understanding what kind of payment you've received, whether it qualifies as a genuine redundancy, and how the tax rules apply to each component.

Navigating the Financial Crossroads of Redundancy

A client in this situation usually says some version of the same thing. “I know I'm getting paid out, but I have no idea what I'll receive after tax.” That confusion is understandable. Redundancy happens at an emotional moment, and the paperwork often mixes employment terms, tax labels, and payroll language in ways that aren't easy to interpret.

There's usually more going on than just tax. You may be deciding whether to look for a new role straight away, whether to reduce debt, whether to hold more cash, or whether this is the point where retirement comes forward. The payout sits in the middle of all of those choices.

A redundancy payment can create breathing room, but only if you understand which parts are protected, which parts are taxable, and which decisions need to happen before the money hits your account.

The first practical step is to stop thinking of the payout as one lump sum. It helps to treat it as a financial event with separate moving parts. Some amounts may receive special treatment. Some won't. Some may open up planning opportunities that don't exist in an ordinary year.

For many people, that shift in mindset brings immediate clarity. Instead of asking, “How much am I getting?” the better question becomes, “What is each part of this payment, and what should I do before I act on it?”

Defining a Genuine Redundancy for Tax Purposes

The tax system doesn't treat every job loss the same way. The phrase genuine redundancy has a specific meaning, and it matters because special tax treatment depends on meeting that definition.

What the rule is really asking

In plain language, the key question is whether the job itself has ended, not just whether your employment has ended. If the employer no longer needs the role, that points toward redundancy. If the role continues and someone else takes your place, that points the other way.

A practical way to think about it is this:

- The position is gone: Your employer no longer requires that role to be performed.

- You are not being cycled back in: There isn't an arrangement to re-employ you in the same business or a related entity.

- The termination reflects the role ending, not a personal issue: It isn't really a resignation, performance dismissal, or another type of exit dressed up as redundancy.

That distinction is where many people get caught out. Two employees can both leave on the same day with similar-looking payout letters, but only one may qualify for genuine redundancy treatment.

Why age used to matter more than it does now

This area changed in an important way. The ATO notes that on 1 July 2019, Australia removed the fixed age limit of 65 for concessional tax treatment on genuine redundancy and early retirement scheme payments, replacing it with a reference to the Age Pension Age for employees dismissed on or after that date, as explained in the ATO guidance on genuine redundancy payments.

That matters for mature workers. Before that change, reaching a fixed age could shut off access to concessional treatment even when the redundancy was real. Now the framework better reflects the fact that people work later and retirement timing isn't uniform.

Practical rule: If you're close to retirement age, don't assume you've automatically missed out on redundancy tax concessions. The age rule changed, and the detail matters.

Where people usually get confused

The biggest misunderstanding is assuming that any involuntary exit is a genuine redundancy. It isn't. Another common issue is relying on the label used by the employer rather than the substance of what occurred.

Use this quick sense-check:

| Question | Why it matters |

|---|---|

| Was your role actually abolished? | This goes to the core of whether the redundancy is genuine |

| Is there any plan for re-employment? | Rehire arrangements can affect eligibility |

| Was the termination really for another reason? | Performance or voluntary departure won't be treated the same way |

If there's uncertainty here, it's worth clarifying before you focus on the tax maths. The best calculation in the world won't help if the payment doesn't qualify for the treatment you were expecting.

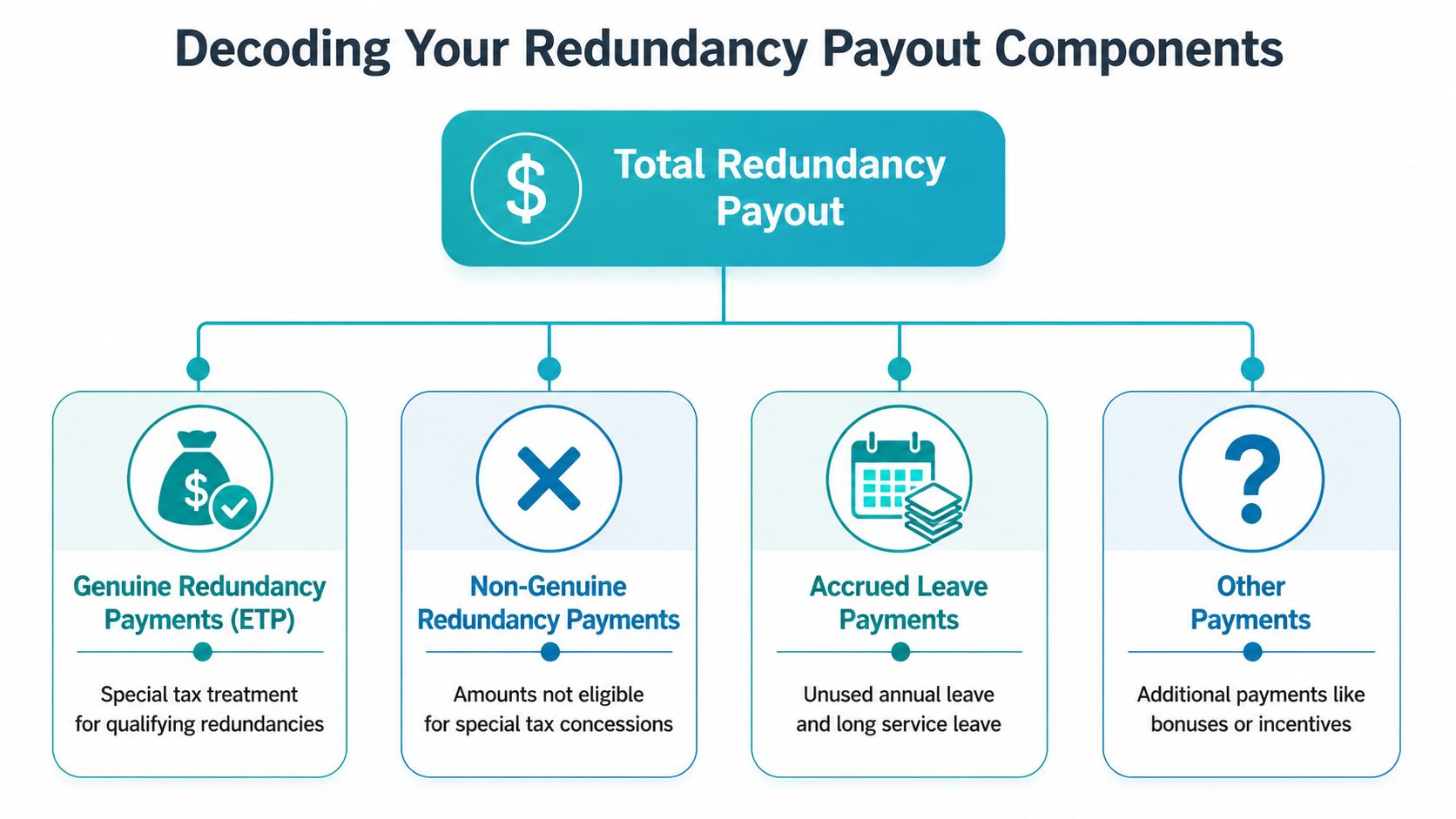

Decoding the Components of Your Payout

Most redundancy letters bundle several items together. That's where people start to feel overwhelmed. The better approach is to break the payout into separate buckets and ask how each one is taxed.

The three buckets that matter most

A typical payout usually contains some mix of the following:

Tax-free genuine redundancy amount

This is the part that may qualify for special treatment if the redundancy is genuine. It isn't merely “whatever the employer calls severance”. It's the amount that falls within the tax-free threshold available under the redundancy rules.

This is often the most valuable part of the package because it can be received without tax up to the applicable threshold.

Employment Termination Payment

The next layer is usually an Employment Termination Payment, often shortened to ETP. Many severance-style amounts are paid as an ETP once they exceed the tax-free redundancy portion.

An ETP can still receive concessional tax treatment, but it isn't tax-free. The amount you keep depends on age, the size of the payment, and whether the amount stays within the relevant cap.

Other amounts taxed differently

Some payments are not part of the genuine redundancy amount or the concessional ETP bucket. Common examples include unused leave and other employment entitlements.

These often surprise people because they may be taxed under their own rules rather than under the redundancy rules they've been reading about.

A cleaner way to read your statement

When you review a payout summary, don't start with the gross total. Start by asking payroll or HR which line belongs in which category.

A simple checklist helps:

- Find the redundancy amount: Identify the payment linked to the loss of the role itself.

- Separate leave entitlements: Unused annual leave and long service leave usually need to be viewed separately.

- Check for extra items: Bonuses, incentives, notice-related amounts, or goodwill payments may not follow the same treatment as the core redundancy amount.

If the payment summary looks confusing, that doesn't mean the tax is complicated beyond understanding. It usually means several tax rules have been stacked into one letter.

Why this breakdown matters

This isn't just an accounting exercise. Each bucket affects your decisions differently.

If more of the payment falls into the tax-free category, you may have greater flexibility around debt reduction or cash reserves. If more sits in the ETP category, timing and contribution strategies become more important. If a large share is leave, you need to know that before estimating your after-tax proceeds.

Until you've split the package into components, you don't really know what your redundancy is worth in practical terms.

How Your Redundancy Payment is Actually Taxed

The most useful way to understand this is through a worked example. Once you see the logic, the rules become much easier to apply to your own situation.

Start with the tax-free threshold

For the 2025-26 financial year, the tax-free portion of a genuine redundancy payment is $13,100 plus $6,552 for each full year of service, according to this explanation of redundancy tax treatment for 2025-26.

Take an employee with 10 full years of service. The tax-free threshold is:

- Base amount: $13,100

- Service amount: $6,552 × 10

- Total tax-free threshold: $78,620

If that employee's genuine redundancy payment is at or below $78,620, that part is tax-free under the rule above.

Then look at what sits above it

If the genuine redundancy payment is higher than the tax-free threshold, the excess generally moves into the ETP area.

The same source explains that amounts above the tax-free portion, up to the ETP cap of $260,000, are taxed concessionally. It also sets out that employees under 60 may face tax of up to 30% plus Medicare Levy on capped amounts, while employees aged 60 or over may face tax of up to 15% plus Medicare Levy on capped amounts. Amounts above the cap are taxed at 45% plus Medicare Levy. If you want broader guidance on structuring these decisions inside your year-end planning, this overview of taxation and tax planning services is a useful reference point.

A simple example using the threshold

Let's say Priya has a genuine redundancy payment of $100,000 and 10 full years of service.

Her calculation starts like this:

| Item | Amount |

|---|---|

| Genuine redundancy payment | $100,000 |

| Tax-free threshold | $78,620 |

| Amount above threshold | $21,380 |

In this example, $78,620 is tax-free. The remaining $21,380 doesn't become ordinary salary just because it is taxable. It falls into the ETP framework and is taxed under those concessional rules, subject to the relevant age-based treatment and cap rules.

The key point isn't just how much tax applies. It's that different parts of the payment are taxed under different systems, and mixing them together leads to bad estimates.

What this means in real life

The attempt to estimate a net payment with one rough percentage usually fails because redundancy tax doesn't work as one flat treatment across the whole payout.

A better order of operations is:

- Confirm the payment qualifies as a genuine redundancy.

- Work out the tax-free threshold using full years of service.

- Isolate any amount above that threshold.

- Treat that excess under the ETP rules.

- Keep leave and other entitlements separate.

If you follow those steps, your estimate becomes much closer to reality. Because of this, you can start making decisions based on the actual after-tax structure of the payout, not a guess.

Strategies to Maximise Your Redundancy Payout

Understanding the tax is only half the job. The more important question is what you can still influence before the year closes and before the money gets absorbed into day-to-day spending.

Timing can change the outcome

One planning opportunity people often miss is timing. If your termination date or payment date has some flexibility, the financial year in which the payment lands can affect how the taxable components interact with your other income.

That won't always be negotiable. But when it is, the right timing can make the overall tax position more manageable and give you more room to coordinate the next steps.

This matters even more if you expect a gap before your next role, a lower-income year, or a transition into retirement.

Super is often the missed lever

A major gap in public guidance is the interaction between redundancy and superannuation. One source highlights that high-income earners can strategically use their annual concessional super contribution cap of $27,500 in the same financial year as redundancy to reduce overall tax liability, as outlined in this discussion of super contribution planning during redundancy.

That's where strategic advice can add real value. Generic guides tend to explain redundancy tax rules on one page and super caps on another, without helping people coordinate them.

Here's the practical logic:

- Taxable redundancy components create planning pressure: If part of the payout falls into a taxable bucket, you may want to look for legitimate ways to reduce overall taxable income.

- Concessional super contributions can be part of that response: Used appropriately, they can support both tax management and long-term retirement savings.

- The timing must line up: Once the financial year closes, that planning window may narrow or disappear.

A redundancy can create an unusual one-year opportunity. You may have a larger taxable event than normal, and that makes contribution strategy more valuable than it would be in an ordinary year.

Other decisions that deserve attention

Not every good move is about minimising tax. Sometimes the smartest strategy is about preserving flexibility.

Consider these questions early:

- Cash reserve first: How much should remain accessible if your next role takes longer than expected?

- Debt second: Should any part of the payout reduce high-cost debt, or is liquidity more important for now?

- Retirement pathway: If redundancy arrives close to retirement, does this change your drawdown timing, pension planning, or super strategy?

These decisions interact. Someone who uses the full payout to clear debt without preserving cash may feel secure on paper but exposed in practice. Someone who keeps all of it in cash may miss a chance to improve both tax efficiency and long-term outcomes.

The strongest redundancy planning usually combines tax awareness, super coordination, and a realistic view of what the next stage of life looks like.

Beyond Tax: Reporting, Centrelink, and Your Next Steps

After the tax questions, the administrative side begins. This is the part people often put off because it feels secondary. It isn't.

Your employer's reporting needs to match the nature of the payment. That means checking your income statement, final payslip, and payment summary details carefully. If a payment has been categorised incorrectly, the flow-on issues can affect your tax return and your understanding of what was paid.

What to review after payment

Keep the review practical. You're looking for clarity, not perfection on day one.

- Match the labels: Does the redundancy amount appear separately from leave and other entitlements?

- Check the dates: The payment date can matter for financial year planning.

- Keep every document: Termination letter, payroll summary, and any explanatory notes should stay together.

If something looks off, raise it early with payroll or your adviser. Small reporting issues can create larger confusion later.

Centrelink can be affected too

A redundancy payout can also affect government support, especially if you're moving into a period without employment income. That doesn't mean you won't qualify for support, but it does mean timing and structure matter.

Centrelink uses its own rules and waiting periods. If you're near retirement age, or you're trying to understand how a change in employment status could affect future entitlements, tools like this Age Pension eligibility calculator can help you start framing the broader picture.

Don't treat redundancy as a tax-only event. It can affect reporting, cash-flow planning, and the way government agencies assess your circumstances.

The broader next step

This is the point where the paperwork and the life planning meet. You may need to update your budget, review your emergency fund, revisit insurance, and map out what happens if work restarts quickly versus later than expected.

That broader view matters because the tax treatment of redundancy is only one part of the financial outcome. What you do in the weeks after payment often matters just as much.

Why a Redundancy is the Perfect Time for Financial Advice

Redundancy compresses a lot of decisions into a short period. You may be dealing with tax rules, super opportunities, income planning, retirement timing, and Centrelink implications all at once. Even confident investors can miss details when those decisions arrive under stress.

That's why this moment often deserves proper advice. Not because redundancy is always complicated in theory, but because it becomes complicated in real life. A technically correct tax answer doesn't automatically tell you how much cash to retain, whether to contribute to super, when to redraw your retirement timeline, or how to sequence the next moves.

Good advice can turn a scattered set of questions into a clear plan. For some people, that means preserving capital while they transition to a new role. For others, it means using the payout as a bridge into retirement. If retirement is part of the conversation, personalized financial advice for retirement planning can help connect the payout to your bigger picture.

The important thing is not to treat the payout as money that arrives and gets allocated later. Once the key deadlines pass, some of the best planning opportunities pass with them.

If redundancy has landed on your desk, clarity is worth getting early.

If you want help making sense of a payout, weighing your options, and turning a stressful employment change into a structured financial plan, book an initial call with Wealth Collective.