Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You're probably here because you've built a solid super balance, you like property as an asset class, and you're wondering whether your super can do more than sit in a standard fund mix of shares, cash, and managed options.

That's a sensible question. It's also where many people take a wrong turn.

To buy property in an SMSF can be a smart long-term move, but it only works when the structure, paperwork, and decision-making discipline are right from the start. This isn't a normal property purchase with a different loan product attached. It's a regulated retirement strategy with property sitting inside it. That changes everything from who can use the asset, to how the contract is signed, to how the fund pays expenses after settlement.

Most problems don't start with a bad property. They start with a rushed setup, the wrong ownership name on a contract, or a strategy that never properly addressed cash flow, compliance, and trustee obligations.

A Clear Path to Buying Property in Your SMSF

If you're considering property inside super, you're not alone. Many Australians are looking at their retirement savings and asking whether direct property could play a more active role in building long-term wealth.

The attraction is easy to understand. Property feels tangible. You can inspect it, assess its location, review lease terms, and compare it against your broader goals. For some clients, that level of control matters more than holding another menu of managed investment options. If you're still weighing up the bigger question, is it worth buying property with super is a useful starting point before you move into execution mode.

Why this strategy needs a project mindset

Buying through an SMSF is rarely difficult because one rule is unclear. It becomes difficult because several moving parts must line up at the same time:

- Trust structure: The fund deed, trustee setup, and ownership arrangements must support the transaction.

- Investment logic: The property has to fit the fund's retirement purpose and investment strategy.

- Transaction control: The contract, finance, bare trust, legal review, and settlement process must all be coordinated correctly.

- Post-purchase discipline: Rent, expenses, valuations, records, and reporting need to be handled through the fund properly.

A successful SMSF property purchase usually looks boring on paper. That's a good sign. It means the process was organised before emotion took over.

Clients often think the hard part is finding the property. In practice, the hard part is getting the structure right before you sign anything. Once that foundation is in place, the path becomes much clearer.

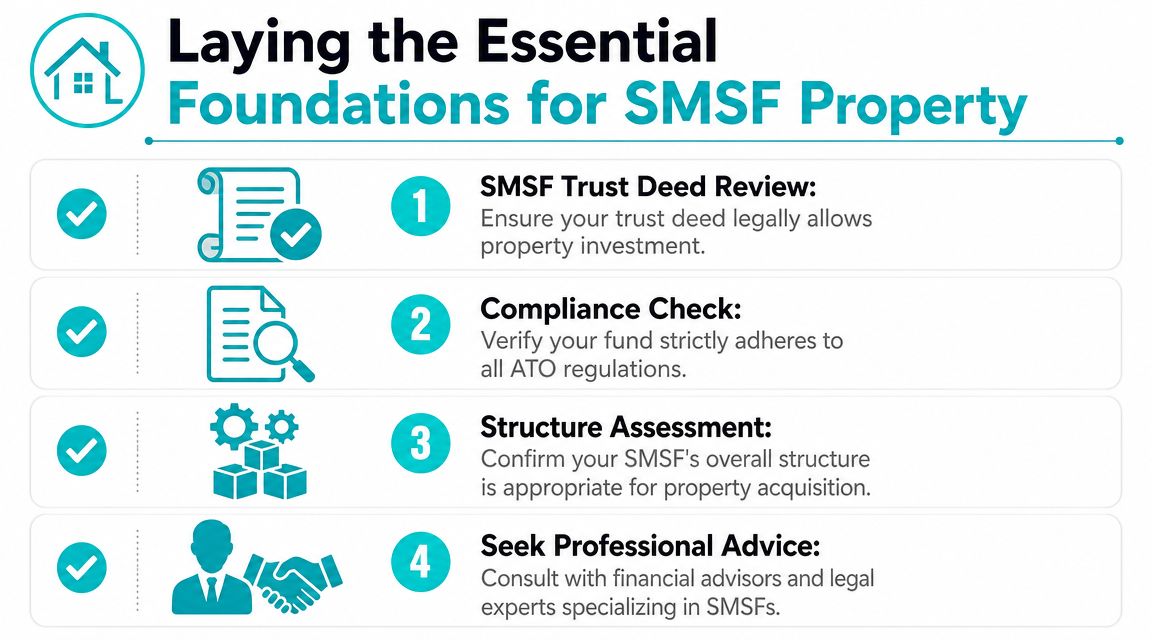

Laying the Essential Foundations

This is the phase people underestimate most. Before you inspect a property, speak to a lender, or ask a conveyancer to review a contract, the SMSF itself needs to be ready.

A good way to think about it is the slab under a house. If that's wrong, everything built on top becomes more expensive to fix.

Start with the deed and structure

Your SMSF trust deed needs to support what you're trying to do. If the fund may borrow, acquire direct property, or use a holding arrangement for an LRBA, the deed and related documents need to align with that intention. Trustees also need to understand their duties before any transaction begins, because once you control an SMSF, you also carry the legal responsibility for how it operates.

This isn't just about legality. It affects timing. A property can come on the market quickly, but if the fund structure still needs work, rushing at that point creates avoidable risk.

Check whether direct property actually fits the fund

Property inside super has become more prominent. As of March 2024, the Australian Taxation Office reported more than 616,000 SMSFs nationwide holding $933 billion in assets, about 24% of the $3.9 trillion invested in Australian superannuation. Between the June quarters of 2021 and 2024, SMSF allocations to residential property rose 26.4% to $55.2 billion, while non-residential property rose 25% to $102 billion, according to this report citing ATO data.

That tells you two things. First, plenty of trustees are using property in SMSFs. Second, popularity doesn't remove the need for judgment. A strategy can be common and still be unsuitable for a particular fund.

Your investment strategy needs to be real, not generic

An SMSF investment strategy should do more than tick a box. If the fund is going to buy direct property, the strategy should reflect that in a way that makes sense for the members, their retirement timeframe, and the fund's need for liquidity and diversification.

A weak strategy usually sounds broad and vague. A stronger one connects the asset choice to the fund's actual circumstances.

Use this pre-purchase review before moving further:

- Deed authority: Confirm the trust deed and trustee structure support direct property and any intended borrowing arrangement.

- Member suitability: Check that all trustees understand their obligations and can manage the ongoing responsibilities.

- Investment alignment: Make sure direct property fits the fund's retirement purpose and overall portfolio approach.

- Cash management: Consider whether the fund can handle acquisition costs, vacancies, maintenance, loan obligations, and compliance costs without strain.

- Professional coordination: Line up advice early, not after a contract is in front of you.

Practical rule: If a property opportunity is forcing you to fix the SMSF structure in a hurry, the opportunity is arriving too early.

For readers still at the setup stage, how to start a self-managed super fund is the right place to sort out the mechanics before you think about suburb lists or lease yields.

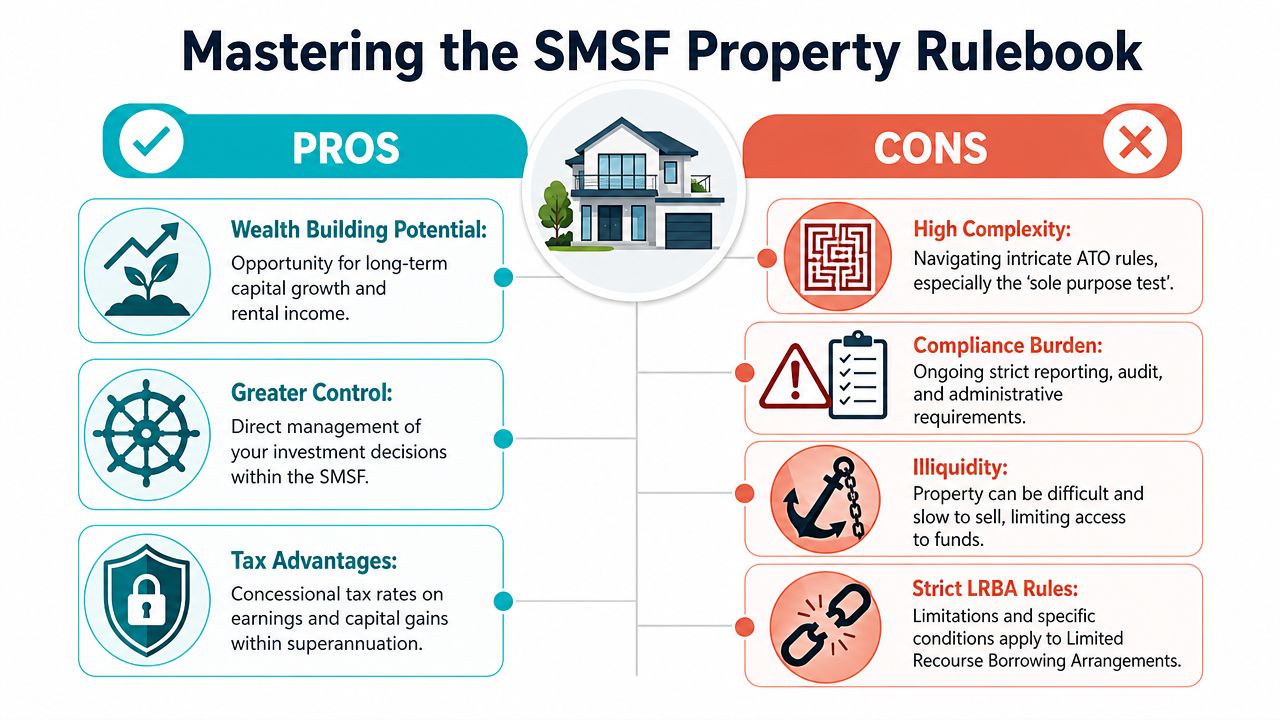

Mastering the SMSF Property Rulebook

Most SMSF property mistakes happen because trustees treat the rules as technicalities. They aren't. The rules shape what you can buy, who can use it, and how the arrangement must operate over time.

The sole purpose test in plain English

The property must be held to provide retirement benefits for members. That's the core principle.

If a property gives you or a related party a present-day personal benefit, you've usually moved into dangerous territory. That's why an SMSF residential property can't become your holiday home, your child's rental, or a “temporary” place for a family member to stay while they sort themselves out.

The rule isn't there to frustrate trustees. It exists because superannuation receives concessional treatment on the basis that the money is preserved for retirement.

Related parties and use restrictions

The practical rules are clear. An SMSF property purchase must satisfy the sole purpose test, the asset cannot be acquired from a related party, and it cannot be lived in or rented by a fund member or related party. If the property is business real property, it may be leased to a member only at market rates and under specific rules, as explained by Moneysmart's guidance on SMSFs and property.

That leads to a few common real-world outcomes.

Residential property scenario

You find a good apartment and think your adult daughter could rent it at a fair price. That doesn't work. Market rent doesn't fix the related-party issue for residential property.

Commercial property scenario

You own a trading business and lease a warehouse elsewhere. Your SMSF may be able to purchase qualifying business real property and lease it to your business, but the arrangement has to be properly documented and operate on market terms. Rent can't be casual, discounted, delayed, or treated like a family arrangement.

If a lease wouldn't pass a strict commercial review by an unrelated third party, it doesn't belong inside an SMSF.

What works and what usually doesn't

A quick filter helps.

| Situation | Generally workable | Main issue to check |

|---|---|---|

| Residential property leased to unrelated tenants | Yes | Ongoing arm's-length operation |

| Residential property used by you or family | No | Breach of retirement purpose and use rules |

| Commercial property leased to your business | Potentially | Must be business real property at market rates |

| Buying a property you already own personally | Usually no | Related-party acquisition problem |

Property language also causes confusion, especially for first-time SMSF trustees. If you need a plain-English refresher on the terms brokers, agents, and lenders use, this ultimate real estate investment glossary is handy before you start reviewing contracts and lease clauses.

Funding the Purchase with an LRBA

An SMSF can sometimes borrow to acquire property, but the borrowing structure is specialised. The usual vehicle is a Limited Recourse Borrowing Arrangement, or LRBA.

What limited recourse actually means

“Limited recourse” means the lender's security rights are limited to the asset held under that arrangement. In plain terms, if the loan fails, the lender's claim is directed at that property rather than the fund's other assets under the borrowing structure.

That protection is one reason the setup is more formal than a standard investment loan. The law expects a specific ownership and borrowing framework, not a shortcut.

The moving parts in the structure

At a high level, the arrangement usually involves:

- The SMSF trustee: Makes the investment decision and provides the fund money.

- A bare trustee or holding trustee: Holds legal title to the property while the LRBA is in place.

- The lender: Advances funds under the limited recourse loan terms.

- The SMSF beneficial interest: The SMSF remains the beneficial owner and receives the economic benefit of the asset.

A common misstep clients make is assuming the bare trust can be sorted after the contract is signed. That's often too late. The names on the contract and the intended ownership structure need to match the legal advice from day one.

Finance assessment is about more than approval

A lender doesn't just ask whether the SMSF wants the property. The lender wants to see that the whole arrangement is coherent. Even before formal application, trustees should pressure-test these questions:

- Can the fund cover the deposit and purchase costs from SMSF resources?

- Will the fund still have enough liquidity after settlement?

- Is the property likely to produce reliable rental income under a sensible lease structure?

- Can the fund manage loan repayments during vacancy, repairs, or delayed leasing?

A good explainer on broader investment property borrowing mechanics is LendingXpress investment financing. It isn't SMSF-specific legal advice, but it's useful context when comparing ordinary investment debt with the more controlled LRBA environment.

The loan is only one part of the decision. The harder question is whether the fund can carry the property well after the excitement of settlement disappears.

Why trustees need a slower process here

An LRBA is where haste becomes expensive. If the bare trust is wrong, if documents are inconsistent, or if the contract names are incorrect, fixing the problem can involve legal cost, delay, and in some cases a complete restart of the transaction path.

That's why the finance stage should feel deliberate. The right outcome isn't “approved quickly”. It's “structured correctly”.

Executing the Purchase From Search to Settlement

Once the fund structure and funding path are sorted, the transaction becomes a project. Here, careful buyers separate themselves from hopeful buyers.

The SMSF can't just like a property. Trustees need evidence that the asset is appropriate, correctly priced, and capable of being held in a way that will survive legal review, annual accounts, audit scrutiny, and the ATO's valuation expectations.

Property selection needs an SMSF lens

A property that looks fine in a personal name purchase may be unsuitable in an SMSF.

For example, a property with confusing lease terms, weak tenant quality, unresolved building issues, unusual title arrangements, or poor documentation can create ongoing administration problems inside the fund. Trustees should also think about practicality. An SMSF asset should be straightforward to explain to an auditor and easy to support with records.

Valuation is not optional

The ATO requires SMSF trustees to value fund assets at market value in financial accounts and statements, and says property valuations should be based on factors such as recent comparable sales, independent appraisals, and arm's-length pricing. The value should reflect what a willing buyer and seller would agree on in an open market, according to the ATO guide to valuing SMSF assets.

That matters before and after purchase. On the way in, trustees need confidence they aren't overpaying. After settlement, they need records that support the fund's reporting position.

A property can be a good asset and still be a poor SMSF purchase if the valuation support is thin or the documentation is sloppy.

The transaction checklist that actually matters

The cleanest way to handle this phase is with a working checklist. Not a generic one. A file-specific one that's updated as each item is cleared.

| Verification Area | Action Item | Status |

|---|---|---|

| Property suitability | Confirm the asset matches the SMSF investment strategy and intended use | Pending |

| Ownership structure | Verify the purchasing entity and any bare trust details before signing | Pending |

| Market value support | Obtain comparable sales evidence and, where appropriate, an independent appraisal | Pending |

| Legal review | Have a property lawyer or conveyancer review the contract and special conditions | Pending |

| Related-party check | Confirm the seller, tenant, and use case comply with SMSF rules | Pending |

| Lease review | Assess lease terms, rent setting, and arm's-length operation if tenanted | Pending |

| Finance readiness | Ensure funding approval and SMSF cash requirements are in place | Pending |

| Settlement administration | Confirm bank account flow, signing authority, and record-keeping process | Pending |

Contract review comes before emotion

Trustees often become emotionally committed after an accepted offer. That's the wrong order.

A compliant SMSF purchase needs contract review before you lock yourself in. The purchasing name, trustee references, and any conditions tied to finance or structure all need to be checked by the right professionals. If borrowing is involved, this step becomes even more sensitive because the title-holding arrangement must line up with the legal structure already established.

Small errors become expensive later

The most common transaction problems are rarely dramatic. They are administrative. A contract signed in the wrong name. Deposit funds moved from the wrong account. A tenancy assumption that was never documented. A valuation that can't be defended cleanly at year end.

A coordinated advice process is essential. Wealth Collective works in this space by helping clients map strategy, structure, and implementation in a way that keeps the project orderly rather than reactive.

Ongoing Management Costs and Compliance

Settlement isn't the finish line. It's the point where trustee discipline becomes visible.

Once the property sits inside the SMSF, every dollar connected to it needs to move through the fund properly. That means clean records, consistent process, and no mixing of personal and fund money.

Money in and money out

The easiest way to keep this straight is to treat the property like a separate operating asset of the fund.

Money in includes rent and any other property-related receipts. Those amounts should go directly into the SMSF's bank account.

Money out includes rates, insurance, repairs, loan repayments, property management fees, and other allowable expenses. Those should be paid directly by the SMSF, not covered personally with the idea of “sorting it out later”.

That audit trail matters. If trustees blur the line between personal funds and SMSF funds, the paperwork becomes harder to defend and the compliance risk rises.

The ongoing habits that keep the fund clean

Strong trustees usually keep a simple operating rhythm:

- Bank account discipline: Use the SMSF account for all property income and expenses.

- Document retention: Store lease agreements, invoices, valuations, insurance records, and settlement documents in one organised system.

- Lease integrity: If the property is leased, keep rent collection, renewals, and any reviews consistent with arm's-length terms.

- Annual reporting support: Make year-end accounts and audit easier by maintaining records as you go, not rebuilding the file months later.

For trustees who need help with the record-keeping and reporting side, SMSF accounting support can remove a lot of friction from the annual cycle.

Good SMSF property management is quiet. Rent arrives where it should. Expenses are paid from the right account. The file tells a clear story without explanation.

Why this phase decides whether the strategy stays effective

The purchase gets attention because it feels significant. The management phase is where the strategy either remains sound or starts to wobble.

If the fund constantly runs tight on cash, if repairs create stress, if rent collection becomes irregular, or if trustees delay record-keeping, the property starts controlling the fund rather than serving it. That's usually the sign that the original plan didn't properly account for real-world ownership.

Create Your SMSF Property Plan with Confidence

To buy property in an SMSF can be a strong strategy when the fund is properly structured, the asset fits the retirement purpose, and the trustees treat the purchase like a regulated investment project rather than a casual property deal.

The key isn't just knowing the rules. It's applying them in the right sequence. Structure first. Rule checks before commitment. Finance built around the legal framework. Then disciplined execution from contract through to ongoing management.

That's where many trustees benefit from experienced guidance. Not because the process is impossible to understand, but because there's very little room for avoidable error once contracts, lending, and compliance obligations all intersect.

If you're weighing whether an SMSF property purchase fits your broader retirement plan, the next step should be a proper review of your fund, your goals, your cash flow, and the type of property you're considering.

Ready to explore whether an SMSF property strategy suits your circumstances? Book a complimentary introductory call with Wealth Collective and get clear guidance on the structure, trade-offs, and next steps.