Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You're probably carrying two thoughts at once right now. One says, “I want a stable home for my kids.” The other says, “I've only got one income, costs keep rising, and I don't want to make a mistake that traps me.”

Both thoughts are reasonable.

Buying a home as a single parent in Australia is possible. It's also not something you should approach with blind optimism. The smart move is to treat it like a strategy problem, not a hope problem. You need the right loan structure, the right support scheme if you qualify, and a budget that still works when life gets messy.

You Can Buy a Home as a Single Parent

A lot of single parents assume they're outside the “normal” borrower picture. You're not. In Australia, there were about 992,000 single-parent families in 2021, making up around 15% of all families according to family household data referenced here. That matters because it means single-parent households are not a niche edge case. Lenders, policymakers, and support schemes know this is a major part of the housing market.

I see the same pattern often. A parent has done the hard yards. They've rebuilt after separation, managed rent, covered school costs, kept food on the table, and still saved something. Yet when they think about a home loan, they freeze. Not because they're careless, but because one wrong move feels bigger when no second income is sitting beside yours.

That fear can make you overestimate the barrier.

You're not asking for a special favour

You're not trying to game the system. You're trying to move from unstable housing costs to a home you control. That's a sensible goal. The challenge is usually not whether a single parent can buy. The challenge is matching the purchase to what your cash flow can realistically carry.

Buying on one income doesn't make you a weak applicant. It means you need a tighter plan than most people.

Single parent home loans work best when you stop comparing yourself to dual-income households and start building around your own strengths. Stable income. Clean account conduct. A realistic target suburb or property type. Clear paperwork. A buffer.

What matters most at the start

Before you look at listings, get honest about three things:

- Your borrowing reality: What a lender may approve and what you should borrow are not always the same number.

- Your support options: Some buyers focus only on saving a massive deposit and miss available pathways that can bring the timeline forward.

- Your long-term comfort: If the mortgage only works in a perfect month, it doesn't work.

If you're a single parent reading this, the question isn't “Can someone like me buy?” The better question is, “What structure gives me the best chance of buying safely and keeping the home comfortably?”

That's the question worth answering.

Understanding Your Home Loan Options

Single parent home loans aren't a separate species of mortgage. You're usually choosing from the same core loan types as everyone else. The difference is that your margin for error is smaller, so the loan structure matters more.

Principal and interest versus interest only

For most single parents buying a home to live in, principal and interest is the cleaner option. You pay interest and gradually reduce the loan balance. It's the steady, boring, sensible route.

Interest only can reduce repayments for a period, but it usually delays real progress on the debt. For a household running on one income, that can create a false sense of affordability. The payment looks easier now, then the pressure arrives later.

A simple way to think about it:

| Loan structure | What it feels like in real life | Best fit |

|---|---|---|

| Principal and interest | More disciplined, more predictable debt reduction | Owner-occupiers who want long-term stability |

| Interest only | Short-term breathing room, but less progress | Limited situations, usually not first choice for a single parent buyer |

Variable versus fixed rates

A variable rate moves with the lender's pricing. That means your repayments can change. Sometimes that helps. Sometimes it hurts.

A fixed rate acts more like a short-term cost shield. You get clearer repayment certainty for the fixed period, which can help if you need a tighter household budget. The trade-off is less flexibility. Depending on the lender and loan terms, fixed loans can be less forgiving if you want to make changes later.

If you want a plain-English breakdown of the trade-offs, this guide on fixed or variable home loan rates is worth reading.

What LMI means

Lenders Mortgage Insurance, or LMI, is a cost that often applies when your deposit is smaller. It protects the lender, not you. That's why many borrowers hate it, and fairly so.

For a single-income household, extra upfront costs matter more because they compete directly with your emergency savings, moving costs, and day-to-day breathing room.

Practical rule: Don't choose a loan based only on the headline rate. Check the total cash you need to get through purchase and settle in safely.

Refinancing matters later too

Your first loan doesn't have to be your forever loan. Once you've built equity and your circumstances improve, refinancing can become a useful tool. If you ever reach that point, it helps to compare Australian refinance cashback offers alongside rate, fees, and flexibility, rather than looking at cashback in isolation.

The right home loan for a single parent is rarely the flashiest one. It's the one that still feels manageable when school expenses land, the car needs repairs, and life behaves like life.

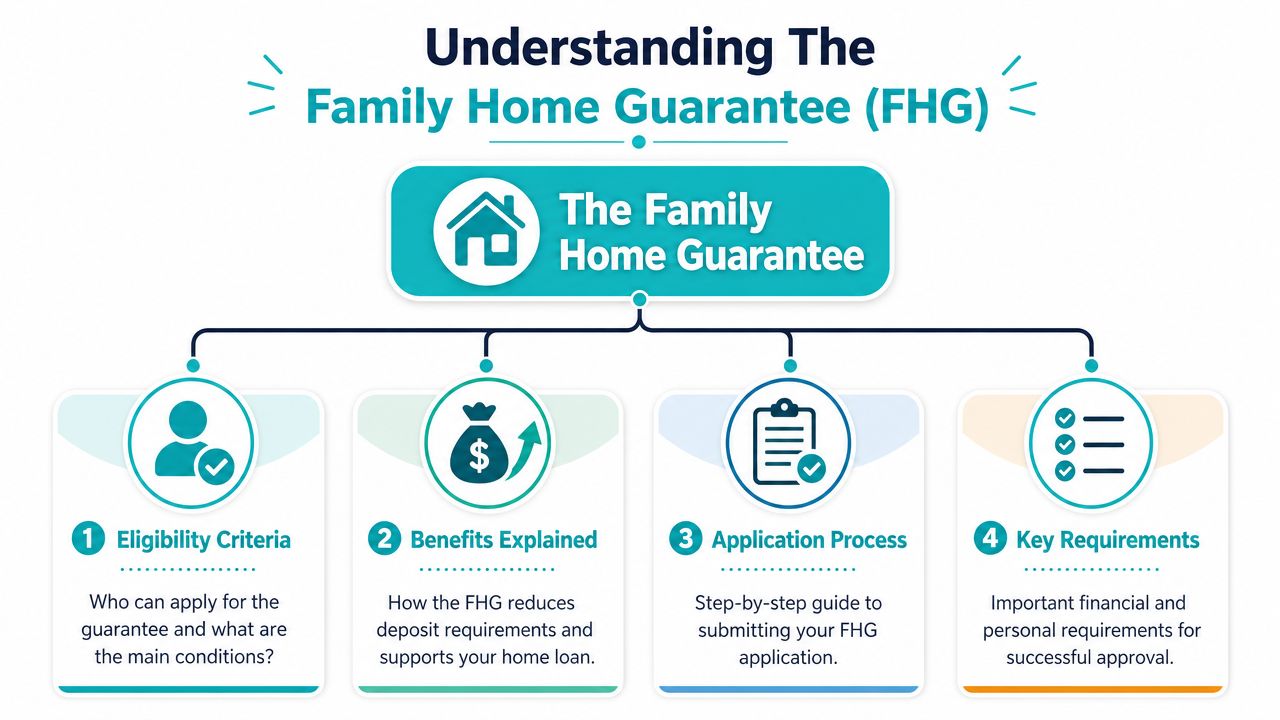

Unlocking Government Support The Family Home Guarantee

You find a place that suits your kids, close enough to school, and finally within reach. Then the deposit knocks you out of the race. That is exactly the problem the Family Home Guarantee is built to solve.

According to Housing Australia's Family Home Guarantee fact sheet, eligible single parents with dependants may be able to buy or build with a minimum 2% deposit, with Housing Australia guaranteeing up to 18% of the property value to the lender. In plain English, that can let you buy sooner without needing a full 20% deposit.

Why this scheme deserves serious attention

For a single parent, time matters. Every extra year spent chasing a bigger deposit can mean another year of rent increases, another lease renewal, and another stretch of trying to save while covering everything alone.

The Family Home Guarantee can shorten that timeline. More importantly, it can protect your cash buffer. That matters just as much as getting approved.

A low deposit is only helpful if you still have money left after settlement for the things real life throws at you. Rates change. Kids need new uniforms. Cars break down. If a scheme helps you buy while keeping more savings in your account, that can make home ownership more sustainable, not just more accessible.

What it does not do

The guarantee does not give you a free pass with the lender. You still need to qualify for the loan based on income, debts, living costs, and repayment capacity.

That is the part many borrowers underestimate.

Getting into a home is one step. Keeping the home without constant financial pressure is the standard you should care about. If the repayments only work on your best month, the loan is too big.

WA price caps can decide whether the scheme works for you

In Western Australia, the property price cap is a hard boundary, not a minor detail. For many Perth single parents, this cap means planning needs to get real quickly.

Under the scheme, the cap is $500,000 for Perth and capital city or regional centres, and $400,000 for the rest of Western Australia, as noted earlier in the Housing Australia fact sheet. If the homes you are inspecting sit above that limit, the scheme will not help you. Change the search area, change the property type, or drop the idea early and build a different plan.

That is why I tell clients to check eligibility and price caps before they fall in love with a suburb.

Use the scheme properly

The best use of the Family Home Guarantee is not borrowing to your absolute maximum. It is buying a home that still leaves room in your budget after the mortgage starts.

Focus on four tests:

- Property fit: The purchase price must sit within the scheme rules for your area.

- Cash fit: You need enough for the deposit, stamp duty if applicable, legal fees, moving costs, and a post-settlement buffer.

- Repayment fit: The loan must remain affordable if rates rise or a large annual expense lands at the wrong time.

- Life fit: The property should suit your family for a reasonable period so you are not forced into another expensive move too soon.

My advice

If you are an eligible single parent in WA, look at the Family Home Guarantee early. It can save years.

But do not treat it as a shortcut to buy the biggest place a lender will allow. Use it to buy safely. The right result is not just getting the keys. The right result is still feeling in control six months later, when the first repair bill arrives and life keeps happening.

Preparing Your Application for Success

Most home loan applications rise or fall on three pillars. Deposit, income, and credit history. If one is weak, the other two have to work harder. If all three are organised, your application becomes much easier to place.

Deposit first, because it shapes everything

The deposit problem is often less about discipline and more about scale. As explained in this home buyer guide for single parents, a 20% deposit on a $700,000 home is $140,000, while a 5% deposit is $35,000. That gap is exactly why deposit-focused government support has become so important.

For a single parent, this changes the game. Saving the larger number can take too long, especially while paying rent. Saving the smaller number may still be hard, but it's often a target you can build a real plan around.

Income needs to look stable on paper

Lenders don't just want income. They want income they can verify and understand.

That means your application gets stronger when you can show consistency. Regular wages are straightforward. If your income includes other acceptable sources that a lender can assess, the documentation has to be clean and complete. The more your paperwork requires interpretation, the more friction you create.

A practical checklist helps:

- Payslips and bank statements: Make sure income landing in your account matches what you declare.

- Employment history: Stability helps. If you've recently changed jobs, be ready to explain the move clearly.

- Expense discipline: Lenders read your statements as behaviour, not just numbers. Frequent overdrawing, dishonours, or chaotic transfers tell a story you don't want told.

- Separation from old debts: If old joint accounts are still hanging around, deal with them before they create confusion.

Credit history is the part too many people ignore

Credit issues don't always mean a hard “no”, but they do narrow your options. Clean credit opens doors. Messy credit gives lenders a reason to hesitate.

If your credit file needs work, start before you apply, not after a lender declines you. Check your report, correct errors, and reduce small consumer debts that make your profile look stretched. Buy now, pay later accounts and personal debt often do more damage to serviceability than people realise.

If you want practical steps, this guide on how to improve your credit score in Australia is a useful place to start.

What a strong application looks like

A strong single parent home loan application usually has the same feel. Not flashy. Clean.

| Pillar | Weak application | Stronger application |

|---|---|---|

| Deposit | Unclear source, no buffer | Clear savings pattern, support scheme considered |

| Income | Irregular or poorly documented | Stable and easy to verify |

| Credit | Missed payments, too many small debts | Managed liabilities and clean repayment history |

Small fix, big impact: Before applying, trim avoidable monthly commitments. Even modest recurring debts can weaken serviceability.

Don't apply too early

Impatience often leads people to hurt their chances. They rush in because they've found a property or they're tired of renting. Then the application exposes loose ends that could have been cleaned up in advance.

A better approach is simple:

- Get your bank statements looking orderly.

- Know how much deposit you have access to.

- Check your credit position.

- Match your borrowing target to a property range that fits your life, not just lender maths.

Approval is easier when your finances tell a coherent story.

Strengthening Your Financial Position for the Long Term

Getting approved is not the finish line. It's the starting line.

Most single parent home loan content often falls short. It obsesses over approval and barely touches what happens after settlement. That's backward. The essential job is building a mortgage that you can live with.

According to the verified data provided for this topic, for many single parents the bigger constraint isn't the deposit but repayment resilience, and the RBA cash rate was 4.10% in June 2026, which is why affordability is so sensitive to income shocks and cost increases. That's the lens you should use. Not “Can I scrape through approval?” but “Can I hold this home together if life turns expensive?”

Stress-test your budget before the lender does

Your budget needs to survive more than the first repayment.

Run your future mortgage through real-life pressure points:

- School costs: They rarely arrive one at a time.

- Transport: One car problem can wreck a monthly plan.

- Childcare shifts: Care arrangements change, and costs can move fast.

- Medical or family interruptions: Single-income households feel disruption immediately.

If your numbers only work in a smooth month, the loan is too big.

Build repayment resilience on purpose

Repayment resilience means you have room to absorb stress without defaulting into panic. That room can come from cash savings, lower fixed commitments, a more conservative purchase price, or protection against a loss of income.

Many buyers find they need to get tougher with themselves. A lender may let you borrow more than you should. Don't treat the bank's maximum as your target. Treat it as the outer limit of risk.

A few actions make a major difference:

- Keep a post-settlement buffer: Don't drain every dollar into the purchase.

- Leave lifestyle inflation out of the plan: New home, new furniture, new spending is a bad combination.

- Attack costly debts early: If personal debt is eating cash flow, fix that fast. This guide on how to pay off debt faster can help you tighten that side of the budget.

- Review your insurance position: If you can't work, the mortgage doesn't stop needing to be paid.

Home ownership feels secure when your cash flow is resilient. Without that, the house can become another source of pressure.

Don't ignore the mental load

Single parents often internalize financial stress. That doesn't make it smaller. If the pressure starts affecting sleep, concentration, or decision-making, get support early. Practical financial planning matters, and so does emotional support. If that's something you need, this resource for support for anxiety and stress may be useful.

That's not separate from financial health. It's part of it. People make worse money decisions when they're exhausted and overwhelmed.

My strongest advice

Buy the home that lets you breathe.

Not the one that looks best on a listing app. Not the one that stretches you to the edge because “property always goes up”. Not the one that leaves you hoping nothing goes wrong.

Single parent home loans should be built around durability. If the loan survives real life, the home becomes an anchor. If it doesn't, the stress can undo the whole purpose of buying in the first place.

Your Path Forward to Home Ownership

A workable path to home ownership as a single parent is rarely a straight line. It usually looks more like this. Clean up the budget. Choose the right loan type. Check whether a scheme like the Family Home Guarantee fits. Prepare the application properly. Then make sure the repayments still work when life isn't tidy.

That last part matters most.

Much of the discussion around single parent home loans focuses on approval. But the deeper need is sustainability. The verified data for this topic notes that much content focuses on “can you qualify?” instead of “can you sustain it?”, and that 80% of Australia's 996,000 one-parent families in 2021 were mother-only families, which is why long-term mortgage safety is such an important and underserved issue, as referenced in this roadmap discussion.

Keep the process simple and realistic

You don't need to know every lending policy in the market. You do need to understand your own numbers and avoid the common traps. Overborrowing. Underestimating living costs. Chasing the wrong suburb. Assuming approval means safety.

If you're still learning the buying process itself, a plain-English Australian home buyer's guide can help you understand the steps and terminology without the usual confusion.

The right first move

Your best next step isn't applying blindly with multiple lenders. It's getting clarity.

That means answering a few direct questions:

- Can your income support the repayments comfortably?

- Does your target purchase price fit your real life?

- Would a guarantee pathway suit you better than a standard low-deposit loan?

- What needs to be improved before you apply?

- How will you protect the home if your income is interrupted?

If you can answer those properly, the rest of the process becomes cleaner. You stop guessing. You stop scrolling endless advice that doesn't fit your circumstances. You start making decisions based on a plan.

Owning a home as a single parent is achievable. But the safest path isn't the fastest path or the most aggressive one. It's the one built around clarity, resilience, and a mortgage you can live with.

If you want help turning all of this into a practical plan, Wealth Collective is a strong place to start. Their Perth and Dunsborough advisers help Australians make clear financial decisions around debt, protection, cash flow, and long-term planning. A free 10-minute introductory call is an easy first step if you want to test what's possible, understand your options, and build a path to home ownership that still feels safe after settlement.