Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

If you're an Australian investor staring at the usual menu of choices, the frustration is familiar. Cash feels safe but often underwhelming. Shares can build wealth, but they can also test your nerves at exactly the wrong time. Traditional bonds can play a role, yet many investors still ask the same practical question: where's the middle ground between low-return cash and full equity volatility?

That's where private credit investing starts to attract attention. Not because it's simple, and not because it's suitable for everyone, but because it sits in a part of the market many investors haven't properly examined. For discerning investors, it can offer regular income, less day-to-day market noise than listed assets, and a different source of return to shares.

The catch is that private credit isn't a plug-and-play holding. It's less liquid, more complex, and far more dependent on manager skill than a broad market ETF. If you're considering it for long-term wealth building or retirement planning, the key isn't chasing a headline yield. It's understanding what you're lending to, how you're being paid, and what could go wrong.

Searching for Returns in a Complex Market

Many investors come to private credit after a long period of feeling boxed in.

They've built wealth sensibly. They've used super, paid down debt, bought quality assets, and stayed invested through market cycles. But as portfolios grow and goals become more specific, the standard choices can start to feel blunt. You might want income without swinging fully into growth assets. You might want diversification without parking too much in low-yield cash.

That search often leads to alternatives, and private credit is now firmly in that conversation. It isn't new, but it has moved from the edges of institutional investing into a more visible role for family offices, SMSFs, and wholesale investors who want something between public bonds and equities.

Practical rule: If you can't clearly explain where the income comes from, you shouldn't allocate capital yet.

For many Australians, the appeal is straightforward. Private credit can provide contractual income from loans made to businesses or projects, often with terms negotiated privately rather than set by public markets. In plain English, you're being paid to lend money where a bank either won't lend, or won't lend on the same terms.

That doesn't make it safer than it sounds. In fact, one of the biggest mistakes investors make is assuming a smoother-looking return pattern means lower risk. Often it just means the asset isn't priced on a public exchange every day. The underlying credit risk is still there.

A more useful way to think about it is this:

- Cash protects liquidity: you can access it quickly, but the return may be modest.

- Shares drive growth: you accept volatility in exchange for long-term upside.

- Private credit seeks income: you trade liquidity and simplicity for potentially stronger contractual cash flow.

That trade-off can make sense in the right portfolio. It can also create problems if you've ignored your need for access to capital, upcoming retirement spending, or concentration risk. The sensible approach is to treat private credit as a specialist tool, not a cure-all.

What Is Private Credit Investing

Private credit investing is easiest to understand with one simple analogy. You are the bank.

Instead of putting money in a bank account and letting the bank decide who gets a loan, investors commit capital to a manager who lends directly to businesses. Those borrowers might be established private companies, property-related borrowers, or businesses that need customized financing a traditional lender won't provide.

Why this market exists

Private credit didn't appear by accident. The market expanded strongly after the Global Financial Crisis, when tighter bank lending and a lower-rate world created space for non-bank lenders. Brookings notes that global private credit assets under management grew from about US$375 billion to more than US$1.6 trillion by March 2023, and the market was estimated at about US$3 trillion at the start of 2025 in its analysis of what private credit is and the risks around it.

That growth tells you two things. First, borrowers value flexible capital. Second, large investors have decided the asset class deserves a serious look.

How the basic transaction works

Private credit is still lending. A borrower receives capital. The lender receives interest and, depending on the deal, other forms of compensation such as fees. The key difference is that the terms are privately negotiated rather than standardised through listed bond markets.

That means loans can be customised around security, repayment schedules, covenants, and borrower circumstances. It also means investors need to trust the manager's underwriting skill, because there's less public information and less ability to exit quickly.

A useful adjacent example is private real estate lending. If you want a practical view of the mechanics in that niche, this overview of how real estate debt funds work shows how managers structure loans, assess collateral, and generate income from debt rather than equity ownership.

Private credit isn't buying a story about future growth. It's lending against a set of agreed cash flows, protections, and legal rights.

What often confuses investors

The term sounds broad because it is broad. Not every private credit fund lends to the same type of borrower, uses the same security, or takes the same level of risk. Some strategies are relatively defensive. Others sit much closer to opportunistic or equity-like risk.

So when someone says they're investing in private credit, the follow-up question matters: what kind of private credit?

Exploring Private Credit Strategies

Private credit isn't one strategy. It's a family of strategies that sit at different points on the risk spectrum.

A good way to visualise this is the capital stack, which is the order in which investors get repaid if a borrower runs into trouble. The closer you are to the top of that stack, the earlier you may be repaid. The lower you sit, the more risk you usually take in exchange for higher potential return.

The Federal Reserve notes that private credit is dominated by senior term loans, which make up more than two-thirds of the market, and that post-default value for direct loans has been around 33%, compared with 52% for syndicated loans and 39% for high-yield bonds, in its review of private credit characteristics and risks. That's a strong reminder that seniority helps, but underwriting still matters enormously.

The main strategy types

Some strategies are designed to preserve capital first. Others are trying to capture more upside by taking subordinated risk, accepting weaker security, or lending into more complex situations.

| Strategy | Typical Risk Profile | Target Return | Position in Capital Stack |

|---|---|---|---|

| Senior secured direct lending | Lower relative risk within private credit | Lower relative return within private credit | First claim, usually secured |

| Unitranche loans | Moderate | Mid-range | Blends senior and subordinated exposure |

| Mezzanine debt | Higher | Higher | Below senior lenders |

| Special situations or distressed debt | Highest | Highest, but less predictable | Varies, often complex or stressed |

What each strategy means in practice

Senior secured direct lending

This is usually the starting point for investors who want private credit exposure without moving too far up the risk curve. The loan is commonly secured against assets or business value, and the lender sits near the front of the repayment queue.

If private credit were a building, this is the ground floor. It isn't risk-free, but it often offers the strongest lender protections.

Unitranche lending

A unitranche loan combines features that might otherwise be split between senior debt and subordinated debt. Borrowers like it because it simplifies their funding. Lenders like it because they may earn a higher blended return for taking on more complexity.

For investors, the catch is that the simplicity for the borrower often means a more nuanced risk position for the lender.

Mezzanine debt

Mezzanine sits below senior debt. That means if things go wrong, senior lenders are usually paid first. Because of that lower priority, mezzanine debt typically seeks a higher return.

This part of the market can suit investors who understand they are taking a step away from defence and closer to return-seeking credit risk.

Special situations and distressed debt

This is the specialist end of the spectrum. Managers may lend to stressed borrowers, fund restructurings, or pursue complex situations where standard lenders won't participate.

It's not the place to start if your main goal is stable retirement income.

A useful filter: Don't ask only, "What's the yield?" Ask, "Where am I in the repayment queue if this borrower struggles?"

If you want to get a feel for how broad the credit manager universe can be, tools like Gritt.io's database can help illustrate the range of lenders and fund types operating globally. The point isn't to shop from a list. It's to see how varied the ecosystem really is.

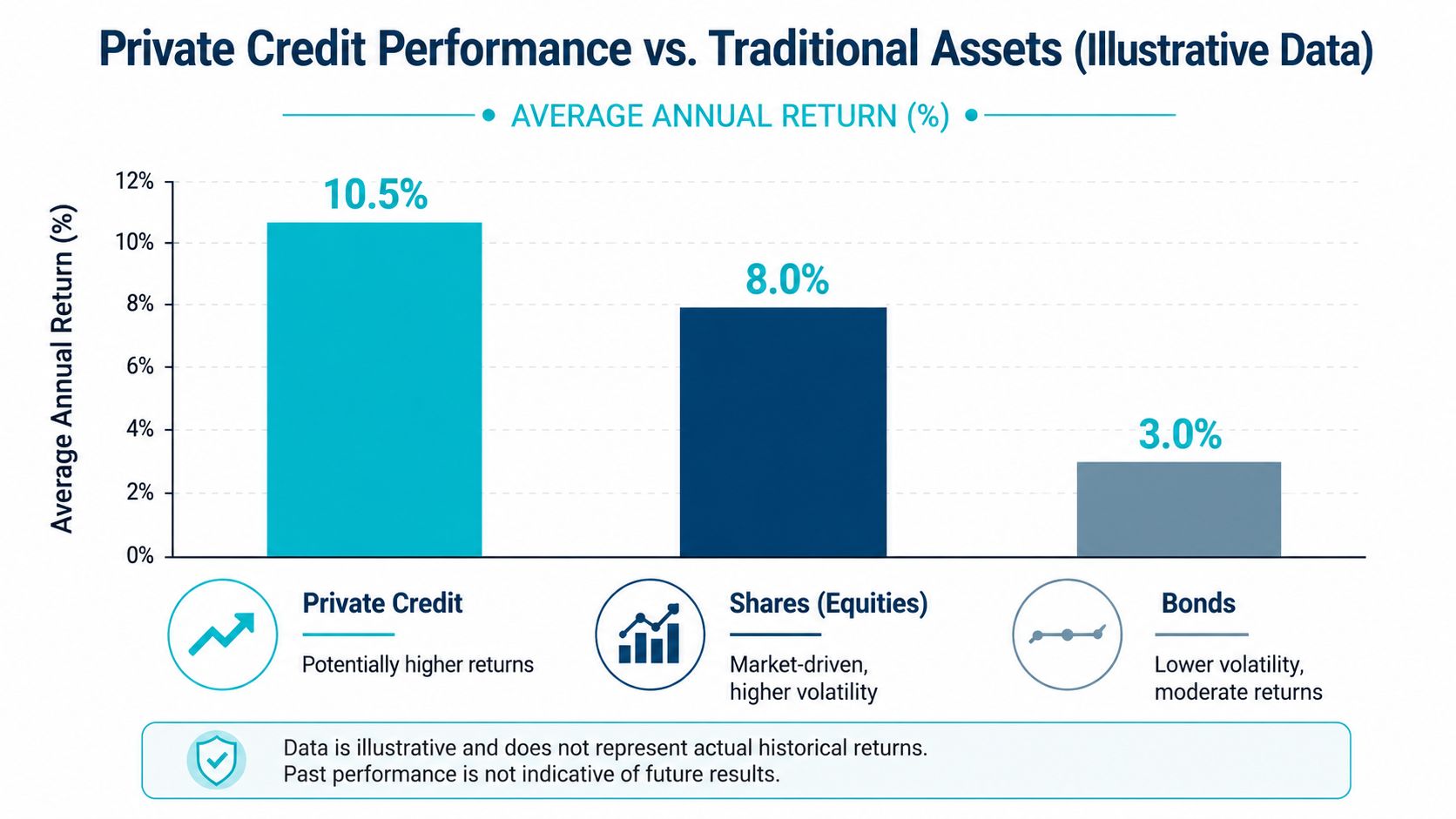

Performance Against Traditional Assets

The strongest case for private credit isn't that it always beats shares or replaces bonds. It doesn't. The case is that it behaves differently, and those differences can be useful in a diversified portfolio.

One of the most important structural features is that private credit is often floating-rate. That means the income paid to lenders can adjust as interest rates change. When rates rise, fixed-rate bonds can come under pressure because their coupons are locked in. Floating-rate loans don't have that same handicap.

Morgan Stanley notes that most private credit lending is floating-rate and that during seven periods of rising rates since 2008, direct lending returns averaged 11.6%, which was about 2 percentage points above its long-term average of roughly 9.6% in its private credit outlook and considerations.

Where the return comes from

Private credit returns are usually more contractual than aspirational. You're not relying on a market rerating a company upward in the same way an equity investor might. You're being paid through interest and loan economics agreed upfront.

That tends to create a different investor experience:

- Compared with shares: returns may look steadier because income is driven by loan payments rather than daily market sentiment.

- Compared with public bonds: yields can be more attractive, but the trade-off is less liquidity and heavier manager dependence.

- Compared with cash: the return potential is higher, but capital isn't available on demand.

Why investors often use it as a portfolio complement

Private credit can help fill the gap between growth assets and defensive assets. For some investors, it can act like an income-focused allocation with less visible volatility than listed markets. For others, it's a diversifier away from public market pricing.

That doesn't mean it belongs in every portfolio. If you're building a long-term strategy, it makes more sense to compare it with the role an asset needs to play, rather than chasing whichever line item has the highest projected income. A good starting point is understanding how each asset class supports your broader plan for long-term investment decisions.

Returns in private credit are often smoother on paper because loans aren't repriced daily. That shouldn't be confused with the absence of risk.

The key comparison most investors miss

Private credit often appeals to investors who say they want "bond-like income with more return". That can be true in some parts of the market. But the risk doesn't map neatly onto public bonds.

Public bond markets offer price transparency, easier trading, and broader benchmarks. Private credit offers bespoke terms, a possible income premium, and less daily price movement. What you gain in potential return and flexibility of deal structure, you give up in liquidity and simplicity.

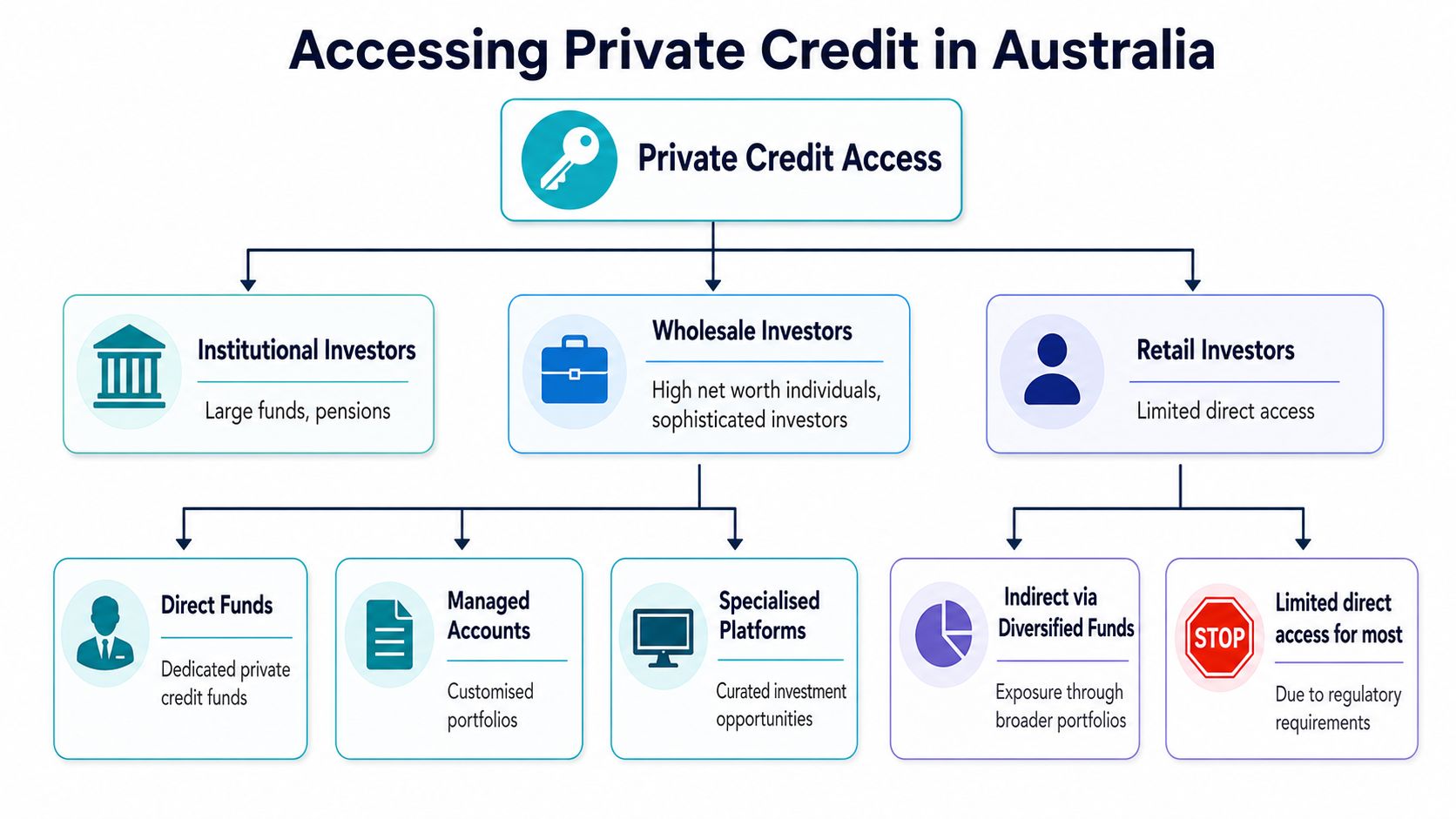

How to Access Private Credit in Australia

For Australian investors, the practical question isn't just whether private credit sounds attractive. It's whether you can access it in a sensible way.

In most cases, direct access sits with institutional, wholesale, or qualified investors rather than the average retail investor. That's because the underlying assets are complex, disclosure can differ from listed investments, and liquidity is limited.

The common access routes

Pooled private credit funds

This is the route most investors encounter first. A manager raises capital from multiple investors and builds a portfolio of loans. The main benefit is diversification across borrowers and deals rather than backing a single loan.

It's often the most practical entry point because the manager handles origination, due diligence, documentation, and monitoring.

Managed accounts or tailored mandates

Larger investors may use a managed account structure or a customized mandate. That can provide more control over sector exposure, risk settings, or liquidity terms, but it also requires more capital and more governance.

This route suits investors who want private credit integrated into a broader asset allocation framework, not merely bolted on as a standalone product.

Direct co-investment opportunities

Some experienced investors participate in specific deals alongside an established manager. That can offer sharper transparency on a given loan, but concentration risk rises quickly if you don't have a broad portfolio around it.

The access issue that matters most

CAIA notes that private credit funds commonly involve eight- to ten-year lock-ups with limited liquidity, and that global private credit AUM is projected to grow from $1.5tn in 2021 to $2.8tn by 2028 in its introduction to private credit strategies. That matters because access is only half the question. The other half is whether you can afford to lock money away.

For many Australians, this becomes especially important inside broader wealth structures, including super and SMSFs. If you're considering private assets in that context, it helps to understand the rules and strategic trade-offs around what an SMSF is, particularly before committing to an illiquid holding.

- If liquidity is critical: private credit may need to be a smaller allocation.

- If cash flow is predictable: a long lock-up may be easier to manage.

- If the portfolio is already heavy in illiquid assets: adding more may reduce flexibility when you need it most.

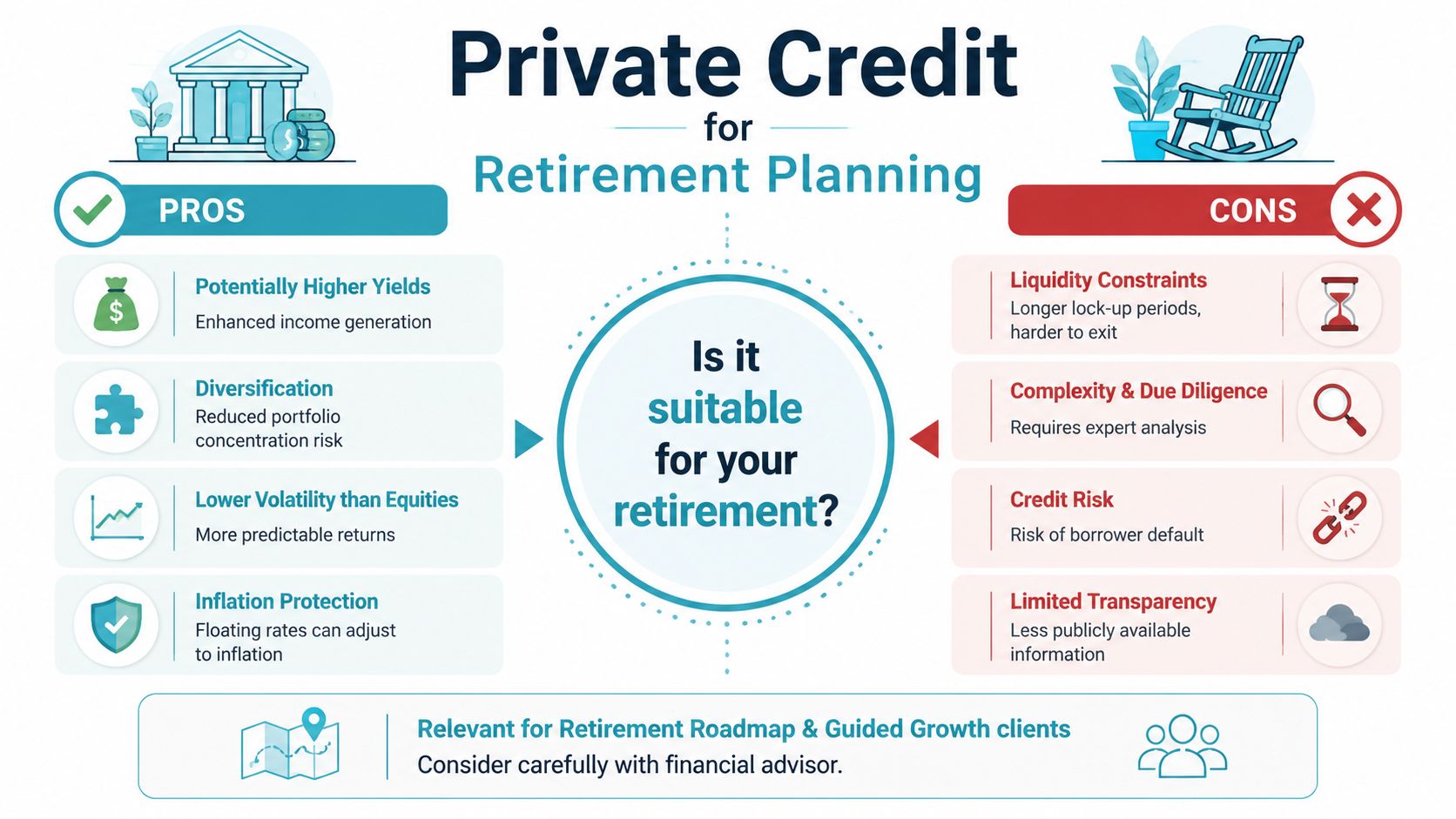

Is Private Credit Right for Your Retirement

Private credit can make sense in retirement planning, but only when it fits the job description.

If the job is to generate income, reduce reliance on share market dividends, and diversify return sources, private credit may be useful. If the job is to fund near-term spending, maintain emergency access, or keep the portfolio simple and liquid, it may be less suitable.

That distinction matters because retirement portfolios don't just need returns. They need usable cash flow, flexibility, and enough resilience to handle unexpected expenses.

Where private credit can help

A well-selected private credit allocation may provide income that feels more predictable than listed equity dividends. The contractual nature of loan payments can be attractive for retirees who prefer assets that are designed to pay them rather than rely on capital growth alone.

Voya estimates that investment-grade private placements have delivered an average total return advantage of 114 basis points over comparable public corporate bonds since 2001, made up of 81 bps of spread, 23 bps of non-coupon income, and 11 bps of lower losses in its guide to investment-grade private credit. That's important because it shows the return edge isn't just coupon. It also comes from fees, structure, and realised credit outcomes.

Where retirees need to be careful

Retirement is where private credit's weaknesses become harder to ignore.

Liquidity risk

You can't assume you'll be able to sell when you want to. If a large expense appears, or markets create a buying opportunity elsewhere, illiquid capital can become frustrating.

Manager risk

Two private credit funds can sound similar and behave very differently. The manager's borrower selection, covenant discipline, workout skill, and portfolio construction all matter.

Complexity

This isn't an asset class most retirees should choose on headline marketing alone. You need to understand the strategy, the borrower type, the security package, and how distributions are generated.

A retirement portfolio should never rely on an illiquid asset to fund immediate spending needs.

A balanced way to think about suitability

Private credit may suit retirement investors who:

- Have other liquid assets available: cash, listed investments, or accessible income reserves.

- Want income diversification: especially away from public market swings.

- Can tolerate complexity: either personally or with professional guidance.

It may be less suitable for people who need regular access to capital, have a short investment horizon, or want maximum transparency.

Retirement income planning works best when each asset has a clear purpose. If you're thinking about how different income sources interact over time, including super pension payments and portfolio withdrawals, it's worth understanding the broader mechanics of retirement income streams.

Your Due Diligence Checklist and Next Steps

By this point, the pattern should be clear. Private credit can offer useful income and diversification, but it asks a lot from the investor. You need patience, careful manager selection, and a realistic view of liquidity.

A sensible due diligence process starts with questions, not product brochures.

What to check before investing

- Strategy clarity: Is the manager focused on senior secured lending, unitranche, mezzanine, or something more opportunistic?

- Borrower quality: What types of businesses or assets sit underneath the loans?

- Security and covenants: What protections exist if a borrower underperforms?

- Liquidity terms: When can capital be redeemed, if at all?

- Fee structure: Are returns driven mainly by lending income, or is the structure relying heavily on fees and complexity?

- Portfolio construction: Is the fund diversified across borrowers, sectors, and loan vintages?

- Workout capability: What does the manager do when a loan doesn't go to plan?

The question behind all the other questions

The biggest issue isn't whether private credit is good or bad. It's whether it fits your life.

A strong investment can still be the wrong choice if it locks up money you'll need, duplicates risks you already have, or complicates a retirement plan that should stay flexible. Private credit investing works best when it's used deliberately inside a broader strategy for cash flow, tax, super, and risk management.

Good due diligence isn't just analysing the fund. It's analysing whether the fund belongs in your portfolio at all.

That last step is where many investors need a second set of eyes. Not because the asset class is impossible to understand, but because the consequences of getting the role wrong can take years to unwind.

If you're weighing whether private credit belongs in your portfolio, Wealth Collective can help you assess it in the context of your full financial life. That means your cash flow, super, debt, retirement timeline, and need for flexibility, not just the investment in isolation. If you'd like a clear, practical view on whether this strategy suits your goals, book a free 10-minute introductory call and start with a conversation that makes the complex feel manageable.