Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

A business can look stable right up until one person is suddenly out of the picture.

For many small businesses, that person is obvious. It is the founder who holds the client relationships, the senior operator who keeps jobs moving, or the rainmaker whose pipeline covers payroll, tax, and supplier commitments. If they die or become permanently disabled, the first problem is not theoretical. It is whether the business can keep trading without blowing up cash flow, breaching lending terms, or losing key staff while you work through the disruption.

Key person insurance is designed for that risk. The business takes out a policy on a person whose loss would cause financial damage, and the point of the cover is to give the business time, liquidity, and options. Used properly, it supports more than an immediate insurance payout. It should sit alongside small business cash flow management, debt planning, and operational resilience planning.

The detail that owners often miss is that the policy itself is only part of the job. In Australia, the tax treatment can change depending on why the cover is in place, and the ownership structure needs to match that purpose from the start. Get that wrong and the policy may still pay, but the commercial and tax outcome can be far less useful than expected.

That is why key person insurance should be treated as a business protection decision, not a box-ticking exercise. The right structure helps protect the business you have worked hard to build, and it gives you a clearer path if a loss triggers wider succession or ownership decisions.

Protecting Your Business from the Unthinkable

At 9:15 on a Monday, your operations manager is in hospital after a serious accident. By midday, client jobs are stalled because only they know the scheduling logic, two suppliers are waiting on approvals, and your lender wants to know who is now overseeing delivery and cash flow.

That is the risk key person insurance is built to address.

A business can survive the loss of an employee. It can struggle badly when the person lost is the one holding together revenue, delivery, lender confidence, or client relationships. In owner-led and specialist businesses, that exposure is often concentrated in one or two people, and it is rarely documented well enough until something goes wrong.

What the policy actually does

Key person insurance gives the business access to capital after the death or total and permanent disablement of a person whose loss would cause financial harm. In many cases, the business owns the policy, pays the premiums, and receives the proceeds. But that is not the only structure, and it is not always the right one. The ownership and purpose need to match from the start, especially if you want the tax outcome and the commercial outcome to work together.

The payout gives the business options at the point they matter most. It can fund wages, cover fixed commitments, support debt repayments, buy time to recruit, and steady relationships with clients and creditors while the business resets.

Practical rule: If losing one person would force you to inject cash, renegotiate with the bank, or pause delivery while you work out who can step in, you have a business risk worth pricing properly.

Why busy owners miss this

Owners usually see the risk. They just keep putting it behind more immediate decisions.

Sales targets, staffing issues, BAS deadlines, supplier problems, and financing conversations all feel more urgent. Protection planning gets delayed because nothing appears broken today. Then a medical event, accident, or sudden death turns a known dependency into a cash flow problem overnight.

A broader continuity review usually exposes this quickly. If you are already reviewing process gaps, leave risks, or single points of failure, a checklist for operational resilience planning can help identify where too much operational knowledge or revenue responsibility sits with one person. It also helps to test whether your small business cash flow management approach would realistically carry the business through three to six difficult months.

The goal is not to insure everyone. It is to identify the people whose absence would hit profit, operations, debt servicing, or business value hardest, then put the right funding structure in place before you need it.

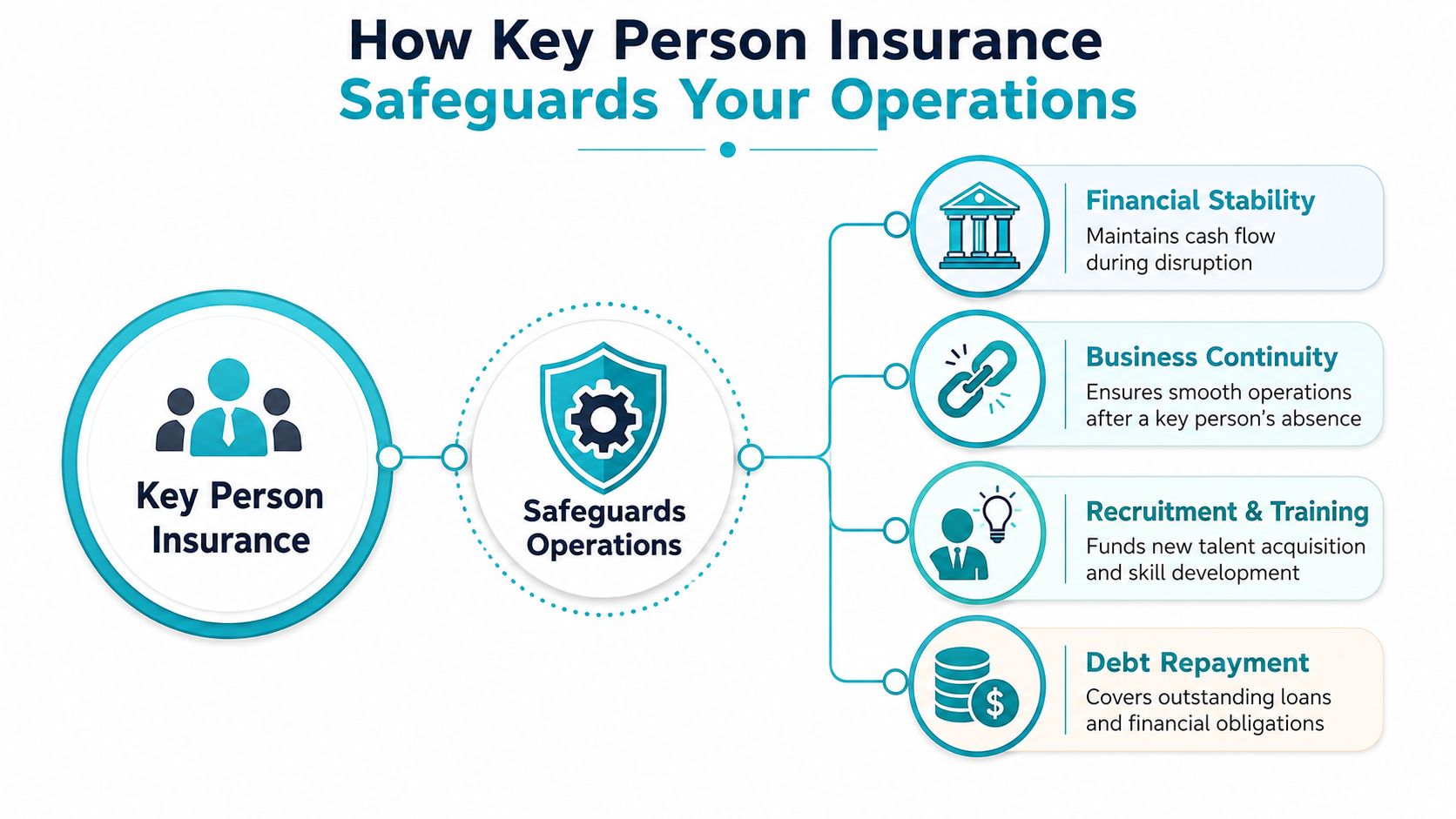

How Key Person Insurance Safeguards Your Operations

Insuring a key person is a lot like insuring a specialised piece of equipment. If an essential machine fails, you don't only pay to replace the machine. You also carry the cost of downtime, delays, missed output, and knock-on problems across the rest of the operation.

The same logic applies to a founder, top salesperson, technical lead, or senior operator. Their absence creates a chain of financial consequences, and the policy payout is there to absorb that shock.

What the payout is designed to cover

A well-structured policy usually supports several business needs at once:

- Lost profits: Revenue often drops before expenses do. Insurance proceeds can buy time while the business adjusts.

- Recruitment costs: Replacing a senior or specialist person usually means search fees, management time, and a slower sales or delivery cycle during the handover.

- Training and transition: Even a strong replacement takes time to become productive.

- Debt and lender confidence: If a bank or financier is worried about continuity, available capital matters.

- Operational breathing room: The business may need to reassign work, bring in contractors, or temporarily reduce capacity.

Why this matters more than many owners think

Dependence on a small number of people is common. Formal protection is not. The Insurance Information Institute reports that 71% of surveyed small businesses were very dependent on one or two key people for their success, yet only 22% had key person life insurance, according to the III guide to life insurance for key employees.

That gap is easy to understand in real businesses. Owners assume they'll “work something out” if something goes wrong. Sometimes they do. Sometimes they end up making rushed decisions from a weak cash position.

If a key person is more likely to be sidelined by illness than death in your business, disability features deserve serious attention, not an afterthought.

Policies can include disability benefits as well. The same III guide notes that such benefits can replace 40% to 70% of a disabled employee's earned income, depending on policy design. That matters because many business disruptions come from long absences, not only death.

What works and what doesn't

The policy works well when the owner has already defined the business problem. Who is exposed. What cash pressure would follow. How long replacement would take. Which debts or commitments would still need funding.

It works poorly when cover is bought as a generic box-ticking exercise. A policy with no clear purpose often ends up underfunded, mismatched to the risk, or structured in a way that creates problems later.

Who Is a Key Person in Your Business

A key person isn't always the person with the biggest title. It's the person whose sudden absence would do outsized financial damage.

In smaller Australian businesses, that often falls into one of three patterns.

The founder with the hard-to-replace capability

A Perth software business might revolve around a founder who built the core product architecture and still handles the most complex client conversations. On paper, there's a team. In reality, the founder holds the commercial trust and the technical judgment that keeps projects on track.

If that founder is gone, the business may face delayed releases, stressed clients, and a difficult handover because nobody else fully understands the product at the same depth. The risk isn't just salary replacement. It's delayed revenue and reduced confidence in the business itself.

The operator who keeps delivery moving

A construction or trade business in the South West may depend on one project manager who coordinates subcontractors, solves site problems, and keeps customers calm when schedules shift. Remove that person and the whole rhythm of the business changes.

Jobs can still exist on paper, but margins start leaking. Variations get missed. Timelines slip. Admin staff spend time firefighting instead of supporting profitable work. In many trade businesses, that one person protects both revenue and reputation.

A key person is the person you can't replace quickly without the business becoming more fragile.

The rainmaker who brings in the work

Professional services firms often have one adviser, principal, or senior relationship manager who consistently wins new business. They may not own the firm, but they drive pipeline and retention in a way no one else does.

If that person leaves through death or disability, the effect can show up in stages. Existing clients become unsettled first. New work slows next. Then the leadership team realises future revenue is thinning while fixed costs stay put.

A simple test you can use

Ask these questions about any role you're considering:

- Revenue impact: Does this person directly generate sales, retain major clients, or influence repeat work?

- Knowledge concentration: Do they hold specialist know-how that isn't documented or easily transferred?

- Leadership dependence: Would the team stall without their decisions or approvals?

- Lender or stakeholder exposure: Would financiers, partners, or investors become concerned if this person disappeared from the business?

If the honest answer is yes to one or more, you may have a key person exposure. The role could be a founder, salesperson, technical expert, production lead, or even an office manager in a tightly run business. The title matters less than the consequence of losing them.

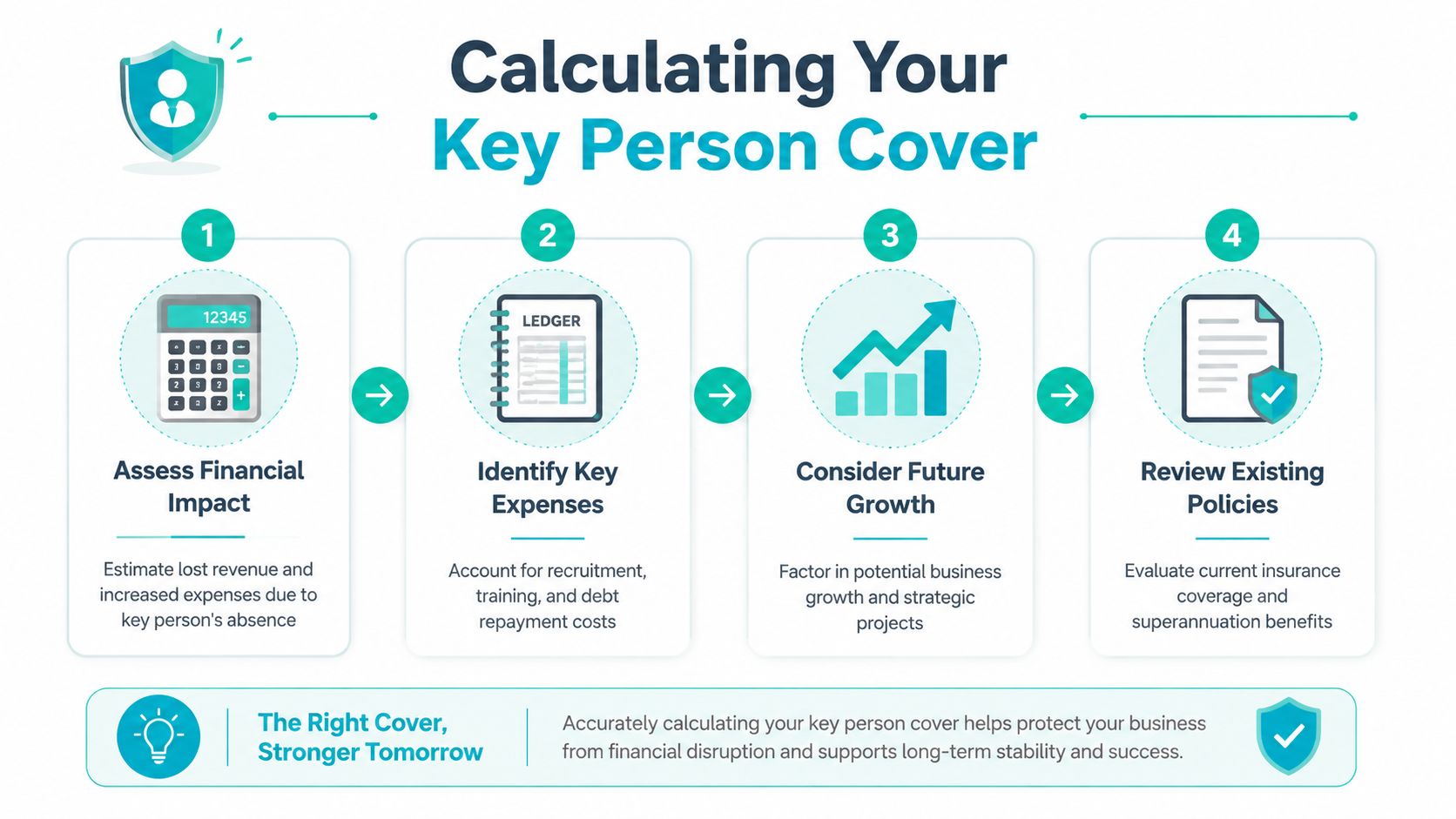

How to Calculate the Right Amount of Cover

A rough number is easy to get. The harder job is choosing an amount that would keep the business stable if a key person died, became disabled, or could not work for an extended period.

I usually start with a simple question. What would this loss cost the business over the next 6 to 18 months?

That framing gets owners away from guessing based on salary alone. Pay matters, but key person cover is really about business exposure. The right figure often needs to cover lost profit, replacement costs, pressure on cash flow, and the time it takes to rebuild client confidence or operational capacity.

Start with a benchmark, then pressure-test it

A salary multiple can be a useful first pass. Some insurers and industry guides suggest a range of several times annual remuneration for key staff, particularly where there will be a long handover, search, and ramp-up period.

That is only a starting point.

For a senior technician, lead adviser, or founder-type rainmaker, the full cost can sit well above a simple multiple of salary. For a manager in a mature business with documented systems and strong second-line support, it may be lower. The number should reflect how the business earns money and how quickly that person can be replaced.

A practical calculation framework

Work through four areas.

Profit at risk

Estimate the profit likely to disappear while the business adjusts. Focus on the work that would be delayed, cancelled, or won at lower margins without that person.Replacement and transition cost

Add recruiter fees, advertising, sign-on incentives, temporary contractors, training time, and the hours senior staff will spend covering the gap.Fixed financial commitments

Include debt repayments, lease costs, wages, and supplier obligations that continue even if revenue drops. This is often where underinsurance shows up first.Strategic interruption

Put a dollar figure on delayed projects, stalled expansion plans, or major client relationships that may weaken during the transition.

A simple working table keeps the discussion grounded:

| Factor | What to estimate |

|---|---|

| Lost output | Reduced revenue or delayed work during absence |

| Hiring cost | Search, recruitment, and onboarding expenses |

| Training lag | Lower productivity until the replacement is fully effective |

| Financial commitments | Loans, fixed overheads, and contractual obligations |

The trade-off owners need to get right

Too little cover leaves the business funding a major shock from working capital at the worst possible time. Too much cover can mean paying for protection that does not match the actual risk, and in Australia that also creates avoidable tax and structuring problems if the purpose of the policy is not clearly defined.

That is why I prefer to separate the need into buckets. One amount for short-term revenue disruption. One for debt or fixed costs. One for recruitment and handover. Once those numbers are visible, it becomes much easier to decide whether the policy should cover temporary business interruption, a longer replacement window, or part of a broader succession plan.

If you also want to understand how deductibility can change depending on the purpose of the cover, our guide on whether life insurance premiums are tax deductible in Australia is a useful companion.

What affects premium cost

Premium pricing usually comes back to the insured person's age, health, occupation, sum insured, policy type, and how long the business needs the protection in place. Adding total and permanent disability or trauma-style protection can also change both cost and policy design.

The practical mistake is choosing a premium first and then forcing the cover amount to fit the budget. A better approach is to calculate the exposure, decide what risk the business can self-fund, and insure the rest. That produces a cover amount tied to a real business problem, not an arbitrary number.

Navigating Tax Rules and Policy Ownership in Australia

Many online explanations become too simplistic. They define the policy correctly, then skip the part that determines whether the arrangement will do what the owner expects.

The ownership structure matters. The tax purpose matters. The paperwork matters.

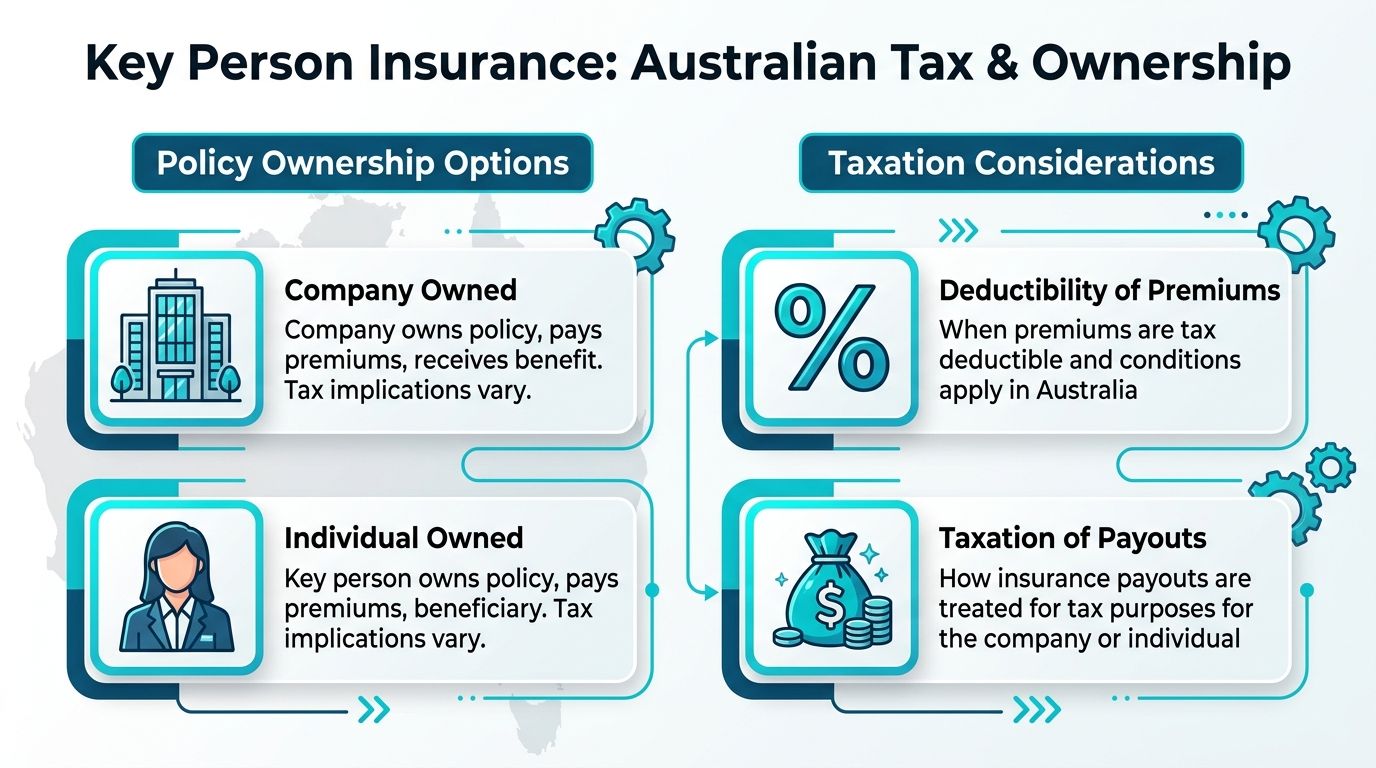

Who owns the policy and who gets paid

In a standard key person arrangement, the company owns the policy, pays the premiums, and receives the payout. The benefit doesn't go to the employee's family. It goes to the business.

That sounds straightforward, but ownership drives the tax analysis. If the policy is employer-owned, you need to be clear about why the cover exists and how it has been documented.

The tax issue most owners overlook

In Australia, key person insurance premiums are generally not tax-deductible, and proceeds may be taxable unless the policy is structured strictly for business revenue protection purposes, based on the rules described in the Wikipedia summary on key person insurance. That same source states an estimated 40% of policies fail to meet this test, which can lead to unexpected Capital Gains Tax liabilities.

That's the practical trap. Many owners think, “If the company owns it, the company gets paid, problem solved.” It isn't that simple. If the policy purpose isn't documented correctly, or if the arrangement drifts between capital protection and revenue protection, the tax treatment may not line up with what you intended.

For a broader explanation of related insurance tax issues, this guide on whether life insurance is tax deductible is useful background. Key person cover has its own nuances, but the same principle applies. Structure matters as much as product choice.

Generic advice fails here because it treats key person insurance as a policy decision. In reality, it's also a tax and governance decision.

What to get right before you apply

Before any application is finalised, the business should have clarity on:

- The purpose of cover: Is the policy meant to protect revenue, protect capital value, support debt, or fund continuity?

- The owner and beneficiary: These must match the business objective.

- Written records: The rationale for the policy should be clear and consistent.

- Consent: The insured person must understand the arrangement and agree to it.

If those details are vague, the policy may still get issued, but the result can be messy when a claim occurs. The businesses that handle this well treat it like a risk-management document first and an insurance product second.

Beyond Key Person Cover Your Next Steps

Key person cover is important, but it shouldn't sit by itself. The best protection plans connect insurance to the rest of the business.

That usually includes succession planning, documented authority lines, better process transfer, and sometimes a buy-sell agreement if ownership is tied to the person being insured. Insurance provides liquidity. Succession planning decides what happens next.

What key person insurance does not solve

A payout can help with continuity, but it won't automatically solve:

- Ownership disputes: If a shareholder or partner is the key person, separate legal planning may be needed.

- Knowledge gaps: If no one else understands the role, money alone won't fix the delay.

- Client concentration: If relationships sit with one person, the business still needs a transfer plan.

- Leadership vacuum: Teams need decision-makers, not only funds.

That's why it makes sense to pair insurance with documented handover plans and critical business succession strategies that address governance, people, and ownership together.

The practical next move

A common gap in understanding key person insurance is its tax treatment and ownership structure. Guidance that stops at the definition leaves out the governance details that determine whether the policy is useful, including the fact that the payout goes to the business rather than the employee's family and that the insured person's written consent is required, as explained in Nationwide's overview of key person insurance.

If you're already thinking about continuity, it's worth treating this as part of the bigger planning picture rather than a one-off insurance quote. A helpful starting point is understanding how key person cover sits alongside succession planning for business owners, especially where leadership, ownership, and family interests overlap.

The businesses that usually get this right do three things well. They identify the key points of dependency. They choose cover for a specific business purpose. They document ownership and tax treatment carefully enough that the policy will still work when it's needed.

If you want a personalized view of whether key person insurance fits your business, Wealth Collective can help you assess the risk, pressure-test the ownership and tax structure, and map it into a broader Protection Plus strategy. A free 10-minute introductory call is a simple way to work out what needs attention now, what can wait, and how to protect the business you've worked hard to build.