Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You might be in this exact position right now. You've remarried or partnered later in life. There's a home, super, perhaps an investment portfolio, maybe an adult child from your first relationship and younger children in your current one. Everyone gets along well enough, and you assume a will sorts it out.

It often doesn't.

In blended families, the biggest estate planning mistakes aren't dramatic. They're ordinary. A house owned the wrong way. Super left to trustee discretion. A stepchild assumed to be “covered”. A will that says one thing while the actual money sits somewhere the will can't control. That's where good intentions fail.

Why Standard Wills Fail Blended Families

A standard will works reasonably well for a straightforward family. One spouse, shared children, simple asset pool. Blended families are different because your plan has to do two jobs at once. It has to protect your current partner and preserve the inheritance you want for children from an earlier relationship.

That tension is where generic documents break down.

According to the 2021 Australian Census data, over 10% of families with dependent children in Australia are classified as blended or step-families, a structural reality that significantly complicates estate distribution and increases the risk of family provision claims against a will, as noted by Moores on estate planning strategies for blended or step-families.

Good intentions don't control asset flow

A common example looks like this. A husband leaves everything to his wife because he wants her secure. He trusts she'll “do the right thing” later and leave the balance to his children. Then she survives him by many years, rewrites her will, or has assets pass under her own arrangements. His children receive far less than intended, or nothing at all.

That result isn't unusual. It's built into poor structuring.

If the family home is held as joint tenants, the deceased's share usually passes automatically to the surviving owner. It doesn't wait for the will. It doesn't ask what the deceased intended for children from the first relationship. It just transfers.

Standard wills often fail blended families because they deal with wishes, not control.

That's why estate planning for blended families needs more than a document signing session. It needs asset-by-asset design.

The emotional risk is as serious as the legal one

People don't only fear legal disputes. They fear the family fracture that follows. Children may believe a new spouse influenced decisions. A surviving spouse may feel attacked for trying to remain secure in the home. Stepchildren may assume they're included when legally they're not.

If you want a practical legal overview to secure your blended family's legacy, that resource is worth reading alongside financial advice.

And if you haven't even addressed the basics yet, start with understanding what happens if you don't have a will. In a blended family, dying intestate doesn't simplify anything. It removes your voice when your family needs clarity most.

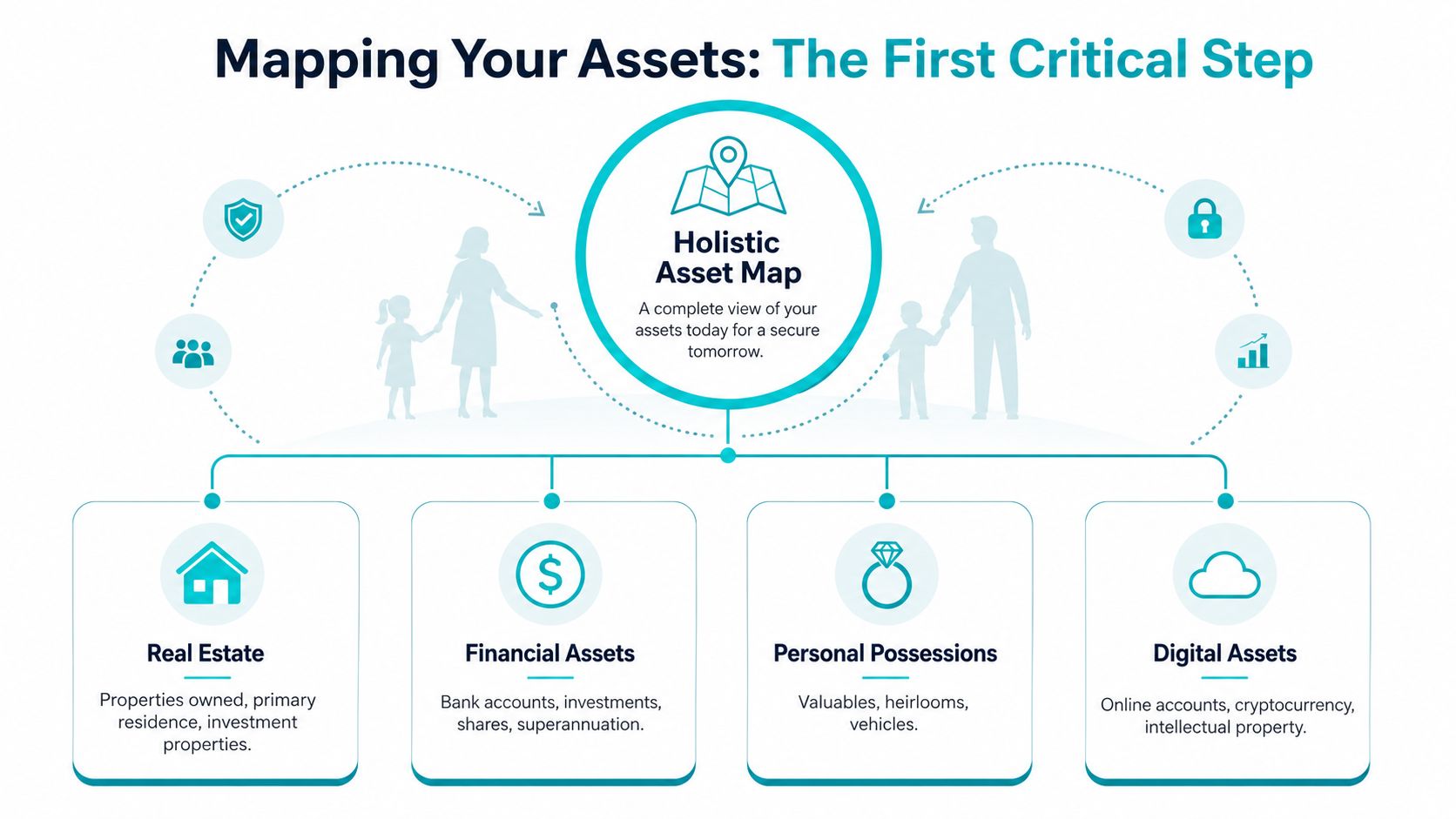

Mapping Your Assets The First Critical Step

Many individuals begin estate planning by updating their will. That's the wrong starting point.

The first job is to build a holistic asset map. You need to know what you own, how you own it, who controls it on death, and whether your will has any authority over it. Without that map, you're planning blind.

A critical step-by-step methodology for blended family estate planning begins with mapping the full asset base, not just the estate, by separating estate assets from superannuation, insurance, and trust-held assets before taking any other action. Experts also assert that updating a will alone is a significant planning gap, as explained in this blended family inheritance guide.

Split your world into two buckets

The cleanest way to start is this simple divide:

| Asset bucket | Typical examples | Controlled by your will |

|---|---|---|

| Estate assets | Sole bank accounts, personal investments, your share of property, personal items | Usually yes |

| Non-estate assets | Superannuation, life insurance nominations, trust assets, company interests | Often no, or not directly |

That distinction changes everything.

A will can direct estate assets. It usually can't override super trustee decisions, trust deeds, or beneficiary nominations sitting elsewhere. If your largest asset is super, then your estate plan is only partly in your will.

Build the map properly

You don't need legal jargon first. You need a list.

- List every asset and liability. Include the home, cash, shares, super, life insurance, trusts, company interests, debts, and digital assets.

- Record ownership structure. Sole name, joint names, trust, company, or super fund.

- Check the control mechanism on death. Will, nomination, trust deed, company constitution, or automatic survivorship.

- Identify intended beneficiaries. Not who you assume receives it. Who receives it under the current paperwork.

Practical rule: If you haven't mapped an asset, don't assume your will controls it.

People often discover the gaps. They realise the home passes one way, super another, life insurance somewhere else, and trust assets according to a deed no one has reviewed in years.

Moving house later in life can add another layer of confusion because paperwork gets scattered between storage, solicitors, and family files. If that's your situation, practical admin matters too. Even a guide on long term storage for your NSW move can help you think more carefully about where critical records end up.

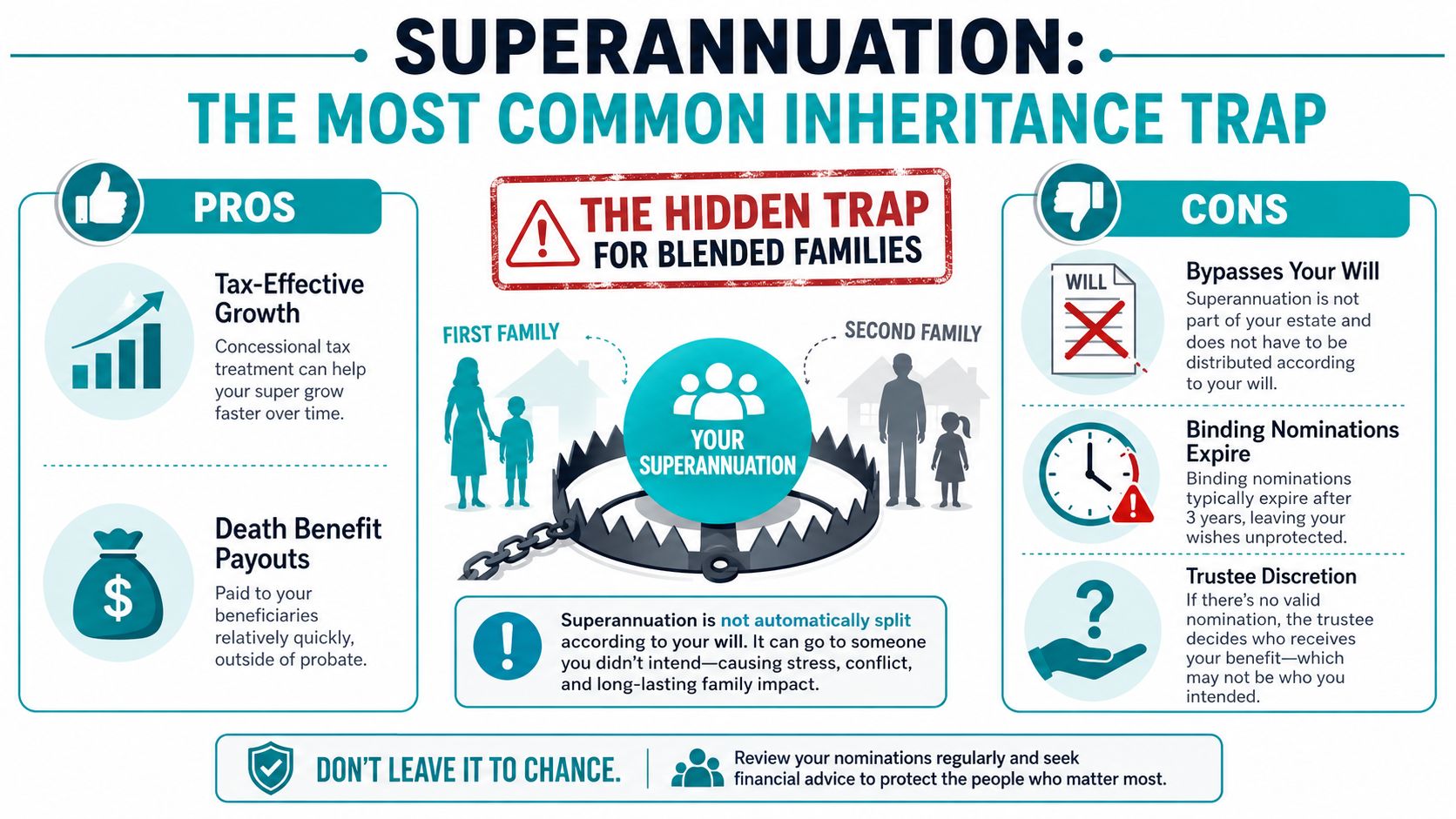

Superannuation The Most Common Inheritance Trap

This is the issue people miss most often, and it causes some of the ugliest disputes.

Your will does not automatically control your superannuation. Super sits outside your estate unless it's paid there. In many cases, the fund trustee decides who receives the death benefit unless you've made a valid Binding Death Benefit Nomination, or BDBN.

That means you can have a beautifully drafted will and still get the biggest asset wrong.

Recent data from the Australian Institute of Family Studies indicates that 42% of blended family members in Western Australia have no valid Binding Death Benefit Nomination, and the 2024 Superannuation Guardian Report found that 31% of blended family disputes in Australia stem from undefined superannuation nominations.

Why wills and super often point in different directions

Here's the trap. Your will might leave your estate equally to your children, or partly to your spouse and partly to children from a prior relationship. Meanwhile your super nomination may be missing, expired, invalid, or directed elsewhere entirely.

When that happens, the family assumes the will settles everything. It doesn't.

A trustee may pay the super death benefit to the current spouse. That may be lawful. It may also be the exact opposite of what the deceased thought would happen.

If you want the mechanics explained in plain English, read what happens to super when you die. It's one of the most misunderstood parts of estate planning in Australia.

What a BDBN actually does

A valid BDBN tells the trustee who should receive your super death benefit, subject to the governing rules. It's separate from your will. It needs its own attention. And in blended families, it should be treated as a frontline document, not an administrative afterthought.

Focus on these points:

- Check validity: A nomination that's old, unsigned, or inconsistent with fund requirements can fail when your family needs it most.

- Match the broader plan: Your BDBN, will, insurance beneficiaries, and property ownership should push in the same direction.

- Review after family change: Remarriage, separation, and changes in dependency should trigger a full review.

If your super is your largest asset, ignoring your BDBN means ignoring your estate plan.

The DIY mistake that keeps repeating

People often say, “I updated my will last year.” That tells me almost nothing. The better question is, “Did you review your super nominations, insurance beneficiaries, and non-estate assets at the same time?”

If the answer is no, the plan is incomplete.

For blended families, superannuation is not a side note. It's usually the central risk. If your children from a prior relationship are meant to benefit, or your current spouse needs security without receiving everything outright, super has to be coordinated with legal and financial advice from the start.

Your Legal Toolkit Wills Trusts and Property Ownership

A common blended-family failure goes like this. The will says one thing, the house title does another, and super sits outside both. The family assumes the documents work together. They do not unless you set them up that way.

Your legal toolkit needs to control the assets your will can govern, protect the people you want to protect, and reduce the room for later arguments. For most blended families, that means a well-drafted will, the right property ownership structure, and often a testamentary trust.

Compare the main tools properly

| Tool | Best use | Main strength | Main limitation |

|---|---|---|---|

| Specialised will | Directing estate assets with clauses specific to your family | Records clear instructions and can include occupation rights | Does not control every asset |

| Testamentary trust | Protecting children's inheritance while supporting a spouse | Adds control, tax flexibility, and asset protection after death | Needs proper drafting and administration |

| Tenants in common | Structuring property ownership between partners | Each owner's share can pass under their will | Needs coordination with the survivor's housing needs |

A standard will is usually too blunt

A simple will that leaves everything to a spouse is often the wrong answer in a blended family. It may keep things easy in the short term, but it also gives away control. If the survivor later changes their own will, remarries, or faces creditor pressure, the children from the first relationship can miss out entirely.

Clauses such as a right to reside or a life interest can deal with this directly. They can let a surviving partner stay in the home, with clear rules around expenses, downsizing, or aged care, while preserving the underlying capital for the children you intend to benefit.

That is the balance you want. Security for the survivor. Protection for the children.

Testamentary trusts solve the problem a basic will cannot

For many blended families, a testamentary trust is the strongest planning tool available because it separates use of an asset from final ownership. A spouse can receive income, housing rights, or limited access to capital. The asset itself can still be preserved for children under rules you set in advance.

If you want a practical explanation of how that structure works, read what is a testamentary trust in Australia.

This is not complexity for appearance's sake. It is control with a purpose. In blended families, that usually means stopping assets from drifting away from the bloodline you intended to protect, while still treating a current partner fairly.

The right structure removes guesswork at the exact point your family can least afford it.

You should also protect the records behind the plan. Wills, trust documents, nomination forms, scanned IDs, and family correspondence contain sensitive information that can cause real harm if handled badly. These File Studio document privacy tips are a sensible reminder that secure storage and sharing matter too.

Property ownership can override your intentions

Property law catches families out because the title often stays untouched for years. Then one death changes everything.

If the family home is owned as joint tenants, the deceased person's share usually passes automatically to the surviving owner. That happens outside the will. If your intention was for your share to pass to your own children, joint tenancy can defeat the plan completely. Holding property as tenants in common gives each owner a defined share that can pass under their will instead.

This point matters more in blended families than almost anywhere else in estate planning. The wrong ownership structure can cancel out good drafting.

Review the title, not just the will. If the property was set up years ago when the family situation was different, fix it now. Life insurance can also help where the home needs to stay available for a spouse but other beneficiaries need a fair outcome through a separate pool of cash.

How to Define Fairness and Prevent Family Disputes

The legal structure matters. It isn't enough.

You also need to decide what fair means in your family. Fair is rarely the same as equal. One child may have already received substantial support. A current spouse may need housing security. A stepchild may have been raised as your own even if the law doesn't treat them that way by default.

If you don't define your own version of fairness, conflict fills the gap.

Stepchildren are often assumed in and legally left out

This is one of the most dangerous assumptions in estate planning for blended families. Many people treat stepchildren as full family members in everyday life and assume the law does the same. It often doesn't.

A 2025 LawConnect Australia study revealed that 68% of stepchildren in blended families in Western Australia are not automatically entitled to inherit, and only 29% of blended family wills in Australia explicitly include stepchildren, creating a high risk of litigation.

That tells you exactly why vague intentions are not enough. If you want a stepchild to inherit, name them clearly and structure the plan to support that outcome. Don't leave room for argument.

Equality can create unfairness

A strict equal split can sound neat and still produce a poor result. Consider these possibilities:

- Housing need differs: A surviving spouse may need the right to stay in the home, while adult children may be financially independent.

- Family history differs: One branch of the family may have already received earlier support, gifts, or business opportunities.

- Emotional expectation differs: A stepchild who has been treated as your child for years may feel blindsided if the documents say otherwise.

A plan can be legally valid and still feel like a betrayal to the people left behind.

That's why I strongly favour documenting not just the outcome but the reasoning.

Communication prevents more disputes than clever drafting

Most family fights begin in silence. Someone dies, a document surfaces, and the people affected hear the plan for the first time from a lawyer or executor.

That's avoidable.

Use simple steps:

- Hold a family conversation: You don't need to disclose every dollar, but key people should understand the broad logic.

- Write a letter of wishes: This can explain values, intentions, and why one person receives use of an asset while another receives capital later.

- Choose the right executor or trustee: Pick someone who can manage tension, not just paperwork.

A calm discussion while everyone is alive is far cheaper than a bitter dispute after death. Of greater significance, it gives people context. Context doesn't remove disappointment, but it often removes suspicion.

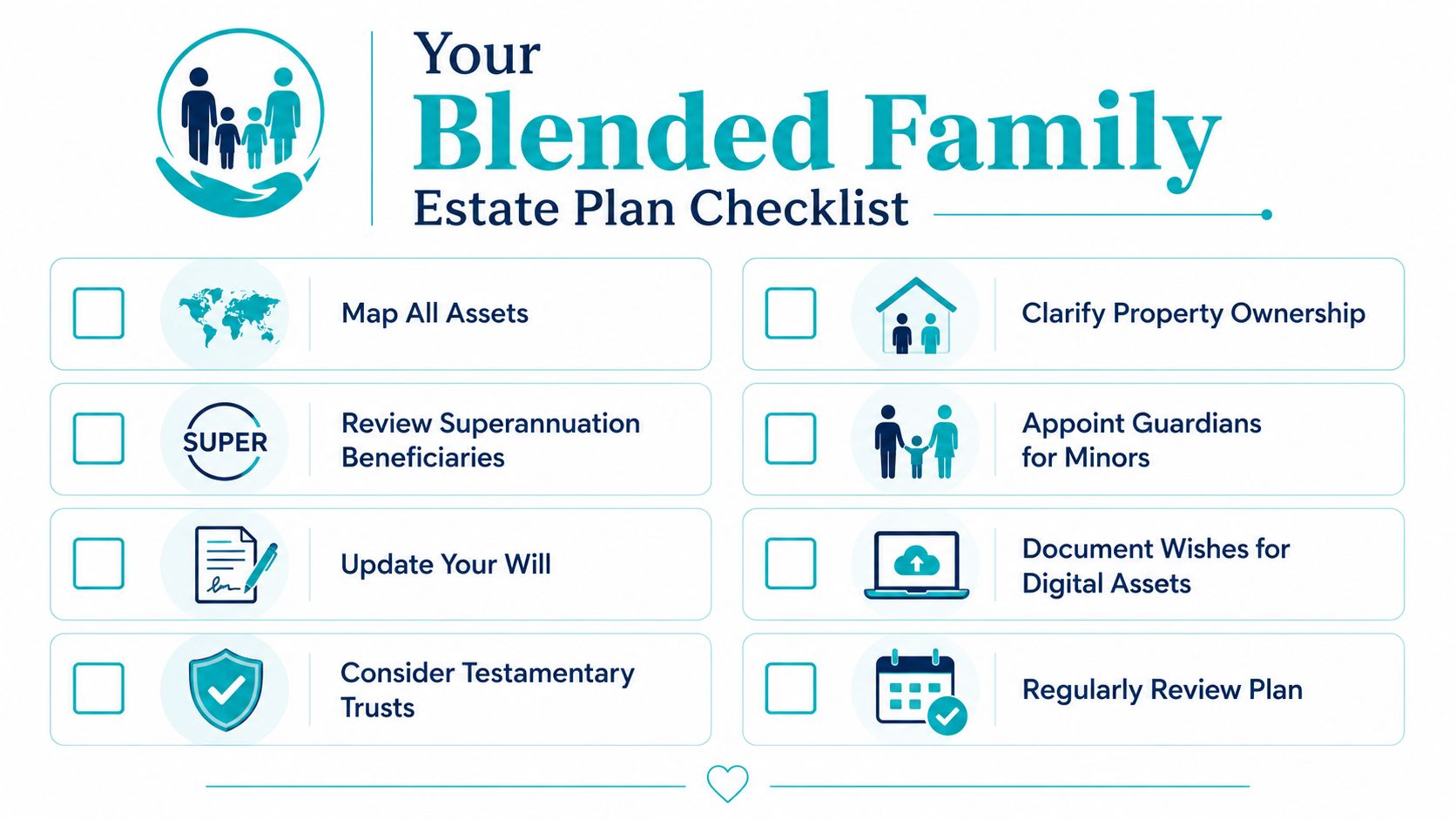

Your Blended Family Estate Plan Checklist

A blended family estate plan usually fails in one place. The will says one thing, but the assets that sit outside the estate go somewhere else.

That mismatch is the trap.

A surviving spouse can receive the house under the will while super goes to adult children under an old nomination. Or the will can divide everything evenly between children while a jointly owned property passes automatically to the new partner. Families do not expect these conflicts because they assume the will controls all assets. It does not.

Use this checklist

- List every asset by control method: Mark what passes under your will, what passes by super nomination, what is held in trust or a company, what is owned jointly, and what has a named beneficiary.

- Check your BDBN first: Make sure your super death benefit nomination is valid, current, and consistent with the outcome you want for your partner and your children.

- Review life insurance ownership: Confirm whether cover sits inside super or outside it, and who controls the payout.

- Check property ownership: Confirm whether the family home and other real estate are held as joint tenants or tenants in common.

- Update your will for a blended family: Generic spouse-first wills create problems. Use drafting that reflects second relationships, prior children, and any staged inheritance you want.

- Consider a testamentary trust: If you want to support a surviving partner without losing control of what ultimately passes to children, examine this properly.

- Name stepchildren explicitly if that is your intention: Assumptions fail. Clear drafting works.

- Record your reasoning: A letter of wishes gives your executor and family context, especially where outcomes are unequal.

- Decide who needs to know now: Quiet clarity beats loud conflict later.

- Organise originals and account details: Your executor needs signed documents, account information, and contact details for advisers and the super fund.

Put your review cycle in the diary

Review your plan every three to five years, and sooner after any major change.

Remarriage, separation, estrangement, a property sale, retirement, a new grandchild, aged care planning, business restructuring, or changes to super can all break the alignment between your will and your non-estate assets. In blended families, that alignment matters more than the document count. One outdated nomination can undo a carefully drafted will.

Treat reviews as risk control. If your family structure, asset mix, or intentions have changed, your documents should change too.

Book a complimentary initial call with a Wealth Collective adviser.

If you want clarity on super, estate structures, and how to protect both your partner and your children, speak with Wealth Collective. A short initial call can help you identify the weak points in your current setup and decide what needs financial advice, legal drafting, or both.