Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You're probably not reading about critical injury insurance for fun.

More often, it's because life feels busy and expensive, and a small part of you knows the plan might not hold if someone in the family gets seriously ill. In Perth and across WA, I see the same pattern. People have a mortgage, kids in school or childcare, rising living costs, maybe a decent income, and a rough assumption that Medicare, sick leave, super, and a bit of savings will carry them through.

Sometimes they won't.

A weekend in Dunsborough, a routine scan, a sudden stroke, a heart event, a cancer diagnosis. The health issue lands first. The money issue follows immediately. Who covers the mortgage while one income drops? Who pays for travel, treatment gaps, rehab, extra care, or time off for the healthy spouse who suddenly becomes the organiser of everything?

Your Financial Shield Against the Unexpected

A WA family can be doing everything right and still get blindsided.

Two good incomes. Mortgage under control. Kids' sport on Saturdays. A bit going into super, a bit into savings, and plans for a proper holiday once rates settle down. Then one partner is diagnosed with a serious medical condition. The first week is doctors, tests, and phone calls. The second week is bills, leave balances, school pick-ups, and the quiet panic of realising income protection might not solve the immediate cash problem.

That's the gap many individuals miss.

Critical injury insurance exists for the moment where your life hasn't fallen apart permanently, but it has been violently disrupted. You may not be permanently disabled. You may not even be off work for all that long. But the financial shock can still be severe, especially if there's a mortgage, young children, or a business relying on you.

Why the problem is bigger than the hospital bill

The focus is often on treatment costs. Fair enough. But in practice, the pressure often comes from everything around the treatment.

- Mortgage repayments keep coming: The bank doesn't pause because you're in recovery.

- One income can drop fast: Even if one partner keeps working, household cash flow usually tightens.

- Care costs show up everywhere: Childcare changes, travel, parking, meals out, home help, and recovery support all add up.

- Decisions get rushed: Families sell investments, redraw from the home loan, or drain savings because they need cash now.

A serious illness doesn't just test your health. It tests your cash flow, your flexibility, and your ability to avoid making bad money decisions under pressure.

What this means for a WA household

If you're a young family in Perth with debt, the risk is simple. You don't need a catastrophe to create financial damage. You just need a major health event at the wrong time.

If you're in your fifties or early sixties, the risk changes shape. The problem isn't just income. It's watching decades of careful savings get chewed up by medical costs, time off work, and lifestyle adjustments.

That's why I don't treat critical injury insurance as a niche add-on. I treat it as part of a serious financial protection plan. It's there to protect the life you've built while you deal with the bigger issue in front of you.

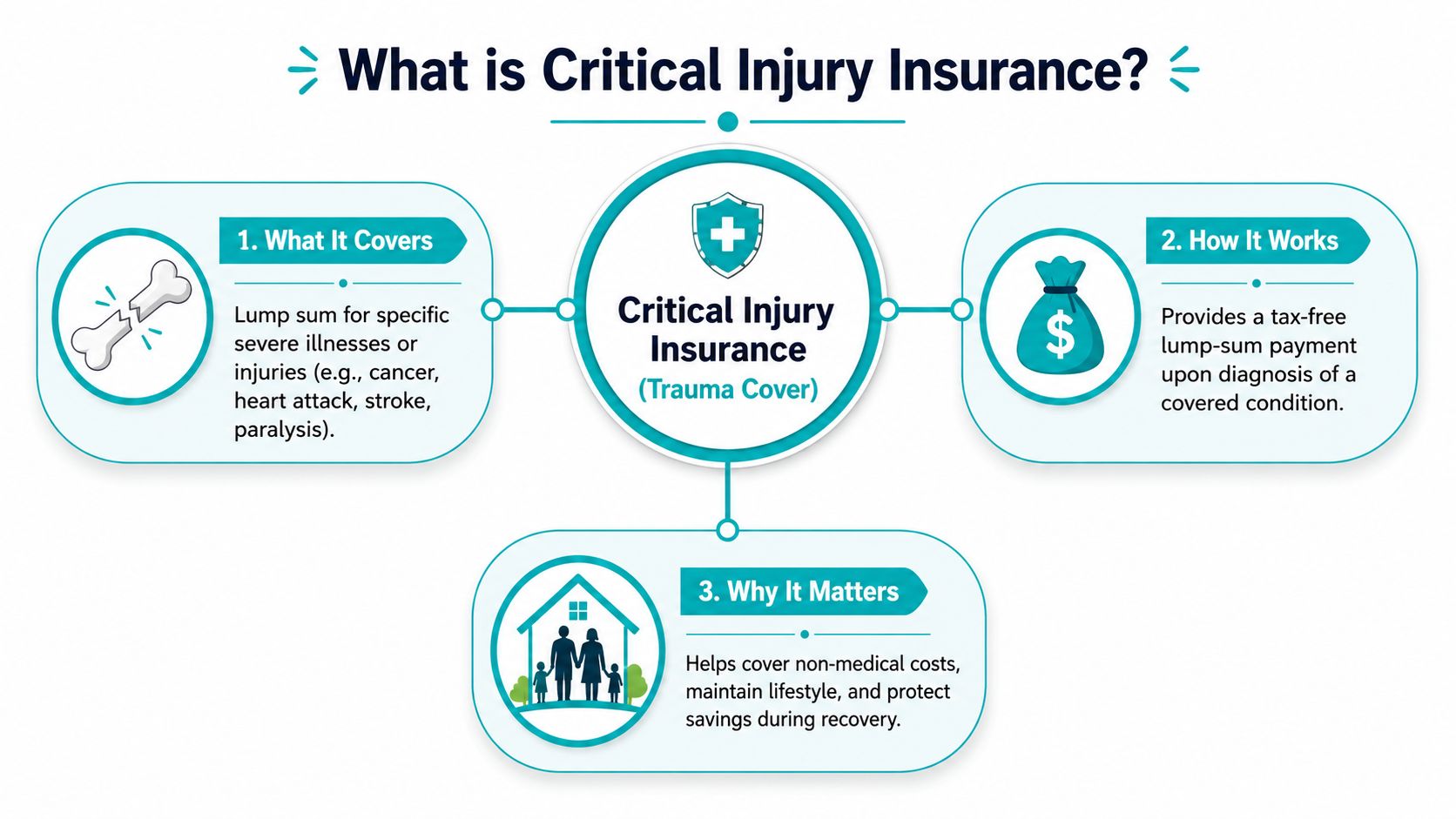

What Exactly Is Critical Injury Insurance

Call it critical injury insurance, trauma insurance, or critical illness insurance. In Australia, they're talking about the same style of cover.

This is a financial first-aid kit. If you're diagnosed with a specified serious medical event covered by the policy, the insurer pays you a lump sum. According to Allianz's explanation of critical illness cover, critical injury insurance in Australia provides an immediate lump-sum payment upon diagnosis of specified severe medical events like cancer, heart attack, or stroke, with most Australian policies setting a minimum cover amount of $50,000.

The simple version

This cover doesn't wait for you to become permanently disabled.

It doesn't require you to prove you'll never work again.

It's triggered by the diagnosis of a condition defined in the policy, provided the medical definition is met.

What the money is actually for

People get relief once they understand this. The payout is there to give you options. Real options.

You might use it to pay down debt so one income can carry the household for a while. You might fund treatment-related costs, rehab, or extra help at home. You might use it to create breathing room so you can focus on recovery instead of scrambling to preserve cash every week.

Think of it as money that buys time, flexibility, and choice.

Practical rule: If a serious diagnosis would force you to redraw on the mortgage, sell investments, or ask family for help, critical injury insurance deserves a proper look.

What it does not mean

It does not mean every diagnosis gets paid.

The event must be one of the listed conditions in the policy, and the definition matters. A policy document is not marketing fluff. It is the contract. If the wording says a condition must meet a particular severity threshold, that threshold matters more than the product brochure.

That's also why legal and insurance outcomes can look very different from each other. If you want a useful outside example of how large injury outcomes can vary in another context, Ares on largest PI settlements is a good reminder that “serious injury” and “payout” are never as simple as people think. Insurance policies work off precise definitions, not broad assumptions.

Clearing the Confusion Critical Injury vs TPD vs Income Protection

A Perth couple with two kids, a big mortgage in Baldivis, and one main income can get this wrong in a very expensive way.

One policy helps if cancer, stroke, or a heart attack hits. Another helps if you are permanently unable to work. Another helps if you are off work for months and the bills keep coming. If you treat them as the same thing, you leave a gap right where your family can least afford it.

Insurance Types at a Glance

| Feature | Critical Injury (Trauma) | Total & Permanent Disability (TPD) | Income Protection |

|---|---|---|---|

| Main trigger | Diagnosis of a specified serious medical condition that meets the policy definition | Permanent disability under the policy definition | Inability to work due to illness or injury, subject to policy terms |

| How it pays | Lump sum | Usually lump sum | Usually an ongoing monthly benefit |

| Main purpose | Immediate flexibility for medical costs, rehab, debt reduction, or family cash flow | Long-term financial support if work capacity is permanently lost | Replace part of income while you're off work |

| When it's most useful | Major health shock with urgent cash needs | Life-changing permanent impairment | Temporary or extended absence from work |

| Tax treatment | Premiums are generally not tax deductible, and benefits are generally received tax-free. The ATO guide to deductions for insurance premiums helps explain the general tax treatment principles. | Tax treatment depends heavily on ownership and whether cover sits inside or outside super | Tax treatment depends on policy structure and who owns the policy |

The practical difference is simple.

If you have a heart attack at 42, trauma cover may pay a lump sum even if you recover and return to work. TPD may not pay because you are not permanently disabled. Income protection may pay a monthly benefit if you are unable to work for a period, but it will not usually hand you a lump sum large enough to wipe down the mortgage, pay for treatment gaps, and buy time in one hit.

That is why young WA families often need more than one type of cover. They are protecting different financial risks, not buying duplicate products.

How I explain it to clients

For a family with school-aged kids and debt, critical injury insurance is the "cash now" policy. It gives you options fast.

For a tradesperson or professional in their peak earning years, income protection is the "keep the household running" policy. It helps cover the monthly burn rate while you are off work.

For someone whose ability to earn is their biggest asset, TPD is the "what if work is gone for good" policy.

Pre-retirees in WA need to think about this differently again. If you are 58, still carrying some debt, and planning to retire in a few years, a serious illness can derail retirement timing even if you eventually recover. Trauma cover can protect retirement savings from being chewed up by medical costs and time off work. TPD is still relevant, but it solves a narrower, harsher scenario.

The mistake that causes paralysis

People compare these policies as if they must pick one winner.

That is the wrong question.

Ask what problem you need solved first.

- Need money quickly after a major diagnosis? Critical injury insurance fits that job.

- Need an income while you are temporarily unable to work? Income protection is the right tool.

- Need support if you are unlikely to work again? TPD is the cover to examine.

TAL explains that critical illness insurance can be held as standalone cover or added to another policy, and the lump sum can generally be used however you choose, including treatment, rehab, income gaps, or debt reduction, as outlined in TAL's overview of critical illness insurance.

If you want a straightforward external comparison focused on purpose, critical illness or income protection cover is a useful read. For a broader Australian breakdown of how these policies fit together, this guide to life insurance types in Australia is worth your time.

My advice is blunt. If you have dependants, debt, or both, do not assume one policy will cover every bad scenario. It will not.

Understanding Policy Features and Common Exclusions

This is the part people skip, and it's the part that matters most when a claim happens.

A trauma policy can look generous on the front page and still disappoint if the definitions are narrow, the exclusions are tough, or the waiting rules catch you out. If you only look at the headline cover amount, you're buying blind.

The clause that catches people

One of the most important technical exclusions is the waiting period. As explained in Medibank's article on critical illness insurance, no payment is made if the condition occurred, was diagnosed, or symptoms became apparent within a waiting period that is typically three months after policy inception.

That matters.

If someone takes out cover after a scare, or after symptoms have already started to show, they may assume they're protected when they're not. Timing matters. So does disclosure.

Definitions are everything

The policy won't just say “stroke” or “cancer” and leave it there.

It will define what level of severity qualifies. A straightforward diagnosis in everyday language may still fail under the policy wording if it doesn't meet the clinical criteria in the Product Disclosure Statement. That's harsh, but that's how insurance contracts work.

When you review a policy, pay attention to:

- Condition definitions: Look at how the insurer defines events such as stroke, heart attack, cancer, and brain-related conditions.

- Severity thresholds: Ask what must happen medically before the claim is payable.

- Exclusions list: Check what is specifically carved out, including any conditions that are limited or excluded.

- Expiry rules: Confirm when cover ends and whether it still fits your stage of life.

Features that can add real value

Not every useful feature appears in the product name.

Some policies include extras that can make the cover more practical for families. Depending on the insurer, that may include reinstatement-style features after a claim or built-in benefits that support dependants. The point isn't to chase bells and whistles. The point is to ask whether the policy keeps working in a way that matches your actual life.

Don't buy a policy because the premium looks neat. Buy it because the wording would still make sense on your worst week.

If you've ever looked at other insurance areas, you've probably noticed the same thing. Fine print shapes outcomes. Even in adjacent topics such as coverage for auto accident chiropractic care, the big issue is rarely the headline promise. It's the policy's specific wording.

And if you're relying on income protection as the fallback, make sure you also understand the gaps. This explanation of what income protection does not cover helps clarify where people often overestimate their safety net.

How Much Does Critical Injury Cover Cost

Cost matters. But asking “what does it cost?” without asking “for whom?” doesn't get you far.

Premiums for critical injury insurance are personal. Age matters. Health matters. Smoking status matters. Occupation matters. The amount of cover matters too. Two people in Perth with similar incomes can get very different pricing because insurers are pricing risk, not fairness.

A concrete example

There is one example I like because it makes the pricing less abstract. According to the critical illness insurance overview on Wikipedia, a 35-year-old non-smoker male in Australia could pay an indicative additional $43.70 per fortnight to add $500,000 in critical illness cover to a $1 million life cover base.

That's not a quote. It's a reference point.

It tells you two useful things. First, this cover can be more accessible than people assume. Second, the number on your own application may be very different.

What usually pushes premiums up or down

- Age: The older you are when you apply, the more likely the premium increases.

- Health history: Existing conditions, past medical issues, and current treatment matter.

- Smoking status: Smokers usually face higher premiums.

- Occupation: Some jobs carry more risk from an insurer's perspective.

- Cover amount: More cover means more premium.

My advice on price

Don't shop for this the way you'd shop for phone plans.

The cheapest premium can be poor value if the definitions are weaker, the underwriting is stricter in the wrong areas, or the structure doesn't fit your broader protection plan. Price matters. Value matters more.

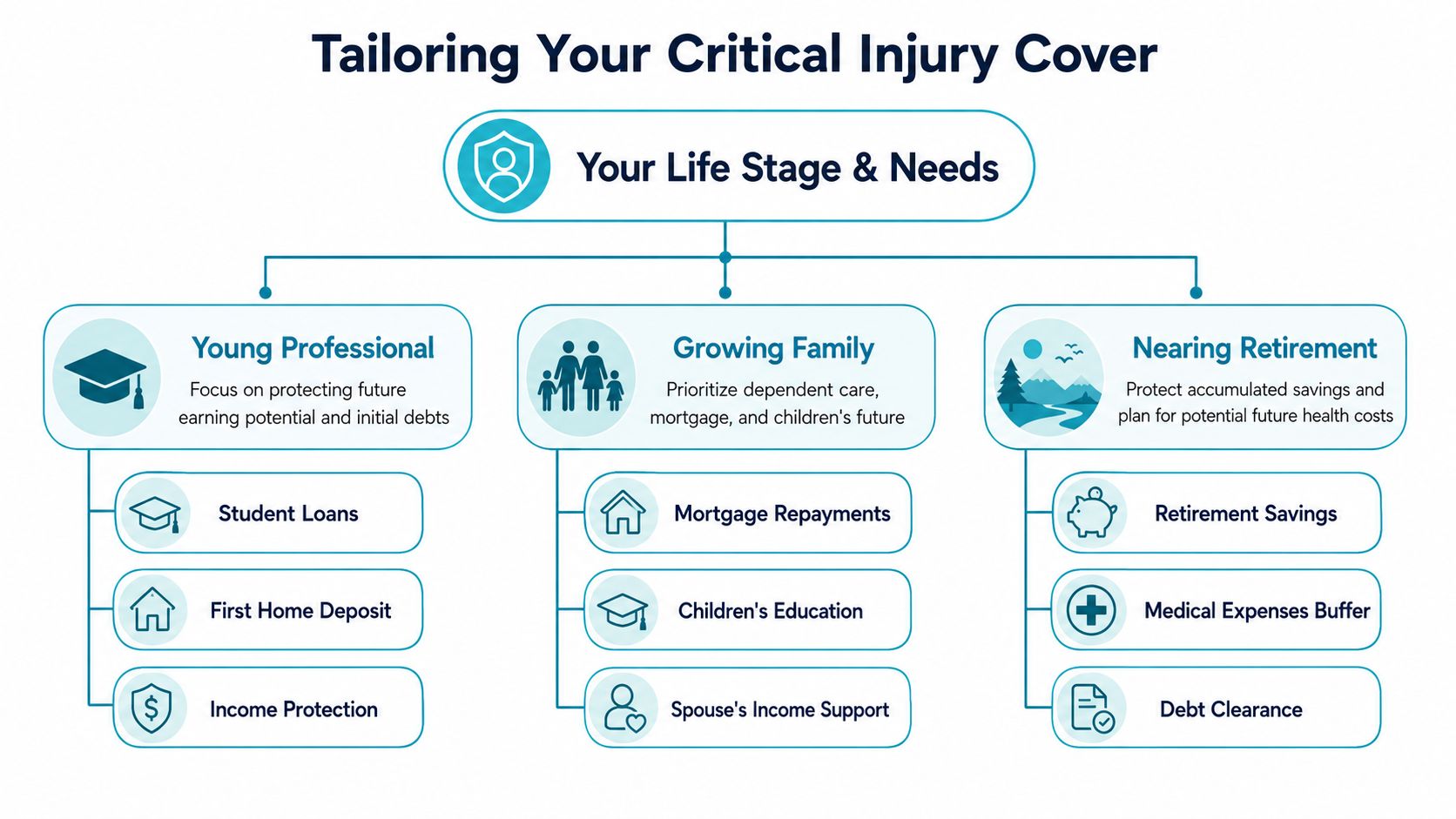

Choosing the Right Level of Cover for Your Life Stage

The “right” amount of critical injury insurance isn't a universal number.

It depends on who relies on you, what debts you carry, how much cash you already have access to, and what would happen if a serious diagnosis hit next month. That's why one-size-fits-all cover usually misses the mark.

The global market for this type of cover has grown substantially. According to Market.us critical illness insurance statistics, the market was valued at USD 192.3 billion in 2022 and is projected to reach USD 541.4 billion by 2032. That doesn't tell you what you should buy, but it does tell you more people are recognising the role this cover plays in personal financial planning.

Young families with a mortgage

This group usually needs the clearest answer.

If you've got children, debt, and one or two incomes doing a lot of heavy lifting, your cover should be built around immediate financial pressure. The mortgage is usually the first target. After that, think about a buffer that gives the healthy partner room to reduce work if needed, organise care, and avoid draining savings at the worst possible time.

A practical framework is to consider:

- Debt pressure: How much of the mortgage or personal debt would you want gone if one of you got seriously ill?

- Household breathing room: Would a lump sum give you space to reduce work hours temporarily?

- Family support costs: Childcare, transport, and day-to-day help often rise when life gets messy.

Pre-retirees in WA

If you're closer to retirement, the objective changes.

The issue may not be replacing decades of income. It may be protecting super, investments, and the retirement timeline you've worked hard to build. A major illness late in your career can force you to spend assets that were supposed to fund your next stage of life.

For pre-retirees, the best use of cover is often simple. Stop one health event from becoming a retirement funding problem.

Business owners and high earners

This group often underestimates how quickly pressure builds.

If you own the business, your absence can affect both household income and business cash flow. If you're a high earner, your lifestyle usually has fixed commitments that don't shrink quickly. In both cases, cover should reflect concentration risk. Too much depends on one person staying healthy.

The right number is the one that protects your actual life, not the one that sounds tidy in a brochure.

How to Secure Your Policy with Confidence

A Perth couple with two kids and a new mortgage does not need more insurance jargon. They need to know one thing. If one of them is hit with cancer, a stroke, or another serious condition, will the policy pay when the pressure is on?

That is the standard to use.

Getting this cover right is usually less about finding a cheap premium and more about making sure the contract matches your real life. For a young family in WA, that means enough money to take heat off the mortgage, cover extra care costs, and give the healthy partner breathing room at work. For a pre-retiree, it means stopping one health event from forcing an early raid on super or investments.

A practical process that works

Start with the outcome you want

Be specific. Do you want to clear part of the mortgage, fund treatment and recovery costs, protect retirement assets, or give your family 12 to 24 months of breathing room?Read definitions before you compare price

Many people stumble here. Two policies can look similar on premium and very different at claim time. Check exactly how the policy defines conditions, what severity threshold applies, when cover ends, and what sits outside the policy.Get the medical disclosure right the first time

Be thorough. Old scans, symptoms you ignored, specialist appointments, medication history. Put it all on the table. Bad disclosure is one of the fastest ways to create avoidable trouble later.Set up your paperwork so your family can act quickly

Keep policy documents, ID, doctor details, and adviser contact details in one place. If you are in hospital, your partner should not be digging through drawers and inboxes trying to work out who to call.

Questions worth asking any adviser

A good adviser should answer these clearly and without hiding behind product jargon.

- What exactly has to happen for this policy to pay?

- Which covered conditions have the tightest definitions?

- How does this policy fit with my income protection and any TPD cover I already have?

- What exclusions are most likely to matter for someone in my situation?

- When does the cover expire, and does that still make sense for my age and stage of life?

- If I am too unwell to manage the claim, who helps my family handle it?

The claims process is usually straightforward on paper. In real life, it lands in the middle of medical appointments, time off work, and a lot of stress. You will generally need claim forms, identity documents, medical evidence from your treating doctors, and clear confirmation that your condition meets the policy definition. That is exactly why advice matters. Good advice is not just about picking a policy. It is about making the claim process easier for your family if life goes sideways.

If you are deciding who to trust, this guide on how to choose a financial adviser will help you tell the difference between genuine advice and a polished sales pitch.

Good insurance advice should leave you with a clear decision, a policy you understand, and a family that knows what to do if something goes wrong.

If you want help working out whether critical injury insurance belongs in your plan, talk to Wealth Collective. They help Perth, Dunsborough, and WA clients cut through the noise, compare cover properly, and build protection around what matters: your income, your mortgage, your family, and your long-term financial life. Start with an initial call and get clear on what needs protecting before a health scare forces rushed decisions.