Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Retirement can feel strangely abstract until the day you stop work and look at your super balance as income, not just a number on a statement. That's when the main question lands. Not “Have I saved?” but how long will retirement savings last if this money now has to support the life I want.

For many people in Perth and across WA, that question arrives with a mix of relief and unease. You may own your home, expect some Age Pension support, and have a super balance that looks solid at first glance. But once you start translating that balance into annual spending, rising costs, and a retirement that could last decades, it's easy to lose confidence.

The Billion-Dollar Question Your Retirement Depends On

You might be in this exact position now. You've worked for years, built up super, and you're trying to work out whether it's enough to carry you through the next stage of life without constant financial stress.

A lot of people expect a simple answer. Divide the balance by annual spending and you're done. In reality, retirement longevity works more like a household water tank. Your super is the tank. Your spending is the tap. Investment returns can top the tank up. Inflation makes the water less useful over time because each dollar buys less. And your lifespan determines how long the tank needs to keep flowing.

That's why “enough” is never just one number.

For some retirees, the question is shaped by the ASFA Retirement Standard guide, which gives a useful starting point for lifestyle expectations. But the bigger issue is personal. Two people with the same balance can get very different outcomes depending on how much they spend, when they retire, how their investments behave early on, and how much support they receive from the Age Pension.

Practical rule: Don't ask whether your balance is good or bad in isolation. Ask whether your spending, income mix, and withdrawal plan match the retirement you want.

The good news is that this can be understood clearly. Once you break the problem into its parts, the fear tends to soften. You stop guessing and start planning.

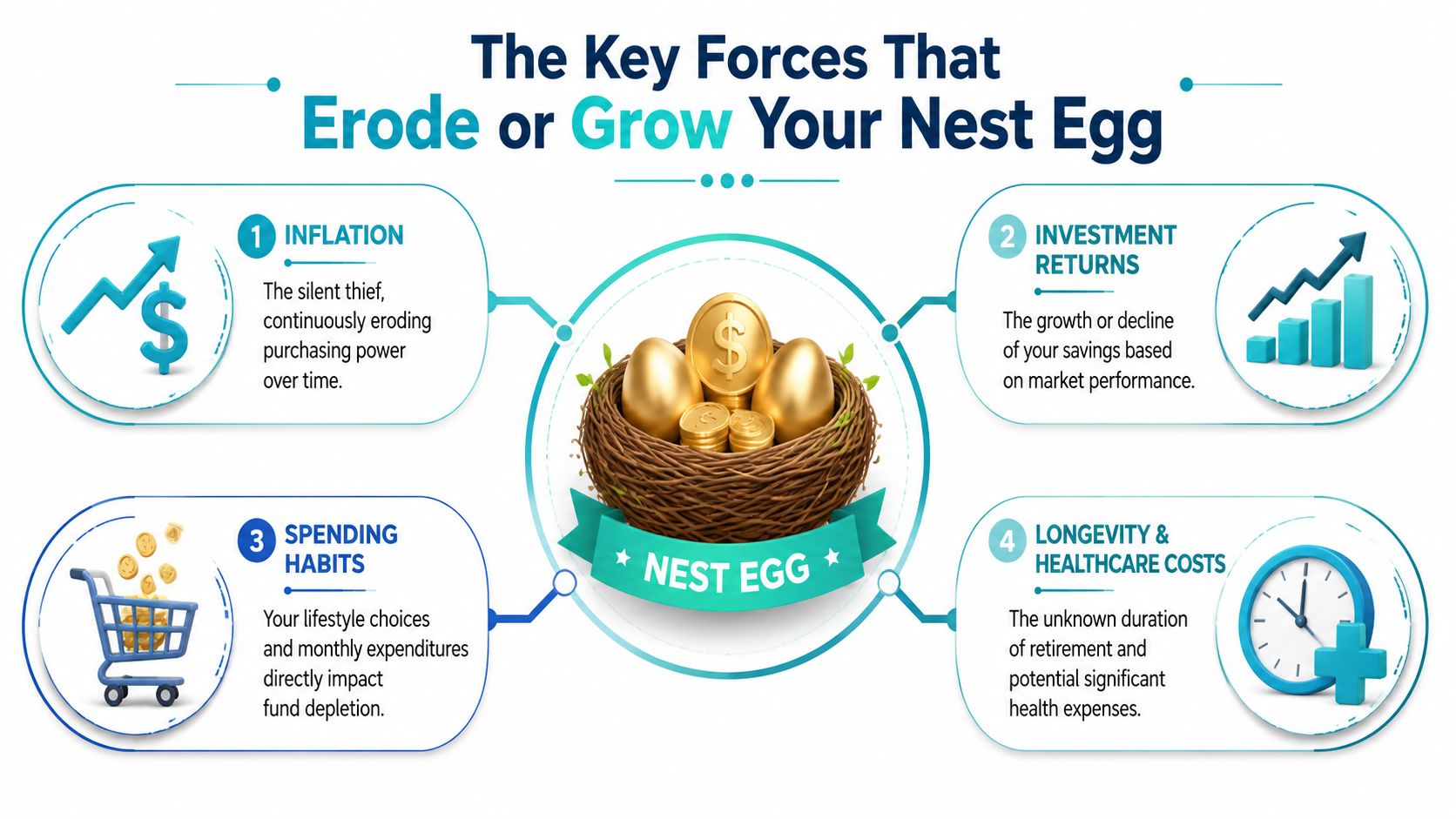

The Key Forces That Erode or Grow Your Nest Egg

Retirement income lasts longer when you understand what's helping your money and what's working against it. Most confusion comes from treating retirement as a straight line. It isn't. It's a moving system with a few major forces constantly interacting.

Investment returns and inflation

Investment returns are often the first element considered. Fair enough. If your super remains invested, returns can help refill the tank while you're drawing income from it. Good years can extend the life of your money. Poor years can shorten it.

Inflation is quieter, but just as important. It doesn't remove dollars from your account directly. It reduces what those dollars can buy. A retirement income that feels comfortable today may feel much tighter later if prices keep rising and your spending needs increase.

That's why retirees need growth as well as stability. Holding everything in cash may feel safe, but safety in retirement isn't only about avoiding market movement. It's also about preserving purchasing power for the years ahead.

Longevity risk is more personal than most people think

A common mistake is planning retirement around life expectancy at birth. That number isn't very useful once you've already reached retirement age.

Research from TAL shows that a 65-year-old Australian woman has an average life expectancy of 88 years, while a man expects to live to 85, and the paper argues that retirees should use confidence levels rather than averages when planning income for life (TAL retirement life expectancy research).

That changes the conversation. If you retire in your mid-60s, your money may need to support you for a long time. For couples, the plan often needs to last even longer because one partner may outlive the other by years.

Average life expectancy is a useful reference point. It isn't a safe finish line for a retirement plan.

Sequence risk and spending habits

The order of returns matters. If markets fall early in retirement while you're drawing income, you can do more damage than the same fall later on. Selling assets after a downturn leaves less capital invested for the recovery. That's called sequence of returns risk.

Then there's spending. This is the lever retirees control most directly. A few years of higher discretionary spending early on can create pressure that's hard to reverse later, especially if markets have also been weak.

A simple way to think about the four main forces is this:

- Returns: Help the portfolio recover and grow.

- Inflation: Pushes your future spending needs higher.

- Longevity: Extends the number of years your plan must work.

- Spending: Determines how quickly you draw from the pool.

When people ask how long retirement savings will last, these are the primary drivers behind the answer.

The 4 Percent Rule and Why It Fails Australian Retirees

A Perth couple retires with a solid super balance, owns their home, and reads that they can draw 4% a year and be fine. That sounds tidy. Real retirement in Australia rarely works that way.

The 4% rule came from US research built around a very specific question: how much could someone withdraw from an investment portfolio and still have it last for a long retirement? As a rough guide, it helped simplify a hard problem. As a retirement plan for Australians, it leaves out too much to rely on by itself.

The biggest issue is that Australian retirees do not usually fund retirement from one bucket alone. Your income may come from super, then partly from the Age Pension, and sometimes from smaller sources such as cash savings or part-time work. A rule designed around personal portfolio withdrawals misses that mix.

A better comparison is a household water tank. Super is one tank. The Age Pension can act like a smaller top-up pipe that starts to matter more as your own water level drops. If you ignore that second pipe, you may assume the tank will run dry much sooner than it really will. If you assume the pipe will cover everything, you can be just as wrong.

That is why the right question for an Australian retiree is not, "Can I draw 4%?" It is, "How much needs to come from my super after allowing for Age Pension eligibility, tax treatment, and the lifestyle I want here in WA?"

For some WA retirees, that answer looks very different from the US version of retirement. A homeowner in Perth with moderate spending may be able to draw less from super than expected because the Age Pension helps cover part of the basics. A retiree who wants frequent travel, high private health costs, or extra support for family may need more from super and need it earlier. Same country. Very different outcome.

This is also why broad retirement targets can mislead if they are taken out of context. A target balance only becomes useful once you connect it to spending, housing, and likely Age Pension support. If you want a clearer benchmark, our guide on how much super you may need to retire in Australia is a better starting point than a single withdrawal rule.

The 4% rule is still useful as a conversation starter. It gives you a rough first estimate. It does not reflect the Australian system well enough to be the final answer.

For Australians, retirement planning works better when you treat withdrawals as flexible rather than fixed. In strong years, you may spend a little more. In weak years, you may slow discretionary spending and let the portfolio recover. That approach fits practical circumstances far better than copying a US rule and hoping it suits your super, your Age Pension position, and your lifestyle in WA.

Calculating Your Savings Timeline From Simple to Sophisticated

A Perth couple retires at 67, owns their home, and has a healthy super balance. Ten years later, one version of that couple is sleeping well and taking the occasional trip down south. Another is worried about whether the money will stretch. The starting balance may be similar. The difference often comes from how income is mapped out, how much support comes from the Age Pension, and how spending changes over time.

That is why a retirement timeline needs to start simple, then become more realistic.

The simple estimate

The quickest calculation is basic division. If you have a super balance and you know roughly how much you plan to withdraw from it each year, you divide the balance by the annual withdrawal.

It is a useful first pass. It gives you orientation, like checking the fuel gauge before a long drive from Perth to Albany.

But it leaves out too much to rely on. Investment returns, inflation, changing spending, tax treatment, and Age Pension support can all shift the result. Retirement is not a straight-line maths exercise. It is closer to managing a water tank. Money flows out for living costs, some flows back through returns, and another tap may open through the pension if you qualify.

A practical Australian example

A comparison from Life Financial Planners shows how sharply spending can change the outcome for a couple retiring at 67 with $500,000 in super. Their example suggests a more modest spending pattern can see savings last much longer than a more comfortable one, even with the same starting balance and retirement age (how long $500,000 lasts in retirement).

| How Lifestyle Affects a $500,000 Super Balance (Couple, Age 67) | ||

|---|---|---|

| Lifestyle | Annual Spending | Savings Last Until Age |

| Modest | $60,000/year | Age 99 |

| Comfortable | $80,000/year | Age 81 |

The lesson is simple. Spending is not a minor detail. It is one of the biggest controls you have.

If you want a clearer starting point for your own target balance, this guide on how much super you may need to retire in Australia can help frame the numbers before you test how long they may last.

Why a better projection looks different in Australia

Australian retirees usually do not fund retirement from one source alone. Super may cover part of the cost. The Age Pension may cover another part. For homeowners in WA, that mix can make a big difference to how long private savings need to last.

Online calculators often confuse people. A calculator built around a fixed annual withdrawal can make it look as if your super must carry the whole load from day one to the end of life. For many Australians, that is not how retirement works in practice.

A better projection asks a more useful set of questions:

- What do you expect to spend each year in the early years of retirement?

- How much of that spending is basic living costs versus discretionary spending like travel or helping family?

- Are you likely to receive a part or full Age Pension now or later?

- How might your spending change if markets fall or health costs rise?

- How long do you want the plan to hold up if one partner lives well into their 90s?

These questions turn a rough estimate into something closer to a working plan.

A more detailed projection

A stronger retirement forecast works like a series of test runs. You start with your likely spending. Then you layer in investment returns, inflation, minimum drawdown rules for account-based pensions, and any Age Pension you may receive over time.

That last part matters. A retiree may draw more heavily on super in the early years, then rely more on the Age Pension later as assets fall and eligibility changes. That is a distinctly Australian feature, and it is one reason imported rules of thumb can miss the mark.

It also helps to compare systems carefully if you read overseas content. For readers sorting through US material as well, understanding 72t distributions can clarify why American withdrawal rules often do not line up neatly with Australian super rules.

The goal is not to predict the future perfectly. The goal is to build a timeline that still makes sense if returns are weaker, inflation runs hotter, or your lifestyle shifts. That is how retirement planning becomes clearer and far less stressful.

Actionable Strategies to Make Your Money Last Longer

A good retirement plan works like a water tank in a long WA summer. Money flows out every month for rates, food, power, insurance, and the enjoyable extras. New water comes in from investment earnings, and for many Australians, from the Age Pension as well. The goal is not to stop using the tank. The goal is to control the flow so it keeps serving you for decades.

Structure your income deliberately

How you take money matters almost as much as how much you have.

In Australia, retirement income usually comes from a mix of super, personal savings, and, over time, some level of Age Pension for many households. Those parts need to work together. Drawing too much from super too early can shrink your balance faster than necessary. Drawing in a way that ignores pension rules can also create avoidable pressure later.

A useful starting point is understanding how different retirement income streams are set up and what job each one is meant to do. One income source might cover regular bills. Another might sit in reserve for larger, irregular costs such as replacing a car, dental work, or helping family.

For readers who also hold US-linked retirement assets or are comparing overseas rules, it can help to read about understanding 72t distributions from Kons Law, because withdrawal rules can differ sharply across systems and create confusion when people consume mixed financial content online.

Focus on the levers you can actually pull

Many retirees feel they have only two options: spend freely and hope, or cut back hard. Real life gives you more control than that.

The first lever is flexible spending. Start with the costs that can move without damaging your quality of life. Travel, gifts, home upgrades, and big once-off purchases are usually easier to delay than council rates, groceries, or health cover. In a weak market year, trimming the optional items first can protect the assets that need time to recover.

The second lever is investment mix. A portfolio that is too cautious can leave your money working too slowly against inflation. One that is too aggressive can produce falls that make it hard to stay calm and stick to the plan. The right balance is the one that supports your spending needs and still lets you sleep at night.

The third lever is timing. Large withdrawals matter more when markets are down. Renovating the kitchen, buying a new vehicle, or giving a substantial amount to adult children in the same year your portfolio falls can do lasting damage to the pool you are drawing from.

Part-time work can help too. Even modest income in the early years of retirement may reduce how much you need to pull from super, which gives your savings more time to recover and compound.

Review the plan in real life, not just on paper

Retirement is not a set-and-forget exercise. It needs regular check-ins.

A simple annual review can go a long way. Compare what you planned to spend with what you spent. Check whether your withdrawals still make sense after market changes. Revisit whether you are likely to qualify for more Age Pension support as your assets change over time. This Australian interplay between super drawdowns and pension eligibility is one reason the popular 4 percent rule is too blunt for many WA retirees.

The households that tend to stay confident are usually the ones making small adjustments early. They do not wait for a problem to become obvious. They review, refine, and keep the water tank at a sustainable level.

From DIY Anxiety to a Confident Retirement Roadmap

DIY retirement planning often works well until the numbers start conflicting with each other. One calculator says you're fine. Another says you're short. A rule of thumb suggests one withdrawal rate. Your actual spending points somewhere else entirely.

That's not because you're bad with money. It's because retirement planning sits at the intersection of investment risk, tax decisions, longevity, pension rules, and human behaviour. Small choices can have long-term consequences, especially in the early years of retirement.

For example, research cited by National Seniors Australia shows that a single person needs $630,000 in super at age 67 to fund a comfortable retirement until age 90, while the median actual balance at retirement is just over $300,000. Without a proper drawdown strategy, many people face the risk that savings may run out 10 to 15 years too soon (National Seniors and Challenger retirement income report).

That gap is exactly why retirement advice needs more than rules of thumb. It needs a plan that reflects your actual life in WA. Your home ownership position, your super mix, your likely pension entitlement, your spending habits, and the kind of flexibility you want if markets turn ugly all matter.

A good retirement plan doesn't promise certainty. It gives you a clear way to make better decisions as circumstances change.

That's where a professional process becomes valuable. Not as a luxury, and not as a stack of jargon, but as a practical way to turn worry into a workable roadmap.

If you want clarity on how long your savings may last, and what to do to improve the outcome, Wealth Collective can help. Their Retirement Roadmap process is built for Australians who want a clear, personalised plan rather than generic rules pulled from overseas articles. Start with a free, no-obligation 10-minute introductory call and get a practical next step toward a more confident retirement.