Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

A lot of people sort out their super, keep an eye on the mortgage, and talk about retirement timelines, yet leave one uncomfortable question unanswered. If you were in hospital tomorrow, or couldn't manage paperwork for a period, who would handle your bank accounts, bills, property decisions, or insurance matters the way you'd want them handled?

That gap catches people at every stage of life. It affects the couple getting serious about retirement, the business owner juggling too many moving parts, and the younger family with joint expenses and long-term plans. A financial power of attorney isn't about expecting the worst. It's about making sure your life can keep running if you can't temporarily or permanently steer it yourself.

Securing Your Financial Future Starts Now

Karen and Michael are close to retirement. They've worked hard, built savings, paid down debt, and started imagining more travel and more time with family. Then a simple planning conversation raises a confronting issue. If one of them lost capacity after an illness or accident, who would deal with the accounts, sign documents, or keep their finances moving?

That's where a financial power of attorney becomes less of a legal phrase and more of a practical safeguard. It gives you a way to choose who can step in and manage financial matters if needed, instead of leaving your family to scramble during a stressful time.

The urgency is real because public understanding is low. Only 6% of Australians feel they possess substantial knowledge of enduring powers of attorney, while 35% say they know nothing about them, according to the Australian Human Rights Commission media release on nationally consistent enduring power of attorney reform.

Why this matters to ordinary households

When people don't understand the document, they often delay it. Delay creates risk. If capacity changes suddenly, loved ones may have responsibility without authority, or authority without enough guidance.

Practical rule: The best time to organise a financial power of attorney is when life feels stable, not when a crisis has already arrived.

Many readers start here because they're already thinking more broadly about protecting family wealth and reducing avoidable risk. If fraud prevention is also on your mind, this guide for protecting loved ones from fraud offers useful companion reading. It sits well beside broader estate planning essentials such as these estate planning insights and updates.

Peace of mind is the real benefit

A financial power of attorney doesn't take control away from you just because you create it. Done properly, it gives you more control now over what happens later. You choose the person. You set the framework. You reduce confusion for the people around you.

That's not pessimistic planning. It's organised planning.

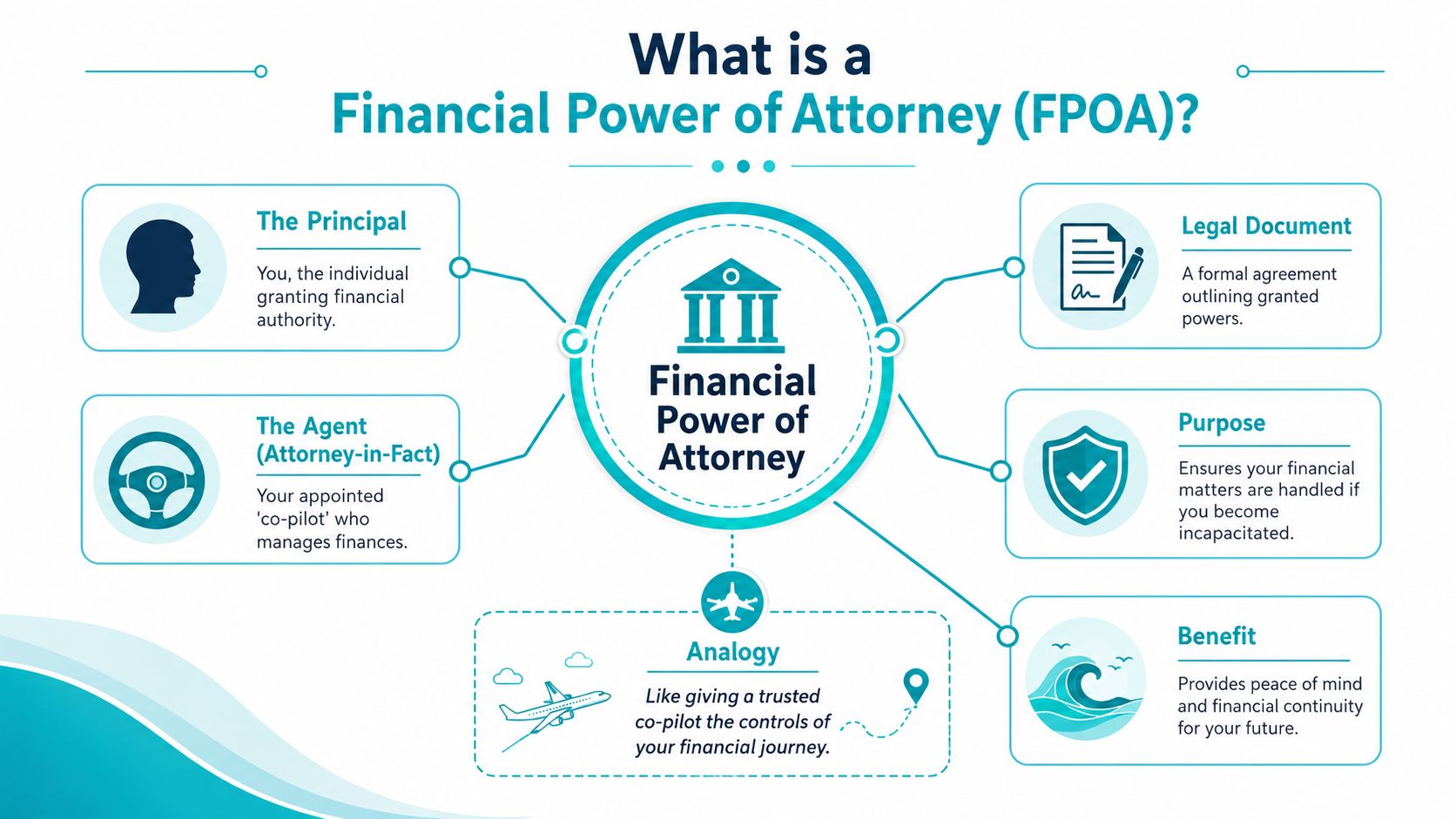

What Exactly Is a Financial Power of Attorney

Think of a financial power of attorney as appointing a financial co-pilot. You're still in command while you can act for yourself. But if something happens and you can't manage the controls, the person you nominated can step in under the authority you've already granted.

In plain language, a financial power of attorney is a legal document that lets someone you choose manage your financial and property affairs. Depending on the document and your state or territory rules, that can include tasks like operating bank accounts, handling bills, dealing with investments, managing insurance matters, or attending to property transactions.

The two people at the centre of the document

The language can sound formal, but the roles are simple.

- The principal is you. You're the person giving authority.

- The attorney is the person you appoint. They aren't necessarily a lawyer. In this context, they're the trusted person authorised to act for you.

- The authority is limited to what the document and the law allow.

One common point of confusion is timing. Some financial powers of attorney can operate immediately. Others are designed to operate when a specific event occurs, such as impaired decision-making capacity.

General and enduring are not the same

This distinction matters more than is often realised.

A general power of attorney is usually used for convenience or a temporary period. For example, you may be overseas and need someone to sign property or banking documents while you're away. But under Australian banking guidance, a general power of attorney ends if you lose capacity, while an enduring power of attorney continues. The same guidance notes that an enduring power of attorney remains valid even if the principal loses capacity and that the attorney's authority ends on the principal's death, when the will takes over, as explained in the Australian Banking Association power of attorney fact sheet.

A will speaks after death. A financial power of attorney operates while you're alive.

That's why an enduring financial power of attorney is such an important part of long-term planning. It's the version built for the period when help is most needed.

What it can and can't do

A financial power of attorney can cover money and property decisions. It doesn't automatically cover healthcare, lifestyle, or personal care decisions. Those usually require different legal arrangements.

The easiest way to remember it is this. If the task involves your money, assets, property, or financial administration, a financial power of attorney may be the right tool. If the decision is medical or personal, you'll likely need another document.

Financial vs Medical vs General POAs in Australia

People often assume one document covers everything. It doesn't. Different appointments do different jobs, and mixing them up can leave serious gaps.

The cleanest way to understand this is side by side.

Power of Attorney Types in Australia at a Glance

| Type of POA | Primary Purpose | Decisions Covered | When It Is Active |

|---|---|---|---|

| Financial Power of Attorney | Lets a trusted person manage financial and property matters | Banking, bills, investments, insurance, property and other financial tasks allowed by the document | Depends on the wording. It may start immediately or on loss of capacity if enduring |

| Medical or Personal Appointment | Lets someone make personal, lifestyle or healthcare decisions under the relevant laws | Healthcare, living arrangements, personal care and related non-financial decisions | Usually when you can't make those decisions yourself |

| General Power of Attorney | Gives temporary or limited authority for financial matters | Specific financial or property actions, often for convenience | While you have capacity and within the period or purpose stated |

Where readers usually get caught out

The first trap is assuming a financial appointment lets someone make medical decisions. It generally doesn't. Financial authority and healthcare authority are separate categories, so families often need more than one document to create a complete plan.

The second trap is forgetting how a general power of attorney works. People sometimes sign one for convenience and assume they're covered for the future. They aren't if capacity is lost.

For people also reviewing the broader consequences of what happens to assets on death, including superannuation, this explanation of what happens to super when you die helps connect the dots between incapacity planning and estate planning.

A simple way to choose the right document

Ask three questions:

- Is the decision about money or property? If yes, think financial power of attorney.

- Is the decision about treatment, care, or living arrangements? If yes, think personal or medical appointment.

- Do I need help only for a limited period while I still have capacity? If yes, a general power of attorney may suit that narrow purpose.

The legal labels differ across Australia, but the practical distinction stays the same. Money decisions need one kind of authority. Personal and medical decisions need another.

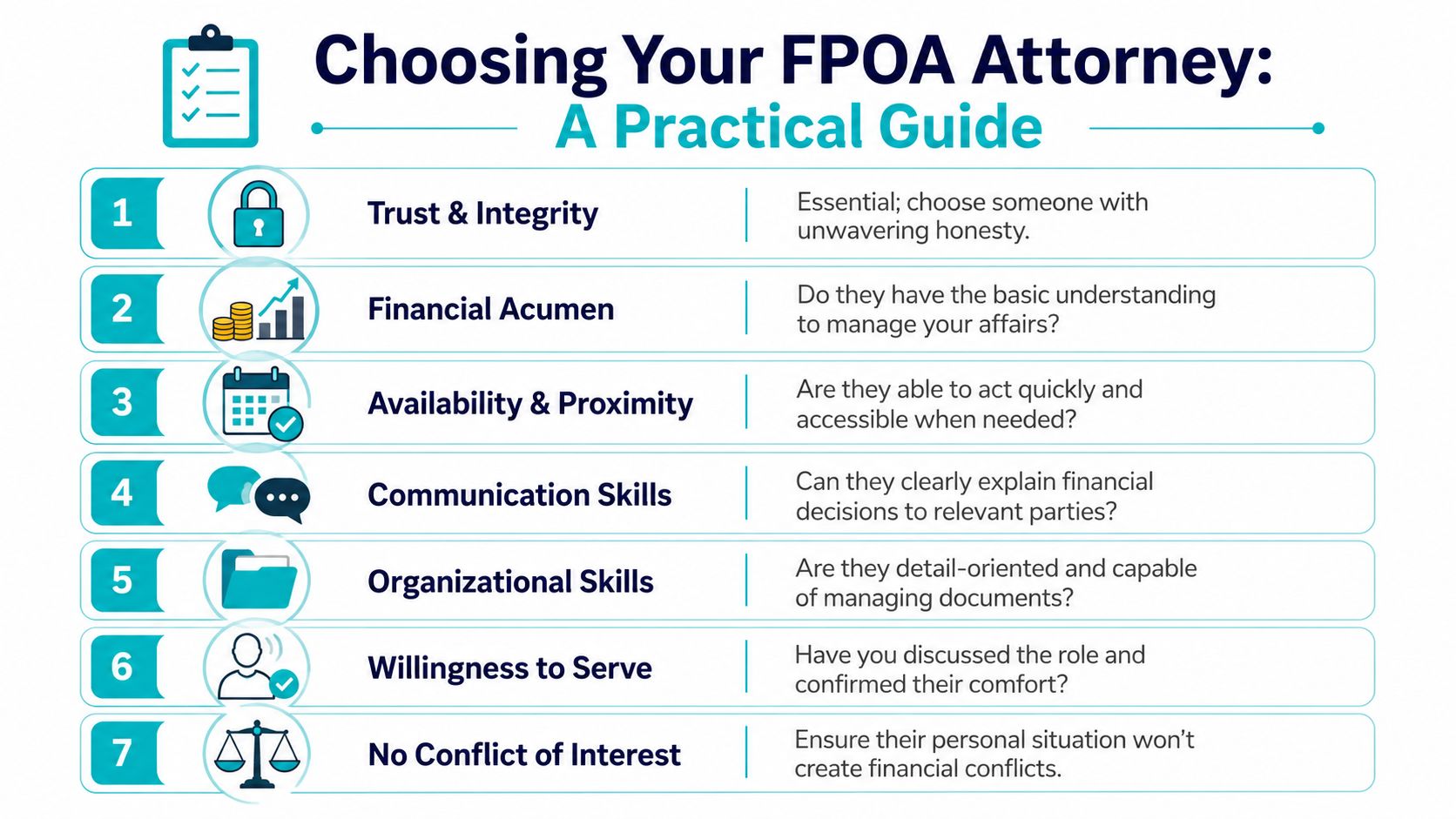

A Practical Guide to Choosing Your Attorney

This is the part that deserves more thought than it typically receives. Many people start and stop with one question: “Do I trust them?” Trust matters, but it isn't enough on its own.

Your attorney may need to speak with banks, keep records, manage deadlines, and make decisions under pressure. A kind family member who hates paperwork or avoids conflict may not be the right fit, even if your relationship is close.

What to look for beyond simple trust

Use this as a working checklist.

- Integrity first: Choose someone who has a strong record of honesty in everyday life, not just someone who says the right things.

- Comfort with money matters: They don't need to be a financial expert, but they should understand bills, records, and the need for careful decision-making.

- Organised habits: Good intentions won't fix lost paperwork, missed notices, or poor record-keeping.

- Availability: Someone who travels constantly, lives remotely, or already feels overwhelmed may struggle to act when needed.

- Calm communication: They may need to deal with siblings, professionals, banks, and service providers.

- Willingness: Never assume. Ask them clearly whether they're prepared to do it.

- Low conflict risk: If family dynamics are tense, think carefully before appointing someone likely to inflame disputes.

Know the duty they're accepting

An attorney isn't free to treat your money as if it were shared family property. They must keep the principal's money separate from their own and use it only for the principal's benefit unless the document says otherwise, as explained by the ACT Law Society fact sheet on being an attorney.

That legal duty is a big reason to choose someone who respects boundaries and keeps clean records.

The right attorney is often the person who combines judgment with discipline, not the person who simply feels closest to you.

Should you appoint more than one person

Sometimes one attorney is ideal. Sometimes two make sense.

If you appoint multiple attorneys, you'll usually need to think about whether they act jointly or jointly and severally.

- Jointly means they must act together. This can create checks and balances, but it can also slow decisions.

- Jointly and severally means either can act alone. This is more flexible, but it requires strong confidence in each person individually.

A practical example helps. Two siblings who communicate well and live nearby might work jointly. A spouse and adult child in different locations may be more effective jointly and severally if quick action is important.

The best choice depends less on legal wording and more on how these people function in real life.

The Legal Process for Appointing and Revoking a POA

A financial power of attorney is one of those documents where the idea is simple but the execution has to be precise. Small errors can create major problems later, especially when banks, land registries, or family members start relying on the document.

The core steps to get it right

Across Australia, forms and rules vary by state and territory, but the broad process is consistent.

- Use the correct form for your state or territory. A generic document copied from somewhere else may not do the job.

- Choose the attorney carefully. Talk through the role before anything is signed.

- Decide how the authority should operate. Immediate authority and authority triggered by loss of capacity are very different arrangements.

- Sign it properly. Many errors commonly happen here.

- Store it safely and give access where needed. A perfect document hidden in a drawer can still create chaos.

The witness requirement is not optional

In Australia, an enduring financial power of attorney is legally invalid unless it is signed in front of a prescribed witness, typically a solicitor, Justice of the Peace, or registered medical practitioner, who must confirm the principal understands the full legal impact of the document, as outlined in this Australian guide to financial power of attorney requirements.

That requirement exists for a reason. It helps confirm you understand what you're signing and helps reduce later arguments about confusion, pressure, or lack of capacity.

Capacity and documentation matter more than people expect

If there's any possibility that your capacity could later be challenged, professional confirmation at the time of signing becomes especially important. Clear records can make a difficult family situation much easier to resolve.

Banks also have their own procedures. They generally require certified copies before they'll record the appointment and allow an attorney to act. If property is involved, there may be extra steps. In New South Wales, for example, a financial power of attorney must be registered with NSW Land Registry Services if the attorney needs to deal with real estate in that state.

Important: A financial power of attorney only operates during your lifetime. It does not give anyone authority after death.

Sometimes it helps to look at another jurisdiction to appreciate how location-specific these rules can be. This overview of BDJ Express Law's Utah POA guide is a useful reminder that power of attorney law is highly local, which is exactly why Australians should avoid relying on overseas templates or assumptions.

Revoking the appointment

Creating a power of attorney doesn't lock you in forever. If you still have capacity, you can generally revoke it. A later document may also replace an earlier one, and in some circumstances a tribunal can revoke an appointment.

That flexibility is reassuring. Good planning should be strong, but it should also be reviewable when life changes.

Common Pitfalls and How to Avoid Them

Most problems with financial powers of attorney don't come from the idea itself. They come from rushed decisions, vague drafting, poor records, or a complete absence of professional guidance.

Pitfall one: treating capacity as a box-ticking exercise

This is one of the most serious mistakes. Existing consumer guides often omit the need for professional confirmation of the donor's capacity at the time of execution, leaving the document vulnerable to later challenges about fraud or undue influence. That omission has been linked to a 25% increase in contested FPOA disputes in Australia over the last 12 months, according to CPA Australia's guidance on financial power of attorney and abuse prevention.

If a family member later claims the person didn't understand what they signed, the quality of the original process becomes essential.

Pitfall two: leaving the attorney without enough guidance

A document can be valid and still be unclear in practice. Problems often arise when the attorney knows they have authority but has no practical guidance about how the principal wants money managed.

That's where a simple written note about preferences can help. It might cover issues like spending priorities, support for a spouse, treatment of gifts, handling of the family home, or who should be consulted before major decisions.

Pitfall three: assuming everyone understands their obligations

Some attorneys don't realise how formal the role is. They may mix funds, keep poor records, or make “temporary” decisions for convenience that later look improper.

Simple systems reduce risk:

- Separate accounts and records: Keep a clear paper trail for every transaction.

- Written decision notes: Record why significant actions were taken.

- Professional check-ins: Use legal and financial advisers when a major decision affects investments, property, or family interests.

For families who want stronger administrative discipline around financial processes and records, tools that automate financial compliance can support consistency, especially where there are many documents to review and store.

Pitfall four: forgetting the wider estate plan

A financial power of attorney doesn't replace a will, and it doesn't solve every planning issue by itself. Families often discover too late that they have one document in place and several other gaps still open.

If you're reviewing incapacity planning, it's also worth understanding what happens if you don't have a will in Australia. The two issues are different, but they often surface at the same time in real families.

Poor planning doesn't only create legal risk. It creates stress, delay, and family tension at the exact moment people have the least capacity to deal with it.

Your Next Steps with Wealth Collective

A financial power of attorney belongs in the same conversation as cash flow, super, investments, insurance, retirement timing, and wealth transfer. It's not just an end-of-life document. It's a continuity document.

That matters at every life stage, although the practical focus changes.

If you're a young professional or building a family

Your checklist may look like this:

- Protect income and momentum: If something interrupts your ability to manage money, who can keep bills, debt repayments, and financial commitments on track?

- Match authority to assets: If you've bought property, built savings, or started investing, your planning should reflect that.

- Coordinate with insurance and super: A financial plan works better when legal authority and financial structures align.

If you're a pre-retiree

This stage often needs sharper detail.

- Review asset complexity: Multiple accounts, investment structures, property, and transition-to-retirement decisions can all increase the need for a well-chosen attorney.

- Clarify decision triggers: Be explicit about when the attorney should act and what major decisions should involve consultation.

- Align with retirement strategy: The person stepping in should understand your broad priorities, not just your account balances.

If you're retired

The focus often shifts toward simplicity, protection, and reduced burden on family.

- Keep documents current: Old appointments can become risky if relationships, health, or finances have changed.

- Reduce confusion for loved ones: Clear authority and clear instructions make a difficult time more manageable.

- Support wealth transfer planning: A financial power of attorney sits alongside broader planning for how money is protected and eventually passed on.

Good advice turns these moving parts into one organised strategy. That's where Wealth Collective's service pillars can make a real difference. Protection Plus helps manage personal risk and insurance. Guided Growth supports wealth-building decisions such as super, debt reduction, and investment strategy. Retirement Roadmap helps pre-retirees and retirees align their legal, financial, and retirement planning choices so they work together instead of competing for attention.

If your financial power of attorney is still on the to-do list, or if you're not sure whether your broader planning is properly connected, now is a sensible time to review it.

If you want clarity on how a financial power of attorney fits into your wider financial plan, book a free, no-obligation introductory call with Wealth Collective. It's a simple way to talk through your next step with an adviser who can help you build, protect, and transfer wealth with more confidence.