Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

June can feel like a scramble. Your payroll team has already paid super. You may have salary sacrificed a bit through the year. Your accountant mentions a deductible contribution. Then someone says you might be able to “catch up” unused caps from earlier years, but only if your balance is under one threshold, unless they're talking about a different threshold entirely.

That's where many people get stuck.

The people I see most confused are often the ones closest to making this strategy worthwhile. Pre-retirees with lumpy income. Business owners who finally have a strong year. Professionals who spent a few years focused on mortgages, school fees, or building a business and now want to boost super quickly. The rules can absolutely help, but only if you apply the right rule to the right balance test.

Your Guide to Smarter Super Contributions

A common scenario looks like this. Someone in their late 50s has sold an asset, wants to push more into super, and has heard two different numbers from two different conversations. One person says the balance test is under $500,000. Another says it's under $1.84 million. They assume one of those numbers makes them ineligible and abandon the idea altogether.

That's often the costly mistake.

The first thing to understand is that super contribution planning isn't one rule. It's a set of separate rules with different gates. If you mix them up, you can end up holding back when you had room to act. Or worse, you can contribute without checking how much of your cap has already been used by employer payments.

Why the confusion matters

For most clients, this isn't about chasing technical perfection. It's about using super as a practical tool to reduce tax pressure now and strengthen retirement cash flow later. That's why concessional contribution limits matter. They set the boundary for before-tax contributions, and the way you use that boundary can change the outcome of a financial year.

The best super strategies usually look boring on paper. They're simply well-timed, well-documented, and matched to the right rule.

The challenge is that end-of-financial-year decisions tend to happen fast. Payroll deadlines arrive. Contribution processing times matter. ATO records need checking. If you're making a personal deductible contribution, the paperwork also has to line up properly. Good strategy comes from slowing the process down just enough to separate assumptions from facts.

What tends to work

Three habits usually make the difference:

- Track employer contributions early: Your compulsory employer payments count toward the same concessional cap, so you can't treat your salary sacrifice as a separate bucket.

- Check the right balance test: The carry-forward rule and the bring-forward rule are not the same thing, even though people often discuss them in the same breath.

- Tie the contribution to a goal: Some people want ongoing tax efficiency. Others want a one-off boost before retirement. The right contribution pattern depends on the purpose.

When clients get clarity on those points, the rules become much easier to use with confidence.

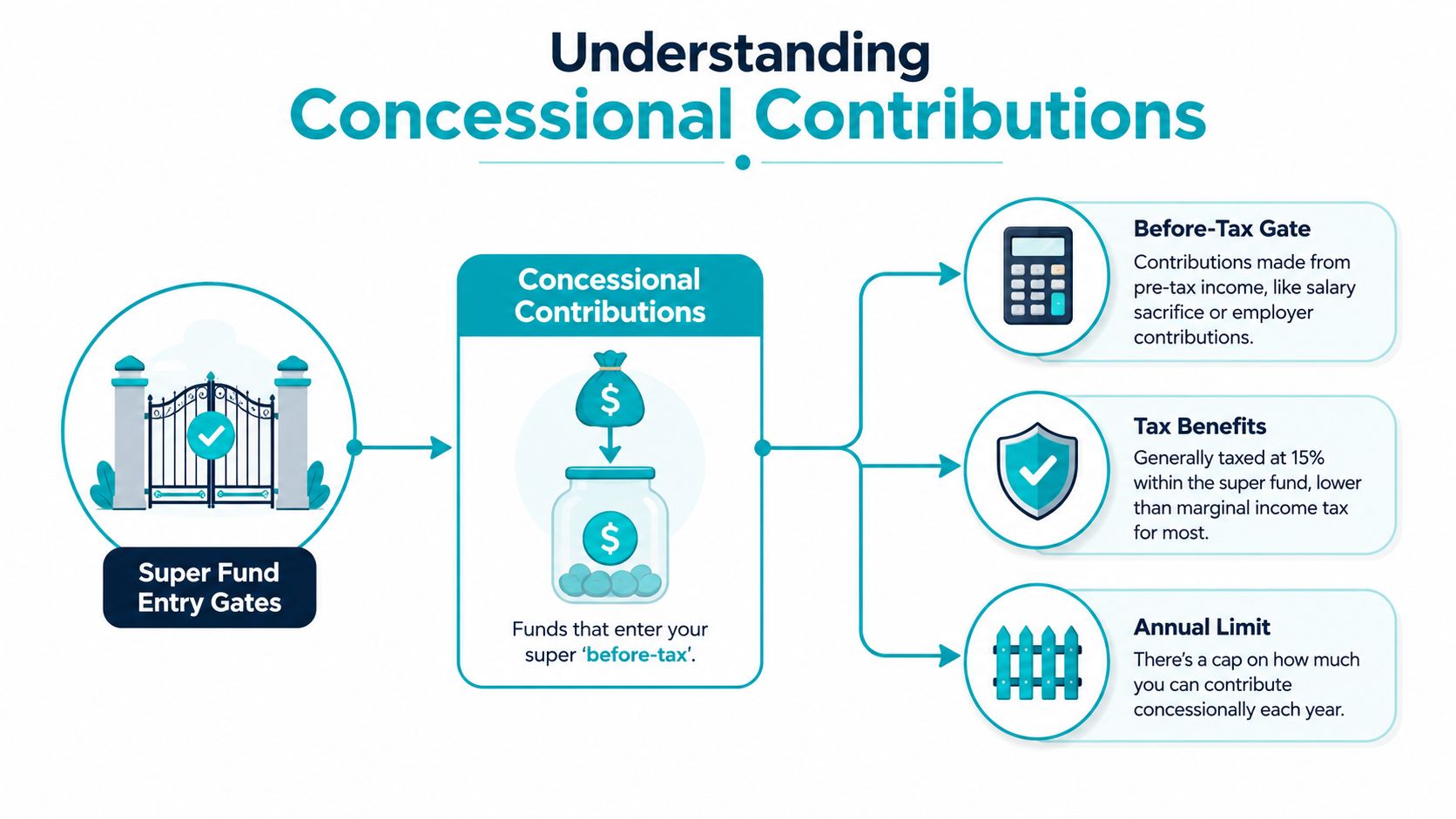

What Are Concessional Contributions

Think of super as having two entry gates. One gate is for money that goes in before tax. The other is for money that goes in after tax. Concessional contributions use the before-tax gate.

That matters because these contributions are generally taxed at 15% within the super fund rather than being taxed fully in your own name first. For many people, that makes concessional contributions one of the cleanest ways to build retirement savings in a tax-effective way.

What counts as concessional

From 1 July 2026, the concessional contribution cap increases to $32,500 per annum, indexed to AWOTE and up from $30,000. This cap covers all before-tax contributions, including employer Super Guarantee payments, salary sacrifice, and personal deductible contributions, as outlined in Heffron's summary of the 2026 super contribution cap changes.

In practical terms, concessional contributions usually fall into three groups:

- Employer contributions: These are the compulsory Super Guarantee amounts your employer pays.

- Salary sacrifice amounts: These are extra before-tax contributions arranged through payroll.

- Personal deductible contributions: These are personal contributions you later claim as a tax deduction, if you meet the requirements.

If you're comparing this with after-tax super strategies, it helps to understand the separate rules around non-concessional contributions, because the limits and balance tests are different.

Why this matters for real planning

The bucket analogy is useful here. If your income lands in your personal bank account first, it has usually already gone through your personal tax system. If part of that income goes straight into super through the concessional route, it enters a different bucket with a different tax treatment.

Practical rule: Don't judge concessional contributions only by whether you “can afford extra super”. Judge them by what they do for tax today and retirement income later.

That's why these contributions are so useful for people who want structure. Regular salary sacrifice can create discipline. A well-timed deductible contribution can tidy up a strong income year. Both can help if they're measured against the actual cap and your wider plan.

The Annual Cap and Its History

The annual cap is the line you need to know before making any before-tax super contribution decision. It isn't chosen at random, and it doesn't stay fixed forever. The cap is indexed to AWOTE and moves in $2,500 increments, which is why it stays unchanged for periods and then lifts when indexation pushes it high enough, according to the ATO's concessional contributions cap guidance.

Historical concessional contribution caps

| Financial Year | Annual Cap |

|---|---|

| 2021 to 2024 | $27,500 |

| 2024 to 2026 | $30,000 |

| 2026 to 2027 | $32,500 |

That history matters because it explains two things. First, older unused cap amounts may have been built under different annual limits. Second, the system is designed to move with wages over time rather than being rewritten manually every year.

Why advisers watch indexation closely

If you only look at the current cap, you miss the planning context. Someone making regular salary sacrifice might update payroll settings when the cap changes. A pre-retiree considering a one-off deductible contribution has a different task. They need to know the current cap, how much employer super is already using it, and whether earlier years created unused room.

That's where historical context becomes practical rather than academic.

For readers who want an accountant's perspective on how the cap increase affects year-ahead tax decisions, Baron Accounting's tax advice is a useful companion read. It's especially helpful if you're aligning contribution timing with broader tax planning.

What doesn't work

What usually fails is estimating. People often say, “My employer super won't be much,” or “I'll just add a round number before 30 June.” That approach causes problems because the cap applies across all super accounts, not one fund at a time, and all concessional contributions are counted together.

A better approach is to treat the cap as a yearly budget. Every employer contribution, every salary sacrifice payment, and every deductible contribution draws from the same allowance. Once you start thinking of it that way, the decisions get cleaner and the risk of a nasty surprise drops.

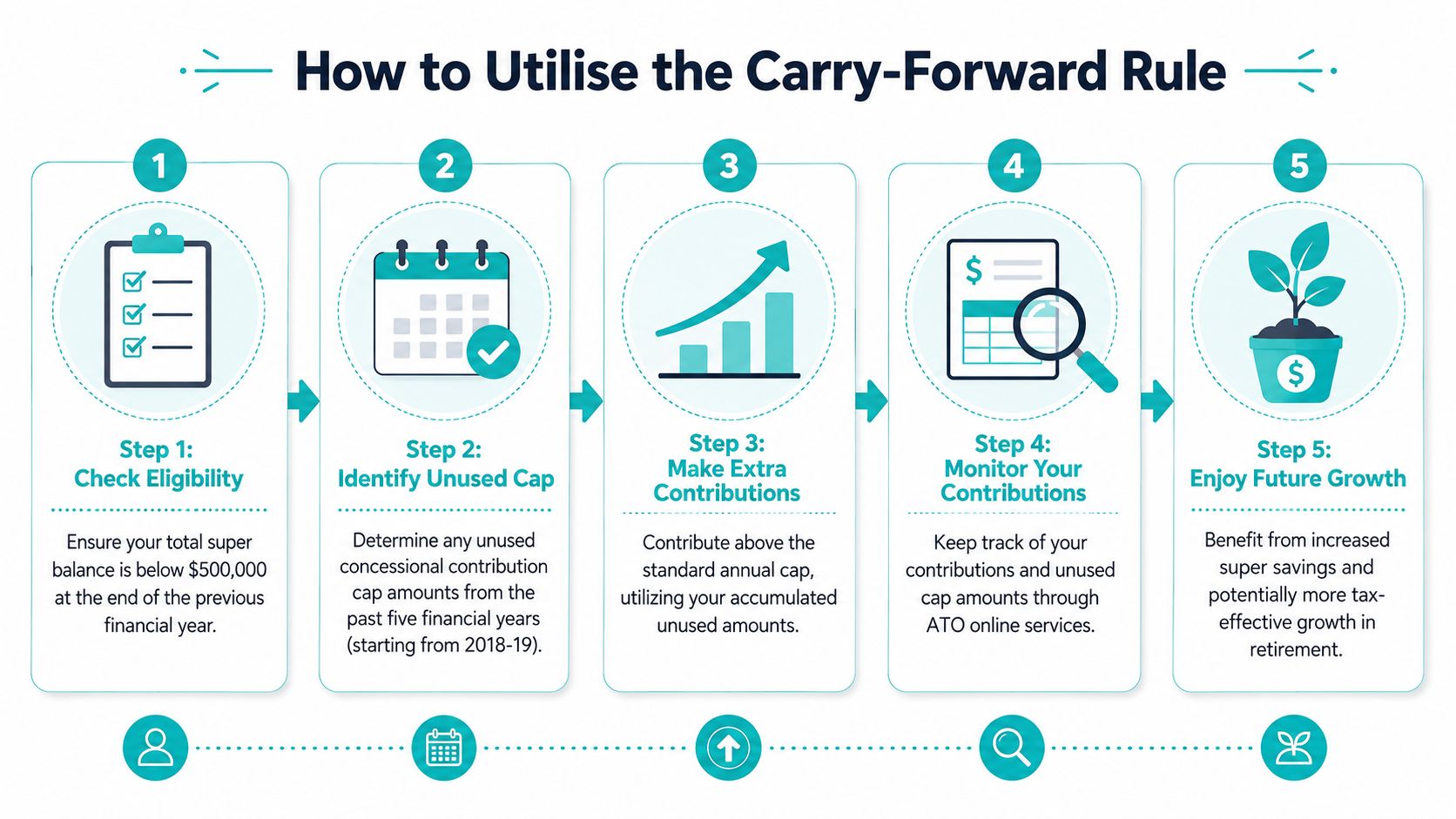

Unlocking the Carry-Forward Contribution Rule

This is the rule many people should check before they rule themselves out.

The carry-forward rule lets eligible people use unused concessional cap amounts from the previous five years, but only if their total super balance was less than $500,000 at 30 June of the previous financial year, as explained in Vanguard's contribution caps guide.

The three questions to ask

If you're trying to work out whether this rule helps you, keep it simple.

Is my balance eligible?

Your total super balance must have been under $500,000 at the previous 30 June.Do I have unused cap amounts?

If you didn't fully use your concessional cap in one or more of the previous five financial years, those unused amounts may still be available.Am I acting before the oldest amount expires?

Unused amounts expire after five years on a rolling basis. Leave them too long and the oldest year drops away.

That rolling window is what makes this rule valuable and easy to waste. Clients often focus on whether they can contribute more now, but the sharper question is whether an old unused amount is about to disappear.

Who tends to benefit

This strategy often suits people whose income hasn't been steady.

- Small business owners: Lean years may have left cap space unused, and a stronger year can create room to contribute more.

- People returning to work: Time out of the workforce often means earlier caps weren't fully used.

- Pre-retirees with a one-off event: An asset sale, bonus, or final high-income year can make a larger deductible contribution worth considering.

If you want a more detailed explanation of the mechanics and timing, this guide on carry-forward concessional contributions is a helpful reference point.

Unused concessional cap space is only valuable if you confirm it before making the contribution. Assumptions are where most errors start.

What works in practice

The cleanest method is to verify your available amount through ATO reporting before any contribution is made. Then map the contribution against your existing employer payments for the year. Finally, make sure the contribution timing and any deduction paperwork are completed correctly.

What doesn't work is relying on memory. Individuals often do not accurately remember how much employer super was paid in each prior year, whether a prior deductible contribution was claimed, or whether an old unused amount is about to lapse. The carry-forward rule rewards precision, not guesswork.

Advanced Rules and Common Pitfalls to Avoid

The biggest mistake I see isn't usually overconfidence. It's false disqualification. People assume they can't use a strategy because they've blended two separate balance tests into one.

That confusion matters most for pre-retirees, because they're often deciding whether to boost super aggressively in the years just before work slows down or stops.

The threshold mix-up that costs people opportunities

A common point of confusion is mixing up the total super balance threshold for carry-forward concessional contributions, which is under $500,000, with the threshold for the bring-forward non-concessional rule, which is under $1.84 million for the full amount, as discussed in this explanation of the carry-forward and bring-forward threshold confusion.

These are not interchangeable tests.

If your balance is above the carry-forward threshold, that affects one strategy. It does not automatically tell you anything about your access to the separate bring-forward non-concessional rules. And if your balance is below the higher bring-forward threshold, that still doesn't make you eligible for carry-forward concessional contributions unless you also satisfy the lower test.

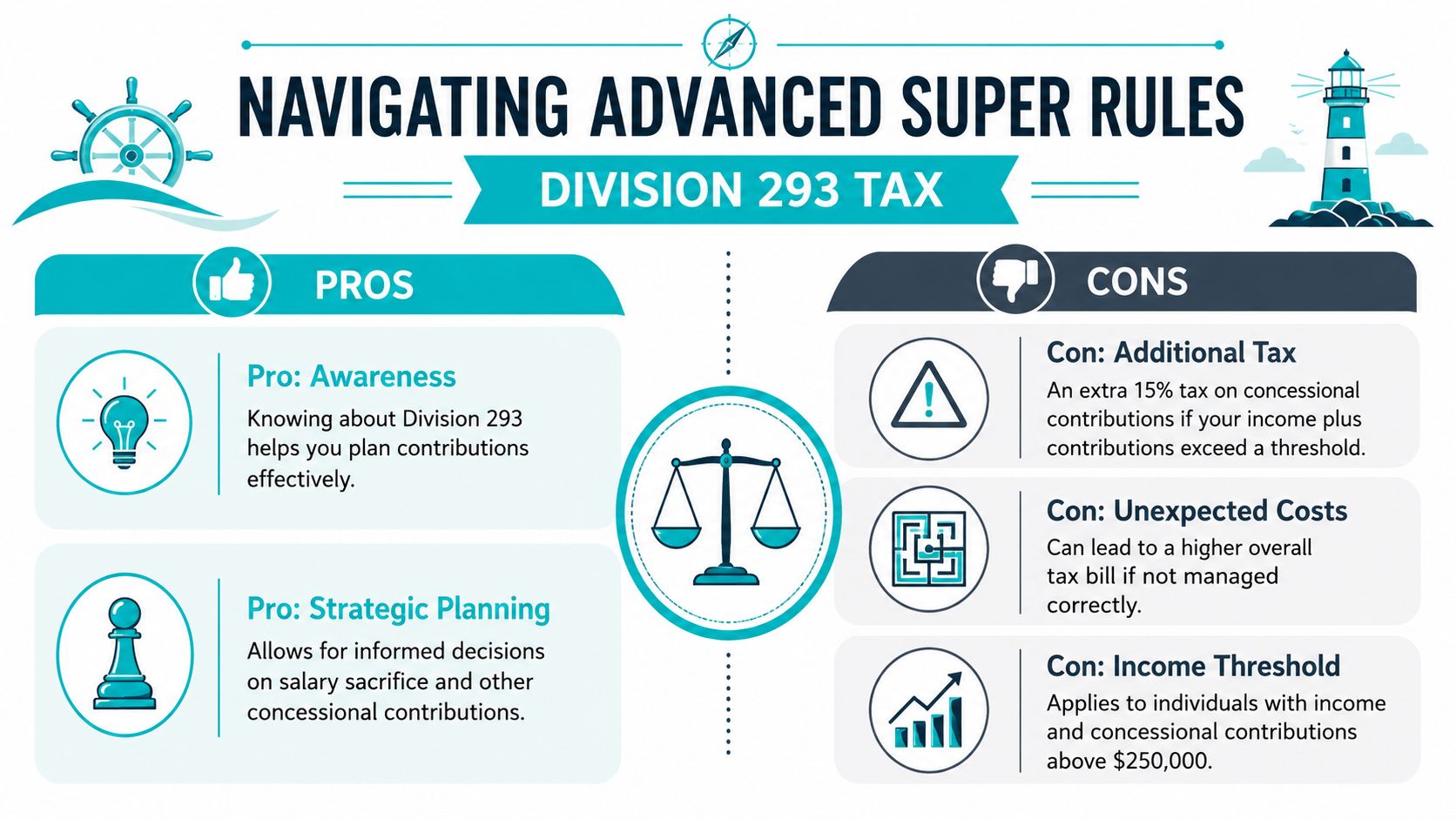

Division 293 tax

There's another advanced rule that catches high-income earners. If your income, including super contributions, is more than $250,000 annually, concessional contributions may face an additional 15% Division 293 tax, lifting the effective tax on those contributions to 30%, based on Vanguard's explanation of contribution tax rules.

The planning point here isn't that concessional contributions suddenly become pointless. Often they can still be useful. The key insight is knowing the extra tax may apply so the contribution decision is made with open eyes.

Clients usually handle Division 293 well once they know it's part of the picture. The frustration comes when they discover it after contributing, not before.

Pitfalls worth checking before you act

- Using the wrong balance threshold: This is the most common planning error in this area.

- Ignoring employer super: Many people only count their voluntary contributions and forget compulsory payments are already filling part of the cap.

- Thinking all super strategies use the same rules: Concessional and non-concessional contributions operate under different caps and balance tests.

- Contributing first and verifying later: That sequence works poorly. The check needs to happen upfront.

If the rules seem close but not quite clear, that's usually the signal to pause. In super planning, “nearly right” can become expensive.

Worked Examples and Tailored Strategies

Rules become useful when they fit a person, not when they sit neatly in a table.

Here are three situations that come up often in advice conversations. The details differ in real life, but the decision logic tends to be similar.

Young accumulator

A professional in their 30s wants to build super without making the budget feel tight. The smartest move often isn't a dramatic one-off contribution. It's a steady salary sacrifice arrangement that gets reviewed when pay changes or when the annual cap changes.

The trade-off is simple. Extra money into super today generally means less cash flow outside super. For someone still building an emergency fund, paying down debt, or saving for a home, pushing too hard can create stress. What works better is a contribution level that's sustainable and monitored through payroll.

In this context, process beats enthusiasm. Check what the employer is already contributing. Add a salary sacrifice amount that stays within the cap. Revisit it each year. Consistency usually wins.

High-income earner

An executive in their 40s often has a different question. They're less worried about whether they can contribute, and more focused on whether the contribution still makes sense if Division 293 applies.

For this person, the mistake is treating concessional contributions as either fully attractive or not worth doing at all. The answer is usually more nuanced. They may still use concessional contributions as part of a broader tax and retirement strategy, but they need to allow for the possibility of extra tax and keep their wider cash flow, debt position, and investment strategy in view.

A clear contribution plan works better than an impulsive June top-up. Where there are bonuses, multiple income sources, or changing remuneration structures, a mid-year check is often more useful than a last-minute estimate.

Pre-retiree planning around the wrong threshold

This is the scenario where the threshold confusion does the most damage.

A person in their late 50s wants to add a meaningful amount to super after a successful financial event. They've heard they need to be under $500,000 to “bring forward” contributions, so they assume the opportunity is gone. In fact, the full non-concessional bring-forward rule is available where total super balance is less than $1.84 million as at 30 June 2026, allowing contributions of up to $390,000, and that is a separate rule from concessional carry-forward, as set out in Rest's contribution caps guide.

That distinction changes the conversation entirely.

The right strategy here depends on what kind of contribution they're trying to make. If the goal is a larger before-tax contribution using unused concessional caps, the lower carry-forward balance test matters. If the goal is a larger after-tax contribution under the bring-forward rule, the higher threshold is the relevant one. Many people wrongly abandon both strategies because they apply one test to both.

What tailored advice usually changes

The planning outcome improves when someone helps coordinate the moving parts:

- Contribution type: before-tax or after-tax

- Balance test: which threshold applies to which strategy

- Timing: whether action should happen now or after a balance date

- Paperwork: especially for deductible contributions

- Broader plan: retirement timing, debt, cash reserves, and tax

That's why a personalized approach matters. A firm like Wealth Collective can pull together ATO contribution records, identify unused concessional cap space, and place that decision inside a broader retirement or wealth-building plan rather than treating super as a stand-alone transaction.

Take Control of Your Super Strategy Today

Concessional contribution limits are one of those areas where a little clarity can save a lot of second-guessing. The rules themselves aren't impossible. The challenge is applying the right rule to the right contribution type, in the right year, with the right records.

If you're taking action soon, focus on a short checklist.

- Confirm the current cap: Know how much room you have before making any before-tax contribution.

- Check your existing contributions: Employer payments count, even if you haven't been tracking them closely.

- Separate the thresholds: Don't let the carry-forward and bring-forward balance tests blur into one rule.

- Match the strategy to the goal: Tax savings, retirement funding, and flexibility outside super all need balancing.

This gets even more important when your finances cross into multiple jurisdictions or asset classes. If part of your retirement picture includes overseas property, understanding the broader tax implications for global property investors can help frame how super fits into your total plan.

For people who want structure around these decisions, Retirement Roadmap and Guided Growth are built for exactly this kind of work. The aim isn't to add complexity. It's to turn contribution rules into a practical plan you can follow with confidence.

If you want help working out which super contribution rules apply to you, book a complimentary introductory call with Wealth Collective. It's a simple starting point for sorting out concessional caps, carry-forward opportunities, and how they fit into your wider retirement plan.