Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

When you hear people talk about a Self-Managed Super Fund (SMSF), the first thing that usually comes to mind is control. And for good reason. It’s the single biggest shift you can make—going from a passive member in a massive fund to someone who actively directs where their retirement savings are invested. This means you can build wealth your way, whether that’s through direct property, specific shares, or other unique opportunities.

What Is a Self-Managed Super Fund?

Think of it this way: a regular super fund is like being a passenger on a bus. You know the general destination is 'retirement', but the driver—a professional fund manager—chooses the route from a set menu of options. An SMSF, on the other hand, hands you the keys to the car.

You, along with up to five other members (usually family), become the trustees of your own private super fund. You are in charge of every decision, from the investment strategy to ensuring it all stays compliant with the law. This is a world away from having your money pooled with millions of others in a standard industry or retail fund.

Who Is an SMSF Designed For?

So, who takes the leap? An SMSF is for Australians who want to be hands-on with their retirement savings and have a clear vision for their wealth. We find it’s a particularly powerful strategy for:

- Business Owners: Many use their SMSF to purchase their own commercial premises, effectively paying rent to their own super fund.

- Experienced Investors: People who want to go beyond the standard investment options and invest directly in specific shares, ETFs, or even unlisted assets not available elsewhere.

- Families and Partners: An SMSF allows you to pool your super balances, creating a larger investment pot that can open up bigger opportunities and create cost efficiencies.

- Anyone Focused on Estate Planning: If you want more control over how your wealth is passed on, an SMSF provides far more sophisticated tools to ensure your wishes are carried out precisely.

An SMSF gives you the power to build a portfolio that truly reflects your personal goals, your tolerance for risk, and your vision for the future. It's about taking direct ownership of your retirement outcome.

This guide will walk you through the powerful benefits an SMSF can offer, from investment control to significant tax and estate planning advantages. Of course, with great power comes great responsibility. For a deeper dive into the mechanics, have a look at our detailed article on what is a SMSF and how it works. At Wealth Collective, our process is built around helping you navigate this journey with clarity and confidence.

Gaining Control and Investment Flexibility

If you've ever felt frustrated by the limited 'set menu' of your industry or retail super fund, you're not alone. Most big funds box you into a handful of broad investment options. A self-managed super fund (SMSF) completely changes the game, giving you direct control to build a portfolio that truly reflects your own financial strategy.

This control allows you to invest in assets you understand and believe in, moving beyond generic fund options. It’s about creating a retirement plan that is genuinely yours.

Expanding Your Investment Horizons

With an SMSF, your investment choices suddenly become much wider. Instead of just picking a "balanced" or "high growth" option, you can take direct ownership of specific assets for a far more targeted approach.

For example, you could:

- Invest in direct property: A huge reason many people set up an SMSF. Many of our business-owner clients use their fund to buy their commercial premises, effectively paying rent to their future selves. For a deeper dive, check out our guide on buying property with your super.

- Build a specific share portfolio: Researched a few key ASX-listed companies or promising tech stocks? You can buy them directly, rather than having them diluted in a generic "Australian Shares" fund.

- Access unlisted assets: This opens up opportunities to invest in things like private companies or specialised managed funds that aren't available on the public market.

An SMSF moves you from being a passenger in your financial journey to being the pilot. It allows you to direct your capital towards assets you've personally researched and believe in for your future.

Think about a local business owner who uses their SMSF to buy the workshop their business operates from. They instantly secure their business location while turning a major expense—rent—into a powerful contribution to their own retirement fund. It’s a smart, strategic move that’s simply impossible in a standard super fund.

A Strategy Guided by Your Goals

Having this much choice is empowering, but it also means having a clear investment strategy is non-negotiable. The aim isn't to invest in everything; it’s to choose the right things that align with your specific retirement goals.

This is exactly where our 'Guided Growth' service comes in. We act as your expert co-pilot, helping you assess opportunities and build a portfolio that matches your risk appetite and ambitions. We handle the complex compliance and administration, freeing you up to focus on making smart investment decisions.

To explore how we can help you take control, book an initial call with our team today.

Making the Tax System Work For You

While investment control is a huge drawcard, the real power of an SMSF often lies in its unique tax environment. This isn't just about shaving a few dollars off your tax bill; it's about using deliberate, powerful strategies to grow your retirement nest egg faster.

These are sophisticated strategies that simply aren't on the table with a standard industry or retail fund. Getting them right, however, requires a solid plan and a good grasp of the rules, which is where having an expert in your corner makes all the difference.

The Goal: A Tax-Free Retirement Income

Here’s where it gets really interesting. Once you retire and switch your fund from accumulating wealth to paying you a pension, the game changes completely. The investment earnings and capital gains your pension assets generate can become entirely tax-free.

Think about that for a moment. If your SMSF owns a portfolio of dividend-paying shares or a rental property, the income they produce could land in your fund without a cent going to the tax office. That’s more money available for you to live on, year after year.

It's a fundamental shift. In a standard fund, your returns are typically taxed. With an SMSF in the pension phase, that entire return can be reinvested or paid out, letting your money work much harder for you in a tax-free environment.

Smartly Managing Capital Gains

Another major advantage of an SMSF is the ability to be strategic with Capital Gains Tax (CGT). You’re in the driver's seat, deciding exactly when to sell an asset to achieve the best possible tax outcome.

For instance, if you're nearing retirement and own an asset that has grown substantially, you can plan the sale carefully. By waiting to sell it after your fund has moved into the tax-free pension phase, you could potentially wipe out the entire tax bill on the gain. That’s a potential CGT rate dropping from 10% (for assets held over 12 months) all the way down to zero.

Let’s see what this looks like with a quick example:

- The Asset: A commercial property bought for $500,000, now valued at $800,000.

- The Capital Gain: $300,000.

- Tax if sold during accumulation phase: $30,000 (at the discounted 10% rate).

- Tax if sold during pension phase: $0.

A single, well-timed decision like this could leave an extra thirty thousand dollars in your super fund, not with the ATO. This is the kind of meaningful impact that highlights the value of an SMSF when managed correctly.

Helping our clients build a tax-optimised plan is the heart of our 'Retirement Roadmap' service. We work with you to structure your fund and time your decisions to make the most of these rules. To see how these strategies could apply to your financial situation, book an initial call with our team today.

Comparing SMSFs with Traditional Super Funds

When you're looking at your super, the choice between a standard industry or retail fund and a Self-Managed Super Fund (SMSF) boils down to one simple question: how involved do you want to be?

Most super funds offer a straightforward, 'set-and-forget' experience. It’s simple, and for many people, that’s enough. But an SMSF is built for those who see their super not just as a retirement account, but as a powerful vehicle for wealth creation they want to sit in the driver's seat for.

The appeal for many is the potential to directly shape their own financial outcomes. And the numbers back this up. Over the five years to June 2024, SMSFs actually outperformed their APRA-regulated counterparts by 1.1 percentage points. It's a trend we've seen consistently, confirming that with the right strategy, taking control can pay off. You can dive deeper into the data yourself in this comprehensive report on SMSF statistics and record growth.

Performance, Fees, and Flexibility

This performance edge often comes from the sheer flexibility an SMSF gives you. You're not picking from a limited menu; you're tailoring every single investment to fit your personal roadmap.

The standard super fund model, on the other hand, usually runs on a percentage-based fee. It’s a quiet problem that gets louder over time—as your balance grows, the dollar amount you’re paying in fees grows right along with it, creating a drag on your long-term returns.

The SMSF model flips this on its head. Most run on a fixed-cost basis for administration and compliance. As your super balance scales up, your fees, as a percentage of your assets, actually shrink. This creates a tipping point where an SMSF becomes a far more cost-efficient engine for growth.

An SMSF’s fixed-fee structure can turn it into a more cost-effective vehicle for growing wealth as your balance scales. This is a critical advantage over percentage-based fees that penalise you for successful investing.

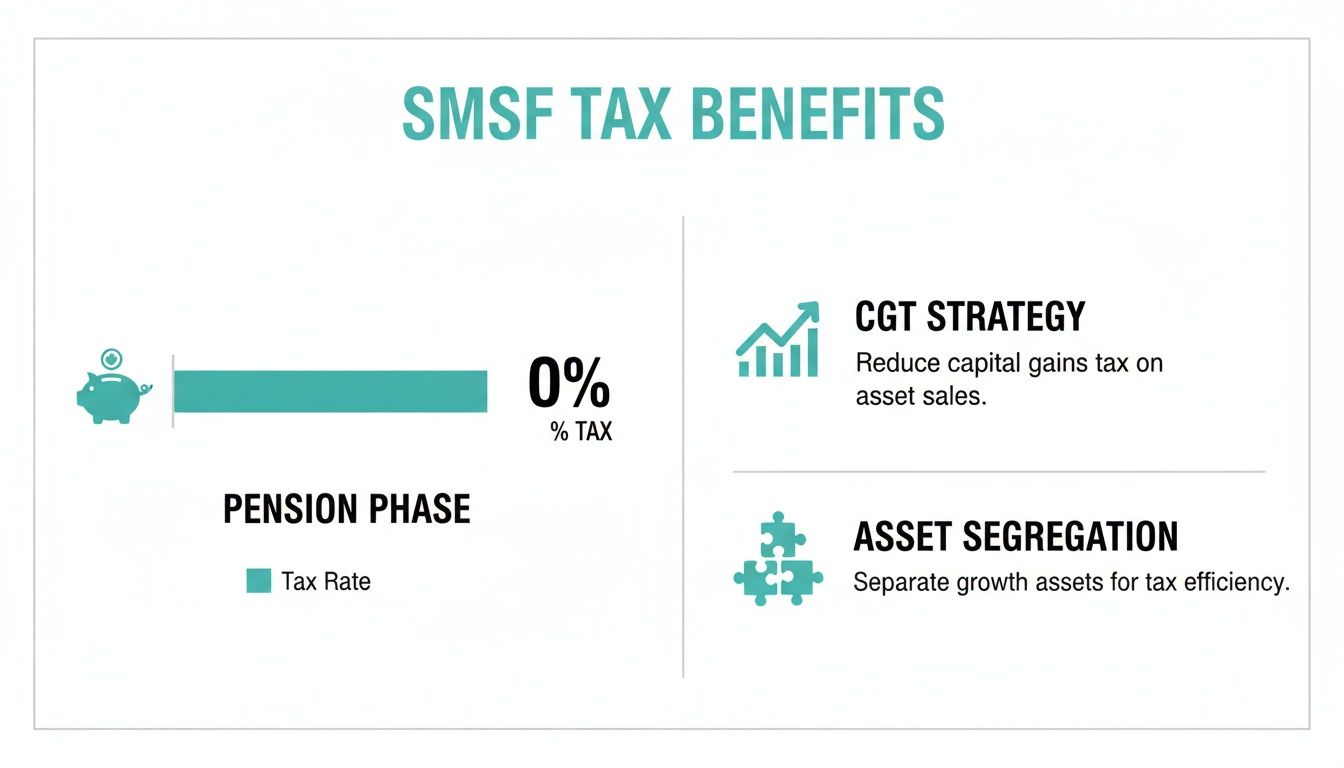

The control an SMSF provides also unlocks some incredibly powerful tax strategies that just aren't possible in a large public fund. This infographic gives a great visual summary of what that can look like.

As you can see, we’re talking about major advantages like operating in a 0% tax environment once you start a pension, or actively managing your assets to legally minimise Capital Gains Tax—things that can make a monumental difference to your final nest egg.

SMSF vs APRA-Regulated Funds At a Glance

To put it all into perspective, here’s a straightforward, side-by-side look at how these two approaches stack up against each other.

| Feature | Self Managed Super Fund (SMSF) | Industry / Retail Fund |

|---|---|---|

| Investment Choice | Almost unlimited, including direct property, shares, and art. | A limited menu of pre-mixed investment options. |

| Control | You are the trustee, making all strategic decisions. | Decisions are made by a professional fund manager. |

| Fee Structure | Often a flat annual fee, making it cost-effective for larger balances. | Typically a percentage of your total balance. |

| Tax Strategy | Advanced strategies like asset segregation and timing CGT. | General tax rules apply to the entire fund, with no individual control. |

Looking at the table, it’s clear they are two very different beasts. The key is figuring out which one is the right tool for you.

Understanding these fundamental differences is the first step. The next is to work out if an SMSF truly aligns with your financial situation and retirement goals. Pinpointing that moment where an SMSF becomes the smarter financial choice requires a personalised look at your circumstances. If you're wondering if you’ve hit that tipping point, a chat with our team at Wealth Collective can bring clarity.

Securing Your Legacy with Estate Planning

Beyond investment returns and tax strategies, one of the most powerful reasons people choose an SMSF is deeply personal: legacy. An SMSF gives you a level of certainty over what happens to your wealth that you simply can't get with a large public fund.

For many of our clients, super isn't just a retirement nest egg. It’s a foundational part of their family's future. An SMSF provides the framework to ensure those assets are managed exactly the way you want, long after you’re gone.

Directing Your Wealth with Precision

In a typical retail or industry fund, your death benefit nomination is often treated as a strong suggestion. The fund's trustee ultimately has the final say on who gets your money, and their decision might not align with your wishes. An SMSF flips this on its head.

By setting up a correctly worded Binding Death Benefit Nomination (BDBN), you create a direct and non-negotiable instruction. It’s a clear roadmap for your super balance, ensuring your wealth flows to your chosen beneficiaries without debate or delay. You can read more about the specifics in our guide on what happens to your super when you die.

An SMSF transforms your estate plan from a hopeful wish into a concrete directive. It puts the power back in your hands to decide exactly who gets your super, how, and when.

Ensuring Generational Wealth Transfer

Here’s where an SMSF really stands apart. It can continue to operate even after a member passes away. This is a game-changer for families wanting to keep specific assets—like a business premises or a family farm—within the super structure for the next generation.

Instead of being forced to sell a valuable property to pay out a death benefit, the fund can hold onto the asset. From there, it can pay a pension to the surviving spouse or children. It’s a seamless way to transfer wealth and keep the family’s legacy intact.

This kind of forward-thinking strategy is at the very heart of our ‘Protection Plus’ service. We specialise in building robust financial structures that don't just grow wealth, but protect it for the generations to come. If securing your legacy is a top priority, let’s have an initial chat to see how an SMSF can make that a reality.

Taking the Helm: Your Role as Trustee and How We Can Help

Let's be upfront: taking the reins of your super with an SMSF isn't just about investment freedom. It also means you’re stepping into the role of a trustee, and that comes with serious legal responsibilities.

But here’s the thing—it's a commitment you don't have to face alone. It’s less like taking on a second job and more like becoming the chairperson of your own wealth, with a dedicated team handling the day-to-day operations for you.

What Being a Trustee Really Means

As a trustee, you are legally responsible for running the fund in line with Australian superannuation law. The rules are clear and strictly enforced, but they essentially boil down to a few core duties:

- Acting honestly in every decision you make for the fund.

- Ensuring the fund meets the sole purpose test, meaning it exists only to provide retirement benefits for its members.

- Creating and maintaining a formal investment strategy, and reviewing it regularly.

- Keeping meticulous records of all decisions, transactions, and member communications.

- Organising an annual audit with an approved, independent SMSF auditor.

That list can feel intimidating. This is where many people wonder if it's all too much. But it’s a structured process, and it’s precisely where a specialist partner like Wealth Collective comes in. We handle the administrative burden and ensure your compliance is bulletproof, freeing you up to focus on the strategic decisions that actually grow your wealth.

We take the paperwork, compliance checks, and endless deadlines off your plate. This frees you up to concentrate on the bigger picture—scoping out that perfect property investment, researching new shares, and confidently steering your fund toward your goals.

Ultimately, the incredible control and flexibility of an SMSF are unlocked when the fund is managed correctly. You don't need to become an expert in tax law overnight, but you do need an expert team in your corner.

Ready to see how we can make managing your own super fund straightforward and successful? Book a complimentary, no-obligation 10-minute initial call with our team to find out more.

Your SMSF Questions Answered

It's natural to have questions when you're considering a big financial step like setting up an SMSF. Let's tackle some of the most common ones we hear from our clients.

How Much Money Do I Need to Start an SMSF?

This is probably the most frequent question we get. While industry bodies often suggest $200,000 to $500,000 as a cost-effective starting point, there’s no magic number set in stone.

The real answer depends entirely on your strategy. For instance, if you and your partner are pooling your super together, a lower combined balance can work perfectly well. Or, if you have a clear plan to buy a property within the fund and expect strong growth, starting with less can make a lot of sense.

It's less about hitting a specific number and more about whether the strategy is right for your goals. A quick chat with an adviser is the best way to figure out if the sums add up for you.

Can I Borrow Within My SMSF to Buy Property?

Yes, you can, and for many people, this is a game-changer. The structure that allows this is called a Limited Recourse Borrowing Arrangement (LRBA).

Essentially, an LRBA lets your super fund take out a loan to buy a single asset, like a commercial or residential property. The 'limited recourse' part is the crucial detail—it acts as a safety barrier. If the loan defaults, the lender can only ever claim the property itself, not any of the other assets sitting in your fund.

An LRBA is a powerful tool, but getting the setup wrong can be a costly compliance nightmare. This is exactly the kind of complex structuring our team at Wealth Collective specialises in, ensuring it’s done right from day one.

What Happens If I Make a Compliance Mistake?

The ATO takes SMSF rules very seriously, and making a mistake—even an honest one—can lead to hefty penalties or nasty tax implications. This is precisely why having an expert in your corner isn't just a good idea; it's vital.

At Wealth Collective, we handle the intricate compliance and administration for you. We lodge the paperwork, watch the deadlines, and ensure your fund’s activities are always above board. It gives you the freedom and peace of mind to focus on what really matters: making smart investment decisions for your future.

Feeling clearer about whether an SMSF is the right move for you? The only way to know for sure is to have a chat. At Wealth Collective, our 'Guided Growth' and 'Retirement Roadmap' services are designed to make the entire process straightforward and stress-free. Book a complimentary 10-minute call with our Perth-based team to get personalised answers to your questions.