Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Searching for the best trauma insurance in Australia reveals a simple truth: there's no single 'best' policy. The right cover is deeply personal, tailored to your health, finances, and life stage. However, the top policies always share three key traits: comprehensive medical definitions, a strong claims history, and a premium that fits your budget.

Defining the Best Trauma Insurance for Your Needs

A serious diagnosis can change everything in an instant. Beyond the emotional toll, the financial pressure can be overwhelming. This is where trauma insurance (also known as critical illness cover) provides a crucial safety net. It pays a lump sum if you're diagnosed with a specified condition, giving you the financial breathing room to focus solely on your recovery.

But this isn't an off-the-shelf product. The real value is hidden in the policy details, not the price tag. A cheaper policy might seem appealing, but it could have narrow definitions for conditions like heart attack or cancer, making a successful claim difficult. Conversely, the most expensive policy might be filled with features you'll never use.

Understanding the Risks and Why Quality Cover Matters

To grasp why robust cover is essential, look at the claims data. A cancer diagnosis is the leading cause, accounting for a staggering 48% of all trauma insurance claims, according to the latest insurer data. Heart-related conditions follow at 20%, with accidents at just 3%. These figures underscore why trauma cover is a non-negotiable part of financial security, especially for young professionals, dual-income families, and business owners. To understand the landscape better, you can review the latest claim statistics.

The goal is to find the perfect fit—a policy that aligns with your life. This table shows how the "best" cover changes depending on your circumstances.

| Your Situation | What "Best" Looks Like | How Wealth Collective Helps |

|---|---|---|

| Young Professional | Affordable premiums with strong cover for major illnesses like cancer and stroke. | We identify policies that offer real value without compromising on critical definitions. |

| Dual-Income Family | Comprehensive cover that can replace lost income and manage the mortgage if one partner gets sick. | Our advisers structure a plan to protect your family’s lifestyle and financial future. |

| Small Business Owner | A policy providing funds to keep the business running or manage debts if you can't work. | We design a strategy that protects both your personal and business finances. |

The most critical aspect of trauma insurance is ensuring the Product Disclosure Statement (PDS) reflects modern medical standards and your personal risks. A policy with outdated definitions or significant exclusions could be useless when you need it most.

This guide provides the knowledge to compare policies confidently. At Wealth Collective, our 'Protection Plus' service takes the guesswork out of this process. Our expert advisers help you navigate the complexity to find cover that genuinely protects what matters, giving you true peace of mind.

8 Key Features to Compare in a Trauma Insurance Policy

When you start researching the best trauma insurance Australia offers, it's easy to get lost in the details. The true difference between a policy that looks good and one that delivers in a crisis is hidden in the fine print. Understanding these key features is essential for securing cover you can rely on.

Not all policies are created equal, and the wording in the Product Disclosure Statement (PDS) can determine your ability to claim. You must look beyond the monthly premium and scrutinise what you're actually paying for.

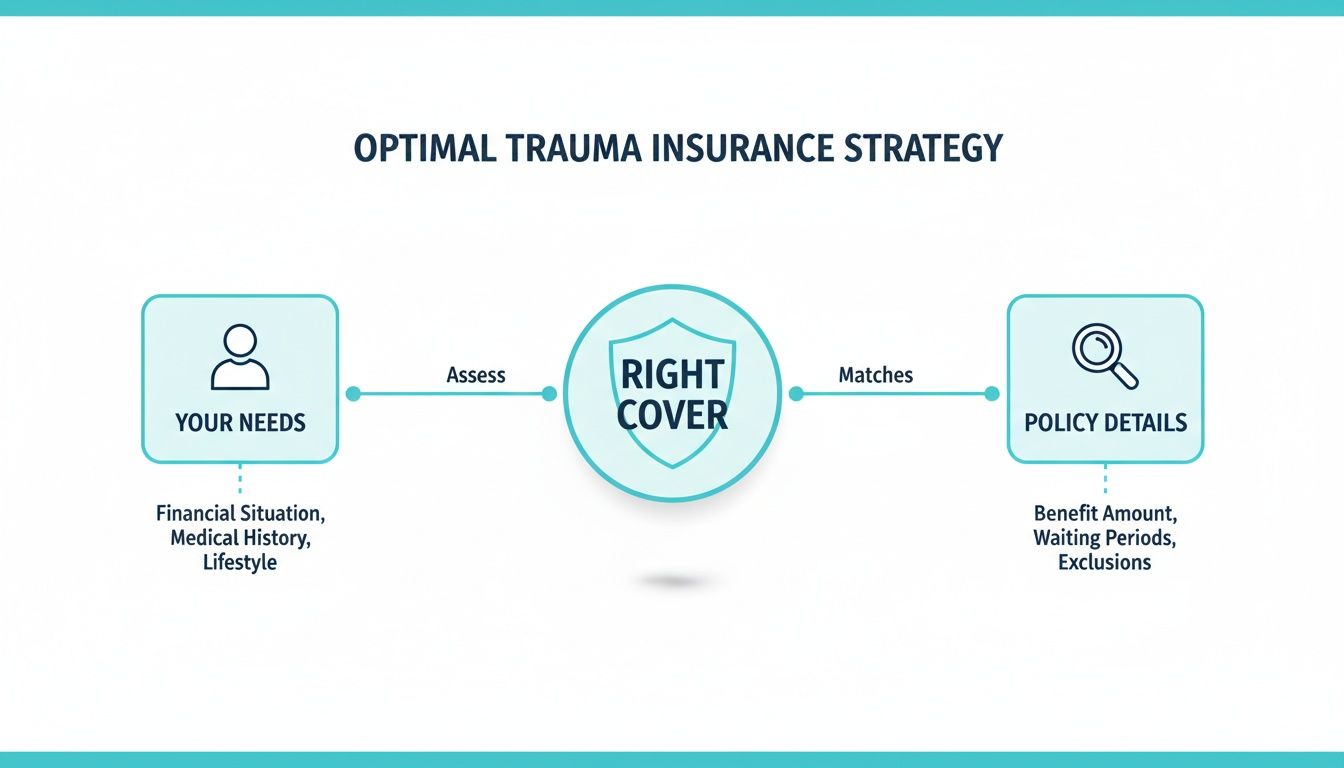

This flowchart illustrates the ideal process—it's about connecting your personal needs with the policy specifics to find the right cover.

A successful outcome depends on aligning these three elements, a process that requires careful consideration and expert guidance.

1. The Devil in the Definitions

If there’s one thing to get right, it’s this. The medical definitions are the specific clinical criteria that determine if your condition qualifies as a "trauma event" and triggers a payout. An outdated or overly strict definition can render your policy useless.

For instance, two policies might both cover "heart attack," but one may only pay for a major event meeting precise medical markers, while a better policy will also cover less severe attacks. Cancer definitions are equally critical. Many policies exclude early-stage or non-invasive cancers which, thanks to improved screening, are now common diagnoses.

You need policies with modern, medically robust definitions that align with current diagnostic practices. This is where an adviser's expertise is invaluable. At Wealth Collective, our process involves constantly reviewing insurer PDS documents to identify which ones offer the most relevant and fair definitions for our clients.

2. Partial Benefits and Advancement Payments

The best trauma policies aren't just all-or-nothing. They often include partial benefit payments or advancement payments for less severe conditions. These provide a smaller, upfront portion of your total cover for situations that don't meet the full trauma definition but still create significant financial stress.

This could include:

- Early-stage cancers: Such as carcinoma in situ, which may not trigger a full payout but requires treatment and time off work.

- Angioplasty: A common, less invasive procedure to clear blocked arteries that wouldn't meet the definition of a major heart attack.

- Loss of hearing or sight in one ear/eye: A serious event that some policies might not cover in full.

These features provide a crucial safety net, getting money into your hands faster and for a broader range of medical events.

3. Waiting Periods and Survival Periods

Two timeframes you must understand are the waiting period and the survival period.

The waiting period is the initial time after your policy begins—usually 90 days—during which you cannot claim for certain conditions like cancer or heart disease. This prevents people from taking out a policy when they already suspect a health issue.

The survival period is the length of time you must live after diagnosis before the insurer pays the benefit, typically around 14 days. It sounds grim, but it distinguishes a trauma claim from a life insurance claim.

A long survival period can add immense stress at the worst possible time. Our advisers prioritise policies with the shortest possible survival period to ensure funds are released quickly when they're most needed.

4. Standalone vs. Linked Policies

You can structure your trauma insurance in two main ways:

- Standalone Policy: This is a completely independent policy. A trauma claim has zero impact on your other insurance, like Life or Total and Permanent Disability (TPD) cover.

- Linked (or Bundled) Policy: This connects your trauma cover with your Life and/or TPD insurance. It’s often cheaper, but there's a trade-off: making a trauma claim reduces the benefit amount of your linked covers. For example, if you have a $1 million linked Life policy and claim $300,000 in trauma benefits, your remaining Life cover drops to $700,000.

To better understand how these policies interact, you can learn more about the different types of life insurance cover and how they form a comprehensive strategy.

5. The Importance of Buy-Back Options

If you opt for a linked policy, a buy-back option is an essential feature. This allows you to reinstate, or "buy back," the full amount of your Life or TPD cover after a trauma claim has been paid, usually 12 months after the event.

Without it, surviving a critical illness could leave you severely underinsured for death or disability in the future. This is exactly the kind of structural detail we scrutinise at Wealth Collective. Our process is designed to ensure your financial safety net remains fully intact, no matter what happens.

Balancing the Costs and Benefits of Your Policy

When considering trauma insurance, it’s easy to focus on the monthly premium—a tangible expense leaving your bank account. But viewing it merely as a cost misses the bigger picture. The real question isn't "What does it cost?" but "What financial future does it protect?"

Think of trauma insurance less as a bill and more as a strategic investment in your financial security. It's the asset that shields your wealth, your home, and your family's future from the devastating financial fallout of a serious medical diagnosis. It’s what can turn a potential financial catastrophe into a manageable life event.

Understanding the Premiums

Let's talk numbers. Many assume quality cover is prohibitively expensive, especially when young and healthy, but that's often not the case. Its affordability makes trauma insurance a smart move for Australians actively building their wealth.

For $300,000 of cover, a 30-year-old non-smoker might pay between $50 to $80 a month. This typically increases to $80-$120 by age 40 and $150-$250 at 50, reflecting the natural increase in health risks over time.

While APRA data shows average annual premiums are $1,778 for $213,000 of cover, the crucial part is that claims are paid. High acceptance rates confirm the value of these policies when needed. You can explore the trauma insurance claims statistics to see just how reliable this cover is.

This monthly investment is a fraction of what most people spend on discretionary items, yet it safeguards your single most important asset: your ability to earn an income and maintain your lifestyle.

When you reframe the premium as the price of guaranteeing financial stability during a medical crisis, its value becomes clear. It's not just another expense; it's a non-negotiable part of a sound financial plan.

The True Value of a Lump-Sum Payout

Now, contrast that manageable monthly premium with the power of a lump-sum payout. Receiving this tax-free payment gives you complete freedom to use the funds where they're needed most, creating financial breathing room when you are under immense pressure.

A payout could be used to:

- Bridge Medical Gaps: Cover out-of-pocket medical costs that private health insurance doesn't, like specialist consultations, experimental treatments, or rehabilitation.

- Eliminate Debt Stress: Pay down—or completely clear—your mortgage, car loans, and credit card debt, instantly reducing your financial and mental overheads.

- Fund Necessary Modifications: Pay for changes to your home or vehicle to accommodate new mobility needs, such as installing ramps or an accessible bathroom.

- Replace a Carer's Income: Allow your partner to take time off work to support you through treatment without the added stress of losing their income.

- Maintain Your Lifestyle: Cover everyday living expenses like school fees, groceries, and utility bills, ensuring your family’s life continues with as much normality as possible.

This financial freedom is the core purpose of trauma insurance. It's a powerful tool that gives you back choice and control. While income protection is vital for replacing your monthly salary, it comes with waiting periods and limitations. You can learn more about how superannuation and income protection work together to create a complete safety net.

At Wealth Collective, our 'Protection Plus' service performs this exact cost-benefit analysis for your specific situation. We don't just find you a policy; we build a protective strategy aligned with your financial goals, ensuring every dollar you invest in premiums delivers maximum security. The first step is a complimentary, no-obligation call to see how we can safeguard everything you're working so hard to build.

Real-World Scenarios Where Trauma Insurance is Crucial

It’s easy to view trauma insurance as just another policy—an abstract concept. But when seen through the lens of real life, its importance becomes clear. It’s not just a product; it’s a financial lifeline designed to protect what matters most when life presents its greatest challenges.

Let's walk through three common scenarios our clients face. Each story highlights a specific financial vulnerability and demonstrates how the best trauma insurance in Australia is never a one-size-fits-all solution, but a carefully tailored strategy.

These examples reflect the kind of tailored, strategic advice we provide at Wealth Collective every day. Our process ensures your cover acts as the critical safety net you need it to be, protecting you when you are most vulnerable.

The Young Professionals and Their First Mortgage

Meet Chloe and Ben, a professional couple in their early thirties. They've just bought their first home—a huge milestone, but one that comes with a significant mortgage. They rely on both their incomes to manage repayments and build their future.

For them, the biggest financial risk isn't a market downturn; it's one of them becoming seriously ill and unable to work.

Imagine Ben is diagnosed with a severe form of cancer, requiring at least a year off work for treatment. Without trauma insurance, the pressure on Chloe would be immense. She’d have to cover the entire mortgage and all their bills on one salary while supporting Ben through his recovery. Their dream home could quickly become a source of financial stress.

A well-structured trauma policy rewrites this story. Upon Ben's diagnosis, they receive a tax-free lump sum of $350,000, giving them immediate options.

- Wipe Out Debt: They can pay down a large portion of their mortgage, slashing their monthly repayments.

- Replace Lost Income: The funds cover Ben's lost salary, so bills are paid without draining their savings.

- Focus on Health: They can afford any out-of-pocket medical costs and choose the best care available without financial constraints.

For Chloe and Ben, trauma insurance wasn't just about covering an illness. It was about protecting their home, their lifestyle, and their ability to focus on what really matters—getting better.

The Small Business Owner Protecting Their Livelihood

Now, consider Sarah, a 45-year-old small business owner. She has poured her life savings and energy into her successful boutique. The business is thriving, but it depends entirely on her presence. To add to the risk, the business debts are secured against her family home.

If Sarah were to suffer a stroke, the consequences would be immediate. Months of rehabilitation would make it impossible for her to run the shop. Revenue would plummet, but expenses—rent, supplier bills, staff wages—would continue. The strain could force her to sell the business for a fraction of its value or, worse, risk her home.

This is where a trauma insurance payout becomes a business-saving lifeline.

A critical illness can dismantle a small business faster than any market downturn. Trauma insurance provides the crucial capital injection needed to keep the business viable while the owner recovers, protecting both their livelihood and personal assets.

With a $500,000 payout, Sarah has options. She can hire a temporary manager to keep the business running, cover all overheads, and service her debts without pressure. The money buys her what she needs most: time to recover fully, knowing her business and home are secure.

The Pre-Retiree Safeguarding Their Nest Egg

Finally, meet Mark and David, a couple in their late fifties. After decades of diligent saving, they are approaching a well-earned retirement. Their superannuation is healthy, and their plan is set. The one thing that could derail it all? A major health event forcing them to access their nest egg years ahead of schedule.

If Mark needs heart bypass surgery, the financial ripple effects would be significant. Even with private health insurance, out-of-pocket costs can be substantial. More importantly, a long recovery could prevent him from making those crucial final contributions to his super. They might have to draw on their retirement savings early to cover unexpected bills, permanently reducing their retirement income.

A trauma insurance policy acts as the ultimate shield for their retirement dream. A lump-sum payment allows them to cover all medical and recovery costs without touching their superannuation. It means Mark can retire when he’s ready, not when his health dictates. For Mark and David, it ensures their retirement looks exactly as they planned it.

These stories all point to a universal truth, a concept you can explore further in our guide on what life insurance covers. At Wealth Collective, our 'Protection Plus' service is about analysing your unique situation—your mortgage, your business, your retirement—and building a trauma insurance strategy that truly protects it. Book an initial call with us to discover how we can help secure your financial future.

Making a Claim: How to Get Paid When it Matters Most

A trauma insurance policy is only valuable if it pays out when you need it. The claims process is the ultimate test of the cover you chose, and it can feel daunting. You’re already dealing with a health crisis; the last thing you need is a stressful, drawn-out claims process.

Knowing what to expect and having an expert in your corner can transform the experience from a potential nightmare into a straightforward process.

Why Claims Get Knocked Back

The fear of a claim being denied is real. While most claims are successful, disputes happen, often due to a few critical and avoidable misunderstandings.

Here are the most common traps:

- Forgetting the Details (Non-Disclosure): Failing to mention a past health issue on your application can have serious consequences. Insurers are thorough, and if they find something was omitted, they can void your policy. Complete honesty from day one is crucial.

- The Devil in the Definition: The medical definitions for events like a heart attack or specific cancers are incredibly precise. If your diagnosis doesn't meet every single criterion in your policy's fine print, the claim will be denied.

- Outdated Policies: Medical science advances quickly, but insurance policies don't always keep pace. A modern, less invasive cancer treatment might not be covered under an older policy’s definition, leaving you unprotected.

These pitfalls highlight a simple truth: the most important work is done before you ever need to claim. Getting the setup right is what ensures a smooth payout.

The Value of Having an Expert in Your Corner

The statistics paint a clear picture. In 2023, policies arranged through a financial adviser had an impressive 86.0% success rate, with some insurers like NobleOak reaching 97.6%. At the same time, claim disputes are rising, often due to those tricky medical definitions. You can dive deeper into these insurance claims statistics on InsuranceWatch.

Having an adviser manage your claim is a game-changer. Instead of you chasing paperwork and deciphering medical jargon while trying to recover, we do it all for you. We become your advocate, your administrator, and your voice.

This is exactly why we created our Protection Plus service at Wealth Collective. We don't just help you find the best trauma insurance; we support you for the entire journey. When it’s time to claim, we manage the whole process from start to finish.

Our process for handling claims includes:

- First Contact & Paperwork: We notify the insurer and work with your doctors to gather all necessary medical reports and forms.

- Submission & Management: We submit the complete claim and act as the single point of contact, so you don't have to deal with insurer calls or emails.

- Advocacy & Follow-Up: We constantly monitor the claim's progress, answer assessor questions, and push for a fast resolution.

- Securing Your Payout: Our deep understanding of policy definitions means we can anticipate potential roadblocks and frame your claim in the strongest possible light.

This hands-on support lifts a massive weight off your shoulders, freeing you to focus on your health and family. It’s the ultimate peace of mind. If you’d like to see how we can provide this security for you, book a complimentary call with us.

Choosing the right trauma insurance is a significant decision. As we've covered, it involves digging into complex policy details, weighing costs, and understanding the fine print. It's a lot to take on, but you don't have to do it alone.

At Wealth Collective, our entire process is designed to make this clear and straightforward, so you can feel confident you have the right protection in place.

It all starts with a complimentary 10-minute chat to understand your situation. From there, our award-winning advisers—with over 50 years of combined experience—do the heavy lifting. We analyse the options and come back to you with a tailored recommendation from one of Australia's top insurers that genuinely fits your life.

The biggest mistake is letting complexity lead to inaction. That first conversation is often the most important step you can take to protect your family's future and everything you're working so hard for.

Our Protection Plus, Guided Growth, and Retirement Roadmap services are designed to turn a complicated financial puzzle into a series of clear, confident decisions. Let us handle the details so you can get on with living your life.

Your financial security is our priority, and it all begins with one simple, risk-free conversation.

Ready to take the next step? Book your complimentary introductory call with a Wealth Collective adviser today and get the peace of mind you deserve.

Got Questions About Trauma Insurance? We've Got Answers

It’s completely normal to have questions when you’re looking into something as important as trauma insurance. Let's tackle a few of the most common ones we hear from our clients.

Is Trauma Insurance Tax Deductible in Australia?

This is a big one. For most people holding a policy in their own name, the premiums are not tax-deductible. The good news, however, is that the lump-sum payout you receive if you need to claim is generally tax-free. This means the full benefit amount goes directly to you, without the tax office taking a slice.

Things can get a little more complex if the policy is held inside superannuation, although this isn't a common way to structure trauma cover. Your personal situation really dictates the best approach, which is why getting tailored advice is so important. At Wealth Collective, we always look at the full picture, including any tax implications.

What's the Real Difference Between Trauma and TPD Insurance?

People often mix these two up, but they serve very different purposes. Think of them as two distinct parts of your financial safety net.

- Trauma Insurance: This pays out when you are first diagnosed with a specific serious medical condition, like cancer, a heart attack, or a stroke. The key here is the diagnosis – it's designed to give you immediate financial breathing room, regardless of whether you can eventually return to work.

- Total and Permanent Disablement (TPD) Insurance: This cover kicks in when an illness or injury leaves you permanently unable to work ever again. It's about your long-term capacity to earn an income, not the initial diagnosis.

They aren't an either/or choice; they work together. Having both gives you much broader protection against different life-changing health events.

Can I Still Get Cover If I Have a Pre-Existing Medical Condition?

Yes, you often can, but it's not always straightforward. Insurers will look closely at the specific condition, its severity, and how it's managed. They might offer you a standard policy, add an exclusion for that particular condition, or increase the premium (called a "loading") to reflect the higher risk.

Being completely upfront and honest in your application is critical. If you leave something out, the insurer could use that as a reason to deny a claim down the track, which would be a devastating outcome.

This is where a good adviser makes all the difference. The team at Wealth Collective has been through this process countless times. We know which insurers are more understanding of certain conditions and can guide you to the one most likely to offer fair terms.

Hopefully, that clears a few things up. But if you're still working through the details of finding the best trauma insurance in Australia, the Wealth Collective team is here to give you personalised answers.

Book your complimentary 10-minute introductory call today