Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

The phone has not stopped ringing. A family member wants to know when the house can be sold. The bank needs documents. Your solicitor has asked for probate papers. Someone mentions tax, and suddenly you are staring at a term that feels cold and technical in the middle of a very human loss. CGT on a deceased estate often lands like that.

Most executors do not start this role because they wanted a crash course in tax law. They step in because someone trusted them. That is what makes the role so heavy. You are trying to protect assets, keep the peace, follow the will, and make decisions that the deceased would have respected.

The good news is that cgt deceased estate rules are manageable once you know where the core decision points sit. The confusion usually comes from three questions:

- When does tax arise

- Who carries the tax responsibility

- Which choices change the eventual outcome for beneficiaries

This guide is written for the person sitting at the kitchen table with estate papers spread out in front of them, trying to work out what matters first and what can wait. It uses plain language, practical examples, and the kinds of issues that commonly derail otherwise well-run estates.

The Weight of Responsibility Navigating Finances After a Loss

Sarah had barely finished arranging the funeral when the paperwork started piling up. There was a will, thankfully. There was also a home, some shares, a bank account, and a stream of questions from relatives who assumed she knew what an executor was meant to do.

She did not.

What unsettled her most was not the legal paperwork. It was the fear of making a costly mistake. If she sold the wrong asset too soon, delayed the wrong task, or misunderstood a tax rule, that error would not just sit on paper. It could reduce what was eventually passed on to the family.

That is a common executor experience. Grief and administration arrive together. You are asked to be organised, neutral, careful, and decisive at a time when you may feel none of those things.

Why CGT causes so much confusion

Capital Gains Tax sounds like a single issue, but for a deceased estate it is really a chain of decisions. The tax result can change depending on:

- What the deceased owned

- When they acquired it

- Whether it was a home or an investment

- Whether the estate sells it or a beneficiary inherits first

- How well records and valuations are kept

For some families, the stress starts even earlier if the estate plan is unclear or disputed. If you are dealing with uncertainty around testamentary intentions, family rights, or estate administration, this practical article on what happens if you don't have a will can help frame the legal side of the problem.

The executor’s primary job

Your role is not to become a tax expert overnight. Your role is to make informed decisions, ask the right questions, and avoid preventable errors.

Practical mindset: Treat each asset as its own file. The house, the shares, and any investment property may each follow different CGT rules.

The most helpful way to approach cgt deceased estate matters is to slow the process down. Work out what asset you are dealing with, what history it has, and what options exist before anything is sold or transferred. That one habit protects more estates than people realise.

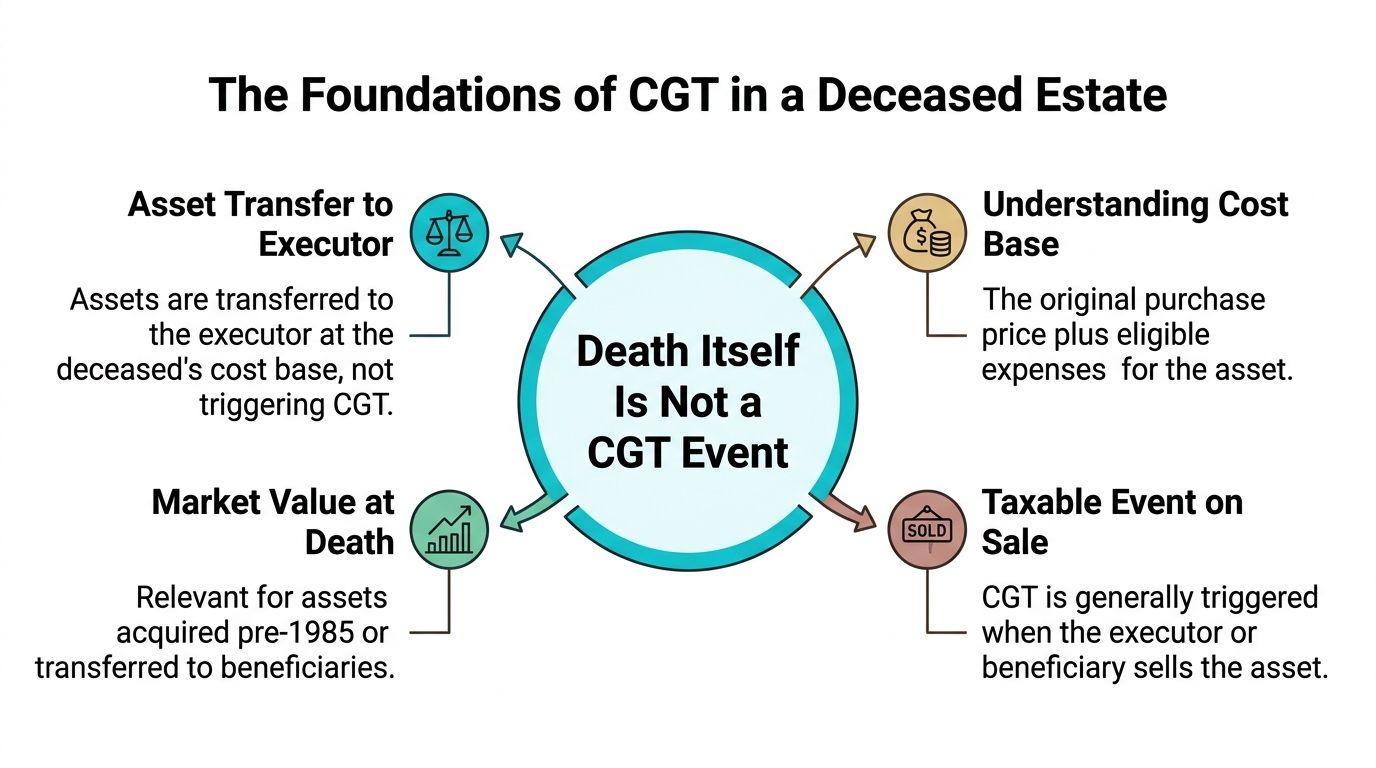

The Foundations of CGT in a Deceased Estate

Most executors expect death itself to create an immediate tax bill. In many estates, that is not what happens. The estate usually acts as a temporary holder of the asset’s tax history until a later decision, such as a transfer or sale, brings the CGT position into focus.

A practical way to view it is as a handover. The legal owner has changed, but the tax story attached to the asset may continue. The key tax question is not just who holds the asset, but what cost base travels with it.

How the tax history carries forward

An asset in a deceased estate often comes with a history: when it was bought, what it cost, and whether any later expenses changed that cost base. Death does not always erase that history. In many cases, it passes through the estate to the beneficiary, and the eventual tax result depends on what happened long before the executor was appointed.

That point matters because executors often focus on probate, transfers, and bank accounts first. Those tasks are important, but CGT risk usually sits in the background until the asset is sold. By then, missing records or a poor early decision can be expensive.

A good rule to remember is this: sale is often the moment when the CGT calculation becomes real.

Why the acquisition date matters so much

One of the first facts to confirm is when the deceased acquired the asset. That date affects which CGT rules apply and what starting point is used for any future gain or loss.

Australia’s CGT system draws a line at 20 September 1985. Assets acquired before that date are called pre-CGT assets. Assets acquired after that date are post-CGT assets.

That split can change the outcome in a major way.

Pre-CGT assets

A pre-CGT asset is often the easiest place for executors to make a wrong assumption. Families may know what the deceased paid decades ago and assume that old purchase price still drives the tax result. For these assets, the more important figure is usually the market value at the date of death.

You can treat that date-of-death value as a reset point for future CGT purposes. The growth in value during the deceased’s ownership before CGT began is generally not what the beneficiary is taxed on later. What matters is what happens from the inherited starting point onward.

That is why a proper valuation can protect the estate. Without it, you are trying to reconstruct a starting line after the race has already begun.

Post-CGT assets

Post-CGT assets work differently. Their tax history usually continues, including the existing cost base and relevant records that support it.

In practice, that means old paperwork still matters. Contract notes, purchase contracts, stamp duty records, legal fees, and evidence of capital improvements may all affect the final gain when the asset is sold by the estate or by a beneficiary later on.

If you want more background on how these decisions fit into a broader taxation and tax planning strategy, that guide can help place the estate issues in context.

A quick comparison

| Asset type | What matters most for future CGT |

|---|---|

| Pre-CGT asset | Market value at the date of death |

| Post-CGT asset | Existing cost base position carried forward |

Key takeaway: In a cgt deceased estate matter, the acquisition date is one of the first facts an executor should verify. If that starting point is wrong, every later calculation can be wrong too.

Where executors usually get tangled up

Confusion usually comes from treating three separate events as if they are one:

- Death

- Transfer to the estate or beneficiary

- Sale of the asset

Each event can have a different tax effect. Keeping them separate makes the rules much easier to apply and helps you make better decisions about whether to hold, transfer, or sell.

Protecting the Family Home from CGT

For many families, the home is the emotional centre of the estate and the largest practical concern. It is also where some of the most valuable CGT relief can apply.

The family home is not treated like an ordinary investment asset. Special rules can allow a sale to occur free from CGT, but only if the conditions are handled carefully.

When the main residence exemption can help

A deceased person’s home may qualify for exemption where it was their main residence throughout ownership and was not used for income production. That can be extremely valuable, particularly where the home forms a substantial part of the estate.

The verified guidance also notes that this exemption can apply to homes valued above a significant threshold, acknowledging that many ordinary family homes now sit at values that can make tax planning highly significant.

For executors, the key point is not the size of the home’s value. It is whether the facts support the exemption.

The conditions to check first

Ask these questions in order:

- Was this the deceased’s main home

- Was it used to earn income

- Will it be sold within the available exemption framework

- Has anyone changed the use of the property after death

A small detail can change the answer. A room rented out. A granny flat arrangement. A period where the property was held for income. These facts matter.

If the home is central to your estate decisions, this plain-English overview of the main residence exemption is worth reviewing alongside your legal and tax advice.

Where partial issues arise

The most common misunderstanding is assuming a property is fully exempt because “it was Mum’s house”. That may be true emotionally, but the tax position depends on use as well as ownership.

If the property was used to produce income, the exemption may be reduced or unavailable in full. That does not automatically mean a disaster. It does mean the executor should not rely on assumptions.

Tip: Before listing a property for sale, confirm whether the home was ever rented, partly rented, or used in a way that produced assessable income. That one question often changes the CGT result.

A practical home scenario

Take a straightforward case. The deceased lived in the home as their main residence and did not use it to produce income. The estate sells it in a way that satisfies the available exemption conditions. In that sort of scenario, the sale can be free from CGT.

Now compare that to a second case. The deceased had moved out and part of the home was producing income. The family still thinks of it as “the home”, but tax law may see a mixed-use asset. That can lead to only a partial exemption.

Why executors should decide early

The family home often becomes the asset everyone wants to discuss first. Some beneficiaries want to keep it. Others want a clean sale. Some want to rent it while the estate sorts itself out.

Each of those choices may affect tax. Delay is not always harmful, but unplanned delay often is. The tax question should sit beside the emotional and practical question, not behind it.

A careful executor does not ask only, “What do we want to do with the house?” They also ask, “What tax protection are we preserving or risking by doing it that way?”

Executor vs Beneficiary Who Should Sell the Assets

You have probate underway, the family is asking what happens next, and one question keeps coming up. Do you sell the asset inside the estate, or transfer it to the beneficiary first and let them sell later?

That choice is not just paperwork. It determines who reports the gain, whose tax position is affected, how much flexibility remains, and whether the estate keeps control of timing.

A practical way to view it is this. Selling from the estate usually favours administration and certainty. Transferring first usually favours personal choice and timing for the beneficiary. Neither path is automatically better. The right path depends on what the estate needs, what the beneficiaries want, and what tax position you are trying to protect.

The two pathways

There are two common routes.

The executor can sell the asset while it is still held by the estate. Or the executor can transfer the asset to the beneficiary, with the sale happening later in the beneficiary's own name.

That single fork in the road often shapes everything that follows. It affects control, record-keeping, family coordination, and the practical tax outcome.

CGT Comparison Sale by Estate vs. Sale by Beneficiary

| Factor | Sale by Estate (as legal personal representative) | Sale by Beneficiary (after inheriting) |

|—|—|

| Who controls the sale | The executor manages timing, sale process, and estate reporting | The beneficiary decides after the asset is transferred |

| Who reports the tax event | The estate or the deceased’s tax position may need to reflect the transaction, depending on timing and structure | The beneficiary is generally responsible after distribution |

| Access to records | The executor may still have easier access to contracts, valuations, and original estate records | The beneficiary may need to reconstruct records later if the file is incomplete |

| Family coordination | Useful where multiple beneficiaries want a clean division of cash rather than shared ownership | Better where one beneficiary wants to retain the asset or time the sale personally |

| Timing flexibility | Often tied to estate administration pressures, debts, and final distribution plans | Can give the beneficiary more control over when a sale occurs |

| CGT discount considerations | Discount eligibility still needs to be checked carefully based on the asset, dates, and who makes the sale | A later sale by the beneficiary may allow access to the CGT discount where the conditions are met, but this should be confirmed against the beneficiary’s specific facts |

When an estate sale often makes sense

An executor-led sale often works best where the estate needs cash, the will points toward a straightforward division, or the beneficiaries do not want the burden of shared ownership.

For example, suppose an estate holds an investment property and three beneficiaries are entitled equally. One wants to keep it, one wants cash immediately, and one lives overseas. In that situation, a sale by the executor may prevent months of disagreement and turn a difficult asset into something easier to divide fairly.

It can also reduce risk where records are incomplete. If the executor still has access to old purchase documents, improvement costs, and valuation evidence, finalising the sale before distribution may be cleaner than handing an unresolved tax history to a beneficiary.

When a beneficiary sale may be better

A transfer first can make more sense where one beneficiary wants to keep the asset, or where an immediate sale would force a decision before the family has worked through the options properly.

Take a different scenario. A daughter inherits her father's share portfolio and plans to keep it as a long-term investment. In that case, there may be no reason for the estate to sell for the sake of tidiness. Transferring the shares may better reflect the will, preserve flexibility, and let the beneficiary decide later whether sale timing suits her own tax position.

That does not mean delay is harmless. It means delay should serve a purpose.

The questions an executor should put on the table

Before you approve a sale or sign transfer documents, ask:

- Does the estate need funds now to pay debts, tax, or specific gifts?

- Will selling inside the estate avoid a dispute between beneficiaries?

- Is one beneficiary expecting to keep the asset rather than sell it?

- Are the cost base records, dates, and valuations strong enough for a later sale?

- Would waiting change access to a discount, exemption, or better sale conditions?

- Does the will support one path more clearly than the other?

These are not technical questions for the sake of it. They are decision points. Good executor work often means slowing the process just enough to choose the path that protects both family harmony and after-tax value.

Executor’s lens: A sensible choice is the one that fits the will, preserves the best available tax position, and avoids handing avoidable problems to the beneficiaries.

Executors often feel pressure to "just get it done." That instinct is understandable after a loss. But with CGT assets, speed alone is not the goal. The better goal is a clean decision, made with the records in hand and the likely tax result understood before the sale happens.

Valuation and Reporting Your Executor Duties

Once the theory is clear, the executor’s work becomes more procedural. That is where many estates either stay clean or become messy.

Two tasks sit at the centre of this stage. Get the right valuation evidence and report the right amounts in the right return.

Why valuation is not optional

A date-of-death valuation is not just a nice file note. It can determine the future tax position for beneficiaries and support the estate’s records if the figures are ever questioned.

This matters particularly where market value becomes the relevant cost base reference point. It also matters where family members disagree later about whether an asset was sold too cheaply or distributed unfairly.

A practical executor should gather valuation evidence early, while records, market context, and property details are easier to verify.

What to value

Not every estate is complex, but executors should consider valuation evidence for assets such as:

- Real property

- Listed shares or managed investments

- Business or private company interests

- Collectables or significant personal assets where relevant

The more unusual the asset, the less safe it is to rely on guesswork.

Reporting obligations in plain English

There can be more than one tax return involved in estate administration. That is another area where confusion is common.

At a high level, the executor needs to identify:

- What belongs in the deceased’s final tax affairs

- What belongs to the estate during administration

- What belongs to the beneficiary after distribution

The principle is straightforward even if the paperwork is not. Income and gains need to be matched to the right taxpayer at the right time.

A practical executor checklist

| Task | Why it matters |

|---|---|

| Identify each asset and acquisition history | Determines which CGT rules may apply |

| Collect title, contract, and cost records | Supports future cost base work |

| Obtain date-of-death valuations where needed | Anchors the estate’s tax position |

| Separate pre-death and post-death transactions | Avoids reporting the wrong amounts in the wrong return |

| Track distributions carefully | Clarifies when the beneficiary takes over responsibility |

Practical tip: Keep one estate register that records asset, owner, acquisition date, estimated tax treatment, valuation status, and intended next step. Executors who do this early make better decisions later.

Where executors expose themselves

The largest risks are usually avoidable:

- Selling before understanding the tax consequences

- Distributing assets before records are complete

- Failing to document market value properly

- Assuming the accountant or solicitor is handling an issue that nobody has taken ownership of

An executor does not need to do every technical task personally. They do need to make sure each task is being done by someone.

Worked Examples CGT in Real-World Scenarios

Rules make more sense when you can see them in motion. These scenarios are deliberately simple. The aim is to show how decision points work, not to replace specific advice.

Example one inherited shares sold by a beneficiary

An executor transfers a parcel of shares to an adult child beneficiary. The shares are not sold during the estate administration period.

The beneficiary later decides to sell. At that point, the beneficiary generally deals with the CGT consequence because the asset has already moved out of the estate.

The practical steps look like this:

- Confirm when the deceased acquired the shares

- Work out the relevant inherited cost base position

- Confirm the date the beneficiary sells

- Check whether the holding period supports the CGT discount outcome

Inherited property disposals by beneficiaries often qualify for the 50% CGT discount if held over 12 months post-inheritance, so timing can matter materially where the facts fit that framework. For shares and mixed investment portfolios, the same discipline applies. Do not sell first and reconstruct the file later.

Example two family home sold with exemption protection

A deceased parent leaves their home to two children. The home was their main residence and was not used to produce income.

The executor and beneficiaries agree that nobody will move in or rent it out. The property is prepared for sale and sold in a way that preserves the available main residence protection.

In that scenario, the result can be straightforward. The estate converts an emotional asset into cash without a CGT bill arising on the sale, assuming the exemption conditions are met.

The key features are not complex calculations. They are factual discipline:

- The property was the main residence

- It was not used for income production

- The sale approach did not compromise the exemption

This is why executors should resist “quick fixes” like renting the property for convenience before they understand the tax implications.

Example three investment property inherited and held

Now consider a different case. The deceased owned an investment property. The beneficiary inherits it and decides not to sell immediately.

That can be the right choice financially or emotionally, but the beneficiary is now stepping into an asset with an ongoing tax story. Future sale proceeds will need to be measured against the relevant cost base position, with supporting records carried forward.

The practical file for that beneficiary should include:

- Acquisition history

- Date-of-death valuation if relevant

- Evidence of improvements

- Sale costs when the property is eventually disposed of

- Records of ownership period after inheritance

What these examples are really showing

Each scenario turns on a different lever.

| Scenario | Main lever |

|---|---|

| Inherited shares | Timing and record accuracy |

| Family home | Preserving exemption conditions |

| Investment property | Cost base records and future sale planning |

Takeaway: In cgt deceased estate matters, the tax result is often shaped long before the sale contract is signed. It is shaped by what the executor documents, preserves, and chooses not to do.

That is why the best executor decisions often look quiet from the outside. They involve asking for valuations early, pausing before a rental arrangement, and documenting the asset trail properly. Those choices rarely feel dramatic. They are exactly what protect the estate.

When to Seek Expert Guidance for Your Estate

You might be days away from listing a property, one beneficiary wants cash quickly, another wants the asset transferred, and a missing box of old records suddenly matters far more than anyone expected. That is often the point when an executor realizes the hard part is not filling out forms. It is choosing the order of decisions before one choice closes off another.

Some estates are straightforward. Others only look that way until a home was partly rented, shares were bought across many years, or family members disagree about what is fair. In cgt deceased estate matters, the cost of a wrong step is often not obvious at the time. It shows up later in extra tax, lost exemptions, delay, or tension between beneficiaries.

The estates that usually benefit from advice are not only the very large ones. Advice often helps when the facts are mixed, the records are incomplete, or the family needs clear reasoning they can trust.

The warning signs that justify advice

Professional guidance is usually sensible when you are dealing with:

- A family home that may have been used to produce income

- An investment property with incomplete purchase or improvement records

- A share portfolio built up over a long period

- Business assets or private company shares

- Several beneficiaries who want different outcomes

- Disagreement about timing, value, or equal treatment

- Pressure on the executor to act quickly before the tax position is clear

None of these points means the estate is in trouble.

They do mean small decisions can have larger consequences.

Where do-it-yourself administration often goes wrong

Executors are often surrounded by partial advice. A solicitor may focus on probate and estate powers. An accountant may prepare returns based on the information provided. A selling agent may focus on the market and timing. Each person can do their own job well, yet the executor is still left with the bigger question. What should happen first, and who should do it?

Strategic advice adds value by looking at the whole decision chain. It helps the executor compare paths before acting. Sell from the estate or transfer first. Wait for a valuation or proceed with existing records. Preserve a concession or accept a different outcome for family reasons. Those are the moments that shape the result.

A useful way to view it is this. Estate tax decisions work like a row of gates. Once you walk through one, some of the others are no longer available.

What good advice should help you decide

You should expect practical guidance, not just a summary of rules.

That guidance should help answer questions like:

- Should the estate sell the asset, or should it pass to a beneficiary first?

- What records or valuations should be obtained before a property is listed?

- Could a planned step affect the main residence exemption?

- Are beneficiaries taking on future tax consequences they do not yet understand?

- What needs to be reported by the estate now, and what information must be handed to beneficiaries for later?

Good advice also helps the executor explain decisions. That matters when family members are grieving and reading the same situation through very different emotional lenses.

The broader family effect

A deceased estate is rarely just a tax file. It is often a turning point for the family’s finances. An inherited amount may change retirement timing, debt decisions, investment plans, or how support is given across generations.

A well-handled estate does more than reduce avoidable tax. It also preserves flexibility for the people left behind. That may mean keeping options open until records are confirmed, choosing a sale path that is fair between beneficiaries, or avoiding a rushed decision that cannot be undone.

If you are acting as executor and feel uncertain before a sale, transfer, or distribution, getting advice early can simplify the process and reduce pressure on the family.

If you want calm, practical guidance on estate-related decisions and the broader financial implications for you or your family, Wealth Collective offers a simple starting point. A free, no-obligation 10-minute call can help you clarify what type of advice you need, whether the issue sits within tax-aware financial planning, intergenerational wealth transfer, retirement strategy, or broader asset structuring. For families dealing with inherited assets, executor responsibilities, or retirement-stage planning, Wealth Collective’s Protection Plus, Guided Growth, and Retirement Roadmap services provide a clear framework for making confident decisions and honouring a loved one’s legacy with care.