Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

It often starts with a new job. You sign some forms, a new super account gets opened, and you don’t think much of it. Fast-forward a few years and a couple of job changes, and suddenly you’re juggling multiple super accounts. This isn’t just messy paperwork; it’s a quiet drain on your retirement savings.

Choosing to consolidate my super is about taking all those scattered accounts and rolling them into one, single fund. It’s the difference between having a handful of small, leaky buckets and one powerful, watertight pipeline building your wealth for the future.

The Hidden Costs of Multiple Super Accounts

It’s a story we hear time and again from new clients. They start a new role, get a new super account by default, and then move on. Before they know it, three or four accounts are silently chipping away at their nest egg.

This is what we call a 'silent leak'. Each account charges its own set of administration fees, investment fees, and insurance premiums. The Australian Taxation Office (ATO) confirms millions of Australians are in this boat, paying billions in duplicate costs that could be working for them instead.

The Real-World Impact of Inaction

So what does this actually look like in dollar terms? Let’s take a realistic example. Sarah, a 35-year-old professional, has accumulated three super accounts from different jobs over the last decade.

- Account 1: $45,000 balance with $550 in annual fees & insurance.

- Account 2: $25,000 balance with $380 in annual fees & insurance.

- Account 3: $10,000 balance with $250 in annual fees & insurance.

Right now, Sarah is paying a combined $1,180 every single year. By consolidating into a single, well-chosen fund, she could likely cut those costs to around $500 annually. That’s a saving of nearly $700 in the first year alone.

The decision to consolidate your super is one of the most powerful and straightforward actions you can take to boost your retirement savings. It stops the drain from duplicate fees and puts that money back to work for your future.

But the real magic isn’t just in the immediate savings. It’s what happens next.

The Compounding Effect on Your Future

That extra $700 isn't just saved; it's invested. It gets put to work and starts earning its own returns, year after year. This is the power of compounding.

Over the next 30 years until she retires, that seemingly small saving of $700 a year could grow into something substantial. Assuming an average annual return of 7%, consolidating her super could add more than $66,000 to Sarah's final retirement balance. That’s a huge difference, achieved simply by plugging the leaks.

This is a core principle we focus on at Wealth Collective: taking clear, practical steps to build a secure financial future. Getting your super sorted is often the first and most effective of those steps. It’s all about making the money you already have work much, much harder for you.

Taking control of your super isn’t just a tidy-up exercise; it’s a strategic financial move. It turns a fragmented collection of accounts into a focused, efficient engine for building your retirement wealth.

What to Check Before You Consolidate Your Super

It's tempting to jump right in and merge all your super accounts. After all, getting everything into one place and saving on fees sounds like a no-brainer. But rushing the process is a classic mistake. Think of it less like a quick tidy-up and more like a strategic move for your future wealth.

It’s a popular move, too. The Australian Taxation Office (ATO) has been tracking this for years, and as of June 2023, over 14 million of us now have our super sorted into a single account. You can see the full trend in the ATO's super accounts data summary.

The key is to do it methodically. This isn't just about picking the fund with the biggest balance—it's about making sure your chosen fund is the right one for the long haul.

Get Under the Hood on Fees

The most obvious win from consolidating your super is cutting out duplicate fees. But simply picking the fund with the lowest advertised fee can be misleading. You need to know exactly what you’re being charged across all your accounts.

- Administration Fees: These are the costs for simply having the account open. They might be a flat dollar amount ($50-$100 a year is common), a percentage of your balance, or a mix of both.

- Investment Fees: This is what you pay for the management of your money. It’s almost always a percentage of the amount you have invested.

- Indirect Costs: These are the trickier ones. They’re fees related to the management of underlying assets and are often baked into the unit price, so you don't see them directly. You'll need to dig into the Product Disclosure Statement (PDS) for this number.

The best way to compare is to work out the total annual fees in dollar terms for each account. You might find a fund with a low percentage fee is actually more expensive for your balance than a fund with a simple, flat fee.

Look Beyond Last Year's Returns

Everyone loves a winner, but a single year of great performance can easily hide a history of mediocrity. Don’t get swayed by a fund’s 12-month return figure. It tells you very little about their long-term skill.

What you really want to see is consistency. Look up the five-year and ten-year net returns for your specific investment options (e.g., 'Balanced' or 'Growth'). This longer timeframe smooths out the market's ups and downs and gives you a much clearer picture of how the fund has truly performed over time.

At Wealth Collective, this is a huge part of our analysis process. We don't just look at the performance numbers. We weigh them against the fees and the level of risk taken to get those returns. That's how we find funds that consistently add real value for our clients.

Remember, the goal is to find a fund that performs well after all fees and taxes are taken out. That’s the "net benefit" that will actually grow your retirement savings.

Don't Skip the Insurance Check

If you take only one thing away from this guide, let it be this: closing a super account automatically cancels any insurance cover attached to it. This is, without a doubt, the most critical—and most commonly overlooked—part of the consolidation process.

We saw this firsthand with a client recently. He was keen to merge three accounts and save on fees. He was all set to close his two smaller funds, but during our review process, we found something crucial. One of those accounts held a brilliant income protection policy with generous terms that simply aren't offered anymore.

If he had gone ahead and closed that account, he would have lost that valuable cover for good. Instead, we helped him arrange a transfer of that specific insurance policy over to his main fund before he closed the old one. He got to consolidate and save on fees, all while keeping his irreplaceable safety net.

Before you make any move, you must check the insurance on each of your accounts:

- What cover do you actually have? (Life, Total and Permanent Disablement (TPD), and Income Protection)

- How much are you covered for, and what are the premiums?

- What are the specific definitions and features of each policy? They can differ dramatically.

Making the wrong move here can be devastating. If you’re even slightly unsure how to compare insurance policies, it’s a clear sign you need to pause and get guidance. A no-obligation initial call with our team could be what saves your financial safety net from disappearing.

How to Consolidate Your Super Yourself

So, you’ve done the research and picked the super fund you want to stick with. Now for the satisfying part: bringing all your super together. Thankfully, the days of printing and mailing stacks of forms are mostly behind us.

There are two main ways you can tackle this yourself, and both are surprisingly straightforward. Which one you pick really just comes down to what feels easiest for you. One uses the government’s myGov portal, and the other goes directly through your chosen super fund. Let's walk through what each one looks like.

Your First Port of Call: myGov and the ATO

This is easily the most popular DIY method, and for good reason. The Australian Taxation Office (ATO) already has a record of all your super accounts, making it the perfect central hub to manage them from. It can even help you find lost super you’d forgotten about.

To get started, you’ll need a myGov account linked to the ATO. Once you’re logged into myGov and are in the ATO section, here's what to do:

- Head to the 'Super' tab in the main menu. This will open up your superannuation dashboard.

- From there, look for an option like 'Manage' or 'Manage your super'.

- Click through to the section for combining your super. You'll see a list of all accounts held in your name, including their latest balances. Simply choose which ones you want to roll over and which fund you want the money to land in.

The system guides you through a final confirmation, showing you the total amount being transferred. A few clicks, and the request is sent off.

The real power of using myGov is the complete overview it gives you. It pulls all the data together, showing you every account the ATO knows about. This is your best chance to make sure no money gets left behind.

The whole thing is usually done and dusted electronically within about three business days. It’s a simple and effective way to take charge.

The Alternative: Go Directly to Your Chosen Fund

Another great option is to let your chosen super fund do the heavy lifting for you. Since they want your business, most funds have made this process incredibly simple through their own websites or apps.

Typically, the steps look like this:

- Log in to your preferred fund’s member portal or mobile app. You'll often find a big button on the dashboard that says 'Consolidate' or 'Find my super'.

- You'll be asked for your consent and your Tax File Number (TFN). This gives the fund permission to use an ATO service to search for your other super accounts.

- A list of your other accounts will pop up. Just tick the boxes for the ones you want to close and transfer into your main account.

Many funds have a simple, visual interface that makes this process quick and easy.

If for some reason an online transfer fails (which is rare), the fund will usually provide a pre-filled form to get the job done manually. It might take a bit longer, but the result is the same. For a deeper dive, check out our guide on how to switch super funds.

Both DIY methods work perfectly well for most people. However, if you're dealing with something more complex—like a defined benefit fund or valuable insurance you don't want to lose—doing it yourself might not be the safest bet. That's when getting professional advice can save you a lot of headaches and money down the track.

The Hidden Advantage of Industry Mega-Funds

So, you’ve gone through the process of tracking down and combining your super accounts. It’s easy to think the job is done, but tidying up is really only half the battle. The other, more critical part is making sure all that money is now sitting in the right fund to actually grow.

The Australian superannuation scene has changed dramatically. We’ve seen a huge wave of mergers, creating what are now known as ‘mega-funds’. These are genuine financial powerhouses, and their sheer size gives them serious advantages that smaller funds just can't compete with.

This isn't just a minor trend; it's a fundamental shift. The largest funds—those with over $50 billion under management—now hold 80% of all super assets. That’s a massive leap from just 63% five years ago. You can dig into the specifics of how this trend impacts the super industry in the full report.

The Power of Scale in Your Super Fund

What does the size of a fund really mean for your retirement savings? It all comes down to economies of scale. Think of it like a massive wholesale club—the more people who join and pool their money, the better the deals are for everyone.

For you as a member, this translates into very real benefits:

- Lower Fees: With millions of members to spread costs across, mega-funds can charge much lower administration and investment fees. That means more of your money stays in your account, compounding for your future.

- Better Investment Opportunities: Their enormous size gives them access to investments that are off-limits to smaller funds. We’re talking about private equity, major infrastructure projects like airports and toll roads, and direct commercial property.

- Access to World-Class Talent: Big funds have the budget to attract and keep some of the sharpest investment minds from across the globe. That top-tier expertise is put to work managing your money.

Essentially, by rolling your super into one of these high-performing giants, you’re plugging your retirement savings into a far more powerful engine for growth.

Choosing the right fund is just as critical as the decision to consolidate. It’s about using these industry trends to your advantage, making sure your single account is set up for the strongest possible long-term performance.

Aligning With a High-Performing Fund

This shift towards bigger funds has a direct impact on your strategy. When you consolidate your super, you have the perfect chance to move your entire nest egg into a fund that can offer these advantages of scale. It’s an opportunity to benefit from lower fees while getting exposure to a wider range of assets that can drive growth.

This is exactly what we focus on at Wealth Collective. We don’t just help you tidy up your accounts; our process strategically positions your super to amplify its growth potential. The goal is to make sure your money isn't just in one place, but in the best possible place for your retirement journey.

If you want a deeper dive into what to look for, our guide on how to choose a super fund is the perfect place to start. Making this choice is a crucial step to ensure your decision to consolidate has the biggest possible impact on your final retirement balance.

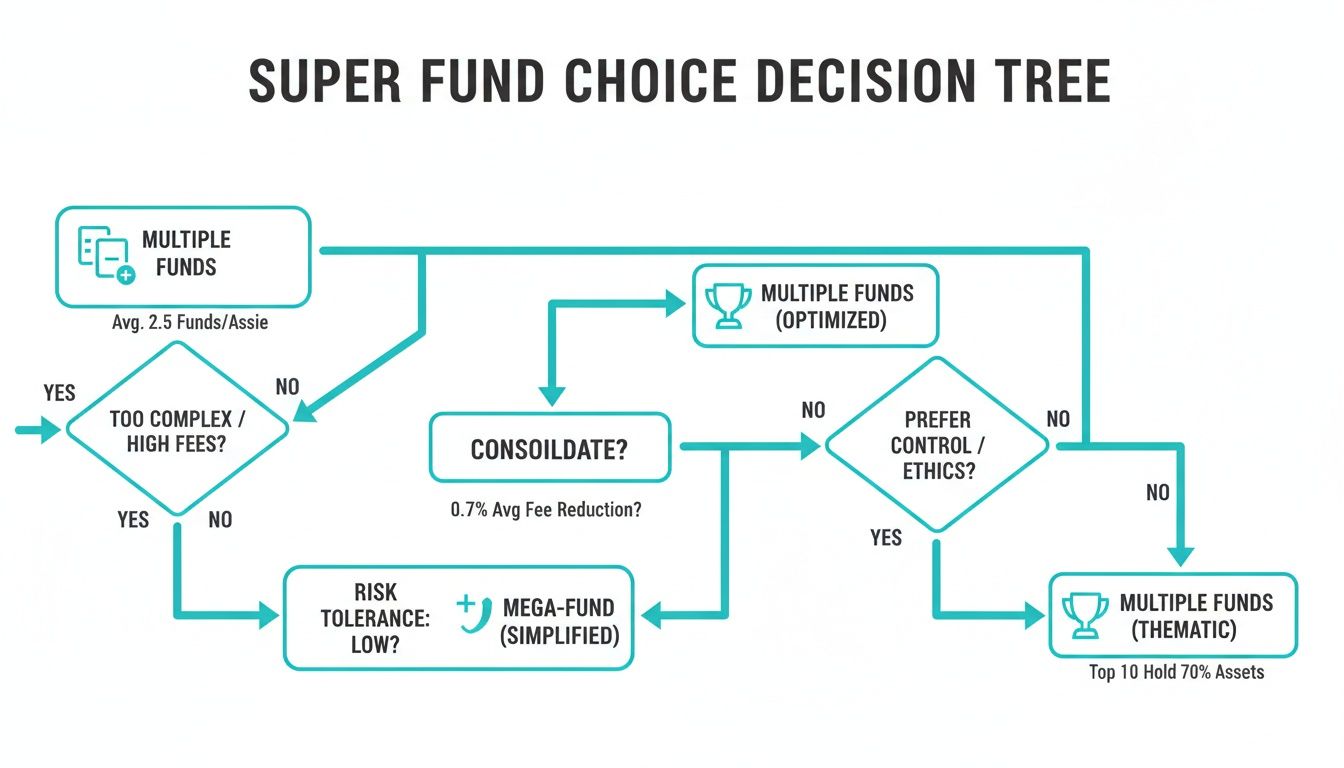

When a DIY Approach Is Not Enough

For straightforward situations, consolidating your super yourself is a great move. But there are times when it’s much more complicated than just clicking a few buttons online. Your financial life has its own unique layers, and trying to sort through them without a clear strategy can lead to costly and irreversible mistakes.

Knowing when you’ve reached the limit of a DIY approach is half the battle. This is the point where simple tidying up becomes serious financial planning—and getting it right can make a huge difference to your retirement.

This decision tree helps visualise the key questions to ask yourself, guiding you on the right path for your circumstances.

As you can see, the more complex your situation gets—whether it’s because of insurance, specific fund types, or your retirement timeline—the more sense it makes to get a professional involved.

Scenarios That Demand an Expert Eye

Some situations are clear red flags, signalling you should pause and get professional advice before you do anything else. If any of these sound like you, a simple online rollover could do more harm than good.

Here are the most common scenarios where our process makes a critical difference:

- You have a Defined Benefit Fund: These are often older, legacy-style funds. The retirement payout is based on a set formula, not just your account balance. Cashing out of one can mean giving up valuable, guaranteed benefits you simply can’t get anywhere else.

- You have valuable Insurance Cover: We’ve touched on this before, but it's critical: closing a super account cancels its insurance policy. A financial adviser can run a proper comparison to make sure you hold onto the best cover, or even arrange for a transfer before you close the old account.

- You run a Self-Managed Super Fund (SMSF): Rolling money out of an SMSF or winding one up is a complex legal and administrative task. You’ve got to navigate specific rules, potential tax issues, and an audit requirement—it all has to be handled perfectly.

- You have significant Capital Gains: If your super investments have grown significantly in value, consolidating can trigger a Capital Gains Tax (CGT) event. An adviser can walk you through the tax implications and map out a strategy to manage or minimise the hit.

For our clients, these are exactly the kinds of complex situations where our 'Retirement Roadmap' service shines. We dig into every detail to make sure any move you make is genuinely going to put you in a better position.

The goal isn’t just to have fewer accounts. It’s to build a stronger, more efficient wealth-creation engine that is perfectly aligned with your specific life stage and retirement goals.

The Value of a Tailored Strategy: A Case Study

Think about a recent client of ours, a 62-year-old small business owner who wanted to retire in three years. He had four separate super accounts and was keen to consolidate, but his situation was tricky—he had a defined benefit account and was unsure about the best way to use his contribution caps before he stopped working.

A simple rollover would have been a disaster. Instead, through our 'Retirement Roadmap' service, we developed a detailed strategy. We advised him to keep the defined benefit fund because of its guaranteed pension outcome, and then we consolidated his other three accounts into a single, high-performing fund.

More importantly, we created a contribution strategy to maximise his final balance before he converted it into a tax-effective pension stream. That tailored plan is projected to add well over six figures to his retirement nest egg compared to what a simple DIY consolidation would have achieved.

This is the real value of expert financial advice. Making sure all your financial pieces work together is the key to a successful outcome. To find out more about selecting the right professional for your needs, you can explore our detailed guide on how to choose a financial advisor.

Turning Knowledge Into A Plan For Your Future

Working through this guide and getting your super organised is a massive step in the right direction. It's far more than just tidying up your finances; it’s a strategic decision that lays the groundwork for a stronger financial future.

But a guide can only take you so far. The real magic happens when you apply these principles to your own life. Your career path, your family situation, and your personal goals for retirement are unique, and your super strategy should be too. This is where getting the right advice can make a world of difference.

We don't just help you consolidate your accounts; we partner with you to build a comprehensive Retirement Roadmap. This process ensures your super, investments, and insurance are all working together in perfect alignment with your most important long-term goals.

Ready to Take the Next Step?

You now have a solid understanding of the "what" and "how" of super consolidation. The next move is to create a plan that's built specifically for you, turning this general knowledge into real-world action. This is how you shift from simply managing your money to actively growing your wealth for the long haul.

If you’re ready to see what a clear, personalised plan could do for your financial confidence, the next step is a simple chat.

Booking an introductory call with our team is a great, no-obligation way to get clarity. It's the first step toward building a clear path to help you build, protect, and ultimately enjoy the wealth you’re working so hard for.

Common Questions About Super Consolidation

Even with a solid plan, a few questions always pop up just before you pull the trigger on consolidating your super. It’s a big move, so getting clear, straight answers is the best way to feel confident about your decision. Let’s walk through some of the most common queries we hear.

Will Consolidating My Super Affect My Insurance?

Yes, and this is probably the single most important thing to get right. When you close a super account, any insurance attached to it—like Life, Total and Permanent Disablement (TPD), or Income Protection—is cancelled. Instantly.

You could accidentally leave yourself or your family without a crucial safety net. I've seen it happen, and it's a devastatingly simple mistake to make.

Before you touch anything, you need to do a full side-by-side comparison. Look at the level of cover, the policy definitions, and what you’re paying in premiums for each policy. Your goal is to make sure your chosen "keeper" fund has the best insurance for your needs, or that you can transfer your preferred cover before closing any other accounts. This is one area where professional advice can save you a world of hurt.

How Long Does Super Consolidation Take?

The timeline really depends on which path you take and the types of funds you’re dealing with.

- Using myGov and the ATO: This is usually the quickest way for standard, APRA-regulated funds. The whole thing is electronic, so it’s often done and dusted within three business days.

- Going directly through your chosen fund: This is also a straightforward option, but it can take a little longer. Expect it to take anywhere from one to two weeks.

- Dealing with complex funds: If you're moving money out of a defined benefit scheme or a Self-Managed Super Fund (SMSF), you need to be patient. These are far more hands-on and can easily take several weeks, or even a couple of months, to finalise properly.

Are There Costs or Taxes When I Consolidate My Super?

For the vast majority of people rolling their money between standard super funds, the process is completely tax-free. It’s considered a "rollover," not a withdrawal, so you won’t be hit with a tax bill for the transfer itself.

Thankfully, exit fees have now been banned on most super products, so you shouldn't be charged for closing an old account. The main thing to be aware of is that the fund manager might have to sell assets to process your transfer, which could trigger a capital gains tax event inside the fund. This is handled internally, but if you have a complex situation like an SMSF, getting advice first is essential to avoid any nasty surprises.

While most consolidations are simple rollovers, things get tricky with structures like SMSFs or defined benefit funds. They have their own set of rules, and overlooking them can lead to unexpected tax bills or the loss of valuable benefits. It’s crucial to know exactly what you’re dealing with.

How Do I Find All My Lost Super Accounts?

The easiest way to hunt down every dollar is through your myGov account. Once you’ve linked it to the Australian Taxation Office (ATO), just navigate to the 'Super' section.

It’s all laid out for you. The dashboard shows every super account in your name, including any "lost" super that the ATO is holding for you. This gives you a complete picture of your retirement savings and is the perfect starting point when you're ready to consolidate my super. As part of our initial review process, the Wealth Collective team can also guide you through this to make sure no stone is left unturned.

At Wealth Collective, we help you turn these questions into a clear, actionable plan. If you’re ready to stop thinking about your super and start building a real strategy for your future, let’s talk. Book a complimentary chat with our team at https://wealthcollective.co and we’ll get started.