Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

While salary sacrifice gets a lot of airtime as a clever way to build your super and cut your tax bill, it’s not without its traps. The biggest, most immediate downsides are a drop in your take-home pay, which can really squeeze your day-to-day budget, and a lower on-paper salary that can seriously dent your borrowing power when you apply for a loan.

Is Salary Sacrifice Always a Smart Financial Move?

Salary sacrifice can be an incredibly effective tool for building wealth, but let’s be clear: it is definitely not a one-size-fits-all solution. For many Australians, especially those with big life goals just around the corner, the potential pitfalls can easily outweigh the tax perks.

At its core, the strategy means you agree to give up some of your pre-tax salary, which your employer then tips directly into your super fund. The tax savings look great on paper, but the real-world impact on your finances can be far more complicated and, in some cases, surprisingly costly.

Who Should Be Cautious

Before you jump into a salary sacrifice arrangement, you need to think carefully about where you are in life. The rigid nature of these agreements can become a real headache if your personal or financial situation changes.

Take a moment to consider if you fit into one of these groups:

- Young professionals saving for a home: That lower salary on your payslip directly affects how much a bank is willing to lend you. This could be the difference that delays you getting a foot on the property ladder.

- Families managing debt or a tight budget: The immediate hit to your take-home pay can make it much tougher to juggle monthly bills, chip away at a mortgage, or save for something important like a family holiday.

- Anyone with a fluctuating or uncertain income: Locking yourself into a fixed contribution can become a serious financial strain if your earnings suddenly drop.

The Hidden Complexities You Need to Know

Beyond the obvious impact on your cash flow, there are technical rules that can easily catch you out. For instance, accidentally breaching the superannuation contribution caps can trigger extra tax penalties that eat away at the very savings you were trying to create. Getting your head around these rules is non-negotiable before you commit. To get back to basics, you can read our guide explaining what salary sacrifice for super is.

Navigating these financial decisions requires a clear understanding of not just the benefits, but the potential pitfalls. A strategy that works for a pre-retiree might be entirely unsuitable for someone in their early 30s focused on buying their first home.

The conversation should never just be about saving tax. It has to be about building wealth in a way that actually fits with your entire life plan. At Wealth Collective, our process is designed to see that bigger picture, helping you make smart choices that support both your immediate needs and your long-term ambitions.

How Salary Sacrifice Squeezes Your Take-Home Pay and Lifestyle

The first thing you'll feel when you start salary sacrificing is the hit to your bank account every payday. It’s the most immediate and obvious trade-off. While you’re doing a great thing for your future self by boosting your super, your present self has to get by on less.

This isn't just about having a little less spending money. A drop in take-home pay can put real pressure on your household budget, especially if you're navigating the high cost of living. It could mean pulling back on the things that make life enjoyable, like family dinners out or weekend getaways. For some, it might even mean pausing bigger goals, like saving for a home deposit or that long-overdue holiday.

This creates a classic "asset rich, cash poor" scenario. Your retirement nest egg might be growing nicely, but your day-to-day financial flexibility feels tight, leaving you with a frustrating gap between what you earn on paper and how you can actually live.

The Real-World Budget Squeeze

It’s one thing to see the numbers on a spreadsheet; it’s another to feel a few hundred dollars missing from your paycheque. That money is often the buffer that covers unexpected car repairs, school excursions, or just allows for a bit of spontaneity.

When that buffer gets funnelled into your super fund, your budget has to be far more rigid. For families already juggling a mortgage, childcare, and climbing grocery bills, this can add a layer of financial stress. The reward of a comfortable retirement tomorrow can sometimes come at the cost of a more stressful present.

Finding the right balance is everything. This is precisely why our financial advice process at Wealth Collective involves modelling these scenarios. We look at your entire financial world to see if the tax perks of sacrificing your salary are genuinely worth the squeeze on your lifestyle right now.

The Hidden Impact on Your Borrowing Power

This is the one that catches so many people by surprise. Beyond the daily budget, salary sacrificing can seriously curb your ability to get a loan. When you go to a bank for a mortgage or an investment loan, they don't care about your total package figure. They base their assessment on your reduced, post-sacrifice income.

This simple fact can have a huge, and often disappointing, outcome. A lower assessable income means a lower borrowing capacity—sometimes by tens or even hundreds of thousands of dollars. If your goal is to build wealth through property, this can be a massive roadblock that delays or even completely scuttles your plans.

A reduced take-home pay doesn't just pinch your day-to-day spending. It can shrink the size of the home or investment loan a bank is willing to give you, as lenders focus on your post-sacrifice income. This can seriously limit your ability to build wealth outside of super.

Let's walk through a real-world example. Say you're on a $90,000 package and you’re keen to max out your super. You decide to salary sacrifice $10,000, which lowers your taxable income to $80,000 and saves you a tidy $3,800 in tax. But with the rising cost of living, that reduced cash flow hits hard.

Even more critically, when you approach a bank for a home loan, they’ll base their calculations on that $80,000 figure, not your full $90,000 salary. Based on standard lending criteria, this could easily knock $50,000 or more off your approved loan amount. That's a huge hurdle if you're trying to get into the property market. You can find out more about how lenders view salary sacrifice in Australia.

Here we have a direct conflict: the very strategy meant to secure your long-term retirement could actively undermine your medium-term goal of buying property. Our process at Wealth Collective is designed to uncover these potential clashes, ensuring your plan for super doesn't accidentally sabotage your other financial ambitions.

Super Caps and Surprise Taxes: The Hidden Traps

While the hit to your weekly paycheque is obvious, some of the biggest downsides of salary sacrifice are buried in the complex rules of superannuation. This is where a seemingly smart tax move can backfire, costing you more than you save if you’re not careful. The devil is truly in the detail.

The Australian Taxation Office (ATO) has firm rules about how much you can put into super each year on favourable tax terms. If you go over these limits—even by accident—you can face some hefty penalties. This is how a simple salary sacrifice plan can get complicated fast, especially for higher-income earners.

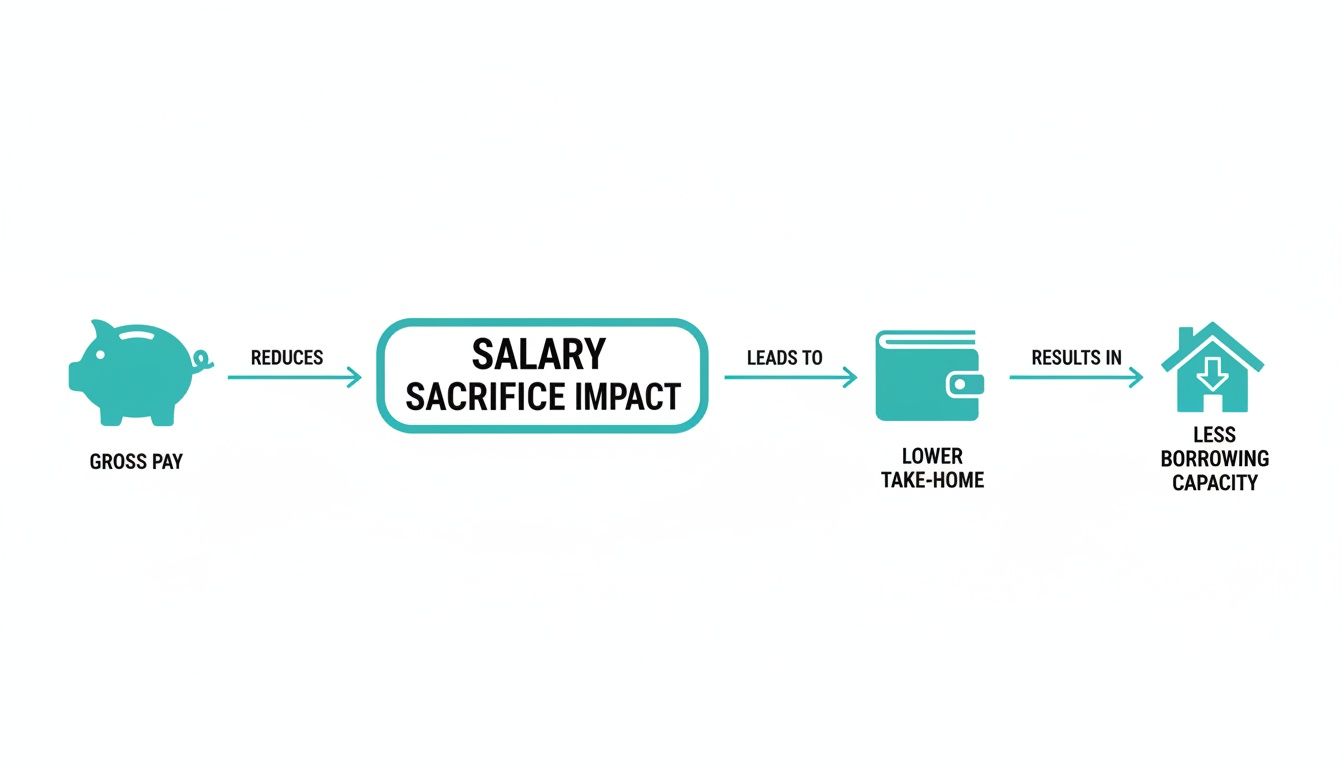

Think of it this way: every dollar you salary sacrifice is a dollar less in your pocket today and potentially a dollar less a bank will lend you tomorrow.

This simple flow shows the direct trade-off you’re making. Boosting your super means reducing your take-home pay, which can directly impact your borrowing power for big life goals like a home loan.

The Concessional Contributions Cap Trap

The most common tripwire is the annual concessional contributions cap. This is the yearly limit on all pre-tax money going into your super fund. For the 2024-25 financial year, that limit is $30,000.

What a lot of people don't realise is that this cap lumps together several types of contributions:

- Your employer's compulsory Superannuation Guarantee (SG) payments.

- Your own salary sacrifice amounts.

- Any personal contributions you make and then claim a tax deduction for.

It's surprisingly easy to overdo it. Say you earn $150,000 a year. Your employer is already putting in $18,000 (12% SG). If you then decide to sacrifice an extra $15,000, your total concessional contributions hit $33,000. You’ve just gone $3,000 over the cap.

The penalty isn't small. The excess amount gets added back to your taxable income and is taxed at your marginal rate, plus an extra charge. This pretty much wipes out the tax benefit you were aiming for and stings you with a penalty on top. While you might be able to use the carry-forward rule, knowing how and when to apply it is key. You can find out more about how to use carry-forward concessional contributions in our detailed guide.

The Division 293 Tax Sting for High Earners

If you're on a higher income, there’s another layer of tax to watch out for: Division 293 tax. This is an extra 15% tax on super contributions for anyone whose "adjusted taxable income" is over $250,000 a year.

In simple terms, it means your super contributions get taxed at 30% instead of the usual 15%. This tax is designed to dial back the super tax breaks for high-income earners.

Here’s where salary sacrifice can catch you out. Imagine your income is $240,000. You decide to salary sacrifice $15,000 to give your super a boost. While this lowers your regular taxable income, the ATO looks at an "adjusted" figure for the Division 293 calculation—and that figure includes your salary sacrifice amount.

Here's how it plays out: An executive on $240,000 sacrifices $15,000. Their income for Division 293 purposes is now $255,000 ($240,000 salary + $15,000 sacrifice). They've just tipped over the $250,000 threshold, and now their contributions are hit with the extra 15% tax, seriously diluting the tax-saving benefit they were after.

This is a classic case of a strategy designed to save tax accidentally triggering a different, unexpected tax. It’s exactly why getting professional advice is so critical. As part of the Wealth Collective process, we run these numbers to make sure your super strategy is actually saving you money and won't lead to any nasty surprises at tax time.

The Hidden Costs and Inflexibility of Your Sacrificed Funds

So, you've wrapped your head around the tax side of things. But beyond the contribution caps and potential tax bills, salary sacrifice comes with a few other significant trade-offs—the kind that can quietly trip you up years down the track.

These hidden costs aren't about tax brackets; they're about flexibility, control, and ensuring you don't inadvertently reduce other crucial benefits from your employer.

The Problem of Preservation

The biggest catch with funnelling money into your superannuation is preservation. Once a dollar is sacrificed into your super fund, it's effectively locked away.

You can’t just pull it out when you need it. That money is inaccessible until you meet a specific 'condition of release', which for most of us means hitting our preservation age (currently 60). This is one of the most serious disadvantages of salary sacrifice.

This inflexibility can be a major problem. Life has a habit of throwing curveballs—a medical emergency, a fantastic business opportunity, or the need to help out family. If too much of your wealth is tied up in super, you might find yourself cash-poor when you need it most.

Think of your super fund like a high-security vault with a time-locked door. Salary sacrifice is a fantastic, tax-friendly way to fill that vault, but the door is set to open at retirement. It's brilliant for your future self but offers zero help for the financial goals or emergencies that pop up before then.

This creates a real conflict for people trying to build wealth. You might be juggling saving for a house deposit, wanting to build an investment portfolio outside of super, and planning for retirement. Over-committing to salary sacrifice can starve your more immediate, accessible savings goals.

The core issue with preservation is the loss of financial control. While the goal is to secure your future, an overly aggressive salary sacrifice strategy can leave you vulnerable and unable to respond to life's immediate financial challenges and opportunities.

It really is a balancing act. A smart financial plan shouldn't force you to choose between today and tomorrow. A well-designed strategy, like the ones we build through the Wealth Collective process, makes sure your money is working for all your goals—short, medium, and long-term—without leaving you financially stranded.

When Your Benefits Get Cut

Now for something a little more subtle: how your employer calculates other work-related benefits. This is a trap that many people fall into because it's often buried in the fine print of an employment contract.

Some companies may base certain entitlements on your reduced, post-sacrifice salary rather than your full package. This can have a compounding negative effect that quietly erodes your overall wealth over your career.

Here’s a look at how this can play out.

Potential Impacts of Before vs After Salary Sacrifice

This table illustrates the potential negative flow-on effects of reducing your gross salary through a sacrifice arrangement, highlighting areas that are often overlooked.

| Financial Component | Calculated on Full Salary (No Sacrifice) | Calculated on Reduced Salary (With Sacrifice) | Potential Negative Impact |

|---|---|---|---|

| SG Contributions | The compulsory 12% is based on your total package. | The 12% might be based only on your lower cash salary. | You receive less 'free money' from your employer. |

| Life Insurance | Cover is a multiple of your higher, pre-sacrifice salary. | Cover is a multiple of your lower, post-sacrifice salary. | Your family could receive a smaller insurance payout. |

| Redundancy Payout | The final payout is calculated using your full salary. | The payout is calculated using your reduced salary figure. | You get a smaller financial safety net if you lose your job. |

As you can see, the difference can be significant.

Over a 20 or 30-year career, these seemingly small reductions can add up to tens of thousands of dollars in lost benefits. It just goes to show how critical it is to read the fine print before you commit. Our role at Wealth Collective is to help you spot these hidden details, ensuring your financial strategy doesn’t contain any unwelcome surprises.

Exploring Smarter Alternatives to Build Your Wealth

So, if salary sacrifice comes with a few tripwires—from borrowing power hits to hidden tax traps—it's pretty clear a 'set and forget' approach isn't going to work for everyone. The good news? There are other, more flexible ways to build your super that won't tie your hands.

This is where knowing all your options really pays off. Instead of being locked into a fixed agreement with your employer, you can take the reins and make contributions that actually fit your life, your income, and what you’re trying to achieve. That kind of adaptability is what a smart financial plan is all about.

For many people, especially those with fluctuating incomes or anyone who wants to keep a tight grip on their cashflow, these alternatives can deliver the same great tax benefits with far less risk.

The Power of Personal Concessional Contributions

One of the best alternatives out there is making personal concessional contributions. On paper, they do the exact same job as salary sacrifice: you get pre-tax money into your super fund, which in turn lowers your taxable income. The real magic, however, lies in one crucial word: flexibility.

Instead of a rigid, automated deduction from every paycheque, you decide when and how much to contribute. You're in complete control.

Here’s why that’s such a game-changer:

- You control the timing: You can wait until the end of the financial year and make a lump-sum contribution when you have a full picture of your finances.

- You adjust to reality: This gives you the chance to look at your actual earnings, any bonuses, and your spending for the year before you commit a single dollar.

- You avoid over-committing: Had an unexpectedly tough year? You’re not stuck making a contribution you can no longer afford.

This strategy is a perfect fit for business owners, freelancers, or anyone whose income isn't the same predictable figure month after month. You still get the tax deduction, but without the rigid commitment. You can explore more strategies in our guide on how to reduce taxable income in Australia.

Options Beyond the Concessional Cap

What happens if you've already maxed out your annual concessional contributions cap of $30,000? That doesn't mean you have to hit the brakes on building your super. Another fantastic tool is making non-concessional (after-tax) contributions.

Now, you don't get an upfront tax deduction with these, but the long-term benefit is huge. Once that money is inside your super fund, any earnings it generates from investments are taxed at a maximum of just 15%. For most people, that’s a much better rate than you’d get on investments held in your own name.

A truly effective financial plan doesn't just lean on one strategy. It's about looking at every available option—from personal super contributions to after-tax top-ups—to build a balanced approach that fits your unique life and goals.

This really gets to the heart of smart financial planning. There’s rarely a single 'best' answer; there's only the best answer for you. The downsides of salary sacrifice just prove it’s one tool of many. A holistic plan, like the ones we design through the Wealth Collective process, means we look at your entire financial world to pick the right mix of strategies.

Whether it’s using the flexibility of personal contributions or strategically topping up with after-tax money, our goal is to build a plan that works for you. We make sure your efforts to build wealth are efficient, adaptable, and perfectly designed to help you live your wildly successful financial life.

Alright, let's be honest. After all that talk about the good and the bad, it's pretty clear that salary sacrifice isn't a one-size-fits-all magic bullet. It can be fantastic for building wealth, but only if it genuinely fits your life right now.

So, how do you figure out if the trade-offs are worth it for you? It's time for a quick reality check. Run through these questions and answer them honestly – it’ll give you a gut feel for whether you should hit go, press pause, or look at other ways to get ahead.

Your Financial Self-Assessment

Before you lock anything in, take a moment to think through the real-world impact.

- Cash Flow Check: How would a smaller pay packet actually feel each month? Can you still comfortably cover the mortgage, pay the bills, and live your life without feeling the pinch?

- Borrowing Power: Are you planning to apply for a big loan anytime soon? If a new home or an investment property is on the cards in the next few years, you need to know if a lower on-paper income will reduce how much the bank is willing to lend you.

- Income Stability: Is your income rock-solid and predictable? If you work on commission, have a side hustle, or your hours fluctuate, locking in a fixed contribution could become a serious financial headache down the track.

- Emergency Buffer: Do you have enough cash savings you can get to in a hurry? Tying up more money in super is great for the long term, but you need a separate stash for those curveballs life inevitably throws your way.

If you find yourself hesitating on any of these, it doesn't mean salary sacrifice is off the table. It's simply a red flag. It tells you there's a potential clash between what you need today and what you're planning for tomorrow, and that needs to be handled carefully.

These are the exact kinds of conversations we have every day here at Wealth Collective. Our job as financial advisers is to take these messy, real-life questions and help you build a clear, simple plan. We don't just look at your super in a vacuum; we look at your entire financial world to make sure every piece is working together.

Trying to navigate the downsides of salary sacrifice on your own is tough. It’s easy to miss something and create an unintended problem for yourself.

If you’re ready to stop guessing and get a concrete strategy that’s actually built for your life, the next step is easy.

Book your complimentary 10-minute introductory call with a Wealth Collective adviser today.

Your Questions Answered

Getting your head around salary sacrifice can feel tricky. Let's tackle some of the most common questions we get from clients, so you can see the full picture before diving in.

Can I Stop or Change My Salary Sacrifice Arrangement?

You can, but this is often where the wheels fall off. While you’re not locked in forever, many employers only let you make changes once or twice a year, or maybe only at the end of the financial year.

This lack of flexibility can be a real trap. If your circumstances change suddenly—say, you have unexpected expenses or your income drops—you could be stuck with an arrangement that no longer works for your budget.

How Does Salary Sacrifice Affect My HECS HELP Debt?

This is a big one and it catches a lot of people out. The ATO calculates your compulsory HECS/HELP repayments based on your 'repayment income'. Critically, this figure includes your gross salary plus any amount you've salary sacrificed into super.

So, while your take-home pay goes down, your HECS/HELP repayment amount does not. That mandatory repayment can suddenly feel a lot bigger when it's coming out of a smaller pay packet.

Is It Better to Make Personal Contributions or Salary Sacrifice?

Honestly, it depends entirely on your personal situation. Both have their place.

Salary sacrifice is the classic ‘set and forget’ option, handled automatically by your payroll. But personal contributions give you total control—you decide how much and when, which is a huge advantage if your income isn't always predictable.

The best move for you comes down to the nitty-gritty of your finances. A financial adviser can map out your income, goals, and cash flow to help you decide which strategy truly fits your life.

Navigating the downsides of salary sacrifice is all about having a clear plan that’s built for you. The team at Wealth Collective is here to translate the complex rules into simple, practical advice. To get a strategy that protects you now and sets you up for the future, book your complimentary 10-minute introductory call today at https://wealthcollective.co.