Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Selling the family home can feel oddly conflicting.

There is relief. Less maintenance, fewer stairs, maybe a move from a big Perth block to something easier to manage in Dunsborough, South Perth, Subiaco, or closer to the grandkids. But once the contract settles, a harder question appears very quickly. What should you do with the sale proceeds now?

For many Western Australians, that money is not just spare cash. It is decades of equity, memories, and future lifestyle choices rolled into one. Used well, it can strengthen retirement income, improve flexibility, and make the next phase of life more comfortable. Used poorly, it can create avoidable tax issues, super mistakes, or Centrelink surprises.

One of the most useful options available is the downsizer contribution to super. It was designed for exactly this stage of life, but it is also one of the most misunderstood strategies in retirement planning.

Your Home Sold What Happens to the Money Now

Take a common WA scenario.

A couple in their late fifties or sixties sell the family home after the kids have long since moved out. The house has become too much work. The garden needs constant attention, the spare rooms sit empty, and the idea of a simpler place near the coast or closer to medical services suddenly feels less like a compromise and more like a smart next step.

They settle the sale, the funds hit the bank account, and then the uncertainty begins. Do they keep the money in cash for a while? Put some into investments? Pay down debt? Help adult children? Or move a chunk into super?

The downsizer rules were introduced on 1 July 2018, and the strategy has become far more widely used since then. Participation grew from 6,500 individuals in its first year to over 15,800 in 2024-25, with $4.165 billion contributed, and more than 80,000 Australians had used the scheme cumulatively by 2025, according to the ATO’s downsizer super contributions data.

That tells you something important. This is no fringe idea. More Australians are using home equity to strengthen retirement savings inside super.

Why the moment after settlement matters

The sale of a main residence creates a rare planning window.

Your home has often been your largest asset, and for many people it has sat outside super for years while other contribution rules became tighter. The downsizer contribution to super gives eligible people a chance to move some of that value into a concessionally taxed environment, without getting blocked by the normal contribution rules that often frustrate pre-retirees.

It also sits alongside other issues that need attention, including the tax treatment of the home sale itself. If you want a practical overview of that side of the equation, this guide to the main residence exemption is a useful companion read.

A home sale is not just a property event. For many retirees, it is one of the biggest balance-sheet decisions they will ever make.

The opportunity and the catch

The opportunity is straightforward. You may be able to put a large amount into super in a tax-effective way.

The catch is that the rules are exact. Timing matters. The paperwork matters. Your broader retirement plan matters even more. A downsizer contribution can be a great move, but only when it fits the rest of your position.

Understanding the Downsizer Super Contribution

The easiest way to think about a downsizer contribution to super is this.

It is an express lane into super for eligible people aged 55 or older who sell their home. Instead of using the usual contribution pathways, which can be restricted by caps and balance tests, the downsizer rules let you contribute from the sale proceeds under a separate set of rules.

What makes it different

A downsizer contribution is not just another personal contribution.

If you qualify, you can contribute up to $300,000 each, or up to $600,000 for a couple, from the sale proceeds of an eligible principal place of residence. This contribution bypasses the usual non-concessional contribution limits and is available even to people who would otherwise be blocked by total super balance restrictions.

That is why it gets so much attention from pre-retirees who have built substantial equity in the family home but have less room to contribute through normal channels.

Why people use it

People generally do not use this strategy because it sounds clever. They use it because it solves a real problem.

They have sold a valuable home, they want their money working harder for retirement, and they know super can offer a better tax setting than holding large sums personally. The downsizer rules can help shift equity from an underused home into a structure built for retirement funding.

That appeal is showing up in fund-level data too. In 2025, HESTA reported record downsizer contributions of over $94 million from members, which was 45% growth over two years. In WA, contributions fell 25% from 2024 peaks, but still recorded the state’s second-highest contribution level since 2018, according to Financial Newswire’s report on HESTA downsizer contribution trends.

A simple Perth example

Say a couple sell a long-held Perth home and free up more capital than they need for the next property.

They may decide to keep part of the proceeds available for moving costs, furnishing the new home, and a cash buffer. Then they may use the downsizer rules to place some of the remaining amount into super, where it becomes part of their retirement pool.

That does not automatically make it the right move. But it shows why the strategy is so practical. It is tied to a real life event and a real source of capital.

Where people get confused

The most common confusion is assuming the downsizer contribution is just another non-concessional contribution with a different name.

It is not. It has its own eligibility rules, timing rules, and paperwork requirements. It also interacts differently with broader super limits.

The key attraction is not just the amount you can contribute. It is the fact that the rules create a separate pathway when the usual paths may already be closed.

That is why this strategy often becomes relevant just when people thought their contribution options had narrowed.

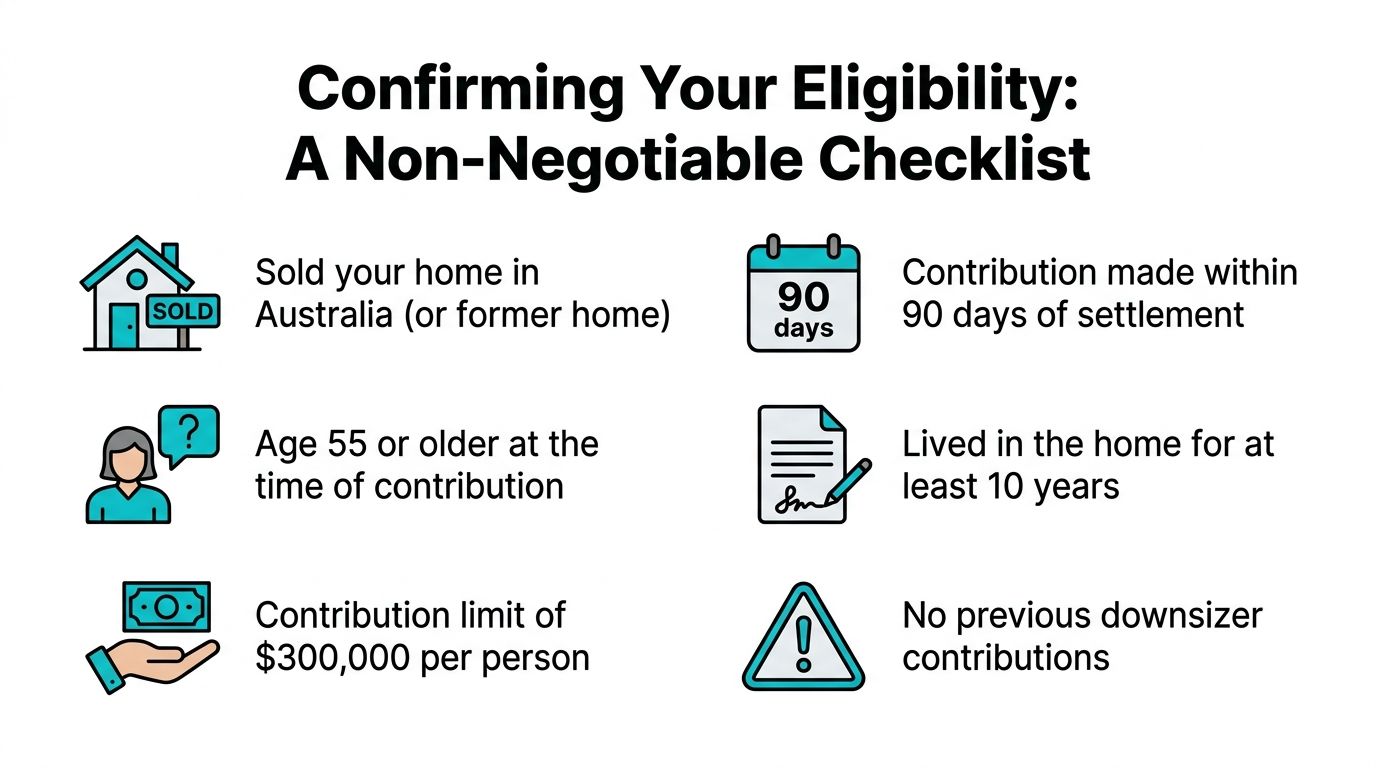

Confirming Your Eligibility A Non-Negotiable Checklist

The downsizer rules are generous, but they are not loose.

You need to satisfy a specific set of conditions. Missing one detail can change the whole outcome, so it helps to treat eligibility as a checklist rather than a rough estimate.

The core tests

Start with these points.

Age requirement

You must be 55 or older at the time you make the contribution.The property must be in Australia

The sale must relate to an Australian property.Ownership period

The home needs to have been owned for at least 10 years before the sale.Main residence status

The property must qualify for at least a partial main residence treatment under the tax rules.Timing of the contribution

The contribution must be made within the required timeframe after settlement.Correct paperwork

You must give your super fund the required downsizer form before or at the time of contribution.

What the 10-year rule usually means in plain English

This is one area that catches people out.

The rule is not about how long you have lived there in a casual sense. It is about the ownership period of the eligible property. If you moved house more recently, rebuilt, changed title arrangements, or have had a more complicated living setup, the practical answer may not be obvious without checking the details carefully.

For many WA households, especially those who have held a Perth family home for a long time, this rule is straightforward. For others, particularly people who split time between city and regional property, more care is needed.

Couples often misunderstand one point

A lot of people assume both spouses must have legal title to the home for both to use the strategy.

That is not always the case. The ownership and residence rules can still allow both members of a couple to make downsizer contributions where the broader conditions are met. But this is exactly the sort of detail that should be confirmed before money moves.

A practical self-check

If you are assessing your own position, ask yourself:

- Am I already 55 or older when the contribution will be made?

- Was the property my home for tax purposes?

- Has it been owned for at least 10 years?

- Will I be ready to contribute within the required post-settlement window?

- Have I used the downsizer rules before?

That final question matters because the downsizer contribution is intended as a one-time opportunity per person.

If any answer feels uncertain, stop and verify it before making the contribution. The rules are too valuable to rely on guesswork.

Where WA situations become less clear

Readers in Perth or Dunsborough often raise similar edge cases.

Maybe the home was held in one spouse’s name. Maybe you lived there for years but rented part of it at some stage. Maybe you are selling after a change in family circumstances. Maybe the sale happened while planning a move into a smaller coastal property.

Those facts do not automatically disqualify you. They mean eligibility should be confirmed carefully rather than assumed.

How Downsizer Funds Interact with Super Caps and Balances

Many people find this confusing, because two things can be true at the same time.

A downsizer contribution can bypass some of the normal super restrictions, but it can still affect other super limits later. If you miss that distinction, you can make a good strategy look simpler than it really is.

The first big advantage

The key benefit is that downsizer contributions bypass the non-concessional contribution caps and the Total Super Balance test.

That matters because many pre-retirees have enough in super that normal after-tax contributions are limited or blocked. The downsizer rules create a separate lane. According to Challenger’s guide on downsizing your home and upsizing your super, downsizer contributions bypass non-concessional caps and the Total Super Balance test, and for couples, both can contribute up to $300,000 each even if only one spouse owns the property.

If you want a refresher on how standard after-tax caps work, this explainer on what are non-concessional contributions gives useful context.

What this means in everyday terms

Think of your super rules as a series of gates.

Normal after-tax contributions often stop at the first gate because of annual caps or your existing total super balance. A downsizer contribution gets you through that first gate if you qualify.

But the money still joins the rest of your super once it is inside.

That means the contribution can still influence later calculations and later decisions.

The second big rule people overlook

A downsizer contribution may bypass the entry restrictions, but it does count toward the Transfer Balance Cap when moved into pension phase.

For 2024-25, that cap is $1.9 million. So if you are planning to start or add to an account-based pension, you need to know how much room you have under that cap.

People often say here, “I thought downsizer money was exempt.” It is exempt from some rules, not all rules.

A simple example

Suppose one member of a couple already has a large super balance and cannot make further normal after-tax contributions because of the usual balance restrictions.

The downsizer contribution may still be available on the sale of an eligible home. That is the good news.

The planning issue comes later. Once that extra amount is inside super, it becomes part of the broader super picture. If the person then wants to move more money into pension phase, the $1.9 million Transfer Balance Cap becomes highly relevant.

Why timing matters

The timing of the contribution can shape later flexibility.

In practice, that means you do not just ask, “Can I contribute this?” You also ask:

- Will this reduce flexibility for a pension strategy later on?

- Should one spouse contribute more than the other?

- Should the contribution happen before another super event?

- How does this sit beside other retirement income plans?

The best downsizer strategy is rarely just about getting money into super. It is about deciding whose super, when, and what that does to pension options later.

Perth property owners often have more scope, and more complexity

In higher-value markets, including many parts of Perth, the strategy can be especially useful because a property sale may generate enough surplus proceeds to make the contribution meaningful.

That is also where the mistakes can become expensive. A large contribution can improve the tax position inside super, but if it pushes the wrong part of the plan out of balance, the result may be less elegant than it first appeared.

The Step-by-Step Process to Making Your Contribution

This part needs accuracy more than creativity.

The downsizer contribution to super is not administratively difficult, but it is unforgiving if handled casually. Most problems come from timing, forms, or assumptions that the fund will fix things later.

Step one Decide before settlement chaos begins

Do not wait until after the move.

By the time settlement happens, there is usually enough going on already. Removalists, utility changes, legal documents, and new property logistics can make a simple super task feel harder than it should. The cleanest approach is to decide in advance whether you are likely to use the downsizer rules.

That gives you time to check eligibility, confirm which fund will receive the contribution, and think about how much to contribute.

Step two Know your settlement date

The 90-day timing rule is central.

Your contribution must generally be made within 90 days of settlement, not just whenever you get around to it. That means the settlement date should be recorded clearly and treated as a real deadline, not a soft target.

Step three Complete the right form properly

The required document is the ATO’s Downsizer contribution into super form (NAT 75073).

This form needs to be provided to your super fund before or at the time of the contribution. If you do not do that, the fund may treat the amount as a standard non-concessional contribution instead.

According to MLC’s technical guide on downsizer contributions and the NAT 75073 form requirements, getting this wrong can lead to the amount being treated as a normal contribution and potentially trigger excess contributions tax of up to 47%. The same source confirms the contribution must be made within 90 days of settlement.

Step four Make the payment to the correct super account

This sounds obvious, but it is worth slowing down for.

You need to contribute the money into the intended super fund correctly, with the form already in place. If you have multiple super accounts, or if you are rolling funds around at the same time, keep the process clean and documented.

A simple checklist helps:

Confirm the receiving fund

Make sure the account is open and ready to receive the contribution.Match the paperwork to the payment

Keep copies of the form, transfer record, and any fund confirmation.Use clear records

If a question comes up later, good records make the answer easier.

Step five Confirm classification after the contribution

Do not assume silence means success.

Check that the fund has recorded the amount as a downsizer contribution, not as another contribution type. If there is an error, you want to spot it quickly.

The rules are generous. The administration is strict. Most downsizer mistakes are not strategic mistakes. They are paperwork mistakes.

What if you are delayed

Extensions beyond the usual timeframe may be possible in limited circumstances, but they are not something to rely on casually.

If settlement timing, bank delays, or other factors have complicated the process, get advice before acting. This is one of those moments where a quick check can prevent a much larger clean-up later.

Weighing the Impact on Tax and Your Age Pension

A downsizer contribution can be attractive for tax reasons, but retirement planning is not only about tax.

For some people, the more important question is what happens to Centrelink entitlements after the money moves from the home into super. The strategy can become nuanced here.

The tax side

A downsizer contribution forms part of the tax-free component of super.

That is a meaningful feature. It can improve the tax profile of your retirement savings and, depending on your broader situation, may support a more efficient long-term structure inside super than holding the same money personally.

This is why the strategy often appeals to people who have spent years accumulating wealth outside super through the family home.

The Centrelink side

Your home and your super are not treated the same way.

For many people, the main residence sits outside the Age Pension assets test. Once sale proceeds are moved into super, that can change the Centrelink picture. The super balance may become assessable, which can reduce Age Pension entitlement.

According to Russell Investments’ explanation of downsizer contributions and Age Pension impact, adding $300,000 to super increases assessable assets by that amount and could reduce a single person’s Age Pension by up to $13,200 annually under current deeming rates and asset test settings.

That does not mean the strategy is bad. It means the strategy must be weighed properly.

A practical way to think about the trade-off

Here is the core trade-off in plain English.

You may move money from an asset that was exempt for pension testing into an asset that is counted. In return, you may gain a better tax setting inside super, better investment flexibility, and stronger long-term retirement funding.

Sometimes that trade-off is clearly worth it. Sometimes it is marginal. Sometimes it is the wrong move.

That depends on factors such as:

- Your age and pension status

- Whether you are single or part of a couple

- Your existing super balances

- How much of the sale proceeds you need outside super

- Whether preserving pension entitlement is a priority

A WA example without overcomplicating it

Suppose a retiree in Perth sells a long-held home, buys a smaller property, and has spare proceeds left over.

If that person contributes a large amount to super under the downsizer rules, the money may now sit in a more tax-effective environment. But if they are already at or near the Age Pension thresholds, the extra assessable asset value could reduce what they receive from Centrelink.

That is why this is never just a contribution decision. It is a retirement income decision.

Why modelling matters

Broad rules are not enough in this area.

Two people can make the same downsizer contribution and end up with very different outcomes because their super balances, pension eligibility, and spending needs differ. A strategy that looks excellent at first glance may become less appealing once the Centrelink effect is mapped out.

If you want to sense-check your own position, an Age Pension eligibility calculator can be a useful starting point before getting specific advice.

Good retirement planning is not about chasing the biggest super balance in isolation. It is about improving the combination of tax position, income security, access to capital, and peace of mind.

The balanced view

The downsizer contribution to super is often helpful, but it should not be treated as an automatic “yes”.

Its value comes from fit. If the contribution improves your long-term retirement position after tax and after Centrelink effects, it is doing its job. If not, the fact that the rules allow it does not mean you should use it.

Common Pitfalls and Advanced Downsizer Strategies

The downsizer rules look simple at a distance. Up close, a few traps appear quickly.

Most are avoidable. The problem is that people often discover them after the sale has settled and the clock is already running.

The common mistakes

Some errors are basic, but still costly.

Missing the deadline

The contribution window after settlement is strict. Once the deadline is missed, the strategy can unravel quickly.Submitting the form late

If the downsizer form is not provided correctly, the contribution may be treated as a normal after-tax contribution instead.Assuming any sold property qualifies

The strategy is tied to an eligible home sale; it does not apply to every property disposal.Trying to use it twice

This is a one-time opportunity per person.

The advanced SMSF angle

For SMSF members, there is a more technical version of the strategy. An in-specie downsizer contribution can involve transferring assets, such as shares, rather than moving cash alone.

That can be useful where liquidity or timing is awkward. But this is not an area for rough estimates or casual paperwork.

The ATO notes that audits for SMSF downsizer contributions rose 15% in 2025 due to non-arm’s length asset valuations, highlighting the compliance risk around downsizer contributions for SMSFs and in-specie transfers.

Why this strategy needs more care

With an in-specie contribution, valuation becomes critical.

If the asset is not valued properly, or the transfer is not handled on arm’s length terms, the compliance consequences can be serious. That makes this approach more specialised than a standard cash contribution into a retail or industry fund.

An advanced approach does not always mean better. Often it means less room for error.

A sensible rule of thumb

If your situation involves an SMSF, multiple properties, a complex title history, or concern about pension limits, do not treat the downsizer contribution as a form-filling exercise.

Treat it as a strategy review. The earlier those details are checked, the easier the process becomes.

Your Downsizer Checklist and Next Steps

The downsizer contribution to super can be one of the most useful retirement planning tools available to WA homeowners. It can also create problems when the details are rushed.

A simple checklist keeps the decision grounded.

| Step | Action Item | Key Consideration |

|---|---|---|

| 1 | Confirm eligibility | Check age, ownership period, residence status, and whether you have used the strategy before |

| 2 | Plan the timing | Work backwards from settlement so the contribution and paperwork happen within the required window |

| 3 | Prepare the form | Give the NAT 75073 form to the fund before or at the time of contribution |

| 4 | Assess the impact | Consider super balance effects, pension phase implications, tax outcomes, and Centrelink consequences |

The main point is simple. A downsizer contribution is rarely just a transaction. It is part of a broader retirement decision involving housing, super, tax, and income planning.

If you have spent years building equity in your home, it makes sense to be just as deliberate about how that equity supports the next stage of life.

If you want help turning a property sale into a clear retirement strategy, Wealth Collective can help. Their Perth and Dunsborough advisers work with pre-retirees and retirees to map out super contributions, Centrelink impacts, retirement income options, and the timing issues that trip people up. A free 10-minute introductory call is a simple place to start.