Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Retirement planning is about more than just numbers; it's about designing the future you've spent your career working towards. This guide provides practical financial advice for retirement planning to cut through the noise and answer the questions keeping you up at night.

Our goal is to help you move from feeling anxious about the future to taking clear, confident action. We want to empower you to build a retirement that isn’t just financially secure, but one that is truly fulfilling. This guide walks you through the core principles of the Wealth Collective process, showing you how to achieve just that.

Your Roadmap to a Secure Australian Retirement

For most Australians, the thought of retirement planning can feel overwhelming, often boiling down to two big questions: 'Will I have enough?' and 'How do I navigate this complex system?'. It’s easy to feel stuck when the path ahead is clouded by complex rules and contradictory advice.

Our goal is to give you clarity and control. What follows is the blueprint we use with our clients at Wealth Collective. We break down the retirement planning process into clear, manageable stages, helping you move from uncertainty to decisive action.

Understanding Your Starting Point

You can't plan a journey without knowing where you're starting from. For many, seeing the average super balance at retirement is an eye-opener. Data from the ABS and ASFA for 2026 shows Australian men aged 60-64 are retiring with around $420,000, while women have about $355,000.

However, one in four people over 60 have less than $200,000 in super, making them heavily reliant on the Age Pension. To put that in perspective, ASFA's 2026 Retirement Standard suggests $595,000 for a single person and $690,000 for a couple to live comfortably. You can explore how Australian retirement savings stack up in our detailed analysis.

This gap between what people have and what they need often comes down to common hurdles:

- Time out of the workforce for family or other reasons.

- Inconsistent super contributions over a career.

- Carrying mortgages or other significant debts into retirement.

The good news is, no matter your starting balance, a smart strategy can make a world of difference. The key is to break down big, intimidating questions into smaller, actionable steps you can take today. This is the foundation of the Wealth Collective approach.

Our Client-Focused Retirement Roadmap

This guide is structured around the Wealth Collective Retirement Roadmap, the same framework we use to provide our clients with direction and confidence. This isn't generic advice; it's a process for translating your personal retirement goals into a solid financial plan.

We help you define your ideal retirement, find ways to boost your savings, and protect your wealth from life’s curveballs.

By following the stages we’ve laid out, you’ll start making informed choices that align with the life you truly want to live. Our aim is to give you the knowledge you need to get started right now, long before you even need to book your free introductory call.

Defining What Your Ideal Retirement Looks Like

Before touching a spreadsheet, the most important part of retirement planning is figuring out what you're actually working towards. This isn't about abstract numbers; it's about painting a vivid, personal picture of the life you want to lead.

This discovery phase is the cornerstone of our Wealth Collective Retirement Roadmap. It’s where we translate your dreams into a concrete financial target, creating the foundation for a plan that's genuinely yours. After all, retirement isn’t just about stopping work—it’s about starting a new chapter filled with things that matter to you.

From Vague Ideas to a Concrete Vision

What does ‘comfortable’ really look like for you? It’s a deeply personal question.

For one couple, it might mean downsizing to free up cash for annual trips to Europe. For another, it could be staying put but finally having the time and money for gourmet cooking classes, regular theatre tickets, and spoiling the grandkids.

To get past vague notions, we help you map out your lifestyle goals. Think about the big one-off expenses and the small, day-to-day costs that will bring you joy.

- Big-Ticket Items: Are you planning a kitchen renovation? Buying a caravan? Helping your kids with a house deposit?

- Recurring Costs: What will your hobbies cost? Think about golf club memberships, art supplies, or a part-time TAFE course. How much should you budget for dinners out and socialising?

- Healthcare: It's also critical to be realistic about future healthcare needs, which tend to increase as we get older.

Writing these things down turns the fuzzy idea of 'a nice retirement' into a detailed blueprint. This isn't about limiting your dreams; it's about understanding them so we can build a financial structure strong enough to support them.

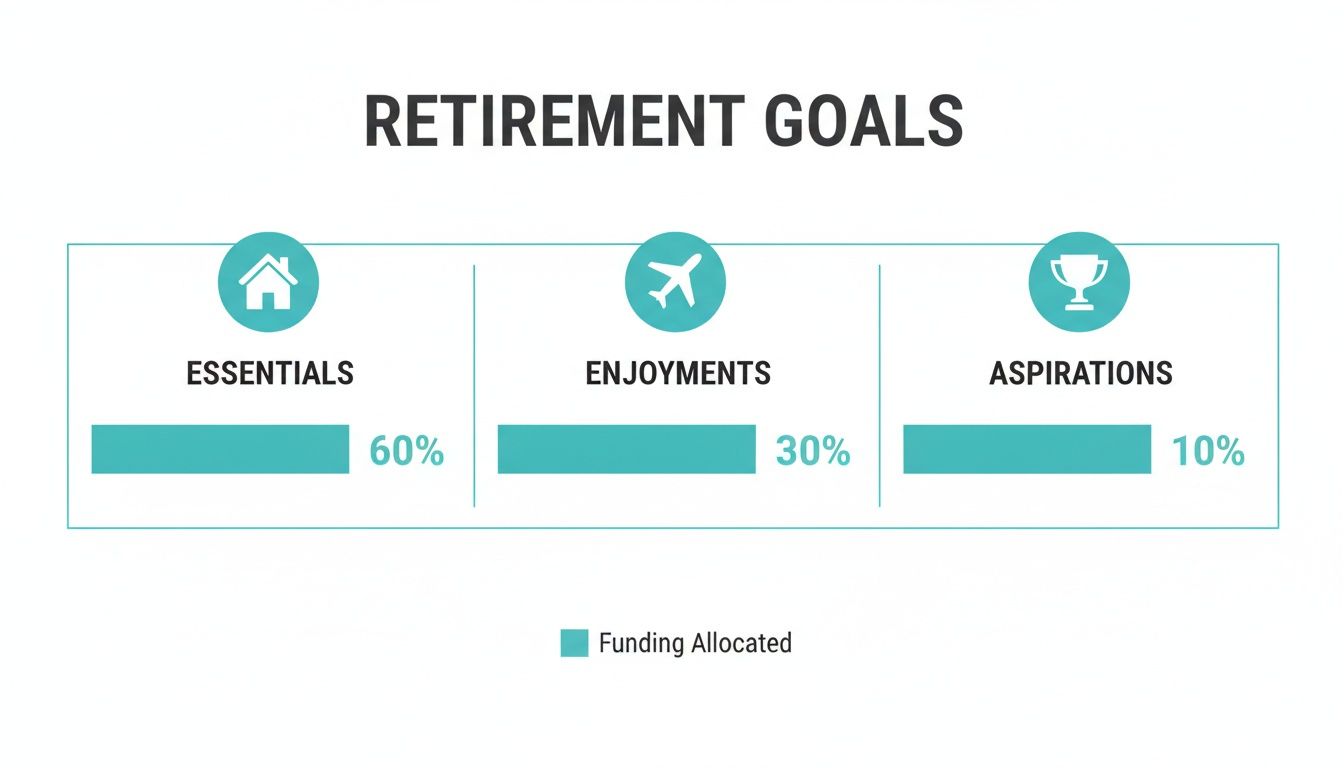

A Framework for Your Retirement Budget

Once you have a list of goals, the next step is to put them into categories. This simple framework helps create a realistic cash flow plan. We encourage our clients to sort their spending into three key buckets.

At Wealth Collective, we believe a successful plan doesn't just cover your needs—it funds your happiness. By bucketing expenses, you ensure that both essentials and enjoyments are accounted for, creating a balanced and fulfilling retirement lifestyle.

Let's break down how it works:

- Essentials: These are your non-negotiables. Think housing costs (rates, rent, or mortgage), utilities, groceries, transport, and basic healthcare. This is the bedrock of your budget.

- Enjoyments: This is where the fun is. This category covers travel, hobbies, dining out, entertainment, and gifts for family. This is the stuff you've worked so hard for.

- Aspirations: These are the big ‘what if’ goals. Perhaps it’s a major overseas adventure, leaving a significant legacy, or making a large philanthropic donation.

This process of defining and sorting your goals is the most valuable piece of the retirement planning puzzle. It anchors your entire financial strategy to what truly matters to you. For a better sense of what a 'comfortable' lifestyle might cost, you can explore the latest ASFA benchmarks in our detailed article.

With a clear vision and a target income in mind, you're no longer guessing. You now have a destination for your Retirement Roadmap. The next step is making sure your financial engine—your super and investments—is powerful enough to get you there.

Making Your Super and Investments Work Harder

Now that you have a clear picture of what you want your retirement to look like, it's time to ensure the engine driving your savings is tuned for performance.

For most Australians, superannuation is the workhorse of their retirement plan. The problem? Many people leave it in a default option, like driving a performance car stuck in first gear. Over the long run, this simple oversight could cost you hundreds of thousands of dollars.

Putting your money to work smarter is at the heart of good financial advice for retirement planning. It comes down to strategic tweaks that can seriously accelerate the growth of your nest egg.

Fine-Tuning Your Superannuation

Let's start with your super fund. Getting this right is often the biggest and easiest win.

- Hunt Down and Consolidate Your Super: If you’ve had a few jobs, you’ve probably collected a few super accounts, each chipping away at your balance with fees. Tracking them down and rolling them into a single, well-performing, low-fee fund is a no-brainer.

- Pick the Right Investment Option: Your super isn't a savings account; it's an investment. Most funds offer options from 'Conservative' to 'High Growth'. The right choice depends on your age and proximity to retirement. If you're in your 40s, you can generally take on more risk for potentially higher returns. Someone retiring in two years will need a very different strategy.

- Give It a Nudge with Extra Contributions: Small, regular top-ups can have a massive impact thanks to compounding. There are some very tax-effective ways to do this.

A tiny 1% improvement in your annual return, or a 1% reduction in fees, might not seem like a big deal. But over 30 years, it can boost your final balance by more than 25%. Small, consistent optimisations are what build serious long-term wealth.

Strategies to Supercharge Your Savings

Once the basics are sorted, you can look at more powerful strategies, especially in the crucial 10-15 years before you plan to stop working.

One popular method is salary sacrificing. It's an arrangement with your employer to direct some of your pre-tax pay straight into your super. Because these contributions are typically taxed at only 15%, it's a far more efficient way to save. You can learn more in our detailed guide on how salary sacrifice works.

You can also make after-tax contributions (non-concessional contributions). While you don’t get an immediate tax deduction, any money your super earns is still only taxed at a low rate of 15% – almost certainly less than your personal income tax rate.

This approach helps you build a solid foundation to cover your needs, wants, and future wishes.

Thinking about your goals this way helps ensure your investment strategy secures the essentials first before you start chasing those bigger, aspirational dreams.

Building Wealth Beyond Your Super

A truly solid retirement plan doesn't rely solely on super. Building a diversified investment portfolio outside of superannuation is key to creating more income streams and giving you greater flexibility.

It's a good idea to benchmark where you are versus where you need to be. The table below shows the gap many Australians face.

Australian Retirement Savings Benchmarks at a Glance (2026)

This table gives you a snapshot of projected average super balances versus what the Association of Superannuation Funds of Australia (ASFA) recommends for a 'comfortable' retirement.

| Age Group | Average Male Balance | Average Female Balance | ASFA Comfortable Target (Single) | ASFA Comfortable Target (Couple) |

|---|---|---|---|---|

| 70-74 | $501,785 | $449,540 | $630,000 | $730,000 |

Source: Rest Super projections & ASFA Retirement Standard

As you can see, the average balances often fall short of the 'comfortable' target, which is why a proactive strategy that includes investments both inside and outside of super is so important.

This is where having a proper plan makes all the difference. It's not just about boosting your super; it's about building a complete, diversified portfolio that aligns with your specific goals and gives you confidence you're on the right track. Our Guided Growth service is designed to do exactly this.

Protecting Your Wealth From Unexpected Events

Accumulating wealth is only one side of the coin. The other, equally crucial part is playing defence—safeguarding the nest egg you've worked so hard to grow.

Think of it this way: you wouldn't build your dream home and leave it uninsured. Your retirement plan deserves the same protection. An unexpected illness, injury, or market shock can quickly unravel decades of careful planning if you don't have a solid safety net.

The Critical Role of Personal Insurance

Personal insurance is arguably more important in the years leading up to retirement. When you’re closer to the finish line, you simply have less time to recover financially from a major setback.

Imagine a 58-year-old, a few years from her planned retirement, who has a serious medical event. Without the right insurance, she might be forced to dip into her superannuation early, drastically reducing her retirement income.

A smart insurance strategy prevents this. It’s your financial backstop.

- Income Protection: If you're still working, this cover replaces a large portion of your income if an illness or injury stops you from working.

- Total and Permanent Disability (TPD): This provides a lump sum payment if you're permanently disabled and can't go back to work.

- Trauma Insurance: This pays a lump sum if you're diagnosed with a specific condition like cancer or a heart attack.

- Life Insurance: This provides a payment to your loved ones if you pass away, helping them cover debts and maintain their quality of life.

Getting the right financial advice for retirement planning means looking at your insurance needs as part of the bigger picture. It’s about making sure one single event doesn't undo a lifetime of hard work.

A Professional Review for Peace of Mind

The world of insurance can be a minefield. Are you paying for cover you don't need? Are you dangerously underinsured? This is exactly why we offer our Protection Plus service.

As part of this service, we conduct a thorough review of your existing policies to see if your cover is adequate, cost-effective, and properly structured. We make sure your insurance strategy lines up perfectly with your retirement goals, so your defensive line is just as strong as your savings plan.

Managing Financial and Longevity Risks

Beyond your health, your retirement plan faces two other major risks: market downturns and the fact that Australians are living longer than ever. A key part of our job is to structure your finances to create a predictable and resilient income stream that can manage both.

We help our clients build a retirement plan that can weather market volatility. This often involves:

- Building a Cash Buffer: We recommend setting aside one to two years' worth of living expenses in cash or a very low-risk account. This means if the market tumbles, you won't be forced to sell investments at a low price to pay your bills.

- Using Allocated Pensions: This structure turns your superannuation into a flexible and tax-effective income stream, letting you draw a regular income while the rest of your capital stays invested for long-term growth.

By combining these strategies, we build a robust plan for your retirement funds, providing the confidence to enjoy your retirement, knowing you're prepared for life's surprises. Book a free introductory call with us to discuss how we can help protect your future.

Tackling the Tricky Stuff: Tax, Centrelink, and Your Estate

Once you stop working, the financial landscape changes completely. It’s no longer just about growing your wealth, but about making it last. This is where things can get complicated, with new rules around tax, the Age Pension, and your estate.

At Wealth Collective, we see this as connecting the dots – ensuring your super, investments, and will all work together. It’s about building a plan that not only funds your retirement but also protects your family down the track.

How Tax Works When You're Retired

One of the best perks of retirement is the way the tax system treats your super.

Once you’re over 60 and have officially retired, any income you draw from your super using an account-based pension is typically tax-free. This is a huge advantage that makes your retirement savings work much harder.

The tax treatment of your superannuation flips on its head once you enter the pension phase after age 60. Even the investment earnings inside your pension account become tax-free, which means your capital can continue to grow without being eroded by tax.

This tax-free environment is fundamental to good retirement planning. It's the reason strategies like a Transition to Retirement (TTR) can be so powerful in the years leading up to finishing work, as they help you get a head start on this tax-friendly setup.

Making Sense of the Australian Age Pension

The Age Pension is a vital part of the retirement puzzle for millions, but qualifying for it isn't always straightforward. Centrelink uses two separate tests to determine eligibility: an income test and an assets test. Whichever test gives you the lower pension payment is the one they'll use.

- The Assets Test: This adds up the value of most things you own, but your family home is excluded. It covers bank accounts, shares, investment properties, and your super balance once you’ve reached Age Pension age.

- The Income Test: This looks at income from all sources, including part-time work, rent, or the "deemed" income Centrelink calculates on your financial investments.

Knowing the ins and outs of these tests is crucial. With smart structuring, you can often improve your eligibility. Even a part-pension provides a reliable, indexed income for life, an incredibly valuable supplement to your own savings.

Why Your Estate Plan Matters So Much

A solid retirement plan looks beyond your own lifetime. It puts a structure in place to ensure the wealth you’ve built is passed on to your loved ones efficiently and as you intended.

If you don't get this right, you risk leaving behind family arguments, unexpected tax bills, and your assets not ending up where you intended. A few key documents are essential:

- A Valid Will: This is the absolute foundation. It’s your instruction manual for who gets what.

- Enduring Powers of Attorney: This lets you appoint someone you trust to manage your affairs if you're ever unable to do it yourself.

- Binding Death Benefit Nomination (BDBN): This is a formal direction to your super fund, telling them precisely who gets your superannuation balance.

The numbers show just how important this planning is. Treasury data reveals that nearly 50% of Australians approaching retirement have less than $250,000 in super. Yet, ASFA suggests a "comfortable" retirement needs more than double that, around $595,000 for a single person. You can read more about how super balances vary by age to see where you might stand. This gap shows why a strategy that covers every angle—including your estate—is so critical.

We help you put these protections in place as part of a holistic plan, giving you peace of mind that your affairs are truly in order. It's the final piece of your Retirement Roadmap and secures the legacy you've worked so hard to build. Book an introductory call with us to see how we pull all these crucial elements into one cohesive plan.

Putting Your Adviser to the Test: Key Questions to Ask

Walking into a financial adviser's office can feel daunting. You're about to trust someone with your future, so how do you know if they're the right person for the job?

The key is to go in prepared. Knowing the right questions to ask—and what a great answer sounds like—can make all the difference. A good adviser should welcome tough questions; it shows you’re serious and gives them a chance to demonstrate their expertise.

To help you get started, we've put together a list of crucial questions tailored to different stages of life.

Key Questions for Your Adviser Based on Your Life Stage

Finding the right adviser is about finding a strategic partner who understands your specific situation. The questions you ask should reflect where you are on your financial journey.

| Your Life Stage | Key Questions to Ask |

|---|---|

| Pre-Retiree (5-10 years from retirement) |

"My focus is shifting from growing my super to living off it. How will you help me create a reliable income stream that lasts?" "Can you show me what my retirement would look like if I retired at 62 versus 65, or if I decide to downsize my home? I need to see the real numbers." |

| Retiree (Already retired) |

"How can we structure my finances to guard against market downturns now that I'm not earning an income?" "What strategies can we use to make my retirement income as tax-efficient as possible and ensure I'm receiving all my Centrelink entitlements?" |

| Young Professional (Building career and wealth) |

"Beyond just contributing to my super, what other strategies should I be using to build wealth for the long term?" "I have some debt (e.g., HECS, mortgage). Should I focus on paying that down aggressively or investing more? What's the right balance?" |

| Small Business Owner | "My personal and business finances are completely linked. How do you approach planning for someone in my situation?" "What's the plan to protect my business and my family if something happens to me? What kind of insurance should I be thinking about?" |

These questions are designed to open up a deeper conversation. Pay close attention to how they answer. Do they use jargon, or do they explain concepts clearly? Do they ask follow-up questions about your specific life and goals?

What to Listen For in Their Answers

Recognising a quality answer is crucial.

For pre-retirees, a great adviser will immediately talk about structuring multiple income streams, building a cash buffer for market volatility, and maximising tax-free income. They should be excited to run different scenarios for you. This detailed cash flow modelling is a cornerstone of our Wealth Collective Retirement Roadmap because it replaces guesswork with certainty.

If you’re a young professional, a sharp adviser will talk about diversified investment portfolios and smart debt management. Their advice should feel comprehensive, much like the philosophy behind our Guided Growth service, which is about making your money work harder for you.

For business owners, the conversation must immediately include risk management. If they don't bring up personal insurance (like Life, TPD, and Income Protection) and business-specific cover, it’s a red flag. This is a key focus of our Protection Plus service.

Finding the right adviser isn’t about them having a perfect answer on the spot. It’s about their approach—a clear focus on your personal goals, a transparent process, and a willingness to have an open, honest conversation.

We believe the best partnerships start exactly that way.

Ready to see if we're the right fit for you? Book a free 10-minute introductory call today and put our team to the test.

Your Retirement Planning Questions Answered

As you get closer to retirement, it’s normal for practical questions to bubble up. Getting straight answers is key to feeling confident. We hear these questions all the time, so let's tackle the most common ones.

When Is the Best Time to Seek Financial Advice for Retirement Planning?

The honest answer? About 10-15 years before you plan to stop working. This gives you the longest runway to make smart adjustments and let the power of compounding work its magic.

But it's never too late. Even if you're only five years out, or have already retired, a good adviser can find ways to optimise your income, help you access Centrelink benefits, and make your money last longer. The most important thing is to start the conversation.

How Much Does Financial Advice for Retirement Cost?

Costs can vary, and it’s a fair question. At Wealth Collective, we are completely upfront about it. The process starts with a complimentary, no-obligation introductory call for you to decide if we're the right fit.

If we both feel it’s a good match, we’ll map out a fixed-fee proposal for developing your personalised Retirement Roadmap. That single fee covers all the research, modelling, and strategic work needed to build your plan. You know the exact cost before you commit—no hidden fees, no surprises.

Can I Just Plan for Retirement Myself?

You certainly can. The challenge is that the financial world—from superannuation law and tax rules to Centrelink and investment markets—is incredibly complex and always shifting.

An adviser brings an objective, professional eye, helping you sidestep common—and often irreversible—mistakes. Think of them as a financial coach; they hold you accountable to your goals and keep your plan on track. Often, the financial value they add through smart strategies and risk management far outweighs the cost of the advice itself.

What Happens in the Free Intro Call with Wealth Collective?

Our free introductory call is a relaxed, 10-minute chat to see if we can genuinely help you. There's no pressure or hard sell. You’ll speak directly with an adviser about where you are, what you’re aiming for, and what’s important to you.

We'll explain our process in simple terms and show you how our Retirement Roadmap service can bring the clarity you're looking for. It's a straightforward conversation to see if we can help you build the wildly successful financial life you deserve.

Ready to swap uncertainty for a clear plan of action? The team at Wealth Collective has helped hundreds of Australians build, protect, and enjoy their wealth. Book your free chat today to see how we can help you create the retirement you've worked so hard for.

Book Your Free Initial Chat Now