Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Picking the right super fund is one of those quiet decisions that can have a massive impact on your life, potentially adding hundreds of thousands of dollars to your final retirement nest egg. It’s about so much more than just a brand name; it’s a deep dive into fees, long-term performance, insurance, and investment options to find a fund that’s genuinely working to grow your wealth.

Why Your Super Fund Choice Shapes Your Financial Future

For most of us, super is just a line on a payslip—something that happens in the background. But treating it as a ‘set and forget’ part of your finances is one of the costliest mistakes you can make. Your super isn't a sleepy savings account; it's a powerful investment engine designed to fund decades of your life once you stop working. Making a conscious, informed choice here is you taking the wheel of your financial future.

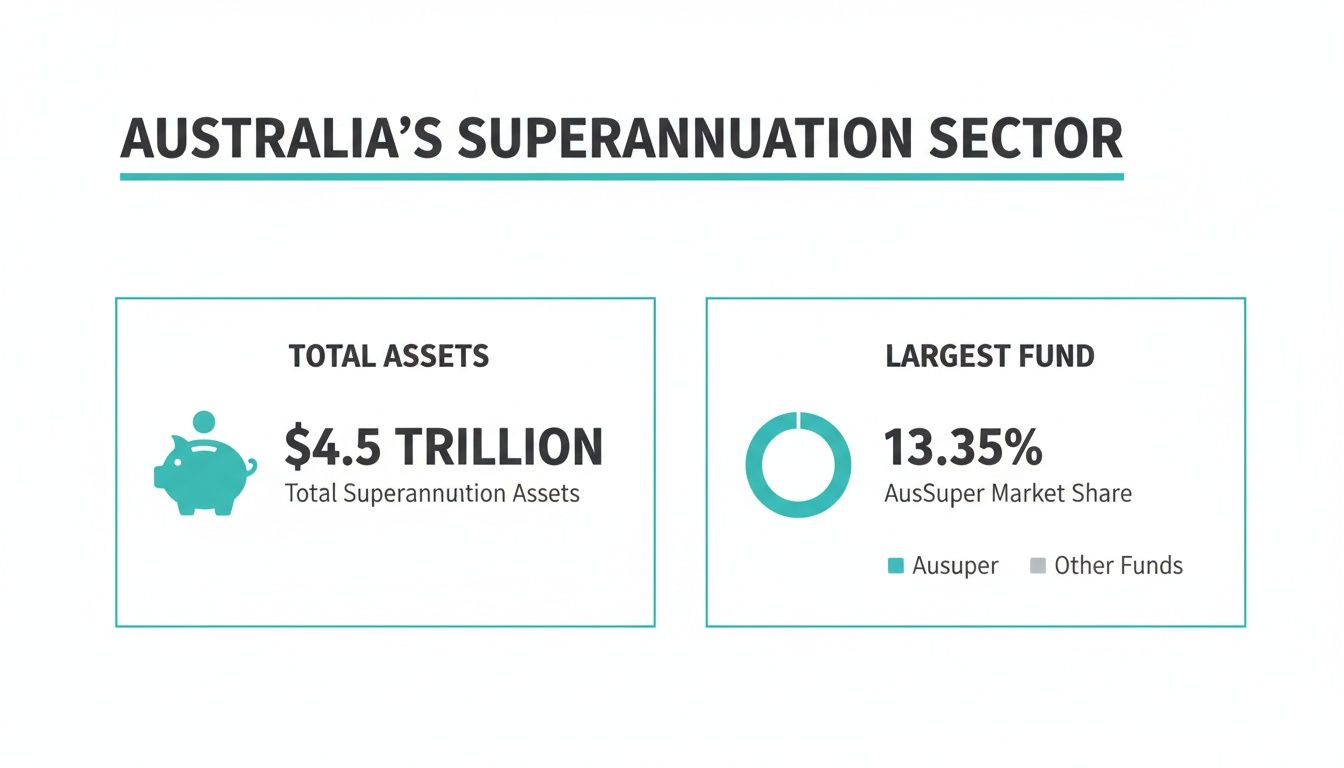

The sheer scale of Australia’s superannuation system shows just how much is at stake. The total value of super assets is forecast to swell to an incredible $4.5 trillion by September 2025, marking a 9.4% jump from the previous year. This is a massive pool of money that's actively growing, but you only get your fair share of that growth if you're in the right place.

The Core Factors to Get Right

Your choice of fund is what determines whether your money is compounding beautifully or being quietly eaten away by high fees and dud returns. When we boil it all down, there are four pillars to a smart super decision:

- Performance: How has the fund performed over the long haul? We’re talking consistent net returns after all fees and taxes have been taken out.

- Fees: What are you actually paying? You need to understand how both administration and investment fees add up over the decades.

- Investment Options: Does the fund give you choices that line up with your personal goals and how you feel about risk?

- Insurance: Is the default cover for life, disability, and income protection actually enough for someone in your situation?

Choosing a fund isn't about finding the absolute lowest fee or chasing last year's highest return. The real skill is in finding the right balance of all these factors—one that fits your personal circumstances and what you want to achieve in the long run.

The Real Cost of Doing Nothing

Sticking with an underperforming fund has a bigger impact than you might think. A seemingly small difference of just 1% in annual returns can easily lead to a $100,000 difference in your final balance by the time you retire. In the same way, paying unnecessarily high fees is like having a slow leak in your retirement savings, draining your balance year after year.

If you’re just getting started and want to wrap your head around the basics, our guide on what superannuation is in Australia is a great place to begin.

To help you get a clear, at-a-glance view of what to focus on, we've put together this quick guide.

Quick Guide to Choosing a Super Fund

This table breaks down the essential factors to consider, making it easier to compare your options and ask the right questions.

| Factor | What to Look For | Why It Matters for Your Retirement |

|---|---|---|

| Net Returns | Consistent 5 and 10-year performance after fees and taxes. | Short-term wins are nice, but long-term growth is what builds a substantial retirement fund. |

| Fees | Low administration and investment fees (compare % and flat fees). | Every dollar paid in fees is a dollar not invested and growing for your future. |

| Investment Options | A range of choices from conservative to high-growth. | Allows you to tailor your strategy to your age, goals, and comfort with risk. |

| Insurance | Flexible and affordable life, TPD, and income protection cover. | Protects you and your family without draining your retirement savings with high premiums. |

| Member Services | Quality of advice, online tools, and customer support. | Good service makes managing your super easier and helps you make informed decisions. |

Think of these factors as your personal checklist for cutting through the marketing noise and finding a fund that truly serves your interests.

This is exactly where personalised advice can make a world of difference. At Wealth Collective, our process is built to cut through the noise and complexity. We analyse the market to pinpoint funds that deliver strong, reliable growth while keeping a lid on costs. We then ensure your investment strategy and insurance cover are perfectly aligned with your stage of life, turning what feels like a confusing choice into a clear, confident plan for your future.

Fees vs. Performance: The Two Numbers That Truly Matter

When you're trying to choose the right super fund, it’s easy to get bogged down in jargon. But if you want to know what really drives your final retirement balance, it boils down to two critical factors: fees and long-term performance.

Getting this part wrong can quietly shave tens, or even hundreds, of thousands of dollars off your nest egg. It’s the small leaks that sink big ships, and the same is true for your super.

Don’t Underestimate the Damage of High Fees

A seemingly small difference in fees can have a massive impact over your working life, all thanks to the power of compounding. Think about it: a fund charging 1.5% per year versus one charging 0.5% might not sound like a big deal.

But over a 40-year career, that single percentage point can eat away a huge chunk of your potential growth. It's a silent drag on your wealth.

To get a clear picture, you need to know what you're actually paying for. Super fund fees typically fall into a few buckets:

- Administration Fees: These are the costs for running the fund—think account maintenance and sending you statements. They can be a fixed dollar amount, a percentage of your balance, or a mix of both.

- Investment Fees: This is what you pay the fund managers to actively manage your money and make investment decisions.

- Indirect Costs: A bit of a catch-all, this covers the transaction costs incurred when buying and selling assets. They aren't always obvious but are deducted from your returns before you see them.

Let’s put that into perspective. On a $100,000 balance, a 1% difference in total fees means $1,000 is gone from your account every single year. That’s $1,000 that isn't being invested and isn't compounding for your future.

The infographic below really puts the scale of Australia's super system into focus, showing just how much money is at play and why keeping an eye on fees is so vital.

With $4.5 trillion in total assets, the super industry is colossal. Seeing how giants like AustralianSuper command such a large market share helps you contextualise where your own fund sits in terms of fees and performance.

Look Past the Flashy One-Year Returns

Just as important as fees is how well your fund invests your money. This is where many people make a classic mistake: they get lured in by impressive one-year returns.

Here’s the thing: a fund that tops the charts one year can easily be at the bottom of the ladder the next. Chasing short-term winners is often a losing strategy.

What you should be looking for are consistent, long-term net returns. This is the growth your investment has achieved after all fees and taxes have been taken out, averaged over 5, 10, and even 15 years. This figure gives you a much more reliable picture of the fund’s skill and strategy.

Your goal isn't to find the fund that was the best last year. It's to find a fund with a proven track record of being consistently good over the long haul.

Recent data shows just how much returns can fluctuate. While some one-year super returns hit an impressive 10.5% to June 2025, the median balanced option is tipped to deliver 8.8% for the full year. A far more telling metric is the five-year real return average of 8.2%. You can explore more about the top super performers for 2025 to see how these numbers play out across the market.

At Wealth Collective, our ‘Guided Growth’ service is built on this very principle. We don't chase fads. We dig deep into a fund's long-term net performance and total fee structure to find options that have proven their ability to outperform while keeping costs in check. It’s all about finding sustainable growth, not a one-hit wonder.

The Real Winner Is the Net Benefit

Ultimately, the most important number is the net benefit—the investment return you receive minus the total fees you pay. A fund might have slightly higher fees, but if its long-term performance more than covers that cost, it could still be the better choice. On the flip side, a low-fee fund that constantly underperforms is a false economy.

Here’s a simple way to look at it:

| Metric | Fund A | Fund B |

|---|---|---|

| 10-Year Average Return | 8.5% p.a. | 7.5% p.a. |

| Total Annual Fees | 1.2% p.a. | 0.6% p.a. |

| Net Benefit | 7.3% p.a. | 6.9% p.a. |

In this scenario, Fund A comes out ahead. Even with higher fees, its stronger performance delivers a better outcome for your money. This is exactly the kind of analysis you need to do to make a truly informed choice.

Cutting through this complexity is where our expert guidance comes in. If you’re ready to make sure your super is working as hard as you are, book a complimentary call with us today.

Matching Investment Options and Insurance to Your Life

While fees and returns are the engine of your super's growth, your investment choices and insurance cover are the steering wheel and the airbags. They’re what make sure your super is actually working for you and your specific life circumstances. Get these right, and your super fund transforms from just a savings account into a powerful tool for building and protecting your wealth.

It's a fact that many Aussies are sitting in a 'MySuper' default option. These are designed as simple, low-cost products, but "one-size-fits-all" rarely fits anyone perfectly. By actively choosing where your super goes, you take control and can genuinely make a huge difference to your final balance.

Aligning Investments with Your Goals and Values

The best super funds give you a menu of investment choices, so you can build a strategy that makes sense for where you are in life and what you actually care about. This isn't just a small tweak; it's a critical part of taking the reins of your financial future.

Think about it. A 28-year-old just starting their career has decades ahead of them. They can generally afford to ride out the market's ups and downs for a shot at higher long-term returns. For them, a High-Growth option, packed with Australian and international shares, often makes a lot of sense.

Now, picture someone five years out from retirement. Their whole mindset is different. The number one priority is protecting the nest egg they've spent a lifetime building. A Conservative or Capital Stable option, which leans more heavily on bonds and cash, is a far smarter choice to dial down the risk.

But it’s not just about risk. Good funds now offer a whole lot more, including:

- Ethical or Sustainable Options: These let you invest your money in line with your values, avoiding industries like fossil fuels or tobacco and backing companies making a positive impact.

- Sector-Specific Choices: If you have a strong belief in a particular industry, like tech or healthcare, some funds let you tilt your investment portfolio in that direction.

- Index Options: A straightforward, low-cost choice. These options don't try to beat the market; they simply aim to track a specific market index, like the ASX 200.

Your investment choice isn't set in stone. In fact, it shouldn't be. The key is to find a fund that gives you the flexibility to adjust your strategy as your life, goals, and priorities change over the years.

Why Your Insurance Inside Super Needs a Closer Look

Here’s one of the most overlooked—and frankly, most critical—parts of your super: the insurance it provides. Most funds bundle in default cover for Life (a death benefit), Total and Permanent Disablement (TPD), and Income Protection.

The problem is, this default cover is just a basic safety net. "Basic" is rarely enough. Ask yourself: would the default TPD payout be enough to clear your mortgage and cover medical bills for the rest of your life if you couldn't work again? Would the default income protection cover your family’s actual living expenses? For most people with a mortgage or dependents, the honest answer is a hard no.

This is where a personal review is non-negotiable. Blindly relying on default cover can leave you and your family dangerously exposed right when you need that protection the most. You have to check that the level of cover truly matches your debts, your income, and the people who rely on you.

What’s more, the premiums for this insurance are paid directly from your super balance. If that cover is too expensive or not structured correctly, it can seriously eat away at your retirement savings over time. It’s a silent drag on your nest egg.

This is exactly where our ‘Protection Plus’ service comes in. We don’t just tick the box on default cover. We do a deep dive, a proper needs analysis, to figure out the exact level of cover your family requires. We make sure it's both adequate and cost-effective, aligning your insurance with your real-world situation so you aren’t left under-protected or overpaying for things you don’t need.

Making sure your investment strategy and insurance are a perfect fit for your life is a core part of choosing the right super fund. If you’d like an expert to review your current setup and ensure it’s providing the growth potential and protection you really need, book a no-obligation call with us today.

Thinking About a Self-Managed Super Fund (SMSF)?

Sooner or later, especially for business owners or those on a higher income, the conversation about super often turns to one specific acronym: SMSF. A Self-Managed Super Fund is precisely what it says on the tin—it's a private super fund where you're in the driver's seat. But while that control is a massive drawcard, it comes with a whole new world of responsibility.

Instead of a big institution managing your retirement savings, an SMSF lets you and up to five other people (usually family members) become the trustees. This makes you personally responsible for every investment decision and for keeping the fund compliant with Australia’s notoriously complex super and tax laws. It’s a serious commitment, far more than just opening a different kind of account.

The Allure of Control: Why an SMSF?

The appeal of an SMSF typically boils down to a desire for greater control, access to unique investments, and more sophisticated tax strategies. For the right person, the benefits are undeniable.

For example, a small business owner we work with was leasing her commercial workshop for years. By setting up an SMSF, she was able to use her super balance to purchase the property. Now, her business pays rent directly into her SMSF, simultaneously building her retirement nest egg and securing a physical home for her business. That’s a move you simply can’t make in a standard industry or retail fund.

Other common reasons people make the switch include:

- Direct Property Investment: SMSFs can invest in residential property, though the rules are very strict.

- Specific Share Purchases: You can buy shares in individual companies you believe in, rather than being stuck with a fund’s generic portfolio.

- Advanced Tax Planning: Once you retire, an SMSF can offer incredible flexibility in how you structure your income and manage capital gains tax.

An SMSF isn’t just a product; it’s a business. You become the fund manager, administrator, and compliance officer all rolled into one. The decision to start one should never be taken lightly or based on a trend.

The growth in this space speaks for itself. By September 2025, there were over 661,000 SMSFs in Australia, holding a staggering $1.07 trillion in assets. The average balance in an SMSF was a remarkable $849,678, dwarfing the averages seen in typical funds. You can dive deeper into the SMSF statistics and growth trends to get the full picture.

The Other Side of the Coin: The Serious Responsibilities

While the benefits are tempting, the downsides can be a harsh reality if you’re not prepared. The admin load is significant. You are legally on the hook for meticulous record-keeping, arranging an annual audit, and lodging specific returns with the ATO. A misstep can lead to hefty penalties.

Cost is the other major hurdle. Setting up an SMSF comes with legal and establishment fees. Then you have ongoing costs like accounting, the mandatory annual audit, and the ATO supervisory levy. These can easily run into thousands of dollars each year. For a full breakdown, have a look at the pros and cons of a self-managed super fund in our detailed guide.

At Wealth Collective, our ‘Retirement Roadmap’ service helps clients navigate this exact crossroad. An SMSF can be a powerful engine for your retirement, but only if it genuinely fits your financial situation, your goals, and your personal capacity to manage it. We provide the strategic advice to figure out if an SMSF is a smart move for you or a complex distraction you're better off avoiding.

Book an initial call with us to get clear, personalised guidance on whether an SMSF is right for you.

Your Final Checklist Before Making the Switch

Alright, you've done the hard yards. You’ve waded through the details on fees, performance, investment choices, and even the world of SMSFs. Now comes the most important part: putting all that knowledge to work to make your final decision.

This isn’t just about picking a fund with a good one-year return. It’s about methodically checking your choice against what really matters for your retirement. Think of this as your final sanity check before you commit.

Nail the Numbers First

Before you get lost in the smaller details, focus on the two metrics that will make or break your long-term growth. Get these right, and you're well on your way.

Start by looking past flashy short-term results and pull up the 5 and 10-year net return figures. This shows you which funds have a track record of steady, consistent performance, not just a single lucky year.

Then, add up all the fees—administration, investment, and any other sneaky costs. A fund quoting a 0.8% total annual fee on a $150,000 balance will cost you $1,200 a year. Every. Single. Year. Does the performance justify that cost?

Align the Fund with Your Actual Life

A fund that’s perfect for a 25-year-old starting out is often a terrible fit for someone nearing retirement. Make sure the fund's features are genuinely right for you, right now.

- Investment Options: Does the fund give you real choice, from conservative to high-growth? Crucially, does it have an option that aligns with your personal risk tolerance and values? If you’re looking for a sustainable or ethical investment, make sure it’s a legitimate offering.

- Insurance Cover: This is a big one. Don't just accept the default cover. Check the amount of Life, TPD, and Income Protection insurance you have and ask yourself if it’s truly enough to cover your mortgage, debts, and your family's needs. Are the premiums competitive? Accidentally losing valuable insurance when switching funds is a devastating—and common—mistake. For a deeper dive on this, our guide on how to switch super funds is a must-read.

Before you sign anything, ask yourself this simple question: Does this new fund leave me better off after fees, with an investment strategy I'm comfortable with, and the right insurance to protect my family? If you can't say a firm "yes" to all three, it's not the right fund.

Watch Out for Hidden Traps

The biggest financial stings often happen during the switch itself. People get so focused on the shiny new fund that they forget to check the fine print on their old one. A few minutes of due diligence here can save you thousands.

- Exit Fees: They’re less common these days, but some older-style funds still charge you for leaving. It’s worth scanning your latest statement or the Product Disclosure Statement (PDS) to be sure.

- Capital Gains Tax (CGT): This is particularly critical for anyone in pension phase or managing an SMSF. Switching investment options can be a CGT event, potentially triggering a tax bill you weren't expecting. It’s vital to understand this before you act.

Get a Professional Sanity Check

You've done the research, you've narrowed it down, and you think you have your winner. But how can you be 100% sure? A quick, expert second opinion can be the most valuable step you take.

At Wealth Collective, this is what we do. We can quickly benchmark your chosen fund against your personal situation and our deep market knowledge. We’ll either confirm you've made a great choice or point out a better option you may have overlooked.

A complimentary 15-minute chat with our team is the smartest final step you can take. It’s a simple, no-pressure way to validate your decision and ensure your super is set up to build the future you deserve.

Frequently Asked Questions About Choosing a Super Fund

Even with all the research in the world, it's natural to have a few last-minute questions before you commit to a super fund. Getting these queries sorted is often the final step you need to feel confident in your decision.

We hear these questions all the time, so let's walk through them with some straight-up, practical answers.

How Often Should I Review My Super Fund?

Your super is definitely not a ‘set and forget’ part of your finances. Ignoring it is like letting your retirement savings drift without a rudder. While you don’t need to obsess over it daily, a proper, thorough review at least once a year is a must.

Think of it as an annual financial health check. This is your chance to make sure your fund is still performing well, the fees haven't crept up, and your investment mix still makes sense for where you are in life.

It's also crucial to take a closer look whenever life throws a curveball. Big changes almost always have an impact on your super needs. We're talking about events like:

- Landing a new job or a significant pay rise.

- Getting married or welcoming a new family member.

- Buying a home or taking on other large debts.

- Any changes to your health.

These moments can completely change your financial picture and, just as importantly, your insurance needs. The cover that was perfect last year might leave you dangerously underinsured today.

At Wealth Collective, this kind of proactive review is central to how we help our clients. We make sure their super strategy is optimised for their life right now, not based on decisions they made years ago.

What Is the Difference Between an Industry and a Retail Fund?

The main thing that separates industry and retail funds is who they're trying to make a profit for.

Industry super funds were originally set up for specific industries and are run to profit their members. Any surplus they make is meant to flow back to you through lower fees or better services. Most are now open for anyone to join.

Retail super funds, on the other hand, are owned by commercial entities like banks or large wealth companies. Their goal is to generate a return for their shareholders, as well as for their fund members.

Historically, industry funds have often shown slightly higher average returns and lower fees. But this is just an average, not a guarantee. There are some excellent retail funds out there, just as there are some lacklustre industry funds.

Don't make the classic mistake of picking a fund just because it's 'industry' or 'retail'. You need to ignore the labels and compare them head-to-head. Focus on the numbers that matter: long-term net performance, all-in fees, and whether the features actually suit you.

Should I Consolidate My Multiple Super Accounts?

For the vast majority of Australians, the answer is a resounding yes. If you have super scattered across multiple accounts, you're almost certainly paying several sets of admin fees and, often, multiple insurance premiums.

Every extra fee is a small leak that slowly drains your retirement savings. Over decades, those small leaks add up to a huge amount of lost money.

Pulling everything into one well-chosen fund has some clear wins:

- Lower Fees: One set of account-keeping fees is much better than two or three.

- Simpler Life: It's so much easier to track your progress and manage your investments with just one account.

- Less Clutter: One annual statement is all you'll have to deal with.

But here’s the crucial bit: before you close any old account, you absolutely must check your insurance. You could unknowingly cancel valuable life, TPD, or income protection cover. If your health has changed since you got it, you might not be able to get that level of cover again.

This is where getting some professional help can save you a massive headache. An adviser from Wealth Collective can look after the whole consolidation process for you, making sure any essential insurance is ported over or replaced properly. We manage the paperwork to get you into the right fund without leaving any gaps in your cover.

Can I Choose My Own Super Fund if My Employer Has a Default?

Yes, you can. ‘Choice of Fund’ laws give most of us the right to tell our employer exactly where to pay our super.

On top of that, the 'Super Stapling' rules now mean your super account follows you from job to job. When you start with a new employer, they have to pay into that "stapled" fund unless you tell them otherwise.

If you're just starting out and don't have a fund, your employer will put you into their default option. But you are never locked in. You always have the power to switch to a fund that’s a better match for your own goals and risk appetite. Just accepting the default could mean settling for average performance and missing out on better features elsewhere.

Trying to figure out how to choose a super fund can feel like a huge task, but you don't have to tackle it on your own. At Wealth Collective, our expert advisers are here to cut through the confusion and create a clear, actionable plan that’s built specifically for you.

If you’re ready to get your super working harder for your future, book a complimentary introductory call with us today.