Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Making money work for you is the shift from simply earning a wage to actively building wealth. It’s about putting your money in a position to generate more money, creating financial security and freedom, even while you sleep. This guide outlines the proven strategies to get you there.

Shifting Your Mindset from Earning to Growing

Trading time for a paycheck can feel like a hamster wheel—you work hard, pay bills, and start all over again. But what if your money could work just as hard, if not harder, than you do?

This isn't a secret reserved for the ultra-wealthy; it’s an achievable goal for any Australian professional ready to move from being a passive earner to an active wealth builder. This starts with a strategic plan.

The Power of a Strategic Plan

The engine behind wealth creation is compounding. Think of it as a snowball effect: the returns your money earns start earning their own returns, creating exponential growth over time.

However, compounding doesn’t happen by accident. It requires a clear, intentional roadmap that directs your money where it can be most effective. This is where professional guidance can turn confusion into a clear path forward.

Making your money work for you is less about how much you earn and more about how purposefully you manage what you have. The goal is to build a system where your wealth grows independently of your direct labour.

At Wealth Collective, our entire process is designed to build this system for you. We provide the clarity and structure needed to become a confident wealth builder, using a framework built on three core pillars.

Our Proven Framework for Success

This framework ensures every part of your financial life works together, creating a solid foundation for growth and security.

- Protection Plus: We secure your foundation first. This pillar addresses personal insurance to ensure unexpected life events don’t derail the wealth you’re building. It's the safety net that lets you pursue growth with confidence.

- Guided Growth: This is where we actively put your money to work. We create personalised investment strategies that align with your goals, timeline, and risk tolerance, moving beyond just superannuation to build accessible, lasting wealth.

- Retirement Roadmap: We help you visualise and plan for the future you want. This involves optimising your superannuation and creating a clear plan to ensure your wealth supports you long after you stop working.

By integrating these pillars, we provide a proven path to making your money work for you. Let's walk through the practical strategies that bring this framework to life.

Building Your Unshakeable Financial Foundation

Before you can grow wealth, you need a solid base. Like building a house, a grand design is useless on shaky ground. This foundation provides stability and control, setting the stage for everything that follows.

The starting point is a clear spending plan. This isn't a restrictive budget; it's a tool for empowerment. It gives every dollar a job and aligns your spending with your values.

This is a cornerstone of the Wealth Collective process. We start by helping you gain a crystal-clear snapshot of your finances. There’s no judgement—it’s about gaining the clarity you need to make your money work for you, not against you.

Automate Your Progress

One of the most effective ways to build wealth is to put your finances on autopilot. This means setting up automatic transfers for your bills, savings, and debt payments, removing decision fatigue from the equation.

Imagine your pay lands, and before you think about it, money is automatically directed to:

- Pay your rent or mortgage.

- Cover regular bills like your phone and power.

- Top up your emergency savings.

- Make extra payments on high-interest debt.

This is the classic "pay yourself first" method, and it works. It ensures your most important financial goals are addressed before you have a chance to spend that money elsewhere. For a deeper dive, see our guide on cash flow management.

The Non-Negotiable Emergency Fund

Think of an emergency fund as your financial lifebuoy. It's a dedicated stash of cash, typically 3 to 6 months' worth of essential living expenses, kept separate for life’s surprises—a sudden job loss, medical crisis, or urgent car repair.

Without this buffer, one unexpected event can send you into high-interest debt, derailing your financial plan. It's the safety net that allows your other wealth-building efforts to continue, uninterrupted.

We’ve seen the power of this firsthand. A Perth couple we worked with, both in roles tied to the same industry, faced a redundancy when a downturn hit. Their six-month emergency fund was a game-changer. They could comfortably cover their mortgage and bills while seeking a new role, without touching their long-term investments.

Strategies for Tackling High-Interest Debt

High-interest debt from credit cards and personal loans actively works against you. The interest costs are like a leak in your financial bucket, draining your income and preventing you from saving and investing effectively.

Two proven methods get great results:

- The Avalanche Method: You apply all extra repayments to the debt with the highest interest rate first, while making minimum payments on everything else. Mathematically, this approach saves you the most money in interest.

- The Snowball Method: You focus on paying off the smallest debt first, regardless of the interest rate. Scoring that quick win provides a powerful psychological boost to tackle the next debt.

Getting out of debt is a serious wealth-building move. We find that clients who prioritise eliminating high-interest debt achieve faster growth in their net worth. This is why our strategies at Wealth Collective focus on helping clients reduce loans; from experience, we know households with lower debt-to-income ratios simply build savings faster.

Building a strong financial foundation isn't about restriction; it's about creating freedom. It’s the process of putting systems in place that allow you to grow your wealth with confidence, knowing you are protected from life's uncertainties.

Once this foundation is solid, you'll have the stability and cash flow to focus on growth. Booking a complimentary call with a Wealth Collective advisor is the perfect next step to build this unshakeable base for yourself.

Superannuation: More Than Just a Retirement Fund

Too many Australians see their super as a locked box—a distant, passive account they can’t touch for decades. That’s the wrong way to look at it.

Your super is one of the most powerful wealth-building engines you have, primarily because of its tax efficiency. Shifting your mindset from "retirement fund" to "wealth engine" is the first step to unlocking its true potential.

Grow Your Nest Egg Faster with Tax-Smart Contributions

The magic of super is its concessional tax treatment. When you contribute extra money from your pre-tax salary—a strategy known as salary sacrificing—that money is taxed at only 15%.

For most working professionals, that’s a massive discount compared to their marginal income tax rate, which can be as high as 45%. This tax difference means more of your money gets invested and starts compounding from day one.

Let’s look at a real-world scenario:

- Imagine a high-income earner on a $150,000 salary. Their marginal tax rate is 37% (plus Medicare levy). If they invest $10,000 outside of super, they lose $3,900 to tax, leaving just $6,100 to invest.

- If they salary sacrificed that same $10,000 into super, they would only pay $1,500 in tax. That leaves $8,500 invested and working for them—a $2,400 immediate head start.

Done consistently, this strategy can add hundreds of thousands of dollars to your final retirement balance.

Strategies That Evolve With Your Life

The best way to use your super changes as you move through life.

- For High-Income Earners: Maximising salary sacrificing up to the concessional cap is a no-brainer to lower taxable income and turbocharge savings.

- For Growing Families: A higher-earning spouse can make a spouse contribution to build their partner’s super balance, potentially earning a tax offset.

- For Small Business Owners: Personal deductible contributions can reduce your business or personal tax bill while building a nest egg separate from the business.

These strategies are a core part of our Retirement Roadmap service. We analyse your specific circumstances to find the optimal contribution methods, ensuring no tax benefits are left on the table. To learn the basics, see our guide to learn more about the fundamentals of superannuation in our detailed guide.

Your Investment Choice Could Be Worth Hundreds of Thousands

Making smart contributions is only half the battle. How your super is invested is just as crucial. Most funds offer a menu of options, from conservative to high-growth, and your choice can have a staggering impact on your final balance.

Don't just set and forget your super. While a 'balanced' option feels safe, the compounding power of a growth-focused strategy over 20-30 years can be life-changing.

With Australia’s superannuation pool hitting $3.9 trillion by June 2026, it's a powerful force. Historically, high-growth super options have returned an average of 8.9% p.a. over 20 years, outperforming many other asset classes. You can explore more about these powerful investing facts and their sources.

That level of growth could turn a $100,000 balance at age 40 into over $650,000 by retirement.

Navigating the contribution rules and investment options can feel overwhelming. A quick chat with an advisor at Wealth Collective can provide the clarity to transform your super from a forgotten account into your most powerful wealth-building tool.

Investing Beyond Super for Real Financial Freedom

Once your foundation is solid and your super is optimised, it’s time to build wealth outside the super system. This is where true financial freedom begins, giving you the flexibility and options you need long before retirement.

A personal investment portfolio allows you to target specific life goals, like saving for a home deposit, funding education, or building a passive income stream. You are building wealth that you can access on your own terms.

The Power of Diversification Explained

You’ve likely heard the term diversification. It’s the age-old wisdom of not putting all your eggs in one basket.

Think of it like building a winning sports team. You need a mix of players with different skills to create resilience. Investing is the same. You need a blend of different assets that perform differently under various market conditions.

Key tools for building a balanced portfolio include:

- Direct Shares: Owning a piece of an individual company, like BHP or Commonwealth Bank.

- Exchange-Traded Funds (ETFs): Excellent for instant diversification. An ETF trades on the stock exchange and typically tracks an index, like the ASX 200, giving you a slice of hundreds of companies in a single transaction.

- Managed Funds: Your money is pooled with other investors into a portfolio that's professionally managed for you.

The goal is to create a blend of assets that strikes the right balance between risk and return for your personal goals and timeline.

What Does a Diversified Portfolio Look Like?

The right mix of assets depends on your goals and risk tolerance. The table below shows a few sample portfolio allocations.

Sample Diversified Portfolio Allocations by Risk Profile

| Asset Class | Conservative Investor (e.g., Pre-Retiree) | Balanced Investor (e.g., Young Professional) | Aggressive Investor (e.g., High Earner) |

|---|---|---|---|

| Australian Shares | 20% | 35% | 30% |

| International Shares | 20% | 40% | 50% |

| Property/Infrastructure | 15% | 10% | 10% |

| Fixed Interest/Bonds | 35% | 10% | 5% |

| Cash | 10% | 5% | 5% |

As you can see, a pre-retiree would lean towards defensive assets like bonds and cash. In contrast, a high earner might take on more risk with international shares to chase aggressive growth. This is just a guide; the right mix is always one built specifically for you.

Redefining Investment Risk

When most people hear "investment risk," they think of a market crash. While that is a risk, the real silent killer of wealth is inflation—the steady increase in the cost of living that erodes the purchasing power of your money.

The biggest investment risk isn’t always losing money in the short term. It’s letting your money sit idle while inflation eats away at its value over the long term.

Cash sitting in a savings account might feel safe, but if it’s earning 1% while inflation is at 3%, you’re losing 2% of your wealth every year. Investing is your best defence.

Consider the Australian market: $10,000 invested in the ASX 200 index in the early 1990s, with dividends reinvested, could have grown to over $250,000 by 2026. That’s the power of compound growth, blowing inflation out of the water. You can dig deeper into what historical market data tells us about successful investing.

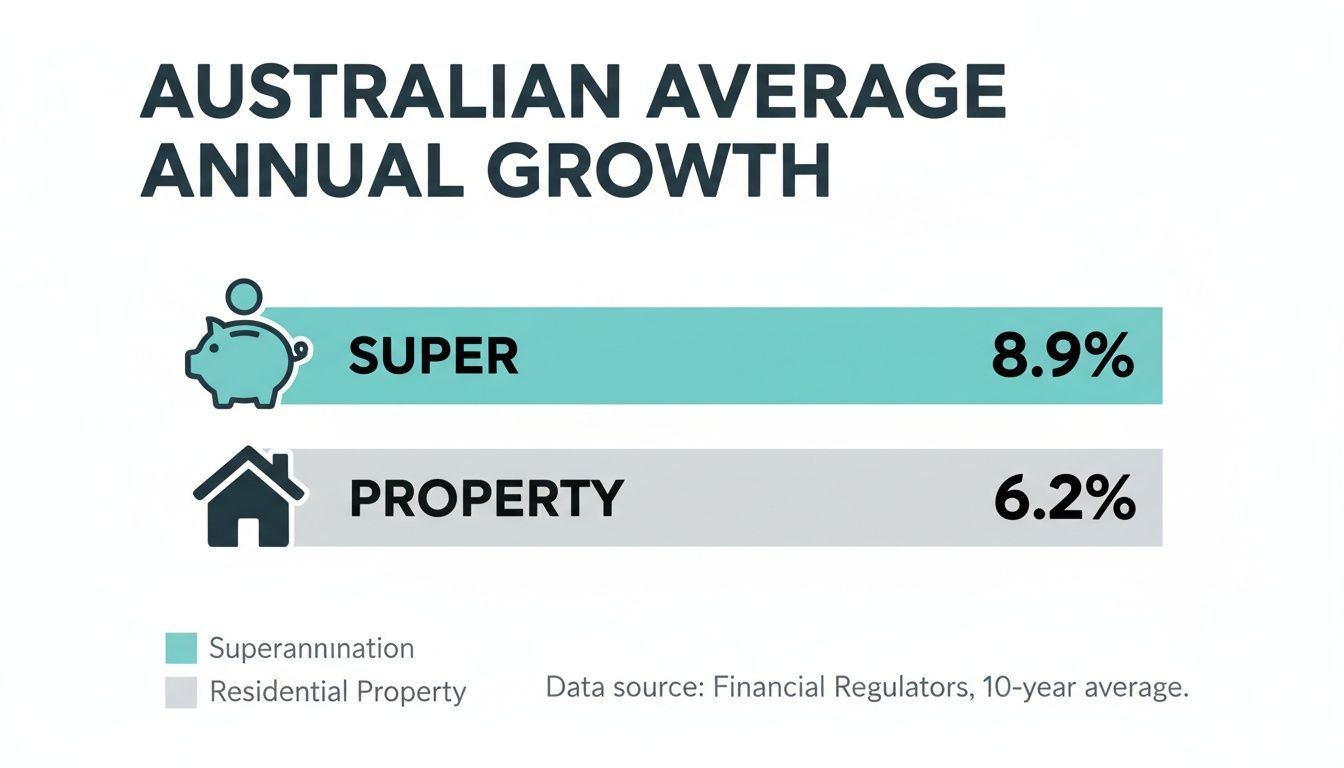

This chart compares the average annual growth of superannuation (which is heavily invested for growth) against property over the last decade.

The data speaks for itself. Growth-focused assets, like those in a typical super fund, have historically delivered stronger returns. This is why our Guided Growth service focuses on creating a diversified portfolio designed to outpace inflation and build real wealth.

If you're ready to move beyond the basics, booking an initial call with a Wealth Collective advisor is the perfect next step.

Protecting The Wealth You're Building

Watching your wealth grow is exciting, but all that hard work can be undone in a moment if it's not protected. Personal insurance is the part of the plan you hope you never need, but it's what ensures bad luck doesn't derail your future.

Think of your financial plan as a high-performance engine. Personal insurance is the roll cage. It’s the safety system that lets you pursue growth with confidence.

Why Insurance Is A Non-Negotiable Part Of Your Plan

Let's be direct: what would happen to your family and your financial goals if you suddenly couldn't earn an income? How would the mortgage get paid?

Personal insurance provides a financial backstop by protecting your most valuable asset: your ability to earn an income. The main types you need to consider are:

- Income Protection: This is your financial lifeline. It pays a monthly benefit, typically up to 70% of your pre-tax income, if you can't work due to illness or injury. It covers your living costs so you don’t have to burn through savings or sell investments.

- Total and Permanent Disablement (TPD): TPD pays a lump sum if an injury or illness leaves you permanently unable to work. This money can help clear debts, pay for medical care, and adapt your home.

- Life Insurance (or Death Cover): This is for the people you leave behind. It pays a lump sum to your family if you pass away, giving them the means to pay off the mortgage, cover future education costs, and maintain their life without financial hardship.

Protecting your ability to earn an income is one of the smartest financial decisions you can make. Without it, your entire wealth creation plan is built on a foundation of risk.

The Real-World Impact Of Protection

It's easy to dismiss insurance as just another expense, but its impact is profound.

Imagine a professional with a family and a mortgage. An unexpected health crisis takes them out of work for a year. Without income protection, they would face draining their savings, selling investments, and potentially losing their home.

Now, picture the same scenario with the right cover. Her income protection policy kicks in, replacing her salary. The bills are paid, and her long-term investment strategy continues untouched. That is the real-world peace of mind that proper protection delivers.

This is precisely where our Protection Plus service comes in. We don't just look at your assets; we analyse your risks to build the right safety net. For more detail, our guide on the main types of life insurance in Australia is a great resource.

A complete financial plan isn't just about growth; it's about resilience. To explore how we can build this essential safety net into your financial life, book a complimentary call with a Wealth Collective advisor today.

So, What's Next on Your Financial Journey?

We’ve covered the blueprint for putting your money to work: build an emergency fund, automate your savings, clear high-interest debt, optimise your super, invest for growth, and protect it all with the right insurance.

This guide is your roadmap. It lays out the proven path that others have followed to achieve financial success.

From a Roadmap to a Personal Itinerary

Knowing the path is one thing; walking it is another. Making your money work for you isn't a passive exercise. Every decision needs to be filtered through your personal goals, stage of life, and risk tolerance.

A roadmap shows the general direction, but you need turn-by-turn directions crafted just for you. This is where expert help makes all the difference, helping you sidestep common mistakes and stay on course.

The most important step you can take is always the next one. You’ve done the reading and gained the knowledge; now it’s time to put it into action.

Take that next step today. We offer a complimentary, no-obligation 10-minute introductory call with an experienced Wealth Collective adviser. It’s a straightforward way to see how these strategies could look in your own life.

In our chat, we can get a feel for your goals and show you how a personalised plan can bring clarity and confidence to your financial future. Let's start the conversation.

Frequently Asked Questions

As you start to get your finances in order, questions are bound to come up. Here are some of the most common ones we hear, along with our straightforward answers.

How Much Money Do I Need to Start Investing?

The myth that you need a huge lump sum to start investing is just that—a myth. You can get started with just a few hundred dollars, thanks to micro-investing apps and Exchange Traded Funds (ETFs).

What’s far more important than the starting amount is the habit. Investing a small, regular amount is what builds serious wealth over time through the magic of compounding. The key is just to begin.

Should I Pay Off My Mortgage or Invest Extra Money?

There’s no single right answer—it comes down to your personal situation and what helps you sleep at night.

Mathematically, if your expected investment returns (after tax) are higher than your mortgage interest rate, you'll likely grow your net worth faster by investing. This is the core idea behind our Guided Growth service.

However, paying down your home loan offers a guaranteed, risk-free return and immense peace of mind. For many of our clients, a hybrid approach—chipping away at the mortgage while also investing—is the best of both worlds. A Wealth Collective advisor can run the numbers for your specific situation to help you find the right balance.

The "right" answer is the one that aligns with both your financial goals and your personal comfort level. A tailored plan considers both the maths and the emotions behind your money.

Is It Too Late to Start If I'm Nearing Retirement?

Absolutely not. It’s never too late to make a real, positive difference to your retirement.

When you're closer to retirement, the strategy simply shifts. We focus on making catch-up super contributions, structuring investments for reliable income, and planning tax-effective drawdowns. Our Retirement Roadmap service is built for this exact stage of life, helping you fine-tune your position for a comfortable retirement.

Turning these ideas into an actual plan for your life is where real progress happens. At Wealth Collective, our job is to translate these concepts into a clear, personalised strategy that works for you.

Ready to see what that could look like? The next step is a simple, no-obligation chat with an advisor.