Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Switching your superannuation fund is more than just paperwork. It involves a close look at fees, investment performance, and insurance before making the move, usually through your new fund or the myGov portal. It's one of the most effective ways to boost your retirement savings, but it's absolutely critical to get your insurance sorted before you close any old accounts.

Why Switching Your Super Fund Is a Powerful Wealth Strategy

It’s easy to think of super as a ‘set and forget’ account that just ticks along in the background, quietly collecting contributions from your employer. But leaving it on autopilot is one of the most expensive financial mistakes an Australian can make.

Learning how to switch super funds isn't just a bit of life admin. It's a genuine, proactive wealth-building move. Picking the right fund can seriously accelerate your savings for retirement, while sticking with the wrong one can silently sabotage your future.

The Real Cost of Inaction

Over your working life, the combined impact of high fees and so-so investment returns can be absolutely devastating. A seemingly tiny difference of just 1% in annual fees can slash your final retirement balance by tens, or even hundreds, of thousands of dollars.

Think about a young professional in Perth with a $50,000 super balance. Over the next 30 years, being in a fund with higher fees and sluggish growth could easily cost them a six-figure sum by the time they retire. For a family in Dunsborough getting closer to retirement, that impact is far more immediate. This isn't just about figures on a page; it's about the kind of life you can afford to live in your later years.

At Wealth Collective, our process views switching super as a foundational step toward taking control of your financial future. It's about consciously choosing a vehicle that's going to work harder for you, not just letting your savings drift in a default option that might not be right for you at all.

A Critical Warning on Insurance

Before you get excited and start switching, there's one thing you must pay close attention to: your personal insurance cover. For years, people felt trapped in underperforming super funds because they didn't want to lose their basic Life, Total and Permanent Disablement (TPD), and Income Protection insurance.

Thankfully, those days are over.

Modern insurance products can now sit separately from your super fund and premiums can still be paid from super via an enduring rollover authority. This means that people are no longer stuck using the basic, group cover arrangements through their own super fund. They can now mix and match the super fund that best fits their needs with a separate, more comprehensive insurance product tailored to their occupation rating, pastimes, medical and family history.

This separation gives you the best of both worlds:

- Choose the best super fund: You’re free to pick a fund based entirely on what matters most—investment performance, low fees, and the features you need.

- Get superior insurance: You can secure a much better policy from a specialist insurer, one that's customised to your specific job, health, and family situation—not just the generic group cover offered by a fund.

This "mix and match" strategy lets you optimise both your retirement savings and your personal protection without having to compromise on either. It’s a core part of the strategic planning we do with our clients, making sure they have all the facts to make a truly confident switch. Making these decisions is what drives clients to book an initial call with us.

Doing Your Homework: A Pre-Switch Reconnaissance Mission

Before you even start window shopping for a new super fund, you've got to do some solid intelligence gathering on your current setup. Trust me, jumping the gun without all the facts is a classic recipe for regret. This prep work is easily the most crucial part of the whole process—it’s what helps you dodge the common traps and make a smart choice based on hard data, not just slick marketing.

Your first mission? Hunt down every single super account you own. It's incredibly common for people to collect extra accounts as they move between jobs, often without even realising it. These forgotten pots of money are quietly being eroded by duplicate fees and insurance premiums you don't need.

And this isn't a small problem. Across Australia, there's been a massive shift towards consolidating super. A huge 79% of the super population—that's over 14 million people—now have just one account. This is a game-changer for everyone from young professionals to those nearing retirement, because multiple accounts are sneaky retirement thieves. The ATO itself warns that these extra costs chew directly into your savings, making consolidation a non-negotiable first step. You can see the data for yourself and read more about the trend towards single super accounts on the ATO website.

Finding All Your Super (Even the Lost Stuff)

Luckily, tracking down all your super isn't the mission impossible it used to be. The Australian Taxation Office (ATO) has made it pretty simple through your myGov account.

- Jump onto myGov: Log in and make sure your account is linked to the ATO's online services.

- Head to the 'Super' section: Once you're in, you’ll see a list of all known super accounts in your name, including any that are flagged as 'lost' or 'unclaimed'.

- Consolidate with a few clicks: The portal lets you roll multiple accounts into your main fund right then and there. This one action alone could save you thousands in unnecessary fees over your lifetime.

By knocking this over first, you get a clear, complete picture of your retirement savings and immediately stop the financial bleed from having too many accounts.

Getting Your Hands on the Key Documents

Now that you've got all your super in one place, it's time to download the vital documents from your current fund. You're looking for two key items: your most recent annual statement and the fund's Product Disclosure Statement (PDS). You can usually find these in your fund's online member portal.

These documents are your treasure map—they hold all the critical details you need to do a proper, apples-to-apples comparison later on. Seriously, don't skip this. Trying to compare funds without this info is like trying to navigate a new city without a map. If you need a refresher on the basics, our guide explains in simple terms what superannuation is and how it works in Australia.

To make this easier, here’s a quick checklist of the critical information you need to pull from your statements. Having these details handy will make the comparison process a whole lot smoother.

Key Information to Gather from Your Current Super Fund

| Information Point | Where to Find It | Why It's Important |

|---|---|---|

| Total Balance | Your annual or most recent member statement. | This is your starting point—the total amount you'll be rolling over to a new fund. |

| Investment Option(s) | Listed on your statement (e.g., 'Balanced', 'Growth'). | You need to know how your money is invested to compare its performance against other options. |

| Fees & Costs | The "Fees and Costs" section of your PDS and statement. | This includes admin fees, investment fees, and indirect costs. High fees are a major drag on returns. |

| Insurance Cover Details | The insurance section of your statement. | Note the type (Life, TPD, IP) and the amount of cover you have. This is critically important. |

| Insurance Premiums | Clearly itemised on your statement's transaction list. | You need to know exactly how much you're paying to see if you can get better value elsewhere. |

| Member Number & Fund USI | At the top of your statement or member card. | You'll need these details to fill out rollover forms or complete the switch online. |

Digging up these details might feel like a bit of a chore, but it’s the foundation for making a switch that genuinely benefits your financial future.

A Word of Warning About Your Insurance

As you go through your documents, pay very close attention to the insurance details. You’ll see cover for Death (Life), Total and Permanent Disablement (TPD), and maybe even Income Protection.

The single biggest mistake people make when switching super is accidentally cancelling valuable insurance cover they can't get back. Before you even think about closing your old account, you absolutely must assess your insurance needs.

The great news is you're no longer forced to stay in a dud super fund just to keep your insurance. Modern insurance products can now be held separately from your super, with the premiums still paid from your super account. This strategy is a real game-changer. It means you can:

- Pick the super fund that offers the best performance and lowest fees for your investment goals.

- Separately choose a comprehensive insurance policy that's properly tailored to your job, health, and family situation.

This "mix and match" approach lets you optimise both sides of the equation—your investments and your protection—without compromising on either. It’s a core part of the Wealth Collective process; we always make sure your financial safety net is secure before touching your investments. With all this intel gathered, you're finally ready to start comparing funds like a pro.

Comparing Super Funds: How to Look Beyond the Marketing Hype

Alright, you've got the lowdown on your current super fund. Now for the most important part: seeing how it stacks up against the competition. This isn't about being wooed by a catchy TV ad or a slick website. It’s about a cold, hard look at what really moves the needle on your retirement savings.

To make a smart choice, you need to cut through the noise and focus on three things that truly matter: investment performance, the fees you're being charged, and the features that actually add value. Getting this right is the secret to a successful switch.

The Real Story on Investment Performance

Everyone's eyes go straight to the performance numbers, but they can be incredibly deceiving. A fund that shot the lights out last year might look tempting, but a single great year often tells you nothing about its long-term reliability. It could just be a fluke or the result of a risky bet that happened to pay off.

You need to zoom out. Think like a seasoned investor, not a gambler.

- Go long. Forget one-year returns. Look at performance over 5, 7, and especially 10 years. This gives you a much better picture of how the fund’s investment brain works through all the market's ups and downs.

- Compare apples with apples. This is a classic mistake. If you’re in a ‘Balanced’ option, you must compare it to another fund’s ‘Balanced’ option. Pitting it against a ‘High Growth’ fund is like comparing a family sedan to a sports car—the results will be completely skewed.

- Look for consistency. Is the fund always somewhere near the top of the pack, or does it bounce from hero to zero year after year? A fund that’s consistently solid is often a far better bet than one that takes wild swings.

A fund that has delivered steady, above-average returns for a decade is showing you it has a process that works. That’s what you want managing your money.

Unpacking the Damage Fees Can Do

Fees are the silent assassins of your super balance. On paper, a 1% or 1.5% fee looks tiny. But over 30 or 40 years, that small percentage compounds into a massive bite out of your retirement nest egg—we're talking hundreds of thousands of dollars. It’s critical you know exactly what you’re paying.

Here are the main culprits to hunt down in the fine print:

- Admin Fees: This is what they charge you just to keep the lights on and manage your account. It could be a flat fee, a percentage of your balance, or a mix of both.

- Investment Fees: This is the cost for the experts to actually invest your money. It’s always a percentage and changes based on your investment option. A High Growth option, for instance, will almost always have higher investment fees than a simple Cash option.

- Indirect Costs: These are the sneaky ones. They're costs related to managing the underlying assets that aren't always clearly listed. You’ll need to dig into the Product Disclosure Statement (PDS) and look for the 'Indirect Cost Ratio' (ICR) to find them.

Add all these fees up to get your total annual cost. Seriously, even a 0.5% difference in total fees each year can mean a six-figure difference to your final balance when you retire. It's that significant.

Features That Genuinely Make a Difference

Beyond the numbers, a good super fund should fit your life and give you the tools you need to feel in control. But again, you have to separate the genuinely useful features from the shiny gimmicks.

Think about what matters to you:

- Investment Options: Does the fund just offer a handful of pre-mixed options, or can you get more hands-on? Some funds let you build your own portfolio from direct shares or ETFs. For those wanting ultimate control, a Self-Managed Super Fund might even be on the horizon. You can explore the pros and cons of an SMSF in our detailed guide.

- Ethical & ESG Choices: If you care about where your money is invested, check out their Environmental, Social, and Governance (ESG) or ethical options. Do they actually align with your values?

- The Digital Experience: Is their app and website easy to use? A clunky online portal is frustrating. A great one makes it simple to check your balance, see how your investments are tracking, and make quick changes.

This stuff is more important than ever. Australians are pouring money into their super, with total contributions recently jumping by 12.7% to $215.6 billion in a single year. With a staggering $4.5 trillion in total super assets—and nearly half of that invested overseas—choosing a fund with good global diversification and low costs is just smart thinking.

APRA’s latest statistics show a clear trend: members who are proactive and switch funds based on this kind of careful evaluation are putting themselves in a much stronger position for the future.

By digging into performance, fees, and features, you stop being a passive passenger and become the driver of your own retirement journey. That clarity is what transforms switching super from a chore into one of the most powerful financial decisions you can make.

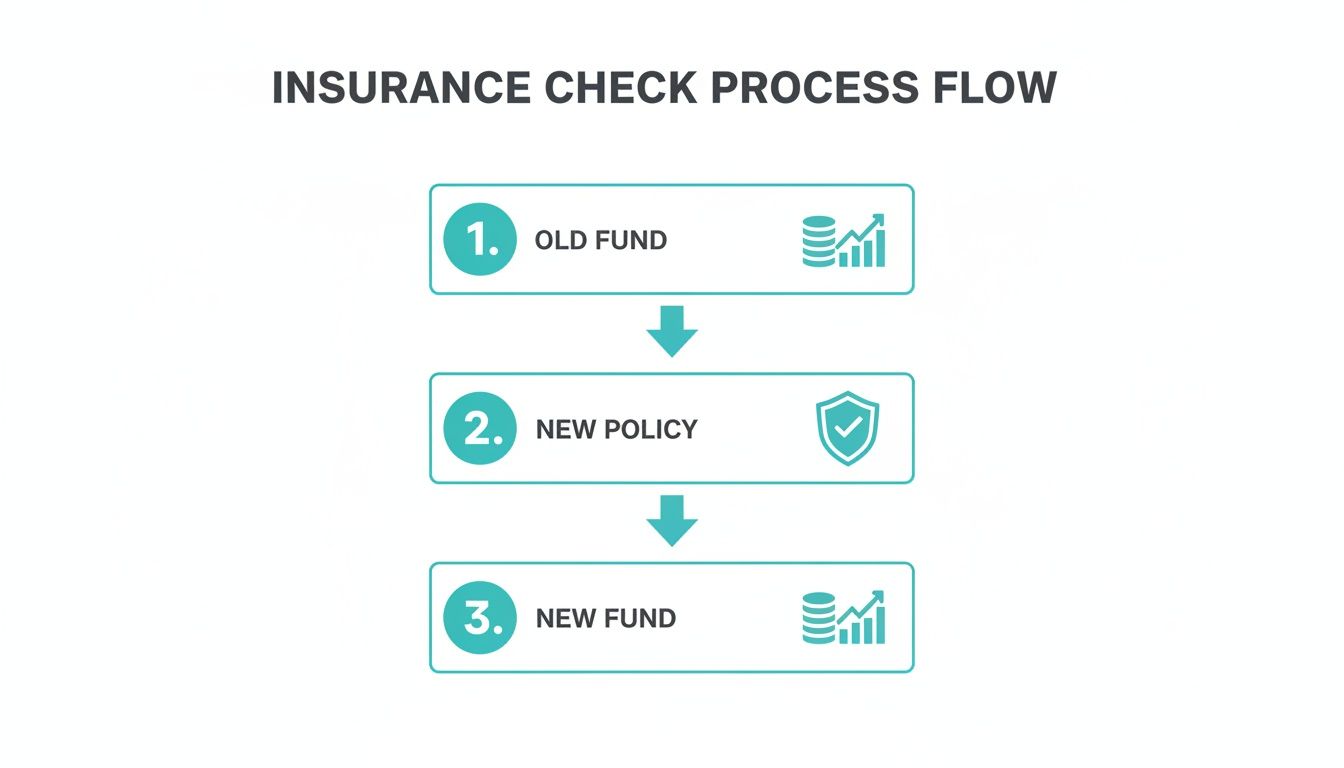

Don't Switch Anything Until You've Checked Your Insurance

Before you even think about moving your super, we need to have a serious chat about insurance. This isn't just a box-ticking exercise; it's a huge red flag that far too many people miss. In fact, one of the most damaging mistakes you can make when switching super funds is accidentally wiping out your existing insurance cover.

For a lot of us, the default Life, Total and Permanent Disablement (TPD), and Income Protection cover tucked away inside our super is the only safety net we have. If you close your old account before you have a new policy locked in, you could leave your family in a terrible position if something unexpected were to happen.

You're No Longer Forced to Choose

For years, this created a real dilemma. People felt trapped in poor-performing, high-fee super funds because they were terrified of losing their insurance. Getting new cover isn't always straightforward, especially if you have a pre-existing health condition. It can be difficult, expensive, or sometimes even impossible to get the same level of protection again.

The great news is, that's no longer the case. The game has changed. You don't have to put up with a bad super fund just to hang onto your insurance. The modern way is to separate the two, which gives you complete control.

This is a game-changer. It means you can have the best of both worlds: a top-performing, low-fee super fund, and a separate, high-quality insurance policy that's actually designed for you. It’s a strategy that puts you firmly back in the driver's seat.

The 'Mix and Match' Strategy: How It Works

The old-school approach meant you were stuck with whatever basic, one-size-fits-all group insurance your super fund offered. These policies can be full of fine print and exclusions, and often aren't a great fit for your specific job or lifestyle.

The smarter way is to 'mix and match' your super and insurance for a truly personalised setup. It's quite simple:

- Pick the Best Super Fund: First, you analyse and choose a fund based purely on its investment strengths—think performance, fees, and features that will help you reach your retirement goals.

- Lock in Better Insurance: Then, you work with an expert to find a comprehensive policy from a dedicated insurer. This policy is built just for you, taking into account your job, hobbies, health, and family situation.

- Link Them Together: You can still have the premiums for your new, separate insurance policy paid directly from your chosen super fund. This is done through what's called an enduring rollover authority, which just tells your super fund to automatically pay the insurer for you.

This strategy guarantees you're never left unprotected. You get the right insurance sorted first, and only then do you move your super. If you want to dive deeper into this, you can learn more about how superannuation and income protection work together in our detailed guide.

Why a Personalised Policy is So Important

That generic group policy you get with your super might look good on paper, but it often falls short when it matters most. A bricklayer, for instance, has a completely different risk profile to an accountant working in an office. A generic policy might not properly cover the specific risks a tradie faces, which could lead to a claim being denied down the track.

A tailored policy, on the other hand, is underwritten specifically for you. It gives you certainty because it's been designed around your life.

This is exactly what our Wealth Collective process is all about. We take care of this entire process for you, assessing your personal needs to find the perfect insurance fit. We make absolutely sure your new, better cover is locked in before we do anything with your super. It’s a careful, structured approach that completely removes the biggest risk of switching funds and a key reason clients seek our guidance.

Making the Switch Happen

You've done the hard yards—the research, the comparisons, and the critical insurance checks. Now for the final, and often most satisfying, part: actually moving your money. The good news is that the rollover process itself is usually more straightforward than the prep work.

So, how do you actually do it? There are a few common paths you can take.

- Let your new fund do the heavy lifting. This is easily the most popular and simplest route. When you're filling out the online application for your new fund, you'll hit a section asking for the details of any old funds you want to roll over. Just plug in the information, and they'll take it from there, managing the entire transfer for you.

- Use your myGov account. If you've got your myGov account linked to the Australian Taxation Office (ATO), you can log in and manage your super directly. It's a secure government portal that puts you in the driver's seat to consolidate and transfer your super balances.

- Work with a financial adviser. If you’re a Wealth Collective client, this is something we handle from start to finish as part of our process. We take care of all the paperwork and coordination to ensure the switch happens smoothly and at the right time, so you don't have to worry about a thing.

Getting Your Ducks in a Row

To make the process seamless, it’s a good idea to have a few details ready to go. This will save you from scrambling to find a statement at the last minute.

You'll need:

- Your Tax File Number (TFN)

- Proof of ID, like your driver's licence or passport

- The name of your old super fund

- Your member number with that old fund

- The Unique Superannuation Identifier (USI) of the old fund

Your member number and the fund's USI are easy to find – they'll be on your most recent annual statement or you can find them by logging into your old fund's online portal.

A Crucial Reminder About Your Insurance

I know we've mentioned this before, but it's the single most important part of this process: get your insurance sorted before you close your old account. Cancelling an old policy before a new one is firmly in place is a mistake you can't afford to make.

The great thing is that modern insurance products are far more flexible. You can hold a policy completely separate from your super fund, but still have the premiums paid directly from your super account. This structure gives you the freedom to pick the best-performing fund and the best-value insurance, without having to compromise on either.

This is the modern, risk-free way to approach it.

The key takeaway here is to have your new, tailored insurance policy fully approved and active before you even think about starting the rollover. This completely removes the risk of being left uninsured, even for a day.

The Final Steps to Lock It In

Once you hit 'go' on the rollover, your money will typically transfer within three to ten business days. It's worth remembering that during this window, your balance is effectively 'out of the market'—it’s not invested anywhere. To play it safe, it's generally a good idea to avoid switching during times of extreme market ups and downs.

After the transfer is done, you should get a confirmation from both your old fund (saying the money has left) and your new fund (saying it has arrived). Log in and double-check that the full balance has landed safely in its new home.

Now for the final, crucial step that people often forget: you must tell your employer. Your new fund will give you a 'Superannuation Standard Choice Form'. Fill this out and hand it straight to your payroll or HR department. If you don't, your employer's super contributions will keep flowing into your old, now-empty account, creating a messy (and annoying) situation to fix later.

It’s so easy to just leave things as they are. But overcoming that inertia and making a proactive switch away from a subpar fund is one of the most powerful moves you can make for your future wealth.

It's a strange quirk of human behaviour. Even though retirement confidence is on the rise in Australia, a staggering 59% of Aussies plan to keep their super in the exact same fund when they retire. This is the highest level of inertia seen globally. Sticking with the status quo can be incredibly costly, especially when you consider that top-performing funds have grown investments by over four times in the last two decades. You can read more about these retirement trends and the power of strategic switching here.

Pitfalls to Sidestep and When to Call for Backup

Even with the best intentions, switching your super can feel like navigating a minefield. It's easy to make a wrong turn that costs you dearly down the track. One of the most common traps I see people fall into is chasing last year's top-performing fund. That’s like driving by looking only in the rearview mirror – it tells you nothing about the road ahead.

Another classic mistake is glossing over the fees. A seemingly tiny difference of 0.5% or 1% might not sound like much, but over a few decades, that small percentage can quietly erode tens, or even hundreds, of thousands of dollars from your final nest egg. And, as we've touched on, forgetting to sort out your insurance is probably the biggest and most dangerous pitfall of all.

Knowing When to Bring in a Professional

Look, if your situation is simple—you're young, have one account, and standard insurance needs—you can often handle a switch yourself. But your super is your future, and some situations really do call for an expert eye.

You should seriously think about getting professional advice if you:

- Are nearing retirement and simply can't afford to get it wrong.

- Have a family or specific health concerns that mean basic, off-the-shelf insurance just won't cut it.

- Feel completely snowed under by the endless choices of funds and investment strategies.

- Are managing a more complicated setup, like a Self-Managed Super Fund (SMSF), where the tax rules are a whole different ball game.

Getting expert advice isn't an admission of defeat. It’s about making a smart, strategic move with confidence, ensuring your decision truly lines up with where you want to be financially.

This doesn't have to be a complicated or intimidating process. At Wealth Collective, our process is designed to give you clarity, not confusion. It all starts with a complimentary initial call so we can get a feel for your situation and see if we're the right fit to help.

Think of it as a simple, no-strings-attached way to get a professional take on your super. It’s about making sure your next step is a solid one. Book your free initial call with a Wealth Collective adviser today and let's get started.

Common Questions About Switching Super

Changing your super fund can feel like a big decision, so it's smart to have a few questions. Let's tackle some of the most common ones I hear from clients, so you can feel confident about making the move.

How Long Does It Actually Take to Switch?

Once you kick off the process, the actual money transfer is surprisingly quick. You can expect your balance to land in the new account within three to ten business days.

This is thanks to the ATO's SuperStream system, which keeps things ticking along. Keep in mind, though, that for this short window your money is technically 'out of the market'—it's not invested while it’s in transit between funds.

Will I Have to Pay Tax on the Switch?

For most people switching between regular accumulation funds, the answer is a simple no. Because it's a direct rollover and not a withdrawal, there are generally no tax implications.

Be warned, though: if you're dealing with a defined benefit fund or a Self-Managed Super Fund (SMSF), things get more complicated. Moving assets out of these structures can trigger Capital Gains Tax (CGT), so getting professional financial advice before you lift a finger is absolutely critical.

Do I Need to Let My Boss Know?

Yes, and this is a crucial final step that’s easy to overlook. Once your new super account is up and running, you need to give your employer a completed ‘Superannuation Standard Choice Form’.

Your new fund will give you this form to fill out. If you forget this bit, your employer will keep paying your contributions into your old, empty account. It’s a messy (and completely avoidable) situation to fix later on.

Getting these details right is exactly where good advice makes all the difference. At Wealth Collective, our process is designed to make sure every box is ticked—from checking your insurance to notifying your employer—so your switch is smooth and strategic.

To make sure your next move is a powerful one for your financial future, book your complimentary initial call with our team today.