Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Dipping into your super before you retire is a huge financial step, and it's one the Australian government takes very seriously. Your super is your nest egg for the future, so the law puts a tight lock on it.

However, life happens. There are a handful of legitimate, though very specific, situations where you might be able to get early access. Think of these not as loopholes, but as safety valves for times of genuine crisis. Navigating this process is complex, and a single misstep can have lasting consequences—this is where strategic advice becomes invaluable.

Should You Access Your Super Early? What to Know First

Let’s be clear: your superannuation isn’t a rainy-day fund. It’s a long-term investment powerhouse, designed to grow over decades to support you when you stop working. That’s why the rules for early access are so strict—they’re there to protect your future self.

Before you even think about applying, you need to understand the very narrow pathways available. Each one has a demanding set of eligibility criteria and a specific application process. It's not as simple as asking your fund for some cash.

Early Release Conditions at a Glance

To give you a clearer picture, we've summarised the main reasons you might be able to access your super early. This table outlines the core conditions and what you can typically access, but remember that specific rules apply to each.

| Condition | Primary Eligibility Requirement | Typical Amount Accessible |

|---|---|---|

| Severe Financial Hardship | Receiving eligible government income support for 26 consecutive weeks. | One lump sum of between $1,000 and $10,000 in a 12-month period. |

| Compassionate Grounds | Needing funds for specific costs (e.g., medical treatment, preventing home foreclosure). | Amount required to cover the specific cost. Evidence is essential. |

| Terminal Medical Condition | Diagnosis from two medical practitioners confirming a life expectancy of less than 24 months. | Your entire super balance, tax-free. |

| First Home Super Saver (FHSS) Scheme | A proactive savings strategy using your super account to save for a first home deposit. | Up to $15,000 of voluntary contributions per year, to a total of $50,000. |

These conditions are rigid. The Australian Taxation Office (ATO) and your super fund will scrutinise every detail of your application.

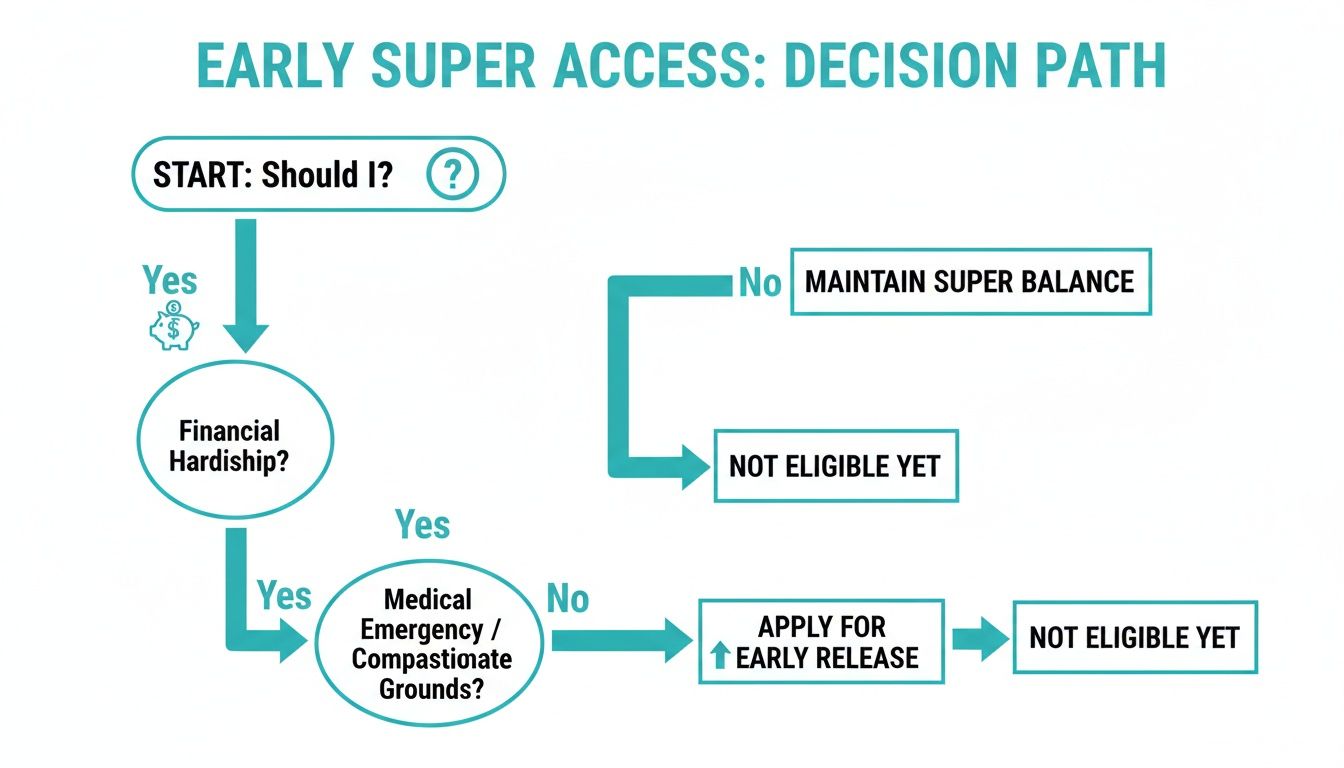

This decision-making flowchart gives you a good visual of the questions you need to ask yourself.

As you can see, the path is only open in very serious circumstances. Any amount you withdraw has a permanent impact on your retirement. You don't just lose the money you take out; you lose all the compound interest it would have earned.

It's absolutely vital to have a solid grasp of what superannuation is and how it works before you consider touching it.

Tapping into your superannuation is an irreversible financial move. It's not just about the money you take out today; it's about the decades of potential growth you sacrifice tomorrow.

The application process itself can be stressful and confusing. A single mistake or missing document can get your application rejected, sending you back to square one. This is where getting professional guidance makes all the difference.

We often help clients navigate this exact situation. It starts with a simple, no-obligation chat to understand where you're at. We’ll explore every possible alternative with you, aiming to build a plan where accessing your super is a true last resort, not your only option.

The Hidden Cost of an Early Super Withdrawal

Thinking about dipping into your super early can feel necessary when you're in a tight spot. But before you go down that path, it’s vital to understand what that decision will really cost you. It’s not just about the money you take out today; it’s about the massive, permanent hole it leaves in your future wealth, thanks to the loss of your greatest ally: compound interest.

Imagine your super balance is a tiny snowball at the top of a very long hill. As it rolls, it picks up more snow, getting bigger and bigger, faster and faster. That’s compounding. When you take a chunk out of that snowball early on, you don't just lose that piece of snow. You lose all the future growth that piece would have gathered over the decades.

The Power of Compounding You Sacrifice

Compounding is the engine room of your super. It’s how your investment returns start earning their own returns, creating a powerful snowball effect that turns a modest balance into a comfortable retirement nest egg. Pulling money out early slams the brakes on this process for the amount you withdraw.

The numbers are genuinely shocking. For a 30-year-old, taking out just $20,000 today could leave them with over $70,000 less in retirement. This isn't just a loss of $20,000; it's the loss of 35 years of growth. That money is no longer invested, no longer earning returns, and no longer compounding.

This isn’t just a scare tactic. Research from Australia’s biggest funds backs it up. Analysis by AustralianSuper and Aware Super showed that a 25-year-old who withdrew the maximum $20,000 during a past early release scheme would be around $77,000 poorer at retirement. That’s the initial $20,000 plus a staggering $57,000 in lost investment earnings. You can dig into the full findings of this super withdrawal research to see the full breakdown.

Seeing the Real-World Impact

Numbers on a page can feel abstract, so let's think about what that lost potential actually means for your quality of life. What could that extra $70,000+ give you in retirement?

- A Reliable Car: The freedom to buy a new, safe car without worrying about breakdowns.

- Years of Travel: Funding for those overseas holidays or trips around Australia you’ve always dreamed of.

- Home Renovations: The cash to update your home, making it more comfortable as you get older.

- Peace of Mind: A crucial financial buffer for unexpected medical bills or emergencies.

When you access your super early, you're essentially trading these future comforts for immediate, but often temporary, relief.

The question isn't just "Can I access my super?" but "Should I?" An early withdrawal is a permanent decision that buys short-term relief at the cost of long-term security.

At Wealth Collective, our ‘Retirement Roadmap’ service is built around helping clients harness the power of compounding to build the future they want. Our first priority is always to preserve and grow your savings, not see them diminished under pressure.

Before you make a decision that can't be undone, let's look at the hard numbers for your specific situation. We can map out exactly what an early withdrawal will cost you personally and explore other pathways you might not have considered. A quick, no-obligation initial call can give you the clarity you need to make a fully informed choice.

Applying for Early Release Due to Financial Hardship

When life throws a serious financial curveball, tapping into your super can feel like a lifeline. It’s important to know that while other early release conditions are handled by the ATO, applications based on severe financial hardship go directly to your super fund.

But let’s be clear: the rules are incredibly strict. This isn't a solution for when you're just feeling the pinch or struggling with debt. The government has a very specific, non-negotiable definition of 'financial hardship' to ensure this option is reserved for those in genuine, severe need.

The Two Strict Eligibility Tests

To even be considered for an early super withdrawal, you must meet one of two precise conditions. There's no grey area here; you either fit the criteria, or you don't.

The most common pathway requires you to prove two things:

- You have been receiving eligible Commonwealth government income support payments continuously for at least 26 weeks.

- You are unable to meet reasonable and immediate family living expenses.

That 26-week rule is a hard line. If you've been on payments for 25 weeks and six days, your application will be rejected. The payments must also be continuous, with no breaks.

There is an alternative, though less common. If you have reached your preservation age plus 39 weeks, you may qualify if you were on income support for a total of 39 weeks after reaching that age and aren't currently working.

How Much Can You Actually Get?

Even if you meet the criteria, the amount you can withdraw is tightly controlled. You can access a single lump sum between $1,000 and $10,000 in any 12-month period. Crucially, this is a gross amount, meaning tax will be taken out before it hits your account.

You only get one shot at this per year. You cannot receive more than one payment in a 12-month period, even if your first withdrawal was less than the $10,000 maximum. This makes it vital to accurately calculate what you need before you apply.

The tax rate usually falls between 17% and 22%, including the Medicare levy. In real terms, a $10,000 withdrawal might only leave you with about $7,800 to $8,300 in your pocket. You must factor this into your budgeting.

A Real-World Scenario: Jake the Tradesperson

Let's look at how this plays out. Jake is a 38-year-old self-employed electrician who injures his back and can't work. Once his savings are gone, he applies for and starts receiving the JobSeeker payment.

After 27 continuous weeks on JobSeeker, Jake is falling behind on rent and essential bills. His ute, which he needs for work, requires urgent repairs he can't afford. He decides to look into accessing his super.

Here’s the evidence he needs to gather for his super fund:

- A Q230 or Q251 letter from Centrelink. This is the official document that proves you've been on income support for the required 26-week period.

- Proof of his expenses. Jake gathers overdue rent notices, power bills, and a formal quote for his ute repairs.

- Bank statements. These show his low balance and prove he doesn't have the funds to cover these immediate costs himself.

Jake applies directly through his super fund’s online portal for an $8,000 withdrawal. About two weeks later, his fund approves the application. A few days after that, he receives a payment of $6,560, after $1,440 (18%) in tax was withheld.

While this money helps him catch up on rent and fix his ute, it’s a permanent $8,000 reduction from his retirement savings, plus all the future compound growth that money would have generated.

The process is detailed and unforgiving. At Wealth Collective, our Guided Growth service is designed to build financial security so that raiding your super isn't your only plan. Before you start an application, a brief call with us can bring clarity and help you confirm it's the right and only path forward for you.

Accessing Super on Compassionate Grounds

Beyond severe financial hardship, there's another pathway for accessing your super early: compassionate grounds. This process is handled directly by the Australian Taxation Office (ATO), not your super fund, and it's designed for very specific, urgent situations where you simply don't have any other way to pay.

It’s important to understand this isn't for covering general living costs. The ATO has a strict, narrow list of what qualifies, mostly centred around critical medical care, palliative needs, essential disability modifications, or preventing the bank from foreclosing on your home. The devil is in the detail—and your documentation.

Understanding the Accepted Grounds

To be considered for an early release on compassionate grounds, your circumstances need to fit perfectly into one of the ATO's approved categories. Each one has its own set of tough evidence requirements, and you must prove you can’t cover the expense by other means, like selling assets or using savings.

Here are the main reasons the ATO will consider:

- Medical Treatment or Transport: For you or a dependant, covering treatment that isn't available through the public system.

- Palliative Care: To help with costs for you or a dependant who is terminally ill.

- Disability Modifications: For paying to adapt your home or car to accommodate a severe disability for yourself or a dependant.

- Preventing Foreclosure: To make a payment that stops your lender from selling your main home.

- Funeral Expenses: To pay for costs related to the death, funeral, or burial of a dependant.

The amount you can access is strictly limited to what's reasonably needed for the unpaid expense. For instance, if you require $18,000 for a medical procedure, you can only apply to withdraw that exact amount, plus enough to cover the tax that will be withheld.

Building Your Application The Right Way

A successful application all comes down to the evidence. The ATO needs undeniable proof that the cost is real, necessary, and that you have no other financial capacity to meet it. The most common reason for rejection is incomplete or incorrect paperwork, which can cause heartbreaking delays.

For medical or dental treatment, you'll need reports from two separate registered medical professionals.

- One report from a specialist confirming the condition and explaining why the treatment is essential.

- A second report from any registered medical practitioner (like your GP) that supports the specialist’s assessment.

You'll also need a detailed quote or an unpaid invoice for the exact cost. If you're trying to prevent foreclosure, you must provide a formal letter from your lender, like a default notice, stating they intend to sell your home if the overdue amount isn't paid.

Your application is only as strong as your documentation. The ATO isn’t assessing the emotional weight of your situation; they are legally required to assess how precisely your evidence meets their strict criteria.

A Real-World Scenario: Essential Dental Surgery

Let's walk through a typical example. Maria is a 45-year-old mother whose son needs urgent and complex dental surgery. The procedure isn't covered by Medicare, and their health insurance leaves a massive out-of-pocket cost of $14,500. The family has savings, but not enough to cover the full bill.

Maria decides to apply for an early release of super on compassionate grounds. Here’s how a successful application plays out:

- Gathers Medical Reports: She gets a detailed report from her son’s oral surgeon outlining the necessity of the surgery. She follows this up with a supporting letter from their family GP.

- Obtains a Formal Quote: The surgeon's office gives her a formal, itemised quote for the $14,500.

- Applies via myGov: Maria logs into her myGov account, links it to the ATO, and navigates to the "compassionate release of super" application. She uploads digital copies of the two medical reports and the quote.

- ATO Approval & Fund Release: Two weeks later, she gets a notification in her myGov inbox that her application is approved. The ATO then sends an authority to her super fund to release the money. After tax is withheld, she receives the funds to book the surgery.

This process can feel incredibly daunting, especially when you're already under enormous stress. The team at Wealth Collective can offer clarity and help you understand the requirements before you start. Our Protection Plus service is designed to ensure you have financial safety nets in place, giving you options beyond your super when life throws you a curveball.

Other Legitimate Pathways for Early Super Access

While financial hardship and compassionate grounds are the most common reasons, they aren't the only ones. A few other specific, and equally strict, pathways exist. Each has its own clear-cut purpose and non-negotiable process.

One of the most profound is for those diagnosed with a terminal medical condition. This involves a clear medical diagnosis and allows you to withdraw your entire super balance, tax-free.

At the other end of the spectrum is the First Home Super Saver (FHSS) scheme. This isn't a crisis response, but a proactive strategy for saving a home deposit inside your super. It’s a smart move we often build into our clients' financial plans from day one.

Withdrawing Super for a Terminal Medical Condition

This is, without a doubt, the most serious reason for early super release, and the process reflects that gravity.

To be eligible, you must have two separate registered medical practitioners certify that you have an illness or injury likely to result in your death within 24 months of the certification date. At least one of these doctors must be a specialist in the area related to your condition.

Once your super fund receives and validates these documents, you can withdraw your entire super balance as a tax-free lump sum. This process is handled directly by your super fund to avoid adding unnecessary stress during an incredibly difficult time.

Using the First Home Super Saver Scheme

The FHSS scheme is a forward-thinking way to use your super account to fast-track your first home deposit. It allows you to make voluntary contributions—either before-tax (concessional) or after-tax (non-concessional)—and later withdraw those funds, plus earnings, to buy your first home.

Here's a quick look at the rules:

- You can contribute up to $15,000 in any single financial year.

- The total amount you can withdraw under the scheme is capped at $50,000 plus associated earnings.

The real power of this strategy is the tax benefit. Making voluntary concessional contributions means the money is only taxed at 15% inside super, which is often much lower than your personal income tax rate. It's an excellent wealth-building tool, which is why we frequently integrate it into our 'Guided Growth' service for clients focused on getting into the property market.

Unlike hardship claims, the FHSS scheme isn't about solving an immediate crisis. It's a strategic plan to leverage the tax-effective environment of superannuation to achieve a major life goal faster.

Rules for Temporary Residents Leaving Australia

If you've been working in Australia on a temporary visa and are heading home for good, you can generally claim back the super you accumulated here. This is known as a Departing Australia Superannuation Payment (DASP).

You can apply for a DASP once your visa has expired or been cancelled and you have physically left the country. The withdrawal is taxed, but it ensures you can reclaim the money you earned. The application is typically handled online through the ATO.

It’s worth noting the huge impact early release schemes have had. During a major initiative, Australia's largest funds saw massive outflows. AustralianSuper lost over $2.5 billion, while Hostplus and REST saw withdrawals nearing $1.7 billion each. You can read more about the multi-billion-dollar impact of early super release and how it affected member balances.

Each of these pathways comes with its own rules. As you get closer to retirement, your options shift again. If that’s you, our guide on how to use a transition to retirement pension may be helpful. Navigating these complexities highlights why personalised advice is so important—it ensures you're on the right track for your specific situation.

Why You Need a Financial Adviser in Your Corner

Thinking about dipping into your super early? It's a huge decision, and going it alone is a minefield. A simple paperwork mistake could get your application rejected, causing serious delays when you need the money most.

Even if approved, you could be hit with an unexpected tax bill or do long-term damage to your retirement savings that is hard, if not impossible, to undo.

This is where the conversation needs to shift. It's less about how to get your super out and more about having a solid plan to get your finances back on track. It’s about doing it the right way, with your eyes open to the consequences.

From Crisis Management to Financial Resilience

At Wealth Collective, our job isn't just to put out today's fire. It's about building you a financial future where raiding your super isn't the only move you have left. We focus on building genuine financial resilience so that when life throws you a curveball, you have options. An adviser provides a clear, objective sounding board when you’re under pressure and can’t afford to make a mistake.

For instance, there used to be a belief that Aussies were reluctant to spend their retirement nest egg. But recent research shows that in 2024–25, around 68% of retirees with tax-free accounts are actually withdrawing more than the minimum. This shows a growing confidence in using super to live well, but it all hinges on having a healthy balance to begin with—something an early withdrawal can seriously undermine. You can read more about these findings on Australian retirement spending habits to get the full picture.

A good adviser helps you see the long-term impact. We can model exactly what that withdrawal will cost you in 30 years and, just as importantly, check every other possible avenue first. This could be anything from negotiating with creditors to accessing government benefits you didn't know existed.

Your superannuation should be your last line of defence, not your first. An adviser’s role is to fortify all your other financial defences so your super can be left to do its primary job: funding a great retirement.

Our services are designed to build that financial strength and peace of mind.

- Guided Growth: We map out a personal strategy to build your wealth, fine-tune your investments, and create a proper emergency fund.

- Retirement Roadmap: This is all about maximising your super's growth so it can comfortably support the retirement you're looking forward to.

Finding the right person to guide you is crucial, and our article on how to choose the right financial adviser is a great place to start.

Instead of trying to make such a high-stakes decision on your own, an initial call with our team can provide the clarity you need. Let us help you figure out a path that solves your immediate problem without sacrificing your future.

Common Questions About Early Super Withdrawal

When you're thinking about how to withdraw super early, you're bound to have questions. It’s a complex area, and it's completely normal to feel overwhelmed. Based on our experience helping clients, these are the most pressing concerns that come up time and again.

How Long Does an Early Super Release Application Take?

This is the first thing everyone wants to know, and unfortunately, there's no single answer. The timeline really hinges on why you're applying.

If you’re applying on compassionate grounds, the ATO needs to review your documentation first, which can take a few weeks. Once they approve it, your super fund then needs its own processing time. For severe financial hardship claims, which go straight to your fund, you’re still likely looking at several weeks from start to finish. It's never an overnight process, so it pays to plan for delays.

Will Withdrawing Super Early Affect My Centrelink Payments?

Yes, it almost certainly will. While the lump sum you pull from your super isn't typically treated as "income" by Centrelink, it is counted as an asset.

That sudden increase in your assets can easily push you over the threshold for payments like the JobSeeker Payment or the Age Pension, potentially reducing or even stopping them altogether. Before you apply, you must contact Services Australia to find out exactly how a withdrawal would affect your specific benefits.

Don’t get caught out by a reduced Centrelink payment. This is a common and nasty surprise that can make a tough financial situation even worse. Always check with Centrelink first.

What Are the Alternatives to Withdrawing My Super?

Dipping into your retirement savings should always be your absolute last resort. Before you go down this path, you need to make sure you've exhausted every other possible option.

Here's where you should look first:

- Get Free Financial Advice: Call the National Debt Helpline for a confidential chat with a financial counsellor. They are an incredible resource.

- Talk to Your Lenders: Your bank might have a hardship program that could let you pause or reduce mortgage or loan repayments.

- Find a No-Interest Loan: For essential items like a fridge or car repairs, look into the No-Interest Loan Scheme (NILS).

- Negotiate With Utilities: Call your electricity, gas, and water providers. They all have programs to help customers who are struggling to pay their bills.

Trying to figure all this out on your own, especially when you're under financial pressure, is incredibly difficult. The team at Wealth Collective can help bring clarity to your situation. We’ll walk you through all the alternatives and help you decide on a course of action that solves today’s problems without jeopardising your future. Book a complimentary initial call with us to see how we can help.