Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

For most working Australians, the short answer is a resounding yes—income protection is absolutely worth considering. It’s one of the most crucial financial safety nets you can put in place.

Think of it this way: you insure your house and your car, but what about your single greatest asset? That’s your ability to get up and go to work every day.

Why Your Income Is Your Most Valuable Asset

We insure our homes against fire and our cars against accidents without a second thought. Yet, so many of us overlook the very engine that pays for it all—our salary. This is a massive financial blind spot.

Over your working life, your ability to earn an income could be worth millions of dollars, easily dwarfing the value of your other possessions. Losing that, even for a short while, can send ripples through your entire financial world.

Without that steady pay cheque, simple things like mortgage repayments, groceries, and school fees can suddenly become a huge struggle. This is where the question of whether income protection is worth it becomes crystal clear.

The Financial Domino Effect of Lost Income

Imagine you’re suddenly unable to work for six months because of an unexpected illness or injury. The consequences can stack up frighteningly fast:

- Draining Savings: Your emergency fund, which might have taken years to build, could be wiped out in just a few months.

- Mounting Debt: You might find yourself relying on credit cards or personal loans just to get by, digging a debt hole that’s hard to climb out of.

- Halting Wealth Creation: Contributions to your super and other investments would likely stop, setting your long-term retirement goals back significantly.

- Compromising Your Lifestyle: The financial pressure could force tough decisions, like selling assets or drastically cutting back on your family’s quality of life.

Income protection acts as a financial firewall. It stops a temporary health issue from escalating into a long-term financial disaster by providing a monthly benefit, typically up to 70% of your pre-tax income. This allows you to focus on recovery without the added stress of financial instability.

Before we dive deeper, let's look at a quick overview of the key factors to consider.

Income Protection At a Glance

This table summarises the core elements that help determine if income protection is the right fit for your circumstances.

| Key Consideration | Why It Matters for Your Finances | Who Benefits Most From Coverage |

|---|---|---|

| Your Dependents | The more people rely on your income (spouse, children), the greater the financial impact if it stops. | Sole income earners, families with young children, and those supporting dependents. |

| Occupation & Risk | Some jobs carry a higher risk of injury or illness, which directly impacts your ability to work. | Tradespeople, manual labourers, healthcare workers, and anyone in a physically demanding role. |

| Existing Savings | A small emergency fund won't last long against major expenses like a mortgage. | Individuals with limited savings or whose savings are tied up in non-liquid assets like property. |

| Debt Levels | High levels of debt (mortgage, car loans, personal loans) require consistent income to service. | Homeowners, recent graduates with student loans, and anyone with significant financial commitments. |

| Self-Employed Status | If you're self-employed, there's no sick leave or employer safety net to fall back on. | Freelancers, contractors, and small business owners whose business relies on them to operate. |

Essentially, the more financial responsibility you carry, the more valuable this cover becomes.

At Wealth Collective, our Protection Plus service is designed to help you identify these exact risks. We firmly believe that protecting your income is the foundational step in any successful financial plan. Our process gives you clarity and confidence, ensuring your goals aren't derailed by the unexpected.

Before you can grow your wealth, you have to protect its source. Booking a quick, no-obligation call with our team is the first step towards securing your financial future.

How Income Protection Actually Works

If you want to figure out whether income protection is worth it, you first need to see it for what it is: a financial backup generator for your life. Think about it—your ability to earn an income is the main power source for your entire financial world. If an unexpected illness or injury suddenly cuts that power, income protection is designed to flick on automatically, restoring the flow and stopping your life from grinding to a halt.

It's not an overly complicated system, but it does have a few key parts that control how it functions. Getting your head around these is crucial to understanding how this insurance can provide a reliable financial lifeline right when you need it most. It’s this structure that makes it such a powerful tool for protecting your lifestyle and future plans.

Let's break down the three main dials you can adjust to control how your policy works.

The Benefit Amount: Your Monthly Pay Cheque

First up, and probably the most important, is the benefit amount. This is the monthly payment you'll receive while you're off work.

Here in Australia, insurers will typically let you cover up to 70% of your pre-tax income. That 70% cap isn't just a random number; it's a regulated industry standard designed to give you a clear incentive to get back to work once you've recovered.

This benefit becomes your replacement salary, and it’s there to cover all those essential living costs, like:

- Your mortgage or rent payments

- Utility bills and groceries

- School fees for the kids

- Any ongoing medical or rehab costs

The whole point is to keep your finances stable so you can put all your energy into getting better, without the added stress of worrying about how the bills will get paid.

The Waiting Period: The Countdown to Your First Payment

Next, we have the waiting period. You might also hear this called the deferred period. Put simply, it’s the time between when you have to stop working and when your first insurance payment lands in your bank account.

You get to choose this waiting period when you first set up the policy. Common options are 30, 60, or 90 days, though some policies offer shorter or longer periods. A longer waiting period means you’ll need to rely on your own funds—like sick leave or your emergency savings—for a bit longer, but the trade-off is that it brings your premium down.

Choosing the right waiting period is a bit of a balancing act. It’s all about lining up your policy with the financial buffers you already have. A shorter period gets you paid faster but costs more, while a longer one is more affordable if you have enough savings to bridge the initial gap.

At Wealth Collective, our Protection Plus process always involves a thorough look at your sick leave and savings. This lets us recommend a waiting period that’s perfectly matched to your situation, so you’re never left in a vulnerable position.

The Benefit Period: How Long Payments Can Last

The final piece of the puzzle is the benefit period. This sets the maximum length of time you can receive payments for any single claim.

Typically, you can choose a benefit period of two or five years, or one that lasts right up until a specific age, like 65 or 70. A policy that pays out until retirement age offers the most comprehensive, long-term protection against a disability that could end your career. On the other hand, a shorter benefit period can be a more budget-friendly choice.

This decision directly shapes how strong your financial safety net is. A two-year period might be enough to cover your recovery from a serious injury, but a longer period is what protects you from a chronic illness that could stop you from ever going back to your old job.

To see how all these moving parts fit together, you can find out more about what income protection insurance in Australia covers in our detailed guide. Making a smart decision really starts with understanding these fundamentals and how they can be set up to protect your most important asset.

The Real-World Risks Income Protection Actually Covers

It's a common myth that income protection is only for some dramatic, career-ending accident. This kind of thinking makes it easy to dismiss, leaving many people wondering if it's really worth it for them. But the truth is, the most common reasons people claim are far more ordinary and relatable than you might imagine.

This insurance isn't just a 'worst-case scenario' plan. It’s designed to cover the genuine, statistically common health issues that can stop anyone from earning a living. Everyday illnesses and injuries are actually the most frequent triggers for needing extended time off work.

The Most Common Reasons For Claims

If you look at the data from Australian insurers, a very clear picture emerges. The need for income protection is often driven by surprisingly common conditions, which really challenges that "it'll never happen to me" mindset. Many policies are claimed on not because of a single, life-altering event, but due to health issues that suddenly or gradually disrupt a person’s ability to work.

For example, the single biggest category for claims is accidents. Recent life insurer statistics show that accidents account for 16% of all income protection claims, making them the leading cause of time off. This could be anything from a slip on a worksite to a car crash on the way to the shops.

Right behind that, mental health conditions and musculoskeletal disorders (like severe back pain) each make up another 8% of claims. You can explore the full breakdown of claim statistics to see just how wide-ranging the covered conditions are.

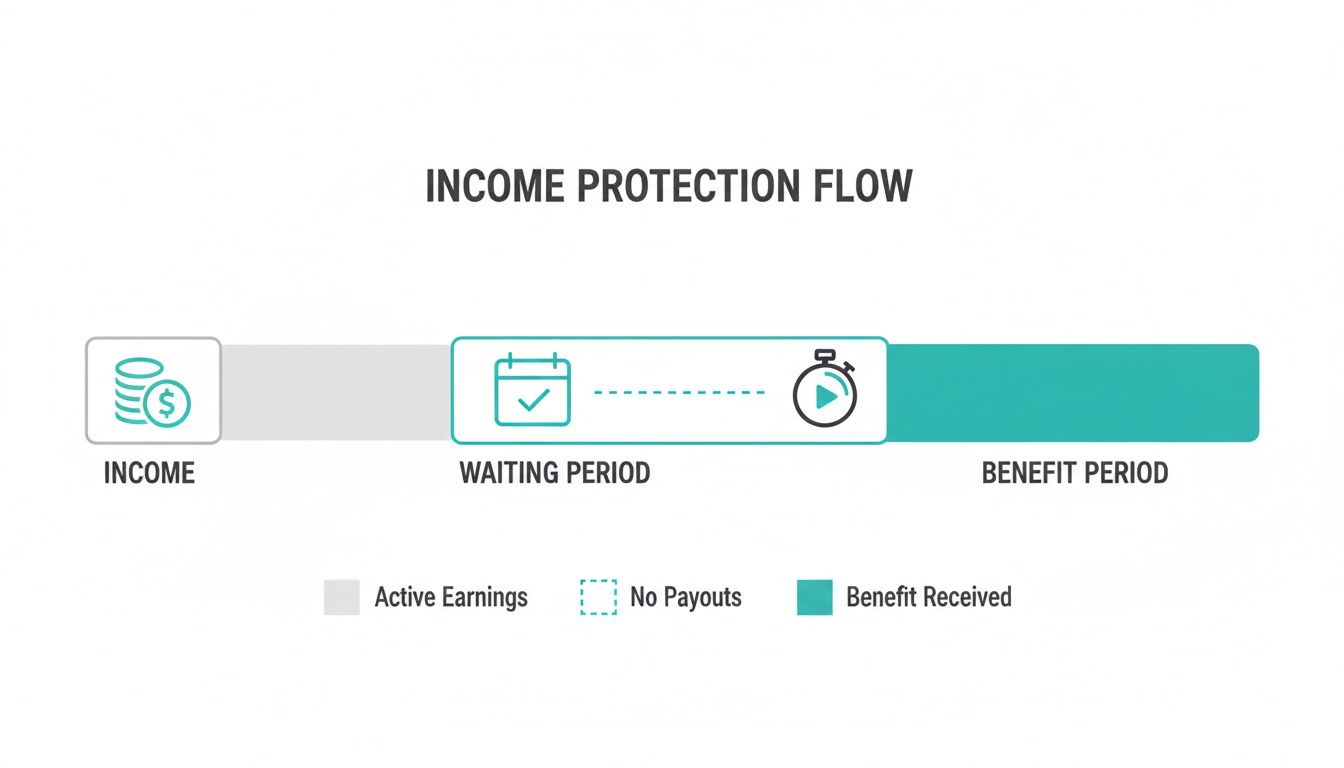

This diagram shows the simple but powerful flow of how income protection works to support you financially.

It maps out the journey from earning your salary to activating that financial safety net after the waiting period, ensuring your income stream continues when you need it most.

The main takeaway here is simple: you're statistically more likely to need income protection for a common ailment like a bad back, severe stress, or a broken bone than for a rare, catastrophic illness.

Understanding this helps shift the conversation from a distant "what if" scenario to a practical risk management strategy. It’s a tool built for the probable, not just the barely possible.

Protection For More Than Just Physical Injury

It’s so important to realise that income protection covers a whole spectrum of health issues, including those that aren't immediately visible. In fact, mental health is one of the fastest-growing categories for claims in Australia today.

Conditions like severe anxiety, depression, and burnout are legitimate medical reasons that can stop someone from doing their job, and a well-structured policy is designed to provide cover for them.

This broad scope really highlights the true value of income protection. It covers things like:

- Musculoskeletal Issues: This includes chronic back pain, joint injuries, and other physical conditions that can make either a desk job or manual labour impossible.

- Serious Illnesses: Cancer, heart conditions, and strokes are also significant causes for claims, often requiring long and difficult recovery periods.

- Mental Health Conditions: This acknowledges that your ability to work is tied to both your physical and psychological wellbeing.

Of course, it's just as important to know what isn't covered. For a complete picture, you can learn more about what income protection does not cover in our other guide.

At Wealth Collective, our Protection Plus service is designed to assess these real-world risks against your specific life and career. We don’t just find you a policy; we help you understand the genuine threats to your income and build a solid defence against them. By starting with a free, 10-minute initial call, we can bring clarity to how this cover addresses the risks you face every day, ensuring your financial plans stay on track.

Does Income Protection Actually Pay Out?

It’s one of the biggest questions people have about any kind of insurance, and it’s a fair one: will the insurer actually pay up when I need them?

This is a huge hurdle for many. You’re putting your hard-earned money into a policy month after month, trusting that it will be there for you if things go wrong. The last thing you want is to find out your safety net has a hole in it, right when you're falling.

Many people worry that insurance companies are experts at finding loopholes and using the fine print to wriggle out of paying claims. This fear alone stops a lot of folks from even considering income protection. But when you look at the actual data here in Australia, a much clearer—and more reassuring—picture emerges.

The Proof is in the Payouts

Let's cut straight to the chase. The vast majority of income protection claims are paid. Insurers provide a critical financial lifeline to thousands of Australians every single year, and the statistics back this up.

The Australian Prudential Regulation Authority (APRA) keeps a close eye on these things. Their latest data shows the industry-wide claims acceptance rate for advised income protection policies is an impressive 94.4%.

This isn't a recent fluke, either. That figure has consistently hovered between 95% and 96% for the better part of a decade, showing a solid track record of reliability. You can see the full picture of Australian life insurance claims statistics for more detail.

And the support comes through quickly. On average, it takes just 1.6 months for a claim to be accepted, meaning that financial relief arrives when you need it most.

How a Financial Adviser Makes All the Difference

While the overall stats are strong, trying to handle a claim yourself when you’re sick or injured is the last thing you need. It can be complex, stressful, and overwhelming. This is where having a professional on your side becomes absolutely invaluable.

An adviser is much more than just someone who sells you a policy. They become your advocate.

At Wealth Collective, our job starts with making sure your application is rock-solid from day one, which minimises any potential hiccups later. But more importantly, if you ever have to make a claim, we step in and manage the entire process. We deal with the insurer, chase the paperwork, and make sure everything is done right.

This isn't just about reducing your stress levels (though that's a huge part of it). It's about getting a better outcome. We know the ins and outs of policy definitions and the claims process, and we fight to ensure you get every dollar you're entitled to.

The Wealth Collective Advantage When You Need to Claim

Picture this: you've just received a serious diagnosis. Your world is spinning, and your focus needs to be on your health and your family. The last thing you have the energy for is spending hours on hold with an insurer or trying to decipher complicated forms.

Our Protection Plus service was designed specifically to lift this weight from your shoulders. When you're a Wealth Collective client, this is what making a claim looks like:

- You make one phone call. That's it. Just one call to us.

- We take over completely. We liaise with the insurance company, your doctors, and anyone else involved to get the information needed.

- You get regular, simple updates. We keep you in the loop without bogging you down, so you can focus 100% on getting better.

This is the real, tangible benefit of getting professional advice. It turns your policy from a piece of paper into a fully supported financial backstop. You’re not just buying insurance; you're securing true peace of mind.

Ready to build a financial plan with protection you can truly count on? Start with a free 10-minute introductory call to see how we can help.

How To Find Value And Navigate The Cost

Deciding you need income protection is one thing, but figuring out how to get great value without breaking the bank is a whole other ball game. The price you pay for a policy—your premium—isn’t just a number plucked from thin air. It’s carefully calculated based on who you are and the level of protection you want.

Think of it like tuning a high-end sound system. Every dial you adjust, from your occupation to the waiting period, changes the final output. In this case, that output is your premium. The goal isn't to find the cheapest policy, because that's almost always a bad move. True value comes from finding cover that's both affordable and strong enough to actually be there for you when you need it most.

Let's break down the main dials you can turn to get the cost and coverage just right.

The Key Factors Driving Your Premiums

A handful of key elements come together to set your monthly premium. Knowing what they are helps you see where you have some control and how your personal situation comes into play.

- Your Age: It’s a simple fact that younger people get lower premiums. Insurers see you as less of a risk, so locking in a policy while you're young and healthy can save you a serious amount of money over the long haul.

- Your Health and Lifestyle: Your medical history, whether you smoke, and your general lifestyle all go under the microscope. Any pre-existing conditions or habits like smoking will usually mean you pay a bit more.

- Your Occupation: What you do for a living is a huge factor. An office-based accountant simply faces less day-to-day risk than a carpenter on a construction site, and the premiums will reflect that.

- Waiting Period: This is the time you have to wait between stopping work due to illness or injury and when your insurance payments kick in. A longer wait, say 90 days, means a lower premium compared to a shorter 30-day period.

- Benefit Period: This dictates how long the policy will pay you for a single claim. A policy that pays right up until you turn 65 offers the ultimate safety net, but it will naturally cost more than a policy that only pays for two or five years.

For most people, adjusting the waiting and benefit periods is the most direct way to tailor a policy to fit their budget. You're essentially trading off short-term self-sufficiency against long-term cost.

The table below gives you a clearer picture of how these choices play out.

How Your Policy Choices Impact Your Premiums

A great way to get a handle on this is to see the cause and effect of adjusting your policy's structure.

| Policy Feature | Your Adjustment Choice | Typical Impact on Premium | Who This Strategy Is Best For |

|---|---|---|---|

| Waiting Period | Lengthening it from 30 days to 90 days. | Lowers your premium significantly. | Individuals with a solid emergency fund or several months of sick leave to bridge the initial gap. |

| Waiting Period | Shortening it from 90 days to 30 days. | Increases your premium but provides faster access to funds. | People with limited savings, the self-employed, or those with high ongoing expenses who can't afford a long delay. |

| Benefit Period | Shortening it from 'To Age 65' to five years. | Reduces your premium by limiting the insurer's long-term risk. | Younger individuals on a tighter budget who still want a strong level of medium-term protection. |

| Benefit Period | Lengthening it from five years to 'To Age 65'. | Increases your premium for the most comprehensive protection. | Sole income earners, those with significant debts like a mortgage, or anyone wanting maximum long-term security. |

By strategically choosing these periods, you can find a sweet spot that delivers the right level of protection for a price you can manage.

Why The Cheapest Policy Is A False Economy

It’s always tempting to grab the cheapest option on the market, but this is often a huge mistake. The real value of an income protection policy is buried in the fine print—specifically, in the policy definitions. These definitions spell out exactly what it means to be "unable to work," and they can be the difference between getting paid and having your claim denied.

A cheaper policy might have tough, restrictive definitions that make it incredibly difficult to make a successful claim. That kind of policy is practically useless. This is where getting professional advice isn't just a nice-to-have; it's essential.

At Wealth Collective, our Protection Plus service is designed to cut through this complexity. We don’t just shop for a price; we dive deep into the policy definitions from different insurers to find you high-quality cover that actually fits your budget. We know exactly how to balance the levers of cost and coverage to deliver real, dependable value. We'll even explore different ownership structures, like looking at holding income protection inside your superannuation, to see if that's the right move for you.

Our expertise means you’re not just buying an insurance policy—you’re securing a promise you can actually count on. It all starts with a simple, no-obligation chat to figure out what you truly need to protect.

Making Your Decision and Taking the Next Step

So, we've walked through how income protection works, the real-world risks it covers, and the strong chance of a successful payout. Now, it all boils down to one personal question: is it actually worth it for you? Answering that means taking an honest look at your own financial situation.

The best way to get a clear answer is to ask yourself a few simple but powerful questions. This isn't about getting lost in spreadsheets; it's about figuring out how strong your personal safety net really is.

A Simple Checklist to Assess Your Need

Grab a notepad and think through these points. Your answers will quickly show you where you might be financially exposed.

- Who depends on your income? Think about your partner, kids, or anyone else you help support. The more people who rely on you, the more crucial a backup plan becomes.

- How long would your savings last? Tally up your essential monthly bills (rent/mortgage, utilities, food) and see how many months your savings would cover. Is it just a few weeks, or do you have a buffer of several months?

- What does your employer provide? Do you know exactly how much sick leave you have saved up? Would your work keep paying you for three, six, or twelve months if you couldn't work? For most of us, this support runs out surprisingly fast.

- What are your major debts? Your mortgage, car loan, and other debts don't just pause because your income does. Keeping up with those repayments is essential to protecting your assets.

If working through this list reveals a gap between what you owe and what you have, then exploring your options is the logical next step.

The Value of Expert Guidance

While it’s true that insurance claims acceptance rates in Australia are high, trying to navigate the system on your own can be tough. The data shows that while over 94% of claims are paid, the number of people disputing decisions has more than doubled, rising from 124 per 100,000 insured lives in 2018 to 289 recently. The interesting part? Claims lodged with the help of an adviser consistently get better results. You can read the full data insights on insurance claims to see the trends for yourself.

This highlights a crucial point: having a professional advocate in your corner isn’t just about convenience; it tangibly improves your chances of a smooth, successful claim when you're at your most vulnerable.

At Wealth Collective, our Protection Plus service is designed to remove the stress and complexity from this whole process. We don't just sell you a policy; we help you build a financial fortress.

It all starts with a free, no-obligation 10-minute introductory call. It’s just a simple chat for us to understand your situation and show you how we can help secure your financial world. No friction, no pressure—just clear, practical guidance.

Book Your Free 10-Minute Call Today and take the first confident step toward protecting your most valuable asset.

Got Questions? Let's Get Them Answered.

It's completely normal to have a few questions when you're looking into personal insurance. Getting clear on the details is how you make a smart decision. To help, we’ve put together straight answers to some of the most common things people ask us about income protection.

Are Income Protection Premiums Tax Deductible in Australia?

Yes, for the most part, they are. When you hold an income protection policy in your own name (i.e., outside of super), the premiums you pay are generally tax-deductible. This is a massive plus, as it can seriously bring down the real cost of having the cover in place.

The rules change if your policy is inside your super fund, though. In that case, you can't claim the premiums as a personal tax deduction. This is a perfect example of why getting the structure right from the start is so important.

What’s The Difference Between Income Protection and TPD Insurance?

This is a great question. While they both deal with being unable to work, they kick in for very different reasons and pay out in different ways. They’re designed to work together, not replace each other.

- Income Protection: Think of this as your replacement paycheque. If an illness or injury stops you from working temporarily, it pays you a monthly benefit to cover the bills while you recover.

- Total and Permanent Disability (TPD) Insurance: This is for a worst-case scenario. TPD pays a one-off, tax-free lump sum if you suffer a life-altering disability and doctors agree you're unlikely to ever work again.

So, income protection is for the temporary setbacks, keeping your life on track during recovery. TPD provides a significant financial base to reshape your future after a permanent, career-ending event.

Can I Get Income Protection If I'm Self-Employed?

You absolutely can, and frankly, it's something every self-employed person should consider. When you're the boss, there's no sick leave or annual leave to fall back on. If you can't work, the income often stops dead.

Insurers have policies specifically for business owners and sole traders, but proving your income can be a bit more involved than it is for a PAYG employee. This is where getting good advice really pays off.

For business owners, the right advice ensures your policy is set up to reflect your unique financial situation. It’s about building a safety net that protects not just your family's finances, but the business you've worked so hard to build.

This is exactly what our Protection Plus service at Wealth Collective is designed for. We help our self-employed clients get all the right paperwork in order and make a rock-solid application, so you know your cover is secure from day one.

Hopefully, that clears a few things up. But the best answers are always the ones that apply directly to you.

The next step is simple. At Wealth Collective, we start with a free, no-pressure 10-minute chat to see if we can help you build the right financial protection. Book your call today through our website at https://wealthcollective.co.