Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Income protection held in your superannuation is a bit like having a financial safety net built right into your retirement savings. The idea is simple: if you get sick or injured and can’t work for a while, this insurance steps in to replace a chunk of your paycheque. Most Australians actually have a basic level of this cover automatically included in their super fund, with the premiums conveniently paid straight from their super balance. The catch? This default cover is often nowhere near enough to cover your actual living expenses.

Understanding Your Default Superannuation Cover

Think of the automatic income protection in your super fund as a generic, one-size-fits-all raincoat. It’s better than getting caught in a downpour with nothing, but it’s probably not going to be the perfect fit when a real storm hits. This “default” cover is given to members without any medical checks, up to a certain level called an Automatic Acceptance Limit (AAL). While that sounds easy, the convenience comes with some serious downsides.

The whole point of income protection is to make sure you can keep paying the mortgage, the bills, and the groceries while you’re focused on getting better. It provides a monthly income stream so you don’t have to raid your savings or, worse, your retirement nest egg. If you’re new to the concept, you can get a great overview in our guide on what superannuation is in Australia.

The Hidden Dangers of Default Insurance

Relying on the ‘off-the-shelf’ income protection that comes with your super fund can feel like a smart move. It’s automatic, it’s convenient, and the premiums are paid without you ever seeing a bill. But this convenience often masks a serious problem: default insurance is a one-size-fits-all product, which means it rarely fits anyone perfectly.

This kind of cover, often called Automatic Acceptance, has some significant built-in limitations. These shortcomings can leave you and your family dangerously exposed right when you need financial support the most. It’s a huge gamble to just assume this basic cover is enough to protect your income and lifestyle.

Now, it’s not all bad news. On the whole, the insurance industry is paying claims. Recent data shows that income protection claims made through group super funds had an impressive 96.3% acceptance rate. Better yet, the average claim was processed in just 1.4 months. You can discover more insights about the success of insurance in superannuation.

But here’s the catch: a high acceptance rate doesn’t mean the policy itself is any good. The real danger is buried in the fine print—the specific terms and conditions that dictate how much you get paid, for how long, and under what circumstances.

The Problem of Inadequate Payouts

One of the most common traps with default super cover is a low monthly benefit. These policies usually cap the benefit amount. On paper, it might look okay, but for many people—especially higher-income earners—it often covers only a small fraction of their actual salary.

Imagine you earn $150,000 a year, but your default cover is capped at a benefit that only replaces an income of $60,000. That leaves you with a massive shortfall. You’d be forced into a drastic and immediate lifestyle change, creating immense financial stress right on top of the health challenge you’re already facing.

A policy that doesn’t align with your real earnings isn’t a safety net; it’s a false sense of security. You’re paying for protection that won’t actually protect your way of life.

Long Waiting Periods and Short Benefit Periods

Beyond the payout amount, two other critical factors often make default cover fall short: the waiting period and the benefit period.

- The Waiting Period: This is the time you have to be off work before your payments can even start. Default policies often have long waiting periods of 60 or even 90 days. Three months is a long time to go without an income, forcing many to burn through their savings or rack up debt just to get by.

- The Benefit Period: This determines the maximum length of time you can receive payments. A huge red flag with many default policies is a short benefit period, often just two years. That’s completely inadequate for a serious illness or injury that could stop you from working for many years, or even permanently.

This combination of a long wait to get paid and a short window of support creates a very precarious situation for anyone facing a significant health crisis.

The Risk of Pre-Existing Condition Exclusions

Another landmine buried in the policy documents is the exclusion for pre-existing medical conditions. Default group policies can be particularly strict about this. If you had a health issue before your cover started—even one you weren’t fully aware of—any claim related to that condition could be denied.

For instance, a later-in-life diagnosis of a condition like Autism Spectrum Disorder (ASD) can be tricky. While the diagnosis is new, the condition itself is pre-existing. An insurer might use this to dispute a claim, even if it’s related issues like anxiety or burnout that are actually preventing you from working.

It’s crucial to read the insurance guide and Product Disclosure Statement (PDS) in detail, but let’s be honest, these documents are often complex and filled with legal jargon. This is where getting professional advice is so valuable.

A generic, off-the-shelf policy provides a basic level of cover, but it’s rarely enough for your specific circumstances. A tailored policy, on the other hand, is designed around you.

The table below gives you a clearer picture of the differences.

Default Group Cover vs Tailored Personal Policy

| Feature | Default Cover in Super (Typical) | Tailored Policy (Advised) |

|---|---|---|

| Assessment | No underwriting (automatic acceptance). | Full medical and financial underwriting upfront. |

| Benefit Amount | Capped at a low, fixed amount or basic formula. | Based on 70% of your actual pre-tax income. |

| Benefit Period | Often limited to just 2 years. | Can be set to 5 years or to age 65. |

| Waiting Period | Usually fixed at 60 or 90 days. | Flexible options (30, 60, 90 days) to suit your savings. |

| Exclusions | Broad exclusions, especially for pre-existing conditions. | Exclusions are clearly defined and agreed upon at application. |

| Portability | Cover is tied to your super fund; may cease if you change jobs. | Fully portable; you own the policy, regardless of your employer. |

| Customisation | Very limited or no options for customisation. | Highly customisable with optional extras for specific needs. |

As you can see, relying on default cover can leave significant gaps in your financial protection.

At Wealth Collective, our Protection Plus service is designed to uncover these hidden risks. We meticulously review your existing default cover, comparing it against your income, expenses, and goals. We identify the gaps and then build a clear, actionable strategy to ensure your superannuation income protection truly protects you. Don’t leave it to chance—Book a complimentary initial call with our team to ensure your financial safety net is strong enough to catch you.

Comparing Insurance Inside vs Outside Super

Deciding where to hold your income protection is one of those big financial choices that can have lasting consequences. You’ve got two main paths: holding it inside your superannuation fund or taking out a standalone personal policy. Each option has its own set of rules, benefits, and drawbacks, and getting your head around the differences is the key to building a financial safety net that will actually be there when you need it.

Having income protection inside your super is a popular choice, and for good reason. The premiums get paid directly from your super balance, which is a massive plus for your day-to-day cash flow. Because the money isn't coming out of your personal bank account, it doesn't sting as much, and it helps ensure your cover stays active as long as you have enough in your super account.

But this convenience can come at a steep price, one that’s often buried in the fine print of the policy.

The Problem with Default Super Cover

The "off-the-shelf" cover that many super funds automatically include is a classic case of getting what you pay for. It provides a very basic layer of security, but it's often riddled with limitations that can leave you dangerously exposed when you can least afford it. Default policies aren't designed for you; they’re built for the ‘average’ fund member, which means they’re rarely adequate for anyone’s specific situation.

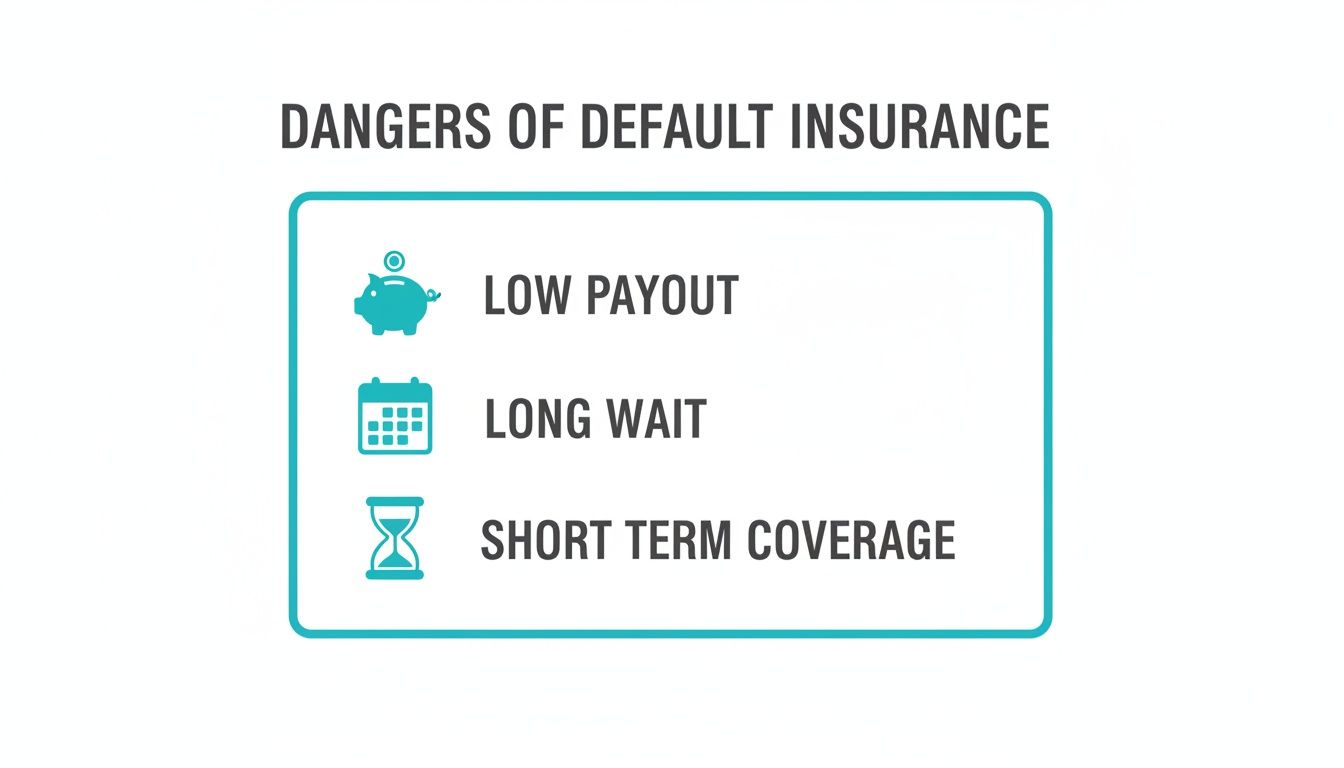

This image highlights some of the most common—and frankly, dangerous—limitations of relying only on default cover.

As you can see, the combination of a low payout, a long wait to receive any money, and a short payment window can create a perfect storm of financial hardship right when you're dealing with a health crisis.

These limitations typically include:

- A Low Monthly Benefit: Default cover often only replaces a small fraction of your real income, which is a huge problem for higher earners. This can force you and your family into immediate and drastic lifestyle changes.

- A Long Waiting Period: You could be waiting 60 or even 90 days after you stop working before you see your first dollar. That's up to three months of trying to get by with no income.

- A Short Benefit Period: Many default policies will only pay out for a maximum of two years. This is nowhere near enough if you suffer a long-term illness or an injury that stops you from working for many years, or even permanently.

Relying on default cover is like taking a rowboat into the open ocean. It might keep you afloat in calm waters, but it won’t save you when a real storm hits.

The Advantages of Policies Outside Super

This is where a personal policy held outside super really comes into its own. Yes, you have to pay the premiums from your own pocket, but in return, you get a huge amount of control, flexibility, and certainty. For many people, especially those in specialised professions or with higher incomes, these benefits are simply non-negotiable.

One of the biggest advantages is the ability to lock in a more comprehensive definition of disability, such as an 'own occupation' definition. This means the policy will pay out if you're unable to perform the specific duties of your own job, rather than any job you might be suited for. It’s a critical distinction for a surgeon, a skilled electrician, or any professional whose career depends on specific physical or mental skills. For those thinking about taking more control of their super, understanding the pros and cons of a self-managed super fund offers more insight into managing your financial future proactively.

On top of that, the premiums for personal income protection policies held outside super are generally tax-deductible, which can significantly lower the real cost of your cover.

At The Wealth Collective, our Protection Plus service always starts with a deep dive into what you currently have. We’re trained to spot these exact gaps and limitations in your default super insurance. From there, we design a smart strategy—often using a mix of cover inside and outside super—to make sure you’re properly protected without paying for things you don’t need.

Don't wait until it's too late to discover your cover isn't up to scratch. Book a complimentary initial call with our team to get clarity and confidence in your financial safety net.

Navigating the Claims Process

Lodging an insurance claim can feel like a massive undertaking, especially when you’re already dealing with your health. But the good news is that it’s usually more straightforward than people imagine. With a bit of preparation, you can get through it and access the benefits you're entitled to.

There's a persistent myth that insurers are always looking for ways to avoid paying out. In reality, the Australian system is quite solid. The latest industry data shows that 96.3% of group superannuation income protection claims get paid, and the average claim is finalised in just 1.4 months. That’s a reassuring statistic for anyone relying on this cover. You can discover more insights about the success of insurance in superannuation.

By understanding what's involved, you can turn what seems like a daunting process into a series of clear, manageable tasks.

Your First Steps After Stopping Work

The minute you know an illness or injury is going to keep you out of work, your first call should be to your super fund. This one phone call gets the ball rolling. They'll confirm that your insurance is active and send you the claim forms you need to begin.

Next, make sure you see your doctor or specialist. Their medical report is the absolute foundation of your claim. They will need to certify that your condition is what's stopping you from working, so having this professional medical evidence locked in from day one is critical for a smooth process.

Gathering Your Documentation

With the forms in hand, your next job is to pull together all the necessary information. This is where a little bit of organisation goes a long way. The insurer needs to verify who you are, what your medical situation is, and what you were earning before you had to stop work.

You’ll typically need to supply:

- Proof of Identity: Your driver’s licence or passport will usually do the trick.

- Medical Reports: This is the detailed statement from your doctor that explains your diagnosis and why it prevents you from doing your job.

- Financial Records: Payslips, tax returns, or even a letter from your employer are needed to prove your income.

It’s really important to be thorough here. One of the biggest reasons claims get held up is because of missing or inconsistent information.

Think of the claims process not as a battle, but as a collaboration. The insurer needs specific information to meet their obligations, and providing it clearly and completely helps them help you faster.

The Insurer's Assessment and Decision

Once you’ve submitted everything, a claims assessor takes over. Their job is to review all your documents and check them against the terms of your policy. They'll look at your doctor’s reports to see if your situation meets the policy’s definition of disability, and they’ll use your financial records to calculate your monthly benefit.

Sometimes, the insurer might ask for more information or an independent medical examination if anything is unclear. This might sound a bit intimidating, but it's a standard part of their process to ensure everything is correct. Once they have everything they need, they will make a formal decision on your claim.

If approved, you’ll get a letter confirming your benefit amount and when you can expect your first payment. Navigating all of this can be stressful, which is why having support like our Protection Plus service makes a real difference. We guide our clients through every stage, handling the paperwork so they can focus on what matters most—their recovery. To see how we can simplify your financial protection, book an initial call with us.

Tailoring Your Cover for Every Life Stage

Your financial safety net isn't something you can set and forget. Life and work are always changing, and your protection needs to keep up. The income protection cover that suits a young professional just starting out will fall dangerously short for a high-income earner with a family, and it’ll look different again for someone on the home stretch to retirement. A smart strategy for income protection inside super is one that grows and adapts right alongside you.

Let's face it, super has become the bedrock of retirement for most Australians. Recent figures from the ABS show the number of retirees who count on super as their main source of income has crept up from 33% to 35%, and that trend isn't slowing down. You can see the data for yourself and understand why protecting your ability to earn—and contribute—is so incredibly important.

That's why a one-size-fits-all approach just doesn't work. We believe in building a plan that’s tuned to your specific life stage, making sure your safety net is always strong enough for whatever comes your way.

For Young Professionals

When you're early in your career, your biggest asset is time. Locking in a high-quality income protection policy while you're young and healthy is one of the shrewdest financial moves you can make. Your premiums will likely be at their lowest, and you’ve got a much better chance of getting covered without any frustrating medical exclusions.

This isn’t just about protecting what you earn today. It’s about ring-fencing your entire future earning potential. A serious illness or accident at this point could throw decades of financial progress off course before it even gets going.

- Your Goal: Lock in comprehensive cover at a great price.

- Key Strategy: Don't just settle for default super cover. Look for a policy with an 'own occupation' definition and a benefit period that lasts right up to age 65.

- Next Step: Getting a professional to review your options can help you find a policy that can scale with your career, so you aren't left underinsured when you start earning more.

For High-Income Earners

If you’re a high-income earner, relying solely on the default income protection in your super fund is a massive financial gamble. The automatic cover most funds provide is usually capped at a level that won’t come close to maintaining the lifestyle you’ve worked hard to build. A monthly benefit that barely covers the mortgage, let alone school fees and other bills, is a recipe for serious stress.

For established professionals, default cover isn't a safety net—it's a false sense of security. The gap between what it pays and what you need can be enormous.

Your main focus should be on supplementing that basic cover to make sure your benefit amount truly reflects up to 70% of your pre-tax income. This often means getting a tailored policy outside of super that you can tweak to fit your exact needs, protecting both your family's lifestyle and your long-term wealth goals.

For Small Business Owners

When you run your own business, your personal and business finances are usually tangled together. If you can't work, it doesn't just cut off your household income—it can put the entire business at risk. This makes income protection an essential tool for both personal security and business survival.

A solid policy ensures your personal bills get paid, stopping you from having to bleed the business dry just to get by. Some policies even have features that can help cover fixed business expenses while you’re out of action, giving your business the breathing room it needs to stay afloat until you’re back on your feet.

For Pre-Retirees

As you get closer to retirement, your financial focus naturally shifts from growing your wealth to protecting it. A sudden illness or injury in your last few working years can be devastating. It could force you to start drawing down on your retirement nest egg years ahead of schedule, which could permanently lower your standard of living in retirement.

At this stage, the goal is to make sure your income protection is strong enough to shield your super balance from any last-minute hits. For those exploring what this phase of life looks like, our guide on transition to retirement pensions offers some really helpful context. It's also the perfect time to review your waiting period and benefit period to make sure they line up with your remaining time in the workforce.

At Wealth Collective, our Protection Plus service is designed to do exactly this—align your cover with your life stage. We dig into your specific situation and build a strategy that provides real security. Book a complimentary initial call with our team to make sure your protection plan is perfectly matched to where you are today and where you want to be tomorrow.

It’s Time to Take Control of Your Financial Future

We've walked through the ins and outs of income protection inside super, and one thing should be crystal clear: while the default cover your fund gives you is a decent safety net, it's often not strong enough to truly catch you if you fall.

You've seen how the common pitfalls of being underinsured—like shockingly low monthly benefits, long waiting periods, and benefit periods that run out far too soon—can leave you and your family in a tough spot. A one-size-fits-all policy just doesn't cut it when your personal circumstances are unique. The good news? A strategy built around your life provides powerful, reliable protection.

Now's the moment to shift from being a passive policyholder to the active architect of your own financial security. Making this change is the single most important thing you can do to shield your lifestyle, support your family, and protect your hard-earned retirement savings from life's curveballs. And getting started is easier than you probably think.

Peace of mind doesn't come from hoping you're covered; it comes from knowing you are. A proactive review is the bridge between uncertainty and confidence.

This is exactly why we created our Protection Plus service at Wealth Collective. A simple, no-obligation chat with one of our advisers can quickly uncover where the real gaps in your cover are. From there, we can map out a clear, practical plan to give you genuine financial security.

This isn't just about ticking an insurance box. It’s about making sure your life goals and your family's future are secure, no matter what happens. Your ability to earn an income is your greatest asset—don't leave its protection to chance.

Take the first step today. Book a complimentary initial call with our team and let's build a financial safety net that gives you complete confidence.

Frequently Asked Questions

Getting your head around income protection inside super can bring up a lot of questions. Let's tackle some of the most common ones we hear from clients, breaking them down into simple, practical answers.

Can I Claim a Tax Deduction for Premiums Paid Through Super?

This is a really common point of confusion. The short answer is no, you personally can't claim a tax deduction for the premiums your super fund pays on your behalf.

But here’s the upside: your super fund itself can usually claim a tax deduction for the cost of providing that insurance to its members. This often means the fund can pass those savings on to you in the form of lower premiums, which is why cover inside super can feel quite affordable. It's a different story for policies held outside super, where you typically can claim the premiums as a personal tax deduction.

What Happens to My Cover if I Change Jobs or Super Funds?

Changing jobs doesn't automatically affect your cover. As long as your super account stays open and has enough money to cover the premiums, your insurance continues as normal. It’s tied to your super fund, not your employer.

The tricky part comes when you switch super funds. Your insurance policy does not automatically move with your super balance when you roll it over. You'll need to cancel the old policy and apply for a completely new one with your new fund, which might mean going through the whole medical assessment process again.

Crucial Tip: Always get your new cover fully approved and in place before you even think about cancelling your old policy. The last thing you want is an unintentional gap in your cover, leaving you exposed.

How Much Income Protection Cover Do I Actually Need?

There’s no magic number here; the right amount is completely unique to your life. To figure it out, you need to look at the big picture: what's your regular income, what are your non-negotiable monthly expenses (mortgage, rent, bills), do you have any debts, and who relies on your income?

As a general rule of thumb, most insurers will let you cover up to 70% of your pre-tax income. A financial adviser can help you do a proper needs analysis, getting down to the exact figure you'd need to keep your household running smoothly if you couldn't work. This ensures you're not paying for too much cover, or worse, finding yourself short when you need it most.

At Wealth Collective, our Protection Plus service is all about giving you this kind of clarity. We help you build a financial safety net that fits your life perfectly. Book a complimentary initial call with our team to make sure your protection strategy is doing exactly what you need it to.