Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Ever looked at your payslip and felt a pang of frustration seeing how much tax comes out? It’s a common feeling. But what if you could shift your perspective? Instead of seeing tax as an unavoidable deduction, think of it as a financial system with rules you can learn and use to your advantage.

That's the difference between simply paying tax and actively engaging in tax planning.

Your Guide to Smarter Taxation and Tax Planning

This guide is designed to cut through the jargon and explain Australian tax in plain English. Our goal is to show you how you can legally and ethically keep more of your money, so it can work for you and your future—not just the Australian Taxation Office (ATO).

Too many people treat tax as a fixed, non-negotiable expense. The reality is, with foresight and the right knowledge, your financial decisions can significantly lower your tax bill. This is what smart financial management looks like, and it’s a crucial step on the path to building real wealth.

Moving From Complexity to Clarity

Good tax planning isn't about exploiting obscure loopholes. It's about being deliberate with your financial structure. It means looking at the whole picture—from your income and investments to your business and retirement savings—and ensuring it’s all set up as tax-efficiently as possible.

The core ideas are surprisingly straightforward:

- Reduce your taxable income using legitimate deductions and strategies like salary sacrificing into super.

- Utilise low-tax environments like your superannuation fund, which is taxed at a much lower rate than your personal income.

- Claim all available tax offsets, which are valuable because they reduce your tax bill dollar-for-dollar.

- Time your financial decisions by, for example, deferring income to a future financial year or bringing forward deductible expenses.

At Wealth Collective, we don’t see tax planning as an add-on; it's the foundation of any solid financial plan. We ensure every financial decision is made with your tax position in mind, a core part of our process.

Whether you're starting your career, running a business, or heading into retirement, these principles apply. Our process is designed to bring you from a place of uncertainty to one of confidence.

This guide provides the foundational knowledge to start taking control. When you're ready for a plan tailored specifically to you, booking an initial call with us is the perfect first step toward putting your money to work.

Decoding the Australian Tax System

Let's be honest: paying tax is nobody's favourite activity. But to make sure you aren't paying more than your fair share, you first need to understand the rules. The Australian tax system might seem complex, but its purpose is simple: funding essential services we all rely on, from hospitals and schools to our roads and social security.

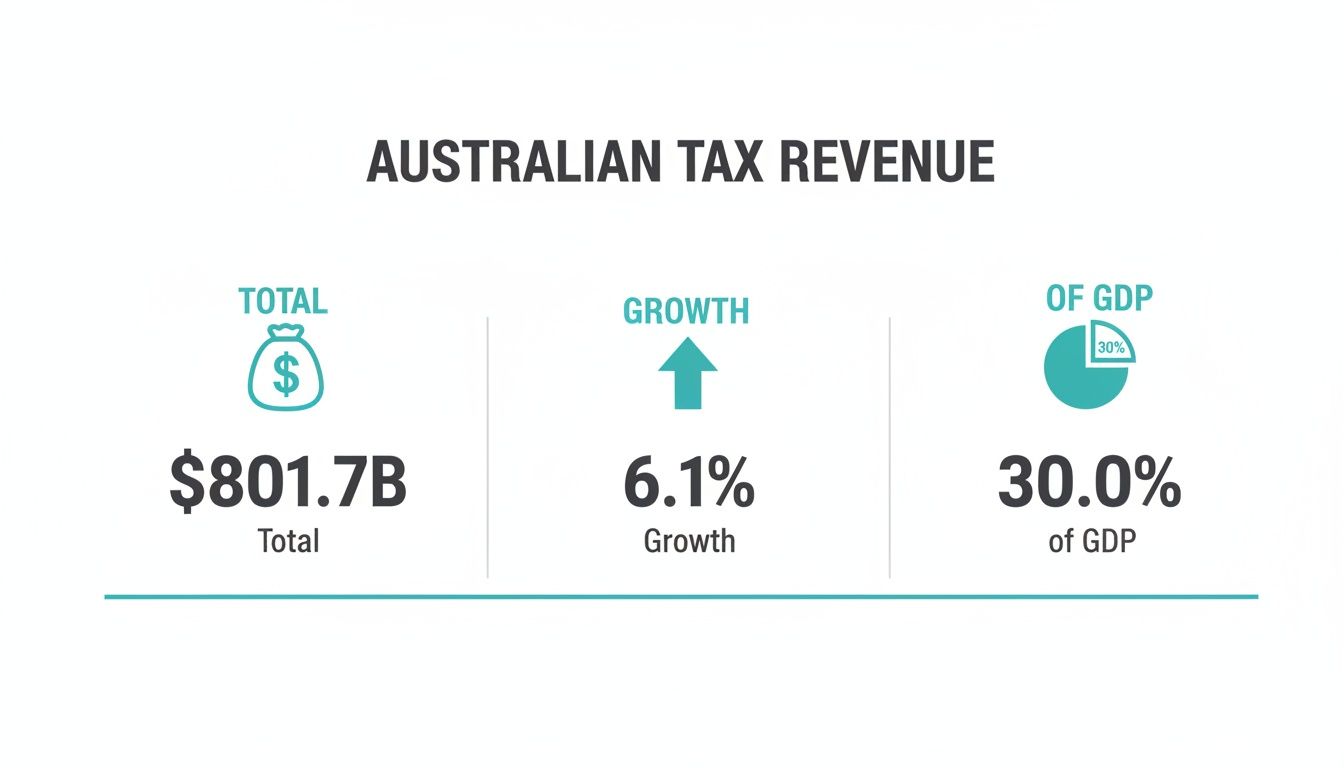

Understanding the fundamentals is the first step toward smart, effective tax planning. The stakes are high. In the 2023-24 financial year, Australia’s total tax revenue hit a staggering $801.7 billion, or 30.0% of GDP. You can see the full breakdown in the latest taxation revenue data from the Australian Bureau of Statistics. For the pre-retirees and retirees we work with, that figure highlights just how much proactive planning can impact your final retirement outcome.

Our Progressive Tax System Explained

At its core, Australia's income tax system is "progressive." The best way to picture it is like a series of buckets. Your first chunk of earnings goes into the first bucket, which is taxed at the lowest rate—or not at all, thanks to the tax-free threshold.

Once that bucket is full, any extra income spills into the next one, which gets taxed at a slightly higher rate. This continues for each dollar you earn, with each new bucket attracting a progressively higher tax rate.

This layered approach means your entire income is never taxed at your highest rate—a common misconception. Only the portion of your income that falls into a specific bracket is taxed at that rate, which is fantastic news for tax planning.

This structure is precisely why strategic tax planning is so powerful. It’s not about finding loopholes; it’s about legally arranging your financial affairs to keep as much of your money in those lower-taxed buckets as possible.

Key Terms You Need to Know

To get comfortable with tax planning, you need to speak the language. Here are three crucial terms:

- Taxable Income: This isn't just your salary. It's your assessable income (everything you earn) minus any allowable deductions. The primary goal of most tax planning strategies is to reduce this figure.

- Marginal Tax Rate: This is the tax you'll pay on the next dollar you earn. It’s the rate of the highest "bucket" your income spills into. Knowing this number is vital because it tells you the exact value of every dollar you can claim as a deduction.

- Tax Deductions: These are specific, allowable expenses you can claim to reduce your taxable income. For every $1 you claim, your tax bill drops by your marginal tax rate (e.g., 32.5 cents, 37 cents, etc.).

Grasping these ideas is the first step in shifting from being a passive taxpayer to an active financial architect. When you're ready to put this knowledge into practice, our team can help build a clear strategy that fits your life. Why not book a free, no-obligation initial call to see how we can help?

The Key Taxes Every Australian Should Understand

To get smart about tax planning, you first need to get familiar with the landscape. While the Australian tax system can seem complex, most of us are really only dealing with three major taxes that have the biggest impact on our financial lives.

Understanding how each one works is the first step. It’s how you identify where your money is going and, more importantly, where you can find opportunities to keep more of it. Let’s break them down.

Income Tax and the Silent Sting of Bracket Creep

Income tax is the big one—it’s what the government takes from your paycheque and the main way it funds public services. As we’ve mentioned, Australia uses a progressive system. This means the more you earn, the higher the rate you pay on each additional dollar.

But there's a sneaky phenomenon at play here called bracket creep. This happens when inflation or a pay rise pushes your income into a higher tax bracket. Suddenly, you’re paying a larger chunk of your earnings to the tax office, even if your real spending power hasn’t increased. It’s a slow, quiet drain on your take-home pay.

To put this in perspective, personal income tax is Australia’s single largest revenue source, expected to account for 56% of all Commonwealth taxes by 2024-25. A big reason for this is bracket creep, as more people get pushed into the higher 37% and 45% tax brackets. You can dig deeper into this trend in the Treasury’s detailed analysis of Australia’s tax system.

Here's a look at the marginal tax rates for the upcoming 2025-2026 financial year, which shows how this progressive system is structured.

Australian Income Tax Brackets for 2025-2026

| Taxable Income | Tax on this Income |

|---|---|

| $0 – $18,200 | Nil |

| $18,201 – $45,000 | 19 cents for each $1 over $18,200 |

| $45,001 – $135,000 | $5,092 plus 30 cents for each $1 over $45,000 |

| $135,001 – $190,000 | $32,092 plus 37 cents for each $1 over $135,000 |

| $190,001 and over | $52,442 plus 45 cents for each $1 over $190,000 |

As you can see, the tax you pay increases in stages as your income rises, rather than one flat rate being applied to everything you earn.

Capital Gains Tax and the 50% Discount

Next up is Capital Gains Tax (CGT). This isn’t a separate tax but is actually part of your income tax. A "capital gain" occurs when you sell an asset—like shares, an investment property, or cryptocurrency—for more than you paid. That profit is then added to your income for the year and taxed at your marginal rate.

But here’s the most important rule to remember with CGT: the 50% discount.

If you hold an asset for more than 12 months before selling, you only have to pay tax on half of the gain.

This single strategy is a cornerstone of smart investing. Simply timing the sale of your assets can have a massive impact on your after-tax returns. It’s also worth noting there are key exemptions, like the main residence exemption for your family home, which can shield you from CGT altogether.

The scale of tax revenue collected from income and capital gains shows just how much of an impact these have on the national economy and your own pocket.

The steady growth in this revenue highlights why being strategic with your tax is so crucial.

Superannuation: The Tax-Effective Powerhouse

Finally, we come to superannuation. Without a doubt, super is Australia’s most powerful vehicle for tax-effective wealth creation. The entire system is designed with tax incentives to encourage us to save for retirement.

Super’s power comes from three incredible tax advantages:

- Low Tax on Contributions: Money going into your super (like your employer's payments or salary sacrifice contributions) is generally taxed at just 15%. For most people, that’s a huge discount compared to their personal income tax rate.

- Low Tax on Earnings: Investment returns inside your super fund are also taxed at a maximum of 15%. This allows your money to compound much faster than it could if you were investing personally.

- Tax-Free Retirement Income: Here's the real prize. Once you reach preservation age (usually 60) and retire, any money you draw from your super as an income stream is completely tax-free.

Understanding how to use these three pillars—income tax, CGT, and super—is the key to shifting from just earning money to actively building wealth. It’s not about what you make, but what you get to keep.

Smart Tax Moves for Every Stage of Your Life

Knowing the rules of tax is one thing. Making them work for you is another entirely. The most effective taxation and tax planning isn't about a single magic bullet; it’s about choosing the right strategies for your stage of life.

Your financial world looks very different in your 20s than it does in your 50s. As your priorities shift, so should your tax strategy. What works for a graduate is miles away from what a pre-retiree or small business owner should be doing.

Let's break down practical strategies that align with your personal journey.

For Young Professionals and Growing Families

When you're building a career or starting a family, it often feels like every dollar is spoken for. The goal here is simple: build powerful financial habits and use straightforward strategies to make your money work harder.

Two of the most impactful moves you can make are:

- Salary Sacrifice into Super: This is a brilliant way to get ahead. You arrange for your employer to send a slice of your pre-tax pay straight to your super. These contributions are typically taxed at just 15%, a huge discount compared to your income tax rate. It’s a win-win: you pay less tax now and boost your retirement savings. For a deep dive, check out our complete guide to salary sacrifice.

- Claim Every Deduction You're Entitled To: Don't give the tax office a cent more than you have to. Meticulously track every work-related expense, from professional development courses and tools of the trade to home office running costs. Each dollar you claim lowers your taxable income, leaving more money in your pocket.

For High-Income Earners

As your career progresses and your income climbs into higher tax brackets, tax becomes a significant drag on your wealth-building ability. This is where smart, structured tax planning becomes non-negotiable. For high earners, we look beyond the basics to manage tax exposure and protect assets.

While Australia’s overall tax take is lower than many developed nations, our system is heavily reliant on personal income tax. This means high earners who don't plan ahead can get hit hard by our progressive rates, making proactive planning incredibly valuable.

For perspective, Australia's tax-to-GDP ratio was 29.4% in 2022, below the OECD average of 34.0%, largely because we lack direct social security levies. However, this is balanced by our heavy reliance on income taxes. You can see the full OECD breakdown for Australia here.

This is where strategies like these come into play:

- Family Trusts: These can be an excellent way to hold income-producing assets, giving you the flexibility to distribute income among family members in a tax-effective manner, often by streaming it to those on lower tax brackets.

- Maximising Concessional Contributions: It’s crucial to take full advantage of the annual cap on pre-tax super contributions. This is your most direct route to shifting money from the high-tax world into the much friendlier 15% tax environment of super.

For Pre-Retirees

As retirement appears on the horizon, your financial focus pivots. The goal is to preserve the wealth you've built and engineer a tax-efficient, or even tax-free, income stream for your post-work years. The years leading up to retirement are your last, best chance to turbo-charge your super.

- Transition to Retirement (TTR) Strategy: This strategy allows you to start an income stream from your super while still working (usually part-time). By combining a TTR with salary sacrificing, you can often reduce income tax and boost super contributions simultaneously.

- Tax-Deductible Personal Contributions: Did you receive a bonus or sell an investment? You can make an after-tax contribution to your super and then claim it as a tax deduction. It’s a powerful move to slash your taxable income for that year while adding a lump sum to your retirement nest egg.

For Small Business Owners

Running your own business offers unique challenges and opportunities for smart tax planning. The right decisions around structure and strategy can have a massive impact on your business's profitability and your personal wealth. Getting the foundations right is everything.

We often guide business owners on:

- The Instant Asset Write-Off: This is a fantastic lever for managing cash flow and tax. It allows eligible businesses to claim an immediate, full deduction for the cost of qualifying assets, rather than depreciating them slowly.

- Choosing the Right Business Structure: Whether you operate as a sole trader, partnership, company, or trust has profound consequences for your tax bill, personal liability, and asset protection. We help clients ensure their structure fits their long-term business and personal goals.

No matter your financial stage, being proactive about tax is essential. The real power comes from turning knowledge into a personalised action plan.

To see how these strategies could be tailored for your specific situation, book a complimentary initial call with our team today.

Common Tax Planning Mistakes to Avoid

When it comes to managing your tax, knowing what not to do is just as critical as knowing what to do. One simple misstep can undo good work, shrink your returns, or even put you on the Australian Taxation Office (ATO)'s radar.

Avoiding these common traps is a huge part of good financial housekeeping. Let's walk through some of the classic blunders we see and why getting a second opinion can be so valuable.

Claiming Deductions Without Records

This one is a classic. It’s easy to claim every possible work-related expense, but without the paperwork to back it up, you’re playing with fire. The ATO's data-matching technology gets smarter every year, making it simpler for them to flag claims that don't pass the sniff test.

A real-world example: A freelance designer had been claiming home office expenses for years. When the ATO sent a 'please explain' letter, she couldn't find receipts for her new computer or a logbook for her office usage. The result? Her claims were disallowed, and she was slapped with a hefty tax bill and penalties.

Think of good record-keeping as your insurance policy. Simply saving digital receipts and maintaining a clear logbook can protect you from a world of financial pain.

Accidentally Triggering a CGT Event

Capital Gains Tax (CGT) is a genuine minefield, and it’s surprisingly easy to trigger a taxable event without realising. Something as simple as transferring an asset to a family member, selling shares to rebalance your portfolio, or even moving out of your family home and renting it out can trigger CGT.

A cautionary tale: An individual owned an investment property for several years. To help his son onto the property ladder, he transferred the title to him for a token amount. He didn't realise the ATO views this as a 'disposal' at full market value, creating a significant capital gain and a surprise tax bill he was completely unprepared for.

The Superannuation Death Benefit Tax Shock

Most of us know that super is a fantastic, tax-effective vehicle during our lifetime. It's also tax-free when paid to a 'tax dependant' (like a spouse or young child) when you pass away. But here’s the kicker that catches so many families by surprise.

When your super is paid to a non-dependant—like an adult, financially independent child—the taxable portion of that money can be taxed at rates of up to 17% or even 32%.

How this plays out: After her father passed away, his adult daughter received his superannuation balance. She was shocked to discover a huge chunk was wiped out by tax simply because she wasn't classed as a dependant. With forward-thinking estate planning, her father could have structured things to dramatically reduce or eliminate that tax bill.

These examples show how easily you can find yourself in a costly mess. Effective tax planning isn't just about finding opportunities—it’s about spotting risks before they become problems.

If you’re unsure about any part of your tax strategy, it’s always best to check. Book a free introductory call with our team. We're here to provide clarity and help you sidestep these common pitfalls.

When to Partner with a Financial Adviser

For many people, lodging their own tax return is perfectly fine. If your financial life is simple, good software can get the job done. But there comes a point where professional advice stops being a cost and starts becoming a powerful investment.

This is the shift from simply doing your tax to proactively planning your financial life to build and protect your wealth. Knowing when you’ve hit that tipping point is a crucial step on your financial journey.

Key Triggers for Seeking Expert Advice

Going it alone with tax gets riskier as your world gets bigger. Certain life events are a clear sign that it’s time to work with an adviser.

- Approaching Retirement: This is the big one. You have one shot at structuring your super, investments, and other assets to create a tax-effective income stream that needs to last for decades. Getting this right is non-negotiable.

- Managing Multiple Investments: Once you start adding shares, an investment property, or other assets, the tax gets complicated, fast. An adviser can help manage Capital Gains Tax, ensure you're claiming every legitimate expense, and structure your portfolio for the best after-tax returns.

- Receiving an Inheritance: A sudden inheritance is a wonderful thing, but it can also create tax and structural complications. Professional advice is essential to integrate those new assets smoothly without a surprise tax bill.

- Starting or Growing a Business: As a business owner, you’re playing a different ball game. An adviser can guide you on the best structure (sole trader, company, trust), help you manage cash flow, and ensure you’re taking full advantage of business-specific tax concessions.

A financial adviser's job is to connect all the dots. We don't just look at tax in a vacuum; we weave it into your investment, debt, and retirement goals so every part of your financial life works together to move you forward.

At Wealth Collective, our process is built to make this transition simple. We get to know you and your situation first, then build a clear, actionable plan. Our Guided Growth and Retirement Roadmap services are designed specifically for these more complex life stages, turning tax from a chore into a strategic tool. Figuring out how to choose the right financial adviser is your first step towards a successful financial life.

If any of these situations sound familiar, it’s probably time to see what’s possible. Book a complimentary initial call to see how our straightforward approach can bring clarity to your finances.

Your Tax Planning Questions Answered

Even after getting a handle on the fundamentals, the world of tax can still feel like a maze. To help clear things up, we've answered some of the most common questions we hear.

What’s the Difference Between Tax Avoidance and Tax Evasion?

This is a big one, and it’s crucial to be clear on the distinction.

Tax avoidance is using the rules to legally reduce the amount of tax you pay. It's the whole point of smart tax planning. Think of strategies like salary sacrificing into super or timing the sale of an asset to qualify for the Capital Gains Tax discount. It’s all perfectly legal and above board.

Tax evasion, however, is breaking the law. This involves deliberately deceiving the ATO, like not declaring cash income or claiming deductions you know you're not entitled to. The ATO's data-matching is incredibly sharp, and the consequences are serious—from massive fines to jail time. At Wealth Collective, our advice is always focused on legitimate tax minimisation, ensuring your strategy is both effective and compliant.

Can I Handle My Own Tax Planning Without an Adviser?

Absolutely. If your financial life is straightforward—say, one job and a handful of simple deductions—you can manage your own tax return. But lodging a return is one thing; genuine taxation and tax planning is another. It’s about looking ahead and structuring your finances to minimise tax over your entire lifetime.

As your world expands with property investments, a growing family, a higher salary, or retirement, the value of professional advice kicks in. A good financial adviser can spot opportunities you'd likely miss and weave them into a single, cohesive plan to build and protect your wealth more effectively.

An expert doesn’t just fill out forms; they build a strategy. They connect the dots between your investments, super, and retirement goals to ensure every decision is tax-effective.

How Does Superannuation Help Reduce My Tax?

Superannuation is Australia’s most effective tax-planning vehicle. It's a triple threat when it comes to saving you tax.

- Low Tax on Contributions: Concessional contributions (like your employer’s payments or salary sacrifice) are taxed at just 15%. For most people, that’s a huge discount compared to their income tax rate.

- Low Tax on Earnings: Inside the super fund, investment returns are also taxed at a low maximum rate of 15%. This allows your nest egg to compound much faster than it could elsewhere.

- Tax-Free Retirement Income: Here's the ultimate payoff. Once you turn 60 and retire, every dollar you draw from your super as an income stream is completely tax-free.

This powerful trifecta is why super is a cornerstone of the Retirement Roadmap service we offer at Wealth Collective. It’s all about building a future that’s not just secure, but also incredibly tax-efficient.

Is Negative Gearing Still a Good Tax Strategy?

Negative gearing occurs when the running costs of an investment (like interest and repairs on a property) are more than the rental income it generates. You can then use that "net rental loss" to reduce your taxable income.

It can still be a worthwhile strategy, especially for higher-income earners. But—and this is a big but—it’s not a magic bullet. The entire plan hinges on the hope that the property's value will grow enough long-term to more than make up for the running losses.

Getting professional advice here is crucial. You need to be sure the investment itself is a smart one and that you can comfortably afford the cash shortfall. This kind of careful analysis is a key part of our Guided Growth process.

Getting your head around the details of taxation and tax planning is the bedrock of a strong financial future. The strategies we've touched on here are just the tip of the iceberg. At Wealth Collective, our specialty is taking the complexity out of tax and turning it into a clear, personalised plan for you.

To see how we can help you keep more of your hard-earned money and put it to work for your goals, book a complimentary initial call with our team today at https://wealthcollective.co.