Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Imagine your Will not just as a final instruction, but as a blueprint for a secure financial structure you leave behind for your family. That's what a testamentary trust is all about. It’s a trust created by your Will that only springs to life after you’re gone, designed to manage and protect the assets you’ve worked so hard for.

So, What Exactly Is a Testamentary Trust?

Unlike a standard family trust you might set up during your lifetime, a testamentary trust isn't a separate, standalone document. Instead, it’s a series of carefully drafted clauses written directly into your last Will and testament.

Think of a basic Will as a simple handover—your assets go directly to your beneficiaries in a lump sum. A Will that includes a testamentary trust, on the other hand, creates a far more sophisticated arrangement. Instead of your beneficiaries receiving their inheritance outright, the assets are transferred into a trust you’ve designed. This trust is then managed by a person you’ve appointed (the trustee), all according to the rulebook you’ve set out in your Will.

A testamentary trust acts as a protective shield for your legacy. It holds and manages assets on behalf of your loved ones, safeguarding their inheritance from a range of risks while offering powerful financial benefits.

This structure delivers two major advantages that a simple Will just can't offer:

- Serious Asset Protection: It effectively quarantines the inheritance from a beneficiary's personal creditors, business risks, or even claims that might arise from a future relationship breakdown.

- Major Tax Efficiencies: It gives the trustee the flexibility to distribute income to family members on lower tax rates, which can dramatically reduce the overall tax bill on the inheritance's investment earnings.

The Game-Changing Tax Advantage for Children

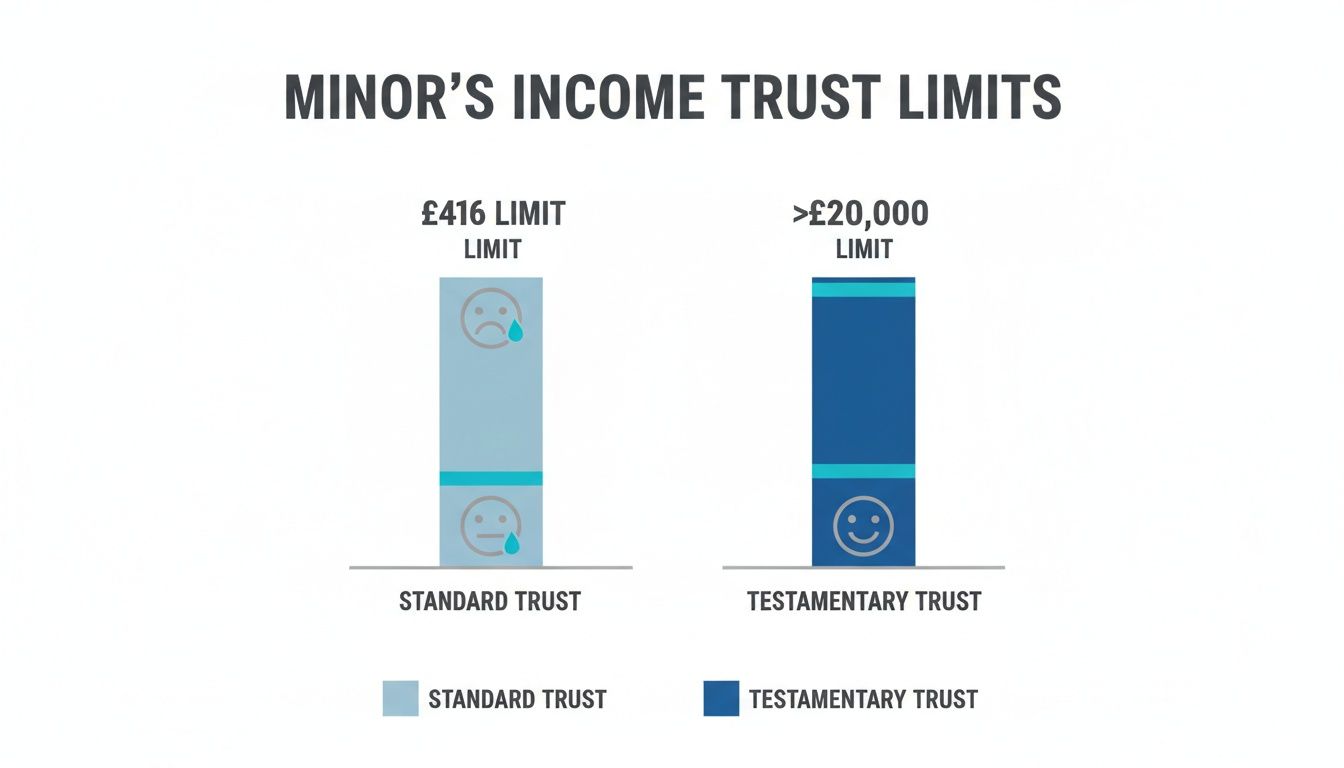

One of the most compelling reasons people choose a testamentary trust is the unique tax treatment for beneficiaries under 18. Normally, any income over $416 distributed to a minor from a regular family trust is hit with penalty tax rates.

But with a testamentary trust, income distributions to children are treated as 'excepted income'. This means they are taxed at normal adult marginal rates. For the 2026 financial year, this gives each child beneficiary an effective tax-free threshold of $18,200—a massive advantage. You can discover more about the tax effectiveness of testamentary trusts and see why so many Australian families use them.

Before we move on, here's a quick summary of the key features.

Testamentary Trust At a Glance

| Feature | Description |

|---|---|

| Creation | Established by clauses within a last Will and testament. |

| Activation | Comes into existence only after the Will-maker's death. |

| Asset Holding | Assets are held in the trust for beneficiaries, not given directly to them. |

| Control | Managed by a trustee, who must follow the rules set out in the Will. |

| Key Benefit 1 | Provides strong asset protection from creditors and legal claims. |

| Key Benefit 2 | Offers significant tax advantages, especially for minor beneficiaries. |

Ultimately, setting up a testamentary trust is an act of foresight. It’s about making a strategic choice to provide lasting security and maximise the value of the legacy you pass on. At Wealth Collective, we see it as an essential conversation for anyone serious about their estate plan. Our role is to work alongside specialist estate planning lawyers to make sure this powerful tool fits perfectly with your family's needs and financial goals.

The best first step is often just a conversation to see if this is the right path for you. You can book a complimentary initial call with our team to explore your options with no obligation.

Unlocking Powerful Tax Savings for Your Beneficiaries

Beyond protecting your assets, one of the most compelling reasons families in Australia set up a testamentary trust is the incredible potential for tax savings. This isn't just a minor perk; it can fundamentally change the value of the inheritance you leave behind, helping your legacy grow for your loved ones rather than being chipped away by tax.

The secret lies in how the Australian Taxation Office (ATO) treats income earned by the trust’s assets. It opens up a powerful strategy for distributing that income to your family in a way that dramatically lowers the overall tax bill, especially if you have young children or grandchildren.

This unique tax treatment is precisely what makes a testamentary trust such a cornerstone of smart estate planning.

The Magic of Excepted Trust Income

So, how does this actually work?

Normally, if you have a standard family trust, any income you distribute to a child under 18 gets hit with huge penalty tax rates. The tax-free threshold is a tiny $416 a year. Anything over that is taxed at the highest marginal rate (currently 45%) plus levies. This is deliberately designed to stop adults from using their kids to dodge tax.

But a testamentary trust is a different story.

Income distributed from a testamentary trust to a minor is called ‘excepted trust income’. Because of this special classification, the child is taxed at the same marginal rates as any adult.

This is a complete game-changer. It means each child or grandchild under 18 can receive up to $18,200 in income completely tax-free each year. That's a world away from the measly $416 cap you'd get with other trusts.

This image shows just how stark the difference is.

As you can see, the tax outcome is vastly better, unlocking a significant amount of money that would have otherwise gone straight to the tax office.

A Real-World Savings Scenario

Let's put this into perspective with a real-world example. Imagine you pass away, leaving behind an investment portfolio that generates $50,000 of income each year for your surviving partner and your two young children.

Without a Testamentary Trust: If your partner simply receives that $50,000 on top of their own salary, it could easily push them into a high tax bracket. A big chunk of that inheritance income would be lost to tax, year after year.

With a Testamentary Trust: The trustee has the flexibility to split this $50,000 income. They could decide to distribute $20,000 to each of the two children and the remaining $10,000 to your partner. Most of the children's income would be tax-free, and your partner pays much less tax on their smaller distribution.

The ability to split income saves the family thousands of dollars every single year. Those savings can then be put to work—reinvested to grow the inheritance, used to pay for school fees, cover university costs, or even build a deposit for a first home. This is a perfect example of our 'Guided Growth' philosophy at Wealth Collective, where intelligent planning helps create lasting wealth across generations. Our approach to taxation and tax planning is all about structuring your assets for the best possible long-term outcome. By working with our team and specialist lawyers, we help ensure your estate plan is a dynamic tool for your family's future, not just a static document.

Protecting Your Legacy from Financial Risks

While the tax benefits of a testamentary trust are impressive, they are only half the story. The other, equally crucial, benefit is asset protection. Think of it as a financial fortress you build around your family's inheritance, safeguarding the wealth you’ve worked so hard for against risks your beneficiaries might face in the future.

For business owners, professionals, and anyone who wants to ensure their legacy lasts, this protection is often the most compelling reason to include a testamentary trust in their will.

The concept behind it is straightforward but incredibly powerful. Assets are held in the trust itself, not in your beneficiary's personal name. This small distinction creates a massive legal firewall, separating the inheritance from their personal financial affairs and shielding it from claims.

A Shield Against Life's Uncertainties

So, where does this protection really matter? Let's look at a few real-world scenarios where a testamentary trust can be a game-changer.

- Relationship Breakdowns: If a beneficiary goes through a divorce or separation, assets held securely within a testamentary trust are generally not considered part of the marital asset pool by the Family Court. This can ensure your child’s inheritance remains with them, not split with an ex-partner.

- Bankruptcy or Creditors: What if your beneficiary faces financial trouble, or their business fails? The inheritance held in the trust is typically safe and beyond the reach of creditors. For professionals in high-risk industries or small business owners, this is an absolutely essential feature.

- Vulnerable Beneficiaries: Sometimes, a loved one might not be equipped to handle a large inheritance all at once. A trust allows you to appoint a trustee to manage the funds responsibly, protecting a beneficiary from poor decisions, financial predators, or their own inexperience.

By placing assets into a trust, you are creating a legal separation between the inheritance and your beneficiary's personal liabilities. This quarantine is what protects the legacy you've built from being eroded by external events.

Control and Longevity for Your Legacy

A testamentary trust also gives you a remarkable degree of control over how your wealth is managed long after you're gone. You set the rules in your Will, and the trustee must follow them, ensuring your wishes are respected for years to come.

This long-term control makes testamentary trusts a cornerstone of legacy planning. You can see how these structures provide lasting security in this comprehensive guide on testamentary trusts.

Building a Multi-Generational Plan

In most Australian states, a testamentary trust can operate for up to 80 years. This incredible lifespan means the trust can be structured to support not just your children, but potentially your grandchildren and even great-grandchildren. It’s a vehicle for creating a truly lasting, multi-generational legacy.

This is where a well-designed estate plan shows its true value. It's not just about passing on money; it's about building a protective framework for your family's financial future. This philosophy is at the heart of Wealth Collective’s ‘Protection Plus’ service offering, where we focus on creating robust strategies that defend your wealth against life’s uncertainties.

Integrating instruments like testamentary trusts is a key part of that defence. It also works hand-in-hand with other protective measures, which is why you may find our guide on how life insurance for families plays a vital role in this protective strategy to be a useful read.

By working with our team and our network of specialist estate planning lawyers, you can design a plan that doesn't just transfer wealth—it protects it for generations. The first step is a simple, no-obligation chat to see how these powerful strategies could work for you.

How to Set Up a Testamentary Trust in Your Will

First, let's clear up a common misconception. A testamentary trust isn't a separate, standalone document you have to sign and file away somewhere. It’s actually built directly into your Will through a series of carefully written clauses.

These clauses spring into action after you pass away, creating the exact structure you designed to protect your assets and your loved ones. Crafting these clauses requires specialist legal advice and some key decisions on your part.

The Core Decisions You Will Make

When you sit down with an estate planning lawyer, the conversation will centre on a few key instructions. These are the building blocks that will define how your trust works for years, or even decades, to come.

You’ll need to have clear answers for:

- Appointing a Trustee: Who will be in charge? This is, without a doubt, the most important decision you'll make.

- Defining the Beneficiaries: Who is the trust for? This can be your children, grandchildren, or even great-grandchildren who aren't born yet.

- Outlining Trustee Powers: What are the rules of the game? You need to set clear boundaries on what the trustee can and can't do with the assets.

Getting these details right is everything. Any ambiguity can lead to family arguments, confusion, or expensive court battles down the track.

Choosing the Right Trustee

Picking a trustee is a choice that will echo for a long time. This person or company will have significant control over your legacy, so they need to be someone you trust implicitly—someone with a good head for finances and the ability to be fair.

You really have three main options:

- A Family Member or Friend: This is often a spouse, a responsible adult child, or a trusted sibling. It can work wonderfully if you have the right person, but be warned, it can also strain family relationships.

- A Professional Trustee: Think of an accountant, a lawyer, or a specialised private trustee company. They bring impartiality and deep expertise to the table, but their services come with professional fees.

- A Combination of Both: You can appoint a family member to act alongside a professional. This approach often gives you the best of both worlds: the personal touch of a loved one, backed by the experience and oversight of an expert.

The trustee's job is to manage the trust's assets for the good of all beneficiaries, all while following the specific rules you've laid out in your will. It's a role with an enormous amount of responsibility.

The Necessity of Specialist Advice

Let me be blunt: this is not a DIY job. Setting up a Will with a testamentary trust is complex. It pulls together threads from succession law, tax legislation, bankruptcy rules, and even family law. It’s incredibly easy to make a small mistake that could unravel the entire structure or create a tax nightmare down the road.

This is precisely where the Wealth Collective process makes a difference. We work hand-in-glove with your estate planning lawyer, ensuring the trust they draft aligns perfectly with your financial goals. We help you map out the financial strategy, and the lawyer ensures it's legally rock-solid. This teamwork turns your Will from a simple document into a dynamic part of your long-term wealth plan.

Having a Will is non-negotiable, but a poorly drafted one can be worse than having none at all. You can learn more about the risks in our guide on what happens if you die without a will in Australia. Booking a call with our team is the best first step you can take toward getting this right.

Real-Life Scenarios for Australian Families

The real value of a testamentary trust becomes clear when you see how it solves genuine problems for everyday people. Let's walk through a few common scenarios we see with our clients.

Each of these stories highlights a challenge that a basic Will simply can't address on its own. But with the right estate planning, a testamentary trust can provide an elegant solution.

Securing the Future for Young Children

Let's start with Sarah and Tom, a professional couple with two kids, aged 8 and 11. Their biggest worry was what would happen if they both passed away unexpectedly. Under a standard Will, their children would receive their entire estate—the house, investments, everything—the moment they turned 18.

The thought of two teenagers suddenly coming into a large sum of money was terrifying. They wanted their children to be financially secure, but not at the expense of good judgment.

This is where a testamentary trust was the perfect fit. In their Wills, they directed their estate into a trust for the children and appointed a trusted trustee to manage the funds. This trustee could then pay for school fees, health costs, and living expenses as the kids grew up. Sarah and Tom specified that their children would only get full control of the remaining capital when they were older and more mature, at ages 25 and 30.

For families with young children, a testamentary trust isn't just about financial strategy; it's about providing parental guidance from beyond the grave, ensuring your wealth supports their future instead of derailing it.

This setup not only protects the inheritance itself, but it’s also incredibly tax-effective. Any income earned by the trust's investments can be distributed to the children each year, with each child able to use their own tax-free threshold, saving a huge amount in tax.

Protecting Hard-Earned Business Assets

Now, think about someone like David, who owns a successful business. He's poured his life into building the company and wants his adult son, who has his own business ventures, to one day benefit from all that hard work.

David’s number one concern was asset protection. He knew that if he simply left his inheritance to his son in a Will, those assets would be legally owned by his son personally. If his son’s own business ever ran into trouble or was sued, David’s hard-earned legacy could be seized by creditors.

A testamentary trust was the answer. By using one, David created a protective shield around the inheritance. The assets are held by the trust for his son’s benefit, not in his son's own name. This means that if his son were ever to face bankruptcy or a lawsuit, those inherited assets would be untouchable.

It’s this peace of mind that David was really after. He can rest easy knowing his legacy will be there to support his son and grandchildren, no matter what financial storms his son might face down the track.

Ensuring Fairness in a Blended Family

Finally, we have Jane and Michael. They’re in their second marriage and have a blended family—Jane has two children from her first marriage, and Michael has one. Their goal is to make sure that if one of them passes away, the surviving partner is taken care of, but that ultimately, all the children are treated fairly.

A simple Will here is fraught with risk. If Jane left everything to Michael outright, there’s no legal guarantee her children would ever see a dollar of that inheritance, especially if Michael were to remarry or change his own Will later on.

A testamentary trust provides a brilliant solution to this complex family dynamic. Jane’s Will can establish a trust to hold her assets, making Michael the primary beneficiary for his lifetime. This gives him access to the income and funds he needs to live comfortably. But—and this is the crucial part—the Will dictates that after Michael passes away, the remaining capital in the trust must be distributed to Jane's two children.

This structure looks after Michael while ring-fencing Jane's assets for her own kids. It removes ambiguity, prevents potential family conflicts, and ensures her wishes are carried out exactly as she intended.

As you can see, a testamentary trust isn't a rigid, off-the-shelf product. It's a highly flexible and powerful tool that can be shaped to solve your family's specific challenges. The team at Wealth Collective, working with expert estate planning lawyers, helps design plans that truly reflect what's important to you.

To see how these strategies might work for your own family, we invite you to book a complimentary 10-minute call with us. It’s a simple, no-obligation first step toward securing your legacy.

So, What's the Next Step for Your Family's Future?

Getting your head around testamentary trusts is one thing; putting a plan into action is what really counts. We've walked through how these trusts can be a game-changer for protecting your assets, saving on tax, and making sure your wishes are carried out. These aren't just abstract ideas—they mean real, tangible security for the people you love.

Let's be upfront: setting up a testamentary trust is more involved and costs more initially than a basic Will. It’s natural to wonder if it's worth it. Think of it less as a cost and more as an investment in your family's future security. The long-term asset protection and potential tax savings often dwarf the upfront legal fees, ensuring the wealth you’ve worked so hard to build actually ends up where you intend it.

A Trust is Only One Piece of the Puzzle

This is where having the right team around you is crucial. A testamentary trust can't just be tacked on as an afterthought; it needs to be carefully woven into your entire financial world to do its job properly.

That’s why we work so closely with specialist estate planning lawyers. We take care of the financial strategy, and they handle the legal drafting, making sure the two are perfectly in sync.

This is a core part of the Wealth Collective process. We connect the dots between the trust and your bigger life goals. For instance, are you:

- Building a foundation for the next generation? We'll make sure the trust strategy aligns with our Guided Growth framework to foster smart, long-term wealth creation.

- Planning for a comfortable retirement? We'll align the trust with your Retirement Roadmap, ensuring it provides for a surviving partner while being as tax-effective as possible.

Our job is to cut through the complexity for you. We act as the bridge to the legal experts, translating your financial situation and your family's needs into a clear brief. This way, the Will and the trust inside it aren't just legally sound—they’re a perfect fit for your family.

A testamentary trust isn't just a legal document collecting dust in a safe. It's a living part of your financial plan. Our job is to make sure it works in concert with everything else you’ve built, protecting and growing it for the people who matter most.

Your Path Forward Starts with a Simple Conversation

Embarking on estate planning can feel like a huge, complicated task, but you don't have to do it alone. The best place to start is with a simple chat.

We invite you to book a complimentary 10-minute call with one of our advisers. There's no obligation whatsoever. It's just a chance for us to hear about your situation and for you to see how these strategies might work for you. Let's take that first decisive step together.

Frequently Asked Questions About Testamentary Trusts

When people first learn about testamentary trusts, a few key questions almost always come up. Let's get straight into the practical answers to the queries we hear most often from our clients.

How Much Does It Cost to Set Up?

There’s no sugarcoating it – a Will that includes a testamentary trust costs more to prepare than a simple one. But it's crucial to see this as a long-term investment in your family's financial security.

The initial legal fees are often a drop in the ocean compared to the powerful asset protection and significant tax savings a trust can provide down the track. In the long run, it can save your estate a substantial amount of money.

Can I Have More Than One Trust?

Definitely. In fact, it’s a very common strategy for a single Will to establish multiple testamentary trusts. You could, for instance, set up a separate, customised trust for each of your children. This allows for different investment approaches or distribution rules that are perfectly suited to their individual needs and circumstances.

A key strength of a testamentary trust is its protective shield. Assets held within the trust are generally not considered part of a beneficiary’s personal property in a Family Court settlement, helping safeguard their inheritance from being divided in a divorce.

Are They Useful If My Children Are Already Adults?

Yes, absolutely. Even if your children are financially independent adults, a testamentary trust is an incredibly powerful tool. Think of it as a safety net that can protect their inheritance from their own potential risks, like business creditors, bankruptcy, or a future marriage breakdown.

It also gives them, and in turn your grandchildren, access to far more effective tax-planning strategies, helping preserve the wealth you've built for another generation. This is a core part of our Guided Growth approach, where we focus on creating lasting, multi-generational security.

Understanding how these strategies fit into your broader financial life is the first step toward securing your legacy. At Wealth Collective, our team works alongside legal experts to ensure your estate plan is robust, effective, and perfectly tailored to your family.

Ready to take the next step? You can book a complimentary 10-minute call with our team to start the conversation.